The history of sovereign finance in emerging markets is characterized by a cyclical tension between state-imposed capital controls and the market’s innate drive for price discovery. This report introduces and develops the theoretical construct of the “Analogue Stablecoin” - a financial instrument that, in the pre-digital era, fulfilled the core functions that cryptocurrencies such as USDT (Tether) and USDC perform in the contemporary global economy. Specifically, this analysis identifies the travellers cheque (TC), within the context of Venezuela’s exchange control regimes (1983–1996), as the archetypal analogue stablecoin: a portable, dollar-denominated bearer instrument that served as a primary vehicle for capital flight, wealth preservation, and arbitrage against a distorted sovereign currency.

Through a rigorous examination of the Régimen de Cambios Diferenciales (RECADI) and the subsequent Oficina Técnica de Administración Cambiaria (OTAC), this report models the specific arbitrage loops that allowed Venezuelan economic actors to extract significant wealth from state coffers. We demonstrate that the “traveler” during this period was frequently not a tourist in the conventional sense, but a financial mule engaged in “round-tripping” - purchasing foreign currency at a subsidized state rate and liquidating it at a parallel market premium that often exceeded 100%. This mechanism was not merely a loophole; it was a structural feature of the Venezuelan economy that effectively transferred oil rents to the middle and upper classes, acting as a regressive social safety net during periods of macroeconomic collapse.

Furthermore, this report expands its analytical scope to include comparative case studies, illustrating the universality of this phenomenon. From the Soviet Union’s Vneshtorgbank checks and Argentina’s “Dolar MEP” bond arbitrage to the utilization of Hong Kong insurance policies by mainland Chinese citizens for capital expatriation, the “analogue stablecoin” emerges as a recurring symptom of financial repression. The findings suggest that regulatory attempts to ban such instruments are historically ineffective, as the market invariably migrates to the asset with the lowest friction and highest liquidity, a lesson with profound implications for current regulatory approaches to digital assets and stablecoins in distressed economies.

1. Theoretical Framework: The Political Economy of the “Analogue Stablecoin”

1.1 Defining the Analogue Stablecoin in a Repressed Economy

To understand the systemic role of travellers cheques in Venezuela between 1983 and 1996, it is necessary to strip away their commercial branding as tools for leisure and tourism and view them through the lens of monetary theory and asset pricing. In the contemporary digital asset ecosystem, a “stablecoin” is defined as a cryptocurrency designed to minimize price volatility by pegging its value to a reference asset, typically a fiat currency like the US dollar. Its primary utility in jurisdictions with weak monetary sovereignty is not speculation, but preservation: protecting purchasing power against hyperinflation, devaluation, and sovereign default.

The Venezuelan travellers cheque of the 1980s fulfilled this exact function, albeit in a paper-based format. It was a bearer instrument, or semi-bearer instrument requiring a countersignature, issued by trusted multinational entities (American Express, Thomas Cook, Visa) with balance sheets vastly superior to the Venezuelan state. In a regime of strict exchange controls, where the local currency (the Bolívar) is artificially overvalued by state decree and undervalued by market sentiment, the travellers cheque transforms from a travel accessory into a “privileged asset”. It becomes the bridge between the official fiction of the central bank and the material reality of the street.

We define the “Analogue Stablecoin” (AS) by three distinct economic characteristics that separate it from standard foreign currency cash:

- Hard Peg and Sovereign Bypass: The instrument represents a direct claim on a stable foreign currency (USD), legally domiciled outside the jurisdiction of the repressed economy. Unlike a local dollar bank account, which can be forcibly converted to local currency (pesification), the travellers cheque is a liability of a foreign entity.

- Cross-Border Portability and Legitimacy: The instrument can physically or legally bypass the jurisdictional boundaries of the repressed financial system under the guise of legitimate non-financial activity (tourism). This “regulatory camouflage” is essential for its function.

- Arbitrage Capability: The acquisition cost of the instrument (at the official state rate) is significantly lower than its liquidation value (at the parallel market rate), creating a risk-free or low-risk profit margin for the holder.

1.2 The Economics of Financial Repression and the “Gap”

Financial repression, a term popularized by McKinnon and Shaw, relies on the state’s ability to force domestic savers to hold government debt or local currency at negative real interest rates. This is achieved through the imposition of capital controls that prevent capital flight and segment the foreign exchange market. However, capital controls almost inevitably create a “dual market”: an official market where the exchange rate Eofficial is fixed by decree to subsidize specific sectors (imports of food, medicine, and ostensibly, travel), and a parallel (or black) market where the rate Eparallel floats freely according to supply and demand.

The “Gap” or “Spread” SSS constitutes the profit margin of the arbitrageur and serves as the primary incentive for the acquisition of the analogue stablecoin. The incentive to engage in the trade of travellers cheques is defined by the function

When $S > C$, where $C$ represents the total transaction costs (including banking commissions, travel expenses, bribes to officials, and the opportunity cost of time), arbitrage becomes not only profitable but the dominant economic activity of the rational actor. In the Venezuelan context, this equation implies that as the spread widens, often due to a collapse in oil prices or a spike in local inflation, the demand for travel quotas becomes inelastic with respect to the cost of travel itself. The flight to Miami becomes merely a transaction fee for the acquisition of dollars.

The state inadvertently subsidizes this arbitrage. By creating bureaucratic mechanisms like RECADI (1983–1989) and OTAC (1994–1996), which allocated dollars at preferential rates for “travel expenses,” the government effectively sold US dollars at a discount to its own citizens. The travellers cheque was the physical vessel for this subsidized capital. The “traveler” was, in economic terms, a mule for financial arbitrage, purchasing the analogue stablecoin at Eofficial and liquidating it abroad or internally at Eparallel. This represents a transfer of wealth from the sovereign’s foreign reserves to private individuals, a phenomenon often described in rentier state literature but rarely modeled as a financial derivative trade.

1.3 Price Discovery in Shadow Markets

In a repressed economy, the official exchange rate loses its information value. It becomes a political number, detached from market reality, maintained only through coercion and the rationing of reserves. The analogue stablecoin aids in restoring true price discovery. The parallel market rate is often determined by the marginal cost of obtaining these instruments. If obtaining a travellers cheque requires a bribe to a banker, a wait time of three weeks, or a physical flight to a foreign jurisdiction, those costs are priced into the black market dollar.

Therefore, the street value of a travellers cheque in 1980s Caracas, or the premium paid to a gestor (fixer) to process the paperwork, was a more accurate reflection of the Venezuelan economy’s health than any statistic published by the Central Bank of Venezuela (BCV). The premium paid for these cheques measured the aggregate “fear” of the population: fear of devaluation, fear of expropriation, and fear of poverty. This function mirrors the role of the “Blue Dollar” in Argentina or the USDT/Naira rate on Binance P2P in Nigeria, serving as the true barometer of economic sentiment.

2. Historical Context: Venezuela’s Descent into Exchange Controls (1983–1996)

2.1 The Collapse of “Saudi Venezuela” and the Onset of Crisis

To comprehend the magnitude of the arbitrage opportunity created by travellers cheques, it is necessary to understand the psychological and economic baseline of the Venezuelan population prior to 1983. For decades, the Venezuelan Bolívar was one of the strongest currencies in Latin America, pegged at Bs. 4.30 to the US dollar. This stability, underwritten by the oil windfalls of the 1970s, produced a consumption culture in which the middle class regarded international travel and imported goods as a birthright. The phrase “dame dos” (“give me two”), used by Venezuelans shopping in Miami, encapsulated a society that perceived its local currency as hard money.

The structural weaknesses of this rentier model became visible in the early 1980s. A combination of declining oil prices, rising global interest rates (the Volcker shock), and sustained capital flight drained the reserves of the Central Bank of Venezuela (BCV). By 1982, it was mathematically impossible to defend the Bs. 4.30 peg. The illusion of stability collapsed on 18 February 1983, a date remembered in Venezuela as Viernes Negro (Black Friday). The administration of President Luis Herrera Campins was forced to devalue the currency and, for the first time in decades, impose strict exchange controls to slow the outflow of foreign reserves.

2.2 The Institutional Design of RECADI (1983–1989)

In response to the crisis, the government established the Régimen de Cambios Diferenciales (RECADI), an agency tasked with rationing the country’s dwindling foreign exchange. The system was built as a multi tier exchange rate structure, a classic form of financial repression intended to shield lower income groups from inflation while allowing the state to service its external obligations.

The tiers were generally structured as follows:

- Preferential Rate: Reserved for essential imports (food, medicine) and public sector external debt payments.

- Official / Commercial Rate: Allocated for authorized industrial imports and student expenses abroad.

- Free Market Rate: A floating rate for luxury goods and unauthorized transactions, which traded significantly higher than the official tiers.

Crucially, “travel expenses” were placed in categories that allowed access to dollars at rates far more favorable than the free market rate. This was a political decision. Stripping the middle class of its ability to travel was seen as politically unacceptable for a democratic government already losing support. As a result, the Cupo de Viajeros (Traveler’s Quota) was institutionalized as a state sanctioned allocation of cheap dollars for citizens travelling abroad. This specific policy choice transformed the travellers cheque into the primary vehicle for accessing the subsidy embedded in the dual exchange rate system.

2.3 The 1994 Banking Crisis and the Resurgence of Controls

After a brief and turbulent period of liberalization under the second administration of President Carlos Andrés Pérez (1989–1993), during which RECADI was dismantled amid major corruption scandals, Venezuela fell back into a deep financial crisis in 1994. The immediate trigger was the collapse of Banco Latino, the country’s second largest bank, which set off a systemic contagion that affected more than one third of the banking sector.

In total, 17 financial institutions failed, representing roughly 60% of the assets of the financial system and around half of total deposits. The fiscal cost of the bailout was enormous, estimated at a minimum of 10% of GDP and, on some measures, closer to 20%. This injection of liquidity, not matched by any increase in production or reserves, intensified the flight to quality. Confidence in the Bolívar eroded, and demand for dollars surged.

In response, the administration of Rafael Caldera, elected on a platform that rejected neoliberal reforms, suspended constitutional guarantees and reimposed strict exchange controls. The Junta de Administración Cambiaria (JAC) and later the Oficina Técnica de Administración Cambiaria (OTAC) were created to replace the defunct RECADI. Once again, the spread between the official fixed rate and the black market rate widened, and once again, the travellers cheque became the key analogue stablecoin for households seeking to protect their savings from a banking system in freefall.

3. Mechanism of the Arbitrage: The RECADI Era (1983–1989)

3.1 The Architecture of the “Cupo de Viajeros”

The “Cupo de Viajeros” was an annual allocation of foreign currency granted to natural persons for the specific purpose of travel abroad. During the RECADI years, the mechanism for accessing this quota was bureaucratic, heavily paper-based, and rife with opportunities for exploitation.

The Arbitrage Workflow

Application and Documentation:

A citizen would apply to RECADI (typically via a commercial bank acting as an intermediary) with proof of impending travel. The primary requirements were a valid passport and a round-trip airline ticket to a foreign destination.

Authorization:

Upon approval, the citizen was authorized to purchase a set amount of US dollars (for example, $5,000 per year, though amounts varied by destination and year) at the preferential rate (for example, Bs. 7.50/$ while the street rate was Bs. 25/$).

Issuance via “Analogue Stablecoin”:

The dollars were rarely handed over in physical cash banknotes, both for logistical reasons and to preserve a minimum of traceability. Instead, they were issued as travellers cheques (brands such as American Express, Visa, Citicorp, Thomas Cook). Officially, this was a security measure to ensure the money was used for travel expenses.

The Arbitrage Event:

The citizen would take possession of the cheques. Instead of spending them on hotels, meals, or leisure in Miami or Europe, they would engage in “round-tripping”. In practice, this meant flying to the destination to satisfy the physical requirement (passport stamp, boarding passes) and then returning quickly, or in some cases simply mailing the cheques to a foreign account if controls were lax.

Liquidation:

The cheques were deposited into a foreign bank account or sold to a broker. The resulting dollars were then sold back on the Venezuelan parallel market. When the parallel rate was 300% higher than the preferential rate, the profit was extraordinary.

3.2 The Travellers Cheque as the Vehicle of Choice

Why were travellers cheques the preferred vehicle for this arbitrage? In the pre-digital era, wire transfers were slow, expensive, and subject to intense regulatory scrutiny by central banks. Physical cash (banknotes) carried significant security risks; transporting $5,000 in $20 bills required physical bulk that was hard to conceal and easy to steal.

Travellers cheques offered precisely the “analogue stablecoin” features that mitigated these risks:

High denomination density:

They were available in high denominations ($50, $100, $500, and even $1,000), allowing large sums of value to be carried in a small, discreet envelope.

Security and recoverability:

If lost or stolen, they could be refunded by the issuer (e.g., American Express), which reduced the operational risk of the “mule” operation. This insurance feature made them superior to cash for the illicit or semi-licit transport of value.

Global liquidity:

They were treated as “good as cash” in international markets but required a countersignature. That requirement created a thin veneer of personal use that reassured Venezuelan regulators the funds were for travel, while in reality the countersignature could be performed en masse at a willing exchange house in Miami or Curaçao.

3.3 Systemic Corruption: The “Chinese RECADI” and the Ghost Travelers

The widespread nature of this arbitrage fostered systemic corruption that reached the highest levels of the Venezuelan state. The most infamous case was the so-called “Chinese RECADI” scandal involving Ho Fuk Wing, a businessman accused of large-scale fraud involving import over-invoicing and currency manipulation. A significant component of the broader scandal was the “ghost traveler” phenomenon.

Investigations revealed that corrupt officials and syndicates would use the passports of deceased citizens, or “rent” the passports of low-income Venezuelans who had no intention of travelling, to apply for the travel quota. Travellers cheques were issued in the names of these individuals but controlled by the syndicate. This industrialized the arbitrage process, decoupling it from the physical act of travel and turning it into a pure financial extraction machine.

The scandal also touched the political elite. Allegations swirled around figures such as Blanca Ibáñez, the private secretary (and widely rumoured partner) of President Jaime Lusinchi, who was accused of using her influence to facilitate access to preferential dollars. The “Agenda Secreta de RECADI” investigations exposed how the allocation of these dollars was often a matter of political patronage rather than economic necessity.

3.4 The Profit Equation of a 1986 Arbitrageur

To illustrate the incentive structure, consider a Venezuelan citizen in 1986. The official exchange rate for travellers is set at Bs. 7.50 per US dollar, while the black market rate is around Bs. 20.00.

Initial capital allocation

The citizen applies for the maximum foreign currency quota, for example USD 5,000 for a trip to Europe.

Cost in bolívares: 5,000 × 7.50 = Bs. 37,500.

Operational cost (the “tourism” pretext)

The citizen buys a ticket to Madrid. Because of fuel subsidies and the distorted exchange rate, the flight is artificially cheap, say Bs. 5,000.

Liquidation abroad

After arriving in Madrid, the traveller does not use the cheques for tourism. Instead, they deposit them into a Spanish bank account or cash them at a bureau de change.

Gross value in foreign currency: USD 5,000.

Repatriation and parallel market sale

The citizen then sells the USD 5,000 on the parallel market at Bs. 20 per dollar.

Proceeds in bolívares: 5,000 × 20.00 = Bs. 100,000.

Net arbitrage profit

Net profit in bolívares:

Bs. 100,000 (sale on parallel market)

minus Bs. 37,500 (official purchase cost)

minus Bs. 5,000 (flight)

= Bs. 57,500.

For context, the minimum monthly wage in 1986 was roughly Bs. 1,500. A single trip could therefore generate the equivalent of almost 38 months of minimum wage income in what was effectively perceived as risk-free arbitrage. This helps explain why international flights departing Caracas were fully booked, while hotels at the destination often reported few Venezuelan guests: many travellers stayed with friends, slept in airports, or returned almost immediately, using the “holiday” only as a vehicle to harvest the exchange rate spread.

4. The 1994–1996 Crisis: The “Analogue Stablecoin” Under Stress

4.1 The Banking Collapse and the Flight to Quality

The 1994 banking crisis fundamentally altered the nature of the arbitrage. During RECADI, the arbitrage was often a mechanism for profit maximization and consumption, funding the “Miami lifestyle”. In the post-1994 environment, it became a mechanism for survival. With inflation accelerating toward 100% in 1996 and the banking system collapsing, holding bolívares was tantamount to watching one’s wealth incinerate.

The crisis began with Banco Latino but quickly spread to Banco de Venezuela and Banco Consolidado. As the government injected liquidity to guarantee deposits, the money supply exploded. Rational actors immediately sought to convert this excess liquidity into hard assets. With capital controls reimposed, the travellers cheque once again became the most accessible “stablecoin” for the average citizen.

4.2 Tightening the Noose: The JAC and OTAC Regime

The Caldera administration, recognizing the massive leakage of reserves through the travel quota, attempted to tighten the mechanism through the Junta de Administración Cambiaria (JAC). The rules for accessing travellers cheques became stricter and more invasive.

- Enhanced documentation: Travellers were required to provide not just tickets, but stamped passports upon return, boarding passes and affidavits of use. This was an attempt to curb the “ghost traveler” phenomenon.

- Quota reductions: The amounts available were scrutinized and often reduced based on destination and duration of travel.

- Interest rate distortion: Domestic lending rates spiked to 54–60% in 1994–1995. While this would nominally discourage borrowing to buy dollars, the expected devaluation and the parallel market premium (often exceeding 100%) meant that the real interest rate for an arbitrageur was effectively negative. It was still profitable to borrow bolívares at 60% interest to buy dollars that would appreciate by 100% or more on the black market.

4.3 Market Distortion and the Informal Economy

The reliance on travellers cheques and the black market distorted the entire pricing structure of the Venezuelan economy. “Imported” goods in the informal sector were priced at the parallel rate, while those with access to the official rate (via travellers cheques or import licenses) could undercut competitors or reap massive windfall profits. This dynamic destroyed domestic production, as it was far more profitable to be a financial arbitrageur than a manufacturer.

The travellers cheque market essentially became the de facto supply of dollars for the informal economy. Small businesses that could not access the labyrinthine OTAC system for official imports would purchase dollars from returning travellers. The “analogue stablecoin” was providing essential liquidity to the real economy where state mechanisms had failed, effectively dollarizing the marginal transactions of the country long before official dollarization was even debated.

5. Comparative Case Studies: The Universality of the Mechanism

To demonstrate that the Venezuelan experience was not a localized anomaly but a predictable outcome of financial repression, we examine four other historical and contemporary instances where “analogue stablecoins” emerged to bridge the gap between official and market realities.

5.1 The Soviet Union: Vneshtorgbank Checks and Series D

In the Soviet Union, the ruble was strictly non-convertible, and ownership of foreign currency was a criminal offense. However, the state needed a mechanism to capture the foreign earnings of diplomats, technical specialists and sailors. The solution was the Vneshtorgbank check (and later Series D checks).

- The mechanism: These checks were theoretically pegged to the ruble but served as a parallel currency. Their primary utility was that they could be spent in “Beryozka” stores, state-run retail outlets that sold Western goods (jeans, electronics, high-quality food) unavailable to the general public.

- The arbitrage: While officially pegged at rates like 1:1 or 4.6:1 depending on the check series and era, the black market premium for these checks was enormous. They traded at 5 to 8 times their nominal value because they represented the only access to the Western lifestyle within the Soviet autarky.

- Analogue stablecoin function: They functioned as a stable store of value superior to the ruble. Just like Venezuelan travellers cheques, they were a secondary currency created by state inefficiency, trading at a massive premium due to their privileged access to goods.

5.2 Argentina: The “Dólar MEP” and the “Blue” Gap

Argentina offers the most direct modern parallel to the Venezuelan case, utilizing financial securities instead of travellers cheques as the arbitrage vehicle.

- Dólar MEP (Mercado Electrónico de Pagos): This mechanism allows investors to buy a bond denominated in Argentine pesos (for example Bonar 30 or Global 30) and sell the same bond in US dollars. This is a legal, albeit regulated, way to convert currency.

- The “gap” (brecha): The difference between the official exchange rate and the MEP or “blue” (street) rate creates the arbitrage incentive. This gap often exceeds 100%, driving the entire economy’s pricing structure.

- Friction as regulation: Just as Venezuela required physical travel, Argentina imposes “parking” periods (waiting periods of 1 to 5 days) between buying the bond in pesos and selling it in dollars. This introduces price risk, serving as a regulatory friction to dampen the arbitrage speed. Recent moves to allow tourists to use credit cards at the MEP rate (the “tourist dollar”) represent the state attempting to capture the arbitrage flow that previously went to informal money changers (”cuevas”).

5.3 China to Hong Kong: The Insurance Policy Arbitrage

Perhaps the most sophisticated “analogue stablecoin” mechanism of the 21st century involves the use of Hong Kong insurance products by mainland Chinese citizens to evade capital controls.

- The mechanism: Chinese citizens face a strict annual cap of 50,000 US dollars on foreign currency conversion. To bypass this, individuals would travel to Hong Kong and use UnionPay cards to purchase large life insurance policies (with premiums often reaching 1 million US dollars or more). The transaction was coded as a “purchase of services”, not a capital transfer, thus bypassing the forex quota.

- The liquidation (cooling-off period): The true arbitrage lay in the cooling-off period mandated by Hong Kong consumer protection laws. Policyholders could cancel the policy within a short window (for example 21 days) for a full refund. Crucially, the refund was paid into a Hong Kong bank account in valid foreign currency (HKD or USD), effectively transforming onshore RMB into offshore USD.

- The regulatory response: In 2016, regulators and UnionPay capped these transactions at 5,000 US dollars per swipe and banned the purchase of “investment-related” insurance products with mainland cards, recognizing that the insurance policy had become a pure capital flight vehicle.

5.4 Nigeria: The P2P USDT Market

In modern Nigeria, the “analogue” aspect has largely been replaced by digital tools, but the economic logic remains identical to the Venezuelan case.

- The mechanism: With the Central Bank of Nigeria (CBN) restricting access to official dollars for imports, Nigerians turned to USDT (Tether) on peer-to-peer (P2P) exchanges such as Binance.

- The premium: The USDT/NGN rate on P2P markets trades at a significant premium to the official naira rate, serving as the true reference rate for the economy. The arbitrage here is often purely defensive: converting naira to USDT to avoid devaluation. The government’s recent crackdown on Binance and P2P merchants mirrors the Venezuelan crackdown on RECADI brokers, blaming the messenger (the exchange rate) for the underlying message (monetary mismanagement).

6. Quantitative Analysis: Modelling the Arbitrage Spread (1983-1996)

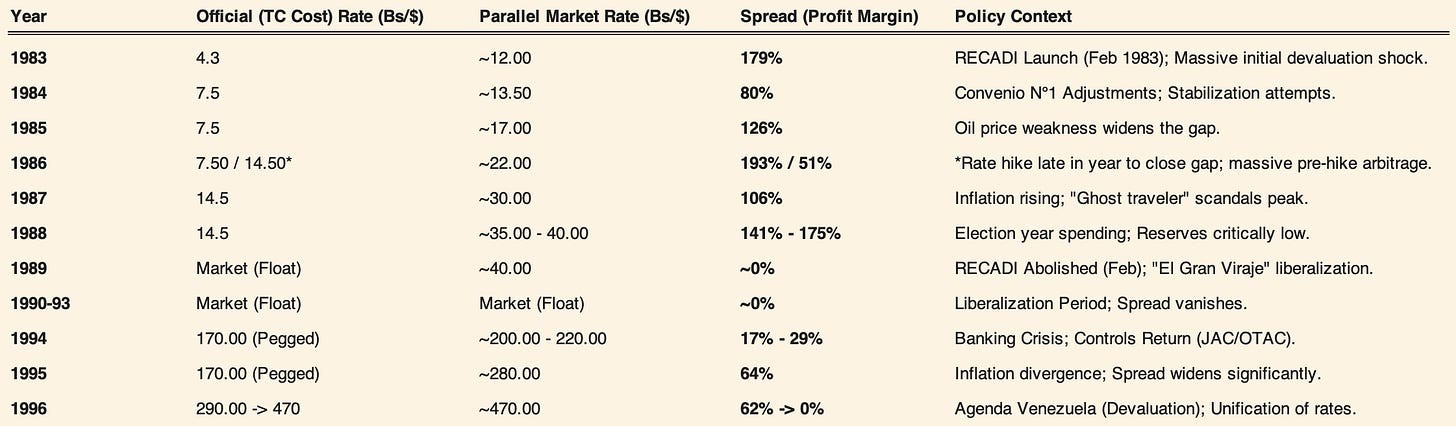

Using the historical data gathered from IMF reports, Central Bank archives, and historical exchange rate datasets, we can reconstruct the incentives that drove the Venezuelan market during the period of study.

6.1 The Spread Index

The following table reconstructs the “Arbitrage Incentive” by comparing the effective cost of the “Analogue Stablecoin” (TCs obtained via the Cupo) versus the Parallel Market Liquidation Price. This “Spread” represents the gross profit margin available to the arbitrageur before transaction costs.

6.2 Interpreting the Data: The “Golden Era” vs. The “Crisis Era”

- The “Golden Era” (1983 to 1988): The spread consistently exceeded 100 percent. In financial market theory, an arbitrage spread of this magnitude is an anomaly that should be competed away almost instantly. The fact that it persisted for five years indicates massive regulatory friction and state subsidy. The travellers cheque was effectively the only instrument that allowed the average citizen to bridge this gap. In practice, the state was paying its own citizens to take money out of the country.

- The Crisis Era (1994 to 1996): The spread reappeared but became more volatile. The risk premium increased as the banking sector itself came under stress. The fact that these spreads persisted even when domestic interest rates were above 50 percent indicates that the market’s expected depreciation of the Bolívar far outweighed the cost of local borrowing. The narrowing of the spread in 1996 aligns with the “Agenda Venezuela” reforms, which devalued the official rate toward the market rate and temporarily closed the arbitrage window.

7. Policy Implications and Future Outlook: From Paper to Digital

7.1 The Analogue-to-Digital Evolution

The economic behavior observed in Venezuela (1983-1996) is functionally identical to the behavior observed in modern markets regarding stablecoins like USDT (Tether) and USDC in high-inflation economies.

- Then: A Venezuelan citizen buys American Express Travellers Cheques at the official rate → Flies to Miami → Deposits in US Bank Account → Sells dollars on the parallel market.

- Now: A Nigerian or Argentine citizen buys USDT via P2P market → Holds in a digital wallet → Sells for local currency to pay expenses or holds for wealth preservation.

The Travellers Cheque was the Proto-Stablecoin. It solved the fundamental problem of financial repression: “How do I hold hard currency without holding physical cash that can be confiscated or demonetized?”

7.2 Lessons for Regulators: The Futility of Bans

Arbitrage Is Unstoppable Under Dual Rates:

As long as there is a statutory gap between the official price of money and the market price, an instrument will always emerge to bridge it. Banning travellers cheques in the 1990s did not stop capital flight; it redirected it into over-invoiced imports and later into credit card scraping (”raspacupo”). Banning crypto exchanges in Nigeria or Argentina will not stop outflows; it will simply push them into other digital assets or back into informal hawala-style networks.

The “Use Case” Fallacy:

Regulators often treat travellers cheques as products for tourism and insurance policies as products for protection. They fail to recognize when these instruments are functioning as financial derivatives. In China, regulators only belatedly understood that Hong Kong insurance policies had become de facto capital flight tools. Regulators today need to examine “utility tokens”, NFTs, or metaverse assets through the same lens: are they genuinely serving their stated consumer use case, or are they in practice vehicles for moving wealth across borders?

Friction As the Only Effective Control (Short of Unification):

The only mechanism that meaningfully reduced the RECADI arbitrage, short of unifying or liberalizing the exchange rate, was an increase in friction - more bureaucracy, stricter physical travel requirements, longer waiting periods. Argentina’s bond “parking” rules play a similar role. Friction, however, also suppresses legitimate economic activity. The “cooling off” period in Hong Kong insurance illustrates a more targeted approach: adding friction at a specific point in the loop in order to break the arbitrage cycle without banning the underlying product outright.

7.3 Wealth Preservation Function

For Venezuelan households, the travellers cheque was not primarily a tool of greed, but of survival. By 1996, with inflation near 100 percent, holding Bolívares was financial self-destruction. Arbitraging into travellers cheques was a rational response to state-induced volatility.

The same logic applies in modern Nigeria or Argentina. The scramble into USDT or Dólar MEP is a rational flight to safety, not a moral failure of households. Policies that attempt to block these exits without addressing the underlying monetary instability - persistent fiscal deficits, monetary financing, and loss of credibility - are destined to fail. They simply raise the premium, the implicit “risk tax”, that the poorest segments of society must pay to access any form of stable asset.

8. Conclusion

The Venezuelan travellers cheque market of 1983–1996 is a powerful and under-studied historical case of the “Analogue Stablecoin”. It shows that under financial repression, markets will always construct a parallel price discovery mechanism. Stripped of touristic branding, the travellers cheque operated as a bearer instrument for arbitrage, channeling wealth from the distorted official sector into the more truthful parallel market.

The very large spreads observed during the RECADI years were not anomalies. They were accurate measures of the subsidy the state extended to the middle class and of its mismanagement of the currency regime. The shift from paper-based arbitrage in the 1980s to digital arbitrage in the 2020s - via stablecoins and fintech rails - reflects a change in technology, not in underlying economic logic.

The core lesson is simple: you cannot repress the market’s search for value; you can only raise the cost of the search.

The history of the Venezuelan travellers cheque is a testament to the ingenuity of economic actors confronting state-imposed distortions, and a direct precursor to the decentralized financial practices of the digital age. The “traveler” of 1986, carrying American Express cheques in a jacket pocket, and the “trader” of 2024, holding USDT on a smartphone, are performing the same essential act: the preservation of wealth against encroachment by a failing monetary regime.

Sources

- The Monetary and Fiscal History of Venezuela, 1960–2016 (University of Chicago, MAFH project)

- “Inflation and the Black Market Exchange Rate in a Repressed Market: A Model of Venezuela” (IMF Working Paper, 2016)

- “The Black Market for Dollars in Venezuela” (Banco de la República)

- “Exchange Measures in Venezuela” (IMF Staff Papers, 1964)

- “Transaction Costs and Corruption: Chinese Capital Flight, 1984–2012”

- “Determinants of Venezuela’s Equilibrium Real Exchange Rate” by Juan Zalduendo

Cover Artwork

Miranda en la Carraca

Arturo Michelena, 1896

Risk Disclaimer:

insights4.vc and its newsletter provide research and information for educational purposes only and should not be taken as any form of professional advice. We do not advocate for any investment actions, including buying, selling, or holding digital assets.

The content reflects only the writer’s views and not financial advice. Please conduct your own due diligence before engaging with cryptocurrencies, DeFi, NFTs, Web 3 or related technologies, as they carry high risks and values can fluctuate significantly.

Note: This research paper is not sponsored by any of the mentioned companies.