Erebor Bank is one of the clearest early tests of whether a newly chartered U.S. bank can combine specialized commercial banking for frontier-technology companies with stablecoin-enabled payment infrastructure. Headquartered in Columbus, Ohio, the bank received final approval from the Office of the Comptroller of the Currency in February 2026, making it the first de novo national bank charter approved under the current administration.

By launch, Erebor had assembled roughly $625 million of initial capital, a notable increase from the approximately $275 million associated with the project around its preliminary approval stage in late 2025. The bank is FDIC-insured, built as a branchless 24/7 institution, and focused on serving companies and investors across sectors such as AI, crypto, defence, and advanced manufacturing.

According to regulatory filings and public statements, Erebor intends to offer deposit accounts, lending products, and payment infrastructure that connects traditional banking services with stablecoin and broader digital-asset functionality. Management has highlighted instant stablecoin-to-fiat conversion, always-on settlement rails, and, over time, the ability to support stablecoin issuance and redemption within a regulated banking framework.

On April 2, 2026, Sui Foundation said Erebor had added support for the Sui network, enabling stablecoin deposits and withdrawals for Erebor customers and making Sui one of only a small number of blockchains supported by the bank. The announcement provides one of the first public indications of how Erebor intends to connect its regulated banking infrastructure with onchain payment functionality. At this stage, however, it does not provide evidence of customer scale, transaction volume, or broader commercial adoption.

Partner Highlight

At insights4vc, we pay attention to teams that are not just shipping products, but shaping categories.

Moto is one of them. The company is building a premium card experience positioned as an alternative to traditional incumbents such as Amex, combining a high-end user interface with more modern financial infrastructure.

Moto is currently expanding access to a limited testing group. To explore it, contact: [email protected]

Founder and Context

The founding of Erebor is best understood through the historical product-building pattern of its principal shareholder, Palmer Luckey. Luckey’s track record, spanning Oculus VR and Anduril Industries, demonstrates a consistent focus on high-capital-intensity sectors where hardware, regulatory barriers, and government-adjacent ecosystems intersect.

In 2012, Luckey disrupted the nascent virtual reality market by focusing on the “last mile” of hardware integration - solving the latency and spatial tracking issues that had plagued VR for decades. His eventual $2 billion exit to Facebook (Meta) in 2014 was not merely a software success but a lesson in managing complex hardware supply chains and engineering-led R&D cycles. This experience is directly relevant to Erebor’s mission to underwrite physical assets like AI chips and robotics, which Luckey describes as “real things” often ignored by traditional financial services.

Luckey’s subsequent venture, Anduril Industries, applied a similar disruptive lens to the defense industrial base. By utilizing private venture capital to build defense systems and then selling them to the government on a “product” rather than “cost-plus” basis, Luckey established deep institutional relationships with the Department of Defense and the intelligence community. Erebor intends to leverage this posture. Luckey has explicitly stated that the bank will “work with the intelligence community from the very beginning” to prevent fraud, taking a preemptive compliance stance that contrasts with the reactive posture of legacy institutions.

Palmer Luckey: Why I Started My Own Bank (Source: TBPN)

Team and Backing

Erebor’s leadership includes Michael Hagedorn, President and former Wells Fargo regional banking executive; Owen Rapaport, Chief Executive Officer; and Jacob Hirshman, Chief Strategy Officer and Noah Pompan, Vice President of Growth, a founding GTM hire with prior experience in partnerships and ventures at MoonPay. The broader founding group, including Palmer Luckey, Rapaport, Hirshman, Trevor Capozza, and Aaron Pelz, combines engineering and product-building depth with meaningful compliance, legal, and financial-regulatory experience. Rapaport’s background is in crypto compliance through Aer Compliance, while Hirshman previously worked on Circle’s stablecoin initiatives and practiced law at Sullivan & Cromwell.

The founding investor base includes Joe Lonsdale’s 8VC, Thiel’s Founders Fund, Lux Capital, Andreessen Horowitz affiliates, and others. Collectively, these relationships give Erebor strong links across technology, finance, and policy circles, though the bank will ultimately be judged on operating execution rather than investor pedigree.

Luckey’s pattern is to spearhead tech ventures (VR, then defence, now finance). He is credible in deep-tech and defence circles, but a banking outsider. His partners (Hagedorn, Rapaport, Hirshman) have financial and crypto credentials. As observers note, Erebor’s brand partly relies on Luckey’s and Thiel’s reputations, but reputation is not a substitute for regulatory or operational track record. The bank will be scrutinised on its own terms as a regulated institution.

What Erebor Is

Erebor Bank is a full-service national bank. The OCC granted a preliminary conditional approval of its charter on 15 Oct 2025, marking it the first new national charter under the current administration. The FDIC approved its deposit-insurance application on 16 Dec 2025, and a final charter was issued in early Feb 2026. The bank is required to open within one year of its charter approval. It launched on 8 Feb 2026 with $625 million in initial capital.

Luckey has framed Erebor’s origin as a response both to SVB’s collapse and to what he sees as a lack of banks capable of underwriting or even understanding complex deep-tech and frontier-industry businesses.

Business Model

Under its charter, Erebor “will provide deposit and lending products” to businesses and individuals in the technology, payment systems, investment and defence industries, including virtual-currency market participants. In practice, management has said Erebor will focus on high-growth tech and deep-tech firms (AI startups, crypto/Blockchain companies, defence contractors, advanced manufacturers) and related venture funds, traders or wealthy founders. It aims to offer a full suite: operating accounts, treasury management, commercial credit (including loans secured by crypto or specialised assets), and cross-border payments. Unlike fintechs that depend on partner banks (e.g. Mercury, Brex), Erebor owns the charter and balance sheet.

Luckey has argued that controlling the charter was strategically necessary because dependence on third-party infrastructure would leave Erebor exposed to external deplatforming, policy pressure, and product constraints.

Stablecoin and Crypto Capabilities

A cornerstone of Erebor’s pitch is integrating stablecoins and blockchain rails. According to filings and interviews, Erebor will accept stablecoin deposits and support “instant, free” conversions between fiat and stablecoins (presumably settling trades on-chain). The bank says it will “mint and burn” stablecoins and even lend against crypto collateral. Its OCC charter explicitly permits it to hold small amounts of crypto assets on its own books to pay blockchain transaction (gas) fees – a notable compliance precedent (the OCC letter calls such crypto holdings “incidental” to banking). In summary, Erebor is best seen as a regulated, crypto‑aware commercial bank: it combines an insured deposit base and lending business with an embedded role in token payments and stablecoin flows.

Operations

The bank is built as a 24/7 digital institution with no physical branches. Its core processing system is being written from scratch by engineers in Luckey’s home region (Newport Beach, CA). According to public sources, Erebor will maintain at least a 12% Tier 1 leverage ratio for its first three years – a significantly higher buffer than typical banks. It also has a capital-call agreement to raise funds if it dips below “well-capitalized” levels. In essence, regulators have capped its leverage in recognition of the risk profile.

Products and Roadmap

Beyond the high-level plan above, specific products have not all been detailed publicly. In interviews, Erebor’s team speaks of “eliminating” the gap between on-chain and off-chain finance by offering regulated bank accounts that interface with stablecoins across all major blockchains. Early customer applications are expected from AI hardware firms, defence innovators, crypto exchanges and payment providers. There’s also talk of “partner programs” (omnibus/FBO accounts) to let crypto platforms integrate Erebor’s services. But as of writing, most product claims are from company presentations, not independently verified.

Why Erebor Exists

Erebor’s genesis is closely tied to the 2023 collapse of Silicon Valley Bank (SVB), which left many startups and VCs suddenly uninsured or without banking partners. Luckey and investors perceived a “structural vacuum” – the loss of specialist startup-focused banks. They argue that traditional banks had become too risk‑averse or slow, particularly for “hard-to-underwrite” startups with non‑standard assets (like defence contracts, AI hardware, or digital tokens). Management frequently cites the analogy of a “farmers’ bank for tech”: just as a rural lender understands tractors, Erebor aims to understand GPUs, aerospace R&D equipment and crypto treasury. By this logic, Erebor will approve loans and credit lines that big banks would deny or delay.

Crypto and DeFi Frictions

Parallel to the SVB gap, Erebor’s founders highlight pain points in the crypto economy. Traditional finance is disconnected from blockchain rails, forcing crypto firms to use multiple intermediaries. As one summary notes, crypto exchanges and protocols now “suffer from the lack of unified financial infrastructure,” often requiring “six hops” on-chain where legacy finance needs only one banking partner. Erebor posits that an insured bank that natively handles stablecoins can dramatically simplify these flows. Their vision is that every innovative company should be able to hold stablecoins alongside cash and move value 24/7 across chains without friction. This is a thesis: that on‑chain settlement and traditional banking can be bridged.

Credit/Treasury Needs

The management narrative emphasizes that today’s startups have complex treasury needs. They raise large rounds earlier and want debt financing and treasury services at high velocity. Moreover, some institutional investors (hedge funds, pensions) want to invest in crypto but lack the banking rails to do so efficiently. Erebor claims it can service both crypto-native clients and traditional VCs by being fully regulated while offering crypto rails.

Filling a Niche (Not a Given)

In reality, whether these gaps are genuine or partly promotional is open. Venture-backed firms do have new financing options (non-bank debt, crypto defi loans, etc), and some existing banks began courting tech niche even before SVB’s failure. Erebor’s founders clearly believe the existing institutions were insufficient. The fact they secured a full bank charter suggests regulators saw some merit in that view. Nonetheless, parts of Erebor’s origin story come from internal statements; independent evidence is limited to the timing (post-SVB) and the charter application text.

Market Gap and Problems Targeted

Erebor claims to address four critical frictions in the modern financial stack:

- Credit Access for Physical Assets: Traditional banks are comfortable lending against real estate or receivables. They are historically inept at valuing “GPU clusters” or “proprietary aerospace research”. Erebor’s model of “technical underwriting” informs credit decisions with a “deep engineering understanding” of these specific industrial assets.

- On-Chain/Off-Chain Fragmentation: Many tech firms must maintain separate relationships for fiat banking and stablecoin settlement. Erebor integrates these into a single “regulated balance sheet,” allowing for continuous liquidity without third-party middleware.

- 24/7 Settlement Needs: The legacy SWIFT and ACH systems operate on 1970s-era schedules. High-frequency tech businesses require 24/7/365 settlement, which Erebor provides via blockchain-based payment rails.

- Global Dollar Access for Innovation: High-growth international firms often face “de-banking” or extreme friction when seeking U.S. dollar exposure. Erebor targets these global customers through foreign correspondent relationships and a digital-first distribution model.

The “Farmers’ Bank” Analogy

Luckey frequently describes Erebor as a “farmers’ bank for technology”. This is a structural observation: a farmer and a founder both run capital-intensive businesses with long time horizons, uncertain returns, and “lumpy” revenue. Just as a rural bank understands that a rancher’s “runway” is measured in calving seasons, Erebor aims to understand that a defense-tech firm’s runway is measured in government testing cycles and hardware iterations.

Competitive Landscape

Erebor’s team has not formally published a list of competitors, so we infer its peers from industry context. The closest direct comparators (or precedents) are:

- Silicon Valley Bank (First Citizens) – Historically SVB was the flagship “innovation economy” bank. Its model (sector focus, founder relationships) was very similar to Erebor’s plan. After SVB’s failure, First Citizens took over, but it inherited losses and retains some tech clients. SVB/First Citizens represents the incumbent model of relationship banking for startups. Erebor is explicit about being the “new SVB” for crypto and deep tech.

- Signature Bank (defunct) – Before its collapse, Signature had aggressively courted crypto firms with real-time stablecoin payments (Signature’s on-chain “Signet” platform). It briefly occupied the niche Erebor is targeting in crypto. Its failure (March 2023) underscores risks of a crypto-heavy book. When it existed, Signature was the nearest analogue to Erebor’s crypto-friendly banking vision.

- Silvergate Bank (defunct) – Another regional bank that focused on crypto exchanges (e.g. Coinbase, etc.) and became heavily entangled with token settlements. Silvergate’s collapse (Mar 2023) similarly eliminated a crypto-bank option. Erebor may thus see an opportunity to replace Silvergate’s role in serving crypto firms.

- Mercury and Brex (fintech banks) – These are not banks but fintech neobanks targeting startups. They offer modern business accounts and API-driven treasury but do so via sponsor-charter banks, not their own. Mercury and Brex compete for the same VC-backed customers’ balances, but they do not underwrite commercial loans or hold crypto on balance sheet. Erebor’s pitch is that owning the charter lets it offer everything end-to-end, unlike Mercury/Brex.

- Anchorage Digital Bank (OCC trust bank) – Anchorage (recently rebranded Pact) has an OCC-issued national trust charter (since 2021) and provides institutional crypto services (custody, staking, USDC reserves, etc.). It is a regulated crypto bank but not a traditional lender. Anchorage is often cited as the leading “crypto bank,” and indeed Sacra analysis calls it Erebor’s sharpest crypto rival. However, Anchorage’s trust model limits it to digital asset custody and stablecoin issuing roles; it cannot extend regular dollar loans or insured deposit services as a full commercial bank.

- Trust Bank Conversions (Circle, Ripple, Paxos, etc.) – Several stablecoin issuers and custodians are converting to bank charters under the GENIUS Act framework. For example, Circle (USDC issuer) is pursuing a national trust charter, and Ripple was granted a conditional charter. These players own major stablecoin networks, giving them distribution advantages. They compete for the same trust banking infrastructure role Erebor envisions, but their model centres on supporting their own tokens and customers. None, so far, pair this with a full-service commercial bank offering to outside clients. If the market standardises on separating custody (trust banks) from lending banks, Erebor’s integrated model could be less compelling.

- Sponsor and Embedded Banking – Smaller banks like Cross River, Lead Bank, and Customers Bank have been active in fintech/crypto, offering embedded stablecoin rails or crypto payroll via partner platforms. They rival Erebor in the sense they can deliver USD accounts to crypto businesses via rails (e.g. Cross River’s stablecoin payments product or Lead Bank’s Stripe/Visa card stablecoin ties). However, those banks typically treat crypto as one product line, not a focus of their balance sheet strategy. Erebor’s counter-position is owning the end-to-end solution itself.

- Large Incumbent Banks (JPMorgan, BNY Mellon, etc.) – Big banks are exploring blockchain payment products (e.g. JPMorgan’s Onyx/Kinesis deposit token) and offer digital-asset custody (BNY’s role with Ripple). These could evolve into full services. JPMorgan explicitly markets “programmable deposits” (on-chain $ accounts) as an alternative to stablecoins. In the long run, if a big bank provides 24/7 settlement and tokenised deposits, it could undercut Erebor’s niche. For now, these incumbents generally maintain conservative credit standards and have not focused on SVB-style startup lending.

Comparison Axes

Along several dimensions Erebor both overlaps and diverges from others:

- Charter/Regime: Unlike fintechs (Mercury/Brex) it holds its own national bank charter. Unlike trust banks (Anchorage, Circle Trust) it plans to offer FDIC-insured deposits and lending. It is unique so far as a commercial bank expressly built for crypto integration.

- Crypto/Stablecoin Capabilities: Erebor’s marquee feature is built-in stablecoin settlement. This goes beyond SVB’s purely fiat model. Compared to defunct crypto banks (Signature, Silvergate), Erebor is more formally regulated (insurer, capital), though any crypto tie still raises concerns. Compared to fintechs, it is willing to have crypto on balance sheet (OCC-approved for gas fees).

- Underwriting Style: Erebor intends to underwrite on the basis of deep technical knowledge of collateral. SVB had a similar “startups and VCs” underwrite model. Mercury/Brex underwrite almost zero; Anchorage only provides custody. Traditional banks use broad credit guidelines. Erebor’s style will likely be very hands‑on and bespoke, akin to SVB but for different industries.

- Payments Stack: By owning a national charter, Erebor can directly use blockchains and stablecoins in its operations, unlike most peers. They advertise support for all major chain assets. This is a clear differentiator – none of the classic competitors (even Signature) announced such a deep integration in their charters.

- Risk Appetite: Erebor’s management claims (via higher capital cushions) to underwrite conservatively despite serving “risky” sectors. In practice, it is targeting exactly the risky end of the market that traditional banks avoid. This raises alarms (see “Risks” below). Its mandated 12% leverage is twice the requirement for a “well-capitalized” bank.

- Identity/Brand: SVB was a tech community pillar; Signature/Silvergate were known in crypto circles. Erebor brands itself as the convergence of innovation (name from Tolkien lore) and defence-tech (Luckey), hinting at alignment with national tech goals. This mix may attract some but make others cautious.

In sum, no existing institution is identical to Erebor. Some have pointed out that Erebor’s “innovation economy bank” model most closely matches SVB. Others note that, as a nationally chartered crypto-friendly bank, Erebor is largely untested. It is neither a conventional bank (charter + stablecoins is new) nor a generic crypto startup (it has real bank capital and regulation). This uniqueness means the competitive set is constructed by analogy rather than direct feature overlap.

Regulatory and Political Context

Erebor’s approvals came amid a sharp shift in U.S. bank policy. Under Comptroller Jonathan Gould’s OCC, the agency has expressly signalled openness to digital-asset banking. The OCC press release noted Erebor is “the first de novo bank to receive preliminary conditional approval” on Gould’s watch, and Gould praised the charter as an example of a “dynamic and diverse financial system”. OCC leadership has stated it “will not impose blanket barriers” on banks engaging in digital assets. Acting FDIC Chairman Travis Hill and other Trump appointees also publicly encouraged innovation in banking, which likely eased the way for Erebor. Industry observers note that both agencies “pushed” new charters and were willing to greenlight specialized banks after a period of little activity.

Stablecoin Policy

Erebor’s approval coincides with a more permissive U.S. policy environment for stablecoin-linked financial infrastructure. Recent changes in supervisory posture, together with the development of a federal framework for payment stablecoins, have reduced some of the legal ambiguity that previously constrained bank participation in token-based payments. Even so, the regime remains politically contingent, and Erebor’s strategy depends in part on whether that policy openness proves durable across future regulatory cycles.

Regulatory Safeguards

To win approval, Erebor’s application was subjected to rigorous scrutiny. The OCC issued strict conditions: for example, in its approval letter the OCC highlighted that holding crypto for gas fees is only allowed incidentally. The FDIC approval imposed a 12% Tier 1 leverage requirement and capital-call commitments. These conditions suggest regulators are aware of risk and are trying to force a conservative stance. On day one, Erebor is classified as “preconditions fulfilled,” meaning it must meet all OCC/FDIC conditions before opening fully.

Political Oversight

Not all reactions were positive. A group of Senators (led by Democrats) wrote a letter strongly criticizing the speed of Erebor’s approval and the founders’ political ties. They accused the process of favouring “billionaire cronies” and raising concentration concerns. Similarly, Bloomberg and Wired commentaries warned that combining crypto and startup banking could be prone to the same pitfalls that sank SVB. These voices underline that Erebor’s emergence is as much a political event as a market one: it’s widely seen as part of a Trump-era push to make the U.S. “crypto capital of the world” (per White House statements). Whether this push endures depends on long-term policy, but so far it clearly influenced regulators’ willingness to charter Erebor.

In regulatory terms, Erebor’s viability seems to hinge partly on this political era. The OCC and FDIC have set precedent by approving it. However, these approvals could have been unique to the current administration’s stance. If a future regulator chose to revoke or tighten rules (for example, if stablecoin rules were made more stringent or an administration less friendly to crypto came in), Erebor might face headwinds. For now, though, it stands as a legal and chartered bank – not a gray‑area fintech.

Risks and Counterarguments

Erebor’s model carries several substantial risks:

- Underwriting and Credit Risk: Targeting early-stage and technical firms means lending on non-traditional collateral. If such firms falter, Erebor’s losses could be large. As critics note, this is exactly the kind of risky “innovation economy” portfolio that led to SVB’s collapse. Unlike SVB, Erebor will have high capital buffers, but its return on equity will be low as a result. If defaults rise (e.g. in a tech downturn), the bank’s profitability and solvency would be tested.

- Deposit Concentration: The bank will serve a small number of large accounts (startups, founders, investment funds) rather than thousands of retail depositors. This means any single client failure or withdrawal (e.g. crypto market shock, big VC pullback) could materially affect liquidity. High concentration also makes funding stability fragile; regulators noted that SVB’s “monocrop” client base contributed to its run. Erebor’s charter conditions mitigate this somewhat (extra capital), but the fundamental risk remains.

- Crypto Correlation: Erebor’s fortunes may be tied to crypto markets. If a stablecoin it supports loses its peg, or if crypto prices crash, both its deposit base and loan collateral could drop in value simultaneously. Given its specialty, Erebor cannot easily diversify away from crypto-linked business. This correlation risk is more severe than for a general bank, and could trigger simultaneous credit and liquidity stress.

- Regulatory/Policy Reversal: So far, regulators have been friendly. But if political winds shift (new administration or Congressional changes), rules could tighten. For example, if the stablecoin reserve regime became more onerous, or if anti‑money laundering requirements on token flows increase, Erebor might have to change course. Its entire thesis rests on permissive rules for token use in banking; a policy reversal could be disruptive.

- Execution Risk: Building a bank from scratch is extremely complex. Erebor is starting with new technology (core banking system, on-chain integration) and untested processes. Implementing 24/7 operations and live blockchain settlement is ambitious. Any technical glitches or compliance failures (e.g. if it misuses on-chain accounts) could result in losses or regulatory penalties before the model proves out.

- Stablecoin Adoption: Erebor’s model assumes that stablecoins will be widely accepted by its customers and partners. This is not guaranteed. Institutional usage of stablecoins is still evolving, and on-chain settlement is not yet standard in most corporate treasuries. If clients do not adopt stablecoins as envisioned, Erebor’s specialized capabilities might remain underutilized, making it just a high-cost niche lender.

- Reputational/Political Risk: Some market participants may view Erebor skeptically because of Luckey’s polarizing political ties or the novelty of a “crypto bank.” The Senate letter and some media suggest this concern. If Erebor ever falters, these criticisms could amplify a loss of confidence. The founders’ network may help with initial deposits, but the bank will ultimately rely on broader market trust.

Strategic Assessment

Why Now: The timing is a product of both market and policy. The 2023 banking turmoil opened an unmet demand for tech and crypto banking. Simultaneously, the Trump administration and GOP Congress pushed through laws (like the GENIUS Act) and regulatory shifts that encourage crypto integration in banking. Luckey’s team was able to move quickly under this window: Erebor’s charter application (June 2025) was approved in just four months. In a different era (e.g. post-2024 election), the same plan might face longer scrutiny. “Why now” is answered by this convergence of sectoral need and political opportunity.

Why This Team: The founder’s deep tech and defence background signals an emphasis on “deep-tech underwriting.” Luckey brings a bold vision and networks (VCs, technologists, defence contacts) that can attract niche customers. The co-CEOs and CFO bring banking and crypto compliance experience, which is essential for executing. Critics might say the team lacks traditional retail banking pedigree; the job, however, is not retail but specialized institutional banking. The involvement of ex-bank executives like Hagedorn adds credibility. In sum, the team combination of tech visionaries and banking veterans seems deliberately chosen.

Why a Bank, Not a Fintech Wrapper: Erebor insists that owning the charter (not just BaaS) is key. A bank can hold deposits, lend directly, and most importantly control the ledger – enabling the promised on-chain settlement. A fintech layer on someone else’s bank couldn’t directly convert and custody stablecoins or internalize gas-payment functions. By being a bank, Erebor integrates the balance sheet into crypto workflows; that is its core differentiator. In short, the thesis is that a bank (with FDIC and OCC oversight) inspires trust and can “internalize” what fintech partners can only outsource. Observers should note that this is a bet on erosion of the “sponsor bank” model in favour of charterholder infrastructure.

Supporting Evidence: To date, evidence is mostly in charter approvals and fundraising. Erebor met all regulatory conditions quickly, and initial capital ($635M) suggests serious backing. The charter documents and press reports confirm the target markets and capabilities (stablecoins, crypto collateral). These show regulators were satisfied that the plan was plausible on paper. However, there is as yet no track record of actual customer flows or loan performance. The fact that Erebor must maintain high capital and no branches indicates it will be conservative initially.

Missing Evidence / Open Questions: Key unknowns remain. Will there actually be enough deposit dollars delivered by startups and crypto firms to fund a large loan portfolio? The bank’s plan relies on attracting high balances from clients like VCs and crypto exchanges; whether those clients will trust and shift funds is untested. Also, the stablecoin operations are unproven: we await details of what stablecoin products will be live at launch and how regulators will audit them. Another question is execution: building a core system from scratch, and syncing it with blockchain APIs, is a technical and operational challenge. Observers should track whether the OCC/FDIC impose any post-opening restrictions (the conditional approval implies milestones). Furthermore, the macro environment matters: a tech/crypto downturn could expose weaknesses in Erebor’s fund base.

12–24 Month Indicators: Key metrics to watch include: Customer onboarding – which types of firms open Erebor accounts first and in what volume; loan issuance – are meaningful credit facilities extended to target companies; stablecoin flows – is the bank actually minting/redeeming or integrating with on-chain networks (for example, its announced partnership with the Sui blockchain suggests one proof of concept); capital health – does it stay above regulatory thresholds (if it drops, the capital call kicks in); regulatory feedback – any formal guidance on Erebor’s activities, or additional OCC rulemakings on crypto banks. Finally, any change in administration or legislation around crypto could alter Erebor’s operating environment, so policy news is crucial.

Conclusion

Erebor Bank represents a high‑profile experiment at the intersection of banking, crypto and industrial policy. It answers a clear need – the post‑SVB funding gap and friction in crypto payments – with a uniquely ambitious product: a federally insured bank that speaks both dollar and token. Its founding team combines tech credibility with banking know‑how, and regulators (OCC/FDIC) have formally endorsed its plan. However, Erebor’s future is not assured. It hinges on execution of a novel business model, regulatory consistency, and actual demand for its integrated services. The bank’s built‑in safeguards (strong capital requirements, charter oversight) mitigate some risks, but systemic and execution risks remain high.

For institutional audiences, Erebor should be watched as a signal. If it thrives, it could herald a broader convergence of banking and tokenised dollars in the US. If it merely survives or fails, it will illuminate the limits of that convergence. Either way, Erebor’s journey will offer valuable data on how stablecoins and startups fit into regulated finance. In the next 1–2 years, the indicators outlined above (customer uptake, loan performance, policy shifts) will reveal whether Erebor is a one-off niche or a blueprint for the next generation of banking.

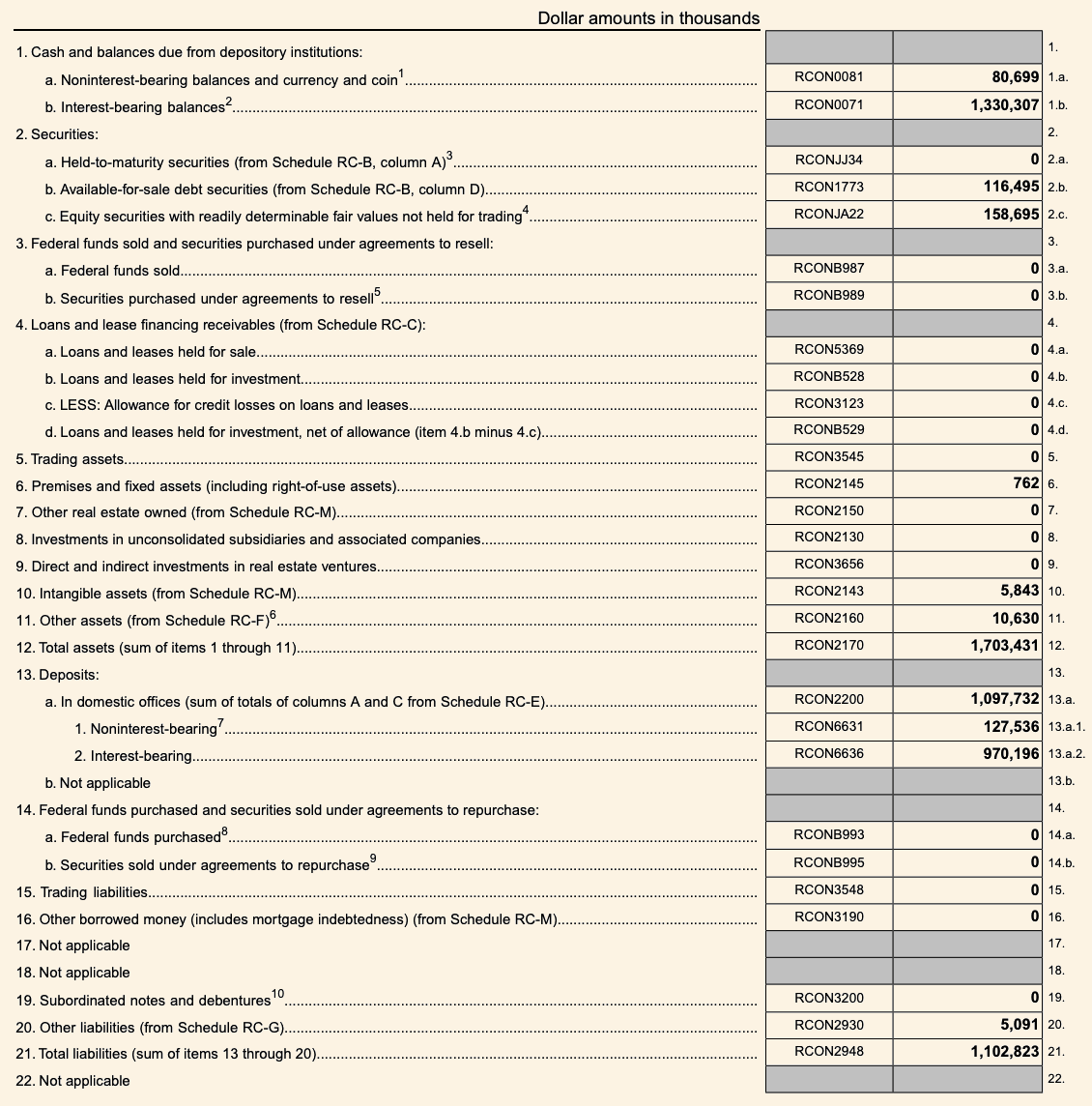

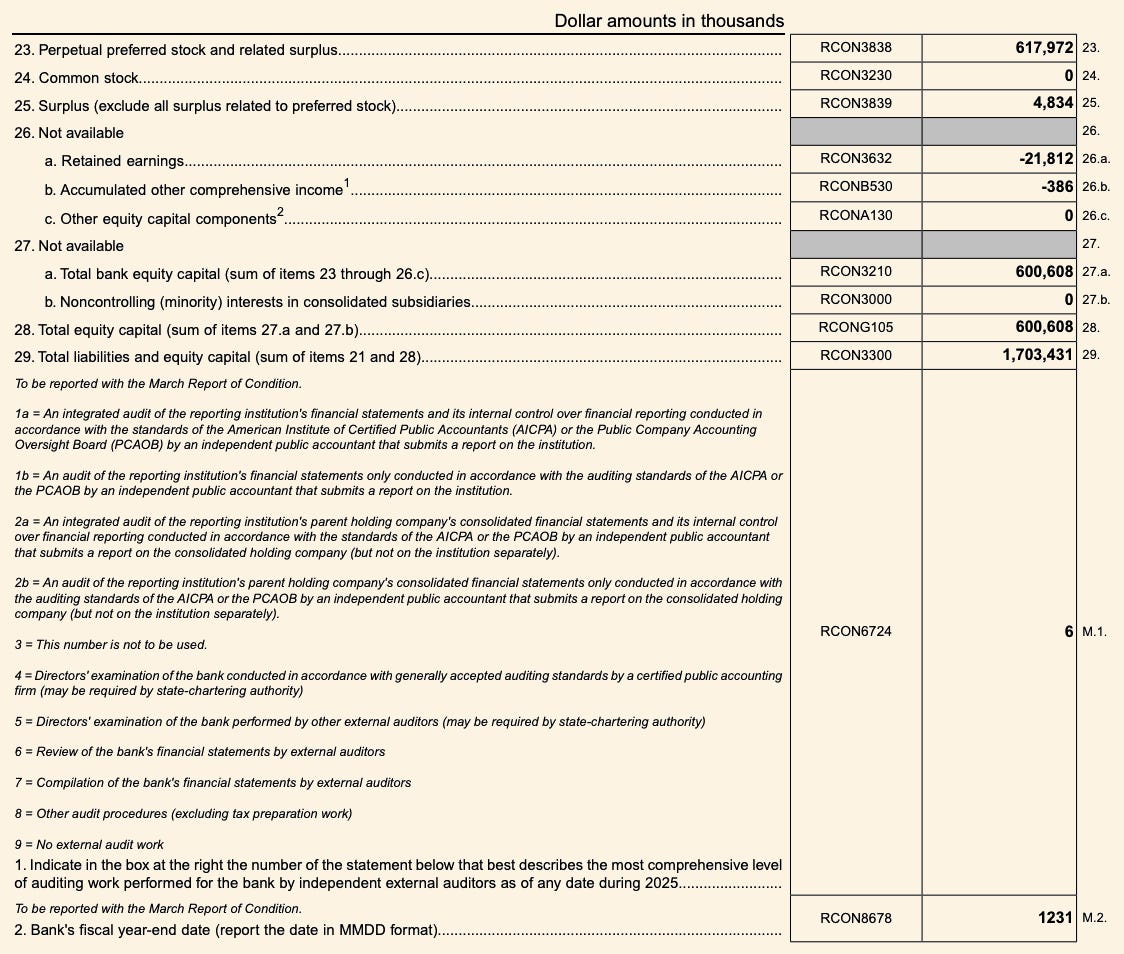

Erebor Bank: Financials (April 2026 update)

Erebor’s first call report shows the bank is already capitalized and deposit-rich, but still in a pre-credit, early-operating phase. As of March 31, 2026, Erebor reported $1.70 billion in total assets, $1.10 billion in deposits, and $600.6 million of bank equity capital, with no loans, no leases, no borrowings, and no trading assets on balance sheet. The asset mix was overwhelmingly liquid: roughly $1.41 billion sat in cash and balances due from depository institutions, alongside about $275 million in available-for-sale debt securities and equity securities. This matters because it shifts the analysis from charter approval to operating execution.

Erebor has assembled the balance-sheet capacity to act like a regulated bridge between fiat banking and stablecoin-native financial infrastructure, but the filing also shows that the lending engine has not yet started. Q1 revenue was mostly balance-sheet yield, with $3.36 million of net interest income, while $10.56 million of noninterest expense drove a $6.01 million net loss, consistent with a newly launched bank carrying technology, compliance, and operating costs before commercial credit, stablecoin payments, and customer activity begin to scale.

Sources:

Cover Artwork

A Calm Sea

Claude-Joseph Vernet, c. 1748

Risk Disclaimer:

insights4.vc and its newsletter provide research and information for educational purposes only and should not be taken as any form of professional advice. We do not advocate for any investment actions, including buying, selling, or holding digital assets.

The content reflects only the writer’s views and not financial advice. Please conduct your own due diligence before engaging with digital assets or related technologies, as they carry high risks and values can fluctuate significantly.

Note: This research paper is not sponsored by any of the mentioned companies.