Founded in 2012 by serial fintech operator Micky “Micky” Malka, Ribbit has built a quiet reputation for funding the financial system’s hard parts, not its hype, backing category-defining platforms from Robinhood and Coinbase in the U.S. to Nubank in Brazil. Malka’s Venezuela upbringing, shaped by inflation, devaluations, and institutional failure, is more than biography: it is the origin of Ribbit’s pattern recognition about what breaks in money, and what must be rebuilt.

This research paper frames Ribbit as an operator-led investing machine with a specific edge: regulatory fluency, systems thinking, and conviction underwriting in compliance-heavy categories. We trace how that method evolved across Ribbit’s early funds, then translate the 2025 “Token Factory” letter into investable primitives: tokens as machine-legible claims on identity, assets, and expertise; agents as the new economic interface; and capital formation at internet speed as a structural shift in how financial products launch, distribute, and compound. Finally, we isolate what most observers miss: Ribbit is neither a fintech momentum fund nor a crypto tourist, but a thesis-driven platform built to operate through regime change, including acknowledging its misses and the limits of its worldview.

Origin Story That Actually Matters

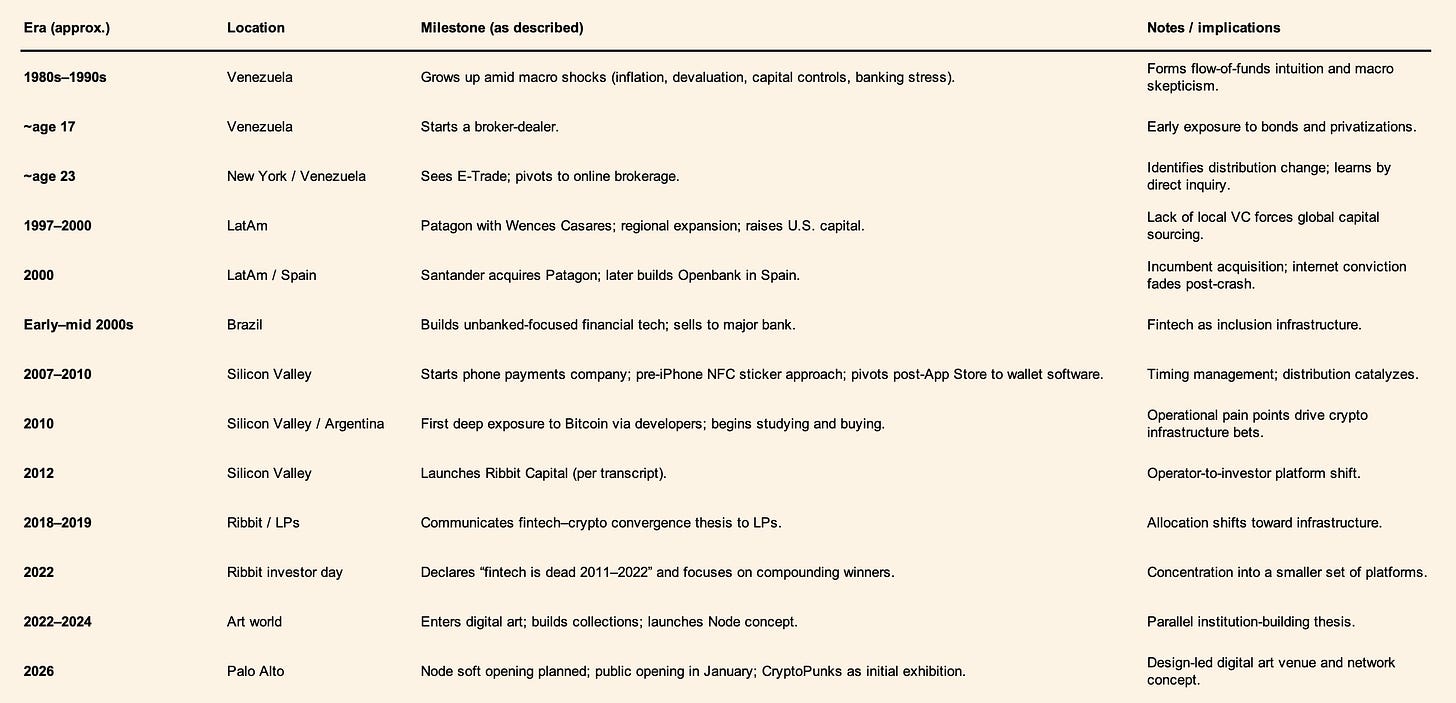

Micky Malka’s journey from teenage fintech founder in Caracas to Silicon Valley power investor isn’t a standard venture biography – it’s the foundation of Ribbit’s strategy. Malka grew up in 1980s Venezuela, where bank runs, currency devaluations, and 100%+ inflation were lived reality. At age 6, he famously wrote a letter to the tooth fairy asking for U.S. dollars instead of bolivars – a cute anecdote with serious subtext: he already sensed his local money was broken. By 17, Malka co-founded a broker-dealer (Heptagon Group) to exploit a local banking quirk that let him earn double interest on weekends during high inflation. In his early 20s, he partnered with Argentine entrepreneur Wences Casares to build Patagon, one of Latin America’s first online banks. When Santander acquired Patagon in March 2000 for ~$750 million (just before the dot-com crash), Malka experienced the euphoric rise and harsh fall of an internet-era startup. He went on to launch Banco Lemon (Brazil, 2003) targeting underbanked customers – which became Brazil’s largest private microfinance institution before its sale to Banco do Brasil in 2009. Stints as interim CEO of OpenBank (a Spanish online bank) and co-CEO of Bling Nation (a Palo Alto mobile payments startup) followed. In short, Malka had built and sold five financial services companies across three continents before he ever wrote a VC check.

This operator’s arc matters because it shaped Ribbit’s DNA. By the time Malka moved to Palo Alto in 2007 to “play in the Champions League” of tech, he had learned how entrenched financial systems could be cracked from the outside – and how regulatory nuances (in multiple languages) could make or break a venture. Thus, when he raised Ribbit Capital’s first fund in 2012, Malka pitched LPs not just a fund, but himself – a battle-tested guide for fintech rebels. He often shares a personal story during fundraising: how as a child he distrusted his country’s money, or how at Bling Nation he struggled to find U.S. investors who grasped payments regulations. These experiences led Malka to design Ribbit as, in his words, “a company that happens to deploy capital” rather than a traditional fund. Ribbit’s early team mirrored this ethos: co-founder Nick Shalek had been a Yale endowment analyst and entrepreneur; early partner Nikolay Kostov came from banking. Everyone on the team, like Malka, had “felt the pain” of financial plumbing and could roll up their sleeves on compliance, legal structure, and product design. Malka set a tone of extreme availability – telling founders that “along with their wives, mothers and friends, I’m a top number on the speed dial”. This approach was high-touch and atypical in venture, but it attracted entrepreneurs in complex fintech fields who valued an investor who spoke their language.

Timeline - Micky “Micky” Malka

Importantly, Malka’s operator lens gave Ribbit a global focus from day one. Having lived through Latin America’s volatility and Europe’s banking evolution, Malka eschewed any “Silicon Valley only” myopia. Ribbit’s Fund I LPs included Spain’s BBVA and SVB, and the fund’s remit spanned the US, Canada, UK, Brazil, Spain, South Africa and beyond – all places Malka believed had high digital adoption and big financial inefficiencies. This global purview set Ribbit apart in 2012, when many VCs stuck to their home turf. It enabled the firm to spot opportunities like Brazil’s Nubank or Britain’s Revolut early, applying lessons across markets (e.g. seeing Brazil’s banking fees as analogous to U.S. stock trading fees pre-Robinhood). In summary, Malka’s unusual resume – from Caracas to Palo Alto – “actually matters” because it equipped Ribbit with an operating playbook, regulatory savvy, and global intuition that few venture investors can rival. Ribbit’s edge is essentially Malka’s life experience, institutionalized.

Ribbit’s Early Funds as a System, Not a Highlight Reel

Ribbit Capital’s first three funds (2012–2017) provide a case study in systematic thesis execution. Rather than spray money at anything labeled “fintech,” Ribbit constructed each fund with a clear theme and a long-term plan.

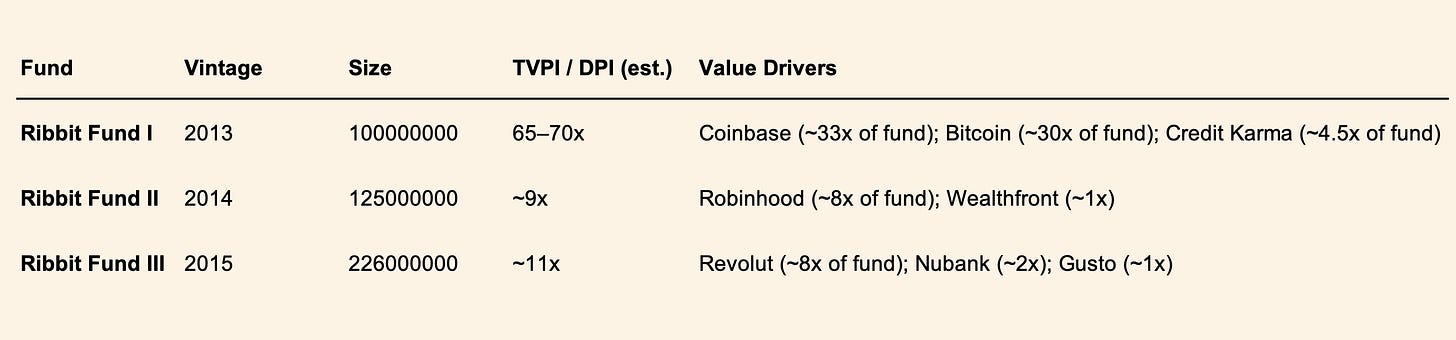

Fund I (2012) launched with $100 million – a modest size Malka deliberately chose to “keep [him] in check”, avoiding the irrationality that too much capital can induce. The core theme was “last-mile fintech”: consumer-facing financial apps bridging legacy institutions and digital-savvy users. Within that mandate, Ribbit identified a handful of “category-defining” investments that could anchor the portfolio. Even in this first fund, Malka’s system thinking was evident – he devoted a slice of capital to a direct Bitcoin position as a strategic exposure (more below) and simultaneously backed startups solving Bitcoin’s on/off ramps (e.g. Coinbase). Fund I’s LPs were mostly high-net-worth allies of Malka, plus two forward-thinking banks (BBVA and SVB) willing to bet on fintech outsiders. Ribbit kept the portfolio concentrated (~12 companies) and globally diverse. Every investment had a role in a broader puzzle: for example, one early deal, ContaAzul (Brazil), addressed SME accounting in an emerging market – planting a flag in Latin America’s fintech ecosystem alongside the U.S. bets.

Ribbit Capital

By Fund II (2014, ~$125 million), Ribbit’s success and Malka’s reputation attracted blue-chip backers – major endowments (Emory, MIT, Duke), family offices (Page family), and venture fund-of-funds (Sequoia Heritage, Iconiq). This institutional LP base signaled trust in Ribbit’s system. Fund II’s theme was a natural extension: double down on the emerging winners from the first fintech wave and expand into adjacencies. In practice, that meant larger checks into companies showing product-market fit (e.g. Ribbit participated in follow-on rounds for its Fund I stars) and new bets in areas like low-cost stock trading and alternative credit. The firm still avoided chasing fads; as Malka put it, “fintech, as we’ve known it, is dead” – meaning simplistic app clones were not enough. Instead, Fund II zeroed in on fintechs with network effects or unique infrastructure. A prime example: Robinhood, which Ribbit backed in 2014. Rather than view Robinhood as just another brokerage app, Ribbit saw a systemic shift – a generation expecting zero-fee, mobile-native finance – and made sure to be part of it. (Notably, Malka joined Robinhood’s board early, reflecting Ribbit’s hands-on commitment.) Fund II’s portfolio was still tightly curated, but it contained future blockbusters (Robinhood, Credit Karma) and set the stage for Ribbit’s role as a heavyweight co-investor in later rounds

Fund III (2016, ~$226 million) solidified Ribbit’s position as the fintech specialist. Its theme was “global scaling” – identifying the fintech disruptors in every major region and supporting them into the late stage. By now, fintech had produced several multibillion-dollar companies, and Ribbit had stakes in many. With Fund III, Ribbit consciously took on a system-wide perspective: Malka often noted that “every country will have its Nubank or Revolut” – i.e. a next-gen bank challenging incumbents. So Fund III backed Nubank (Brazil) and Revolut (UK) almost in parallel in 2016, recognizing the pattern that banking was ripe for disruption in any market with tech-enabled consumers. Likewise, Fund III invested in fintech infrastructure plays (e.g. Ripple, a blockchain network for cross-border payments) to cover the less visible layers of the system. With a larger fund, Ribbit also could lead rounds and write bigger checks, but it maintained discipline: an analysis of Ribbit’s early funds noted that public data on its holdings is sparse, implying Ribbit kept a low volume, high-conviction approach. Importantly, Ribbit was difficult to analyze from outside because it didn’t publicly herald every deal. This was by design – the firm avoided hype, preferring to build quietly.

Case Studies: Three Bets That Define the Method

Ribbit’s investment philosophy is most clearly expressed not through abstract theses, but through how it behaves in decisive moments. Three investments in particular — Coinbase, Robinhood, and Nubank — illustrate Ribbit’s core method across different geographies, cycles, and regulatory regimes. Each reflects a consistent pattern: early conviction in structural infrastructure, deep operational involvement, and long-term alignment through volatility.

1. Coinbase

Ribbit’s participation in Coinbase’s 2013 Series A remains one of the clearest examples of its system-level thinking. At the time, Bitcoin traded below $100, crypto was widely dismissed as speculative, and most VCs viewed exchanges as tactical, low-moat businesses. Ribbit reached a different conclusion.

Coinbase - Logo

![]()

Micky Malka’s conviction did not originate from narrative enthusiasm, but from direct exposure. Ribbit’s first fund had invested directly in Bitcoin earlier that year, revealing practical frictions around custody, security, and fiat conversion. Coinbase addressed precisely those bottlenecks. Internal Ribbit materials from the period framed the company not as a crypto startup, but as “financial infrastructure”: storage, on-ramps, compliance, and trust.

Ribbit joined the round led by Union Square Ventures as a strategic investor rather than lead, focusing on regulatory positioning and global credibility. Malka became closely involved, advising the company through early compliance challenges and helping establish legitimacy with regulators and institutional partners. This role mattered because Coinbase’s ambition was global from inception, not confined to Silicon Valley norms.

By Coinbase’s direct listing in April 2021, Ribbit reportedly still held roughly 4 percent of the company. That position alone was worth several billion dollars, exceeding the size of Ribbit’s entire first fund many times over. More important than the magnitude of the return was the validation of Ribbit’s thesis: crypto was not peripheral to fintech, but foundational to its future. Coinbase became the category-defining institution, not simply a successful startup. Ribbit’s early willingness to treat crypto as durable financial plumbing, rather than a speculative edge case, defined its long-term edge.

2. Robinhood

If Coinbase demonstrates foresight, Robinhood illustrates Ribbit’s relationship-driven model and its tolerance for maximum-risk moments. Ribbit invested in Robinhood’s Series A in 2014, drawn to a simple but powerful idea: removing friction and fees from retail investing. The mission resonated deeply with Malka, shaped by his experiences with financial exclusion in emerging markets.

Robinhood - Logo

![]()

Ribbit’s early check was modest relative to later outcomes, but Malka joined the board and became deeply involved with the founders. As Robinhood scaled, Ribbit remained consistently supportive, helping navigate product, regulatory scrutiny, and public perception as the company grew into a mass-market platform.

The defining test came in January 2021 during the GameStop volatility. Robinhood faced a sudden clearinghouse capital call that threatened its ability to operate. Over a single weekend, the company required emergency financing to remain solvent. Ribbit led a $3.4 billion rescue round, providing the majority of the capital and underwriting the firm at its point of maximum uncertainty.

This decision was not driven by short-term optics or valuation protection. It reflected Ribbit’s belief that venture capital, at its highest level, means standing behind companies precisely when others step back. Months later, Robinhood completed its IPO at a roughly $32 billion valuation. Ribbit’s stake was worth about $1 billion, but the more durable outcome was reputational: founders across fintech internalized that Ribbit does not abandon companies in crisis.

Robinhood therefore represents more than a financial success. It demonstrates Ribbit’s method of long-duration partnership, where trust, board-level involvement, and crisis support are treated as strategic assets rather than optional extras.

3. Nubank

Ribbit’s investment in Nubank exemplifies its global thesis and its ability to translate fintech patterns across markets without imposing uniform solutions. Founded in Brazil to challenge an entrenched banking oligopoly, Nubank aligned naturally with Malka’s prior experience operating financial businesses in Latin America.

Nubank - Logo

![]()

Ribbit invested meaningfully by the mid-2010s, joining the board and supporting Nubank through regulatory engagement, executive hiring, and late-stage financing. While initial ownership was never dominant, Ribbit positioned itself as a trusted long-term partner during Nubank’s rapid expansion across Brazil, Mexico, and Colombia.

By the time Nubank went public in 2021 at a valuation exceeding $40 billion, Ribbit’s stake had diluted but still represented a fund-defining return. More importantly, Nubank validated Ribbit’s belief that the next generation of global financial institutions would not emerge exclusively from the United States. The company demonstrated that world-class fintech could be built in emerging markets if regulatory strategy, product design, and local culture were properly aligned.

Unlike more prescriptive investors, Ribbit adapted its involvement as Nubank scaled, shifting from early-stage partner to late-stage institutional backer while maintaining influence. Nubank remains a strategic reference point for Ribbit’s activity in Latin America and beyond.

The Token Factory Thesis, De-mystified

Ribbit’s so-called “Token Factory” thesis can sound abstract – tokens, agents, knowledge-money – but at its core it is Ribbit’s blueprint for the next decade. In simple terms, Malka and team believe every asset or claim of value will eventually live on a blockchain (as a token), and every user will eventually leverage AI “agents” to interact with these tokens. This worldview dissolves the distinction between “crypto” and traditional finance; as Malka quips, “crypto stops being a separate category as everything becomes tokenized”.

Here’s the breakdown of the thesis:

Money with Knowledge: Ribbit posits that money itself is becoming smarter – able to carry context, rules, and logic. Today, a dollar is dumb (it can be spent but doesn’t know who owns it or what conditions are attached). In contrast, a tokenized dollar (say a stablecoin or CBDC) could embed programmatic rules (only spendable on certain goods, or auto-repaying a loan on due date). Malka calls this marrying of value + context “money needs knowledge”. It echoes the Endeavor interview where he said the next phase after access is personalized finance: apps that adapt to your life stage and data. Tokens enable that by making money carry its own metadata.

Token Taxonomy (Identity, Asset, Expert): Ribbit’s thesis identifies categories of tokens: identity tokens – verifiable credentials about people or entities; asset tokens – digital representations of value (from stocks to real estate to carbon credits); expert tokens – a novel idea of encapsulating human expertise or AI models into tradeable units. For example, an identity token could be your government ID or reputation score, which you selectively share to access services (think of India’s Aadhaar system, which has issued 1.3 billion digital identity tokens – a stat Ribbit cites). An asset token might be a share of a company or a Bitcoin – not new, but in Ribbit’s future everything from energy kilowatts to loyalty points could be tokenized. An expert token is more radical: imagine a piece of an AI or a human’s expertise that can be invoked via a token (similar to how OpenAI’s API access could be tokenized). Ribbit believes these categories will blur the lines between fintech, edtech, healthtech, etc., because all become “token tech.”

Agents and Automation: The other side of the thesis is AI agents. With the explosion of large language models and automation, Ribbit foresees a world where personal AI agents handle routine financial decisions – from budgeting to investing – and even negotiate or execute transactions on your behalf. These agents need two things: access to tokens (to move value) and access to data/knowledge. Ribbit’s thesis suggests that tokens will carry the data agents need, enabling what Malka calls “agentic commerce.” For instance, a smart contract might hold your money but release it based on an AI agent’s decisions (perhaps an agent that monitors market conditions to invest). Ribbit is essentially wagering that finance will be increasingly autonomous, and that platforms enabling trust in these agents (through on-chain transparency, security, etc.) will thrive. Malka’s comment that he spends time with 21–23-year-olds who are AI-native hints that Ribbit is scouting founders who intuit this agent-driven future.

Rebels vs. Status Quo: In the June 2025 Token Letter, Ribbit frames the narrative as “rebels fighting the Status Quo”. The Status Quo (big banks, big tech, entrenched intermediaries) rely on scale, regulatory capture, and closed data to maintain power. But the “weapons” to disrupt them – ubiquitous mobile internet, public blockchains, open AI models – are now in the hands of small teams globally. “Tokens will be their weapons of choice,” Ribbit writes, and agents a powerful antidote to incumbents’ advantages. This almost revolutionary language underscores Ribbit’s stance: the firm sees itself as funding a financial insurgency. It’s reminiscent of early fintech rhetoric (startups vs. banks), but updated for a tokenized world. A concrete example: traditional banks profit from information asymmetry (e.g. your credit score, your identity). A rebel startup might issue an identity token that flips the model – you control your credit data and banks bid for it. That could erode incumbents’ moats. Ribbit’s role, implicitly, is to back those rebels and help them scale before incumbents react.

Everything is a Token – Simplified: As Malka succinctly put it in a recent conversation, “Everything is a token. We call it the token factory revolution – tokenizing information, money, and power.”. In practice, tokenizing information means your personal data or credentials become portable and monetizable by you (not locked in Big Tech silos). Tokenizing money means any store of value can move as freely as an email, 24/7, with built-in rules (today’s financial contracts become tomorrow’s smart contracts). Tokenizing power implies that decision rights or governance (say in a network or a community) can be distributed via tokens (this aligns with the rise of DAO governance tokens in crypto). If this sounds sweeping, it is – Ribbit essentially sees tokens as a new atomic unit of society’s transactional infrastructure.

For investors, demystifying this thesis means spotting where Ribbit is placing bets today. The firm is reportedly loking at ventures in decentralized identity (making KYC cheaper and reusable – a need highlighted by the $115 million+ banks spend on KYC compliance on average), in embedded finance AI (startups that use LLMs to give personalized money advice – fulfilling the “money with context” vision), and in infrastructure bridging traditional finance to crypto (e.g. stablecoin issuers, tokenized asset exchanges). Ribbit is also interested in companies that help incumbents tokenize – ironically, the letter even suggests banks might become issuers of verified identity tokens (turning a cost center into revenue). This is a nuanced stance: Ribbit isn’t maximalist to the point of excluding incumbents; if anything, they believe incumbents who embrace tokenization could thrive (and those who don’t will perish).

Capital Formation at Internet Speed

A central implication of Ribbit Capital’s thesis is how “capital at internet speed” reshapes venture capital itself. If capital can form and move globally in days rather than months, the traditional VC role as a gatekeeper weakens. During the 2021–2023 crypto cycle, meme tokens demonstrated this vividly: global retail capital coordinated almost instantly around narratives and attention rather than fundamentals. While many investors dismissed this as noise, Micky Malka interpreted it as signal: attention has become a form of currency, and capital increasingly follows distribution and narrative velocity.

Ribbit’s conclusion is not that VCs should fund speculation, but that founders now have alternatives to slow, staged fundraising. Token launches, community financing, and hybrid models allow strong teams to raise capital quickly, shifting leverage away from traditional venture firms. In Ribbit’s internal framing, capital is no longer scarce; trust, brand, and attention are. This inversion explains Malka’s emphasis on Ribbit’s reputation as more than capital, a signal of expertise, regulatory depth, and long-term partnership.

Operationally, Ribbit is adapting in three ways. First, it moves faster and with more flexibility, aligning with crypto-native deal norms. Second, it is open to on-chain participation, including token rounds alongside equity. Third, it prioritizes value-add beyond capital, particularly regulatory support, hiring, and market structure guidance, as ownership dilution pressures increase. Malka has suggested that token-native companies may achieve higher capital efficiency, fewer employees, and lower dilution, forcing VCs to justify their role more clearly.

More broadly, internet-speed capital blurs private and public markets. Some startups now reach liquidity immediately through token issuance rather than after years of VC rounds. Ribbit’s strategy is to avoid disintermediation by positioning itself as an ally, advising founders on structure, acting as anchor capital, or supporting market design rather than simply writing checks.

Ribbit Capital: Forward Positioning and Next Decade Playbook

Looking ahead, Ribbit Capital is positioning for a financial system shaped by two forces that appear contradictory but are central to Micky Malka’s worldview:

- consolidation among winners, and

- expansion into entirely new financial domains.

In Malka’s framing, the next decade will produce a small number of dominant fintech platforms, while crypto- and AI-native sectors create new greenfield opportunities in parallel.

Backing the New Financial Institutions

On the consolidation side, Ribbit expects early fintech fragmentation to give way to a smaller group of fintech-native platforms that become systemically important.

Companies such as PayPal, Square, Nubank, and Robinhood are no longer viewed as challengers, but as the next generation of financial institutions that compound influence over time.

Several structural forces reinforce this view:

- Regulatory attitudes have shifted from skepticism to selective endorsement of proven fintech operators.

- Winners increasingly receive licenses, charters, and regulatory clarity that widen the gap with smaller competitors.

- Capital markets reward scale, distribution, and compliance readiness.

Ribbit’s historical behavior suggests it will double down on these winners through follow-on capital, late-stage support, and long-term partnership. This could include growth-focused vehicles, special purpose structures, or selective public-market exposure where Ribbit believes it has an informational edge.

Expansion: Investing Into New Financial Frontiers

At the same time, Ribbit is actively repositioning toward new domains where finance is being redefined rather than merely optimized.

Three areas stand out.

Crypto Infrastructure 2.0 - Despite post-2022 drawdowns, Ribbit remains structurally bullish on crypto. The focus has shifted toward next-generation infrastructure: faster settlement, lower transaction costs, and systems that operate at internet-scale speed. Priority areas likely include exchanges, custodians, cross-border payments, and stablecoin rails, particularly in emerging markets where crypto solves real economic frictions such as inflation and capital controls.

AI-Native Financial Interfaces - Ribbit’s recent writing points to a belief that finance will become increasingly agent-driven. This includes AI systems that manage portfolios, optimize cash flows, or act as financial decision-makers on behalf of individuals and businesses. The implied bet is that the next wave of fintech founders will be AI-native and will design products where software, not humans, is the primary financial actor.

Embedded Finance and Digital Identity - As finance becomes modular, Ribbit appears interested in companies embedding financial services into non-financial contexts such as commerce, telecom, or creator platforms. Closely linked is digital identity. Ribbit has emphasized that identity is evolving into a financial primitive, enabling access, trust, and transaction capability across systems. This opens investment space in credential networks, global KYC infrastructure, and identity wallets that function across borders and platforms.

Tokenization Beyond Traditional Finance

Another signal of Ribbit’s forward positioning is its interest in tokenized assets beyond conventional finance.

Malka’s involvement with Node, focused on CryptoPunks and digital art, reflects a broader thesis rather than a side project. Digital collectibles are viewed as an early example of how new asset classes emerge, gain liquidity, and eventually require financial infrastructure such as marketplaces, custody, lending, and risk management.

This fits Ribbit’s longer-term view of the financialization of everything: art, gaming, work, identity, and online interaction increasingly represented through tokens. As this expands, the definition of fintech widens accordingly.

Ribbit’s hiring and research orientation suggest it is building internal understanding across culture, crypto, and technology to stay ahead of these shifts.

Geographic Expansion: Emerging Market Leverage

Geographically, Ribbit is expected to increase focus on India, Southeast Asia, and parts of Africa.

Malka has repeatedly highlighted India’s real-time payment infrastructure as a global benchmark. While Ribbit historically centered on the Americas and Europe, mobile-first financial systems in high-growth regions now offer scale, regulatory momentum, and rapid unicorn formation.

With over $14 billion in assets under management, Ribbit has the capacity to deploy larger checks in these markets and support companies through multiple stages of growth.

Fund Strategy and Firm Structure

From a capital formation perspective, Ribbit is likely to raise another flagship fund in the near term, potentially exceeding $1 billion. While this may test the firm’s historical discipline around fund size, the breadth of opportunity across tokens and AI-driven finance provides a rationale for scale.

One element that is unlikely to change is Ribbit’s tight partnership model. Rather than expanding into a multi-partner platform, the firm continues to center decision-making around Malka and a small group of long-tenured partners. This concentration remains part of Ribbit’s identity and appeal to LPs.

Summary: Ribbit’s Forward Playbook

Ribbit’s strategy can be summarized in two parallel tracks:

- Strengthen the incumbents of the future, supporting platforms like Robinhood and Nubank as they mature into global institutions.

- Incubate the insurgents of the future, backing token- and AI-native companies reshaping identity, payments, markets, and financial interfaces.

Few firms attempt to operate at both ends of this spectrum. Ribbit’s track record suggests it has earned the right to try.

🐸

Sources

- https://www.reuters.com/

- https://aum13f.com/firm/ribbit-management-company-llc

- https://www.lavca.org/ribbit-capital-debuts-with-100m-early-stage-fund/

- https://www.ribbitcap.com/

- https://postcardsfromistanbul.substack.com/p/allocators-notebook-ribbit-capital?utm_source=substack&utm_campaign=post_embed&utm_medium=web

- https://www.youtube.com/watch?v=pdFfT8dXU7E

Token Letter by Ribbit Capital (2025)

Cover Artwork

Four studies of a frog

Jacques de Gheyn, 1600 - 1604

Disclaimer

This institutional research note was prepared by insights4vc and is for informational purposes only. It is not investment advice or an endorsement of any specific security or strategy. All information herein is sourced from public filings, credible media, and internal notes believed reliable, but accuracy and completeness are not guaranteed. Opinions expressed are the author’s own, reflecting analysis of cited sources and subject to change.

Neither insights4vc nor the author has any affiliation with Ribbit Capital or the companies mentioned, and we do not hold any financial interest in them at the time of writing. This report contains forward-looking statements which are speculative in nature. Readers should conduct their own due diligence or consult professional advisors before making any investment decisions. The author and publisher assume no liability for any errors or omissions or for any actions taken based on the information herein.