FOMO is trying to answer a question that extends far beyond crypto trading: what happens when financial activity becomes social by default?

The company has built a noncustodial consumer trading application that combines embedded wallets, multichain spot execution, perpetual futures and a public feed of verified trading activity. Instead of asking users to manually publish screenshots, performance claims or market opinions, FOMO can turn transactions executed through its platform into persistent social content.

That distinction has attracted significant attention. Since its formation in 2024, FOMO has announced approximately $94 million in financing, including a $75 million Series B led by Index Ventures, with Union Square Ventures and Benchmark participating. The round reportedly valued the company at $550 million and placed FOMO among the most heavily funded emerging consumer platforms in onchain finance.

The growth figures are equally striking. By June 2026, FOMO reported more than 600,000 users, over $4 billion in cumulative trading volume, 110 million social interactions and 68,000 first-time crypto buyers funded through Apple Pay. Public protocol data also indicates a sharp recent acceleration in both spot and perpetual trading activity.

But the central investment question is not whether FOMO can build a fast-growing trading interface. It is whether the company can transform trading activity into a durable financial social graph.

Most of FOMO’s execution infrastructure is provided by external partners, including Privy, Coinbase, Hyperliquid, Trade[XYZ], market-data providers and routing infrastructure. Its potential defensibility therefore sits above execution: in the connections between identities, transactions, followers, notifications, written theses, discovery history and reputation.

That moat remains unproven. The company has not publicly disclosed cohort retention, follower concentration, discovery-to-trade conversion or the extent to which users engage with the platform when they are not actively trading. FOMO’s chief executive has also acknowledged that the product remains considerably more trading-heavy than social. Meanwhile, Robinhood, Coinbase, Phantom, eToro and other platforms are moving toward increasingly similar combinations of execution, verified activity and social discovery.

This report examines FOMO as a company, product, trading platform and emerging financial network. It evaluates the founders, product evolution, user growth, protocol economics, investor base, competitive positioning and regulatory risks. Most importantly, it asks whether FOMO is building a genuinely defensible social layer for global finance, or an effective consumer interface operating on increasingly commoditized infrastructure.

From Solana Trading App to Financial Social Network

FOMO's history is unusually compressed. Public corporate records identify FOMO Labs Inc. as a Delaware corporation formed in 2024, with Paul Erlanger and Se Yong Park listed as directors in a later securities filing. The public record reviewed for this report does not establish an exact incorporation date. FOMO announced a $2 million pre-seed on February 18, 2025, before the product was public, and a March preview described a forthcoming noncustodial social trading application that would associate visible trades with user identities.

Paul & Se - Empire Podcast by Blockworks

That chronology matters because the social thesis was not merely attached after early memecoin success. Before launch, FOMO was already arguing that financial influencers could selectively disclose winners while hiding losses and that verified execution could make reputation more credible. However, the first product was narrower than today's narrative: a mobile-first, Solana-only application optimized for simple access to long-tail tokens. The public beta launched on May 6, 2025. Its immediate wedge was therefore best described as simplified Solana trading with social primitives, not yet a general financial network.

Product breadth expanded rapidly. Base and a unified multichain balance appeared by September 2025; BNB Chain, richer profit-and-loss displays, comments and average holding time followed in October; Monad and redesigned profiles arrived in November; trade-linked theses and a new Coinbase-native Apple Pay integration were highlighted in January 2026; and messages followed in February. TradingView charts launched in April, the web application on April 29 and perpetual futures on June 11. A May company article separately named Ethereum, but public materials do not document when or whether all features became available there. The sequence shows an expanding brokerage surface and an increasingly explicit social layer developing together.

Selected chronology

Source: Company announcements, product recaps, SEC filings and contemporary reporting cited throughout Section 1. Evidentiary qualifications are preserved in the final column.

The historical record supports a qualified interpretation of product evolution. FOMO began with a memecoin-adjacent access problem: consumers often encountered an asset through a creator but could not navigate wallets, bridges, gas and unfamiliar DEX interfaces. It then generalized that observation into a larger claim about discovery. The social framing was present before launch, but the full "financial social network" ambition became more operationally visible only after feeds, holding statistics, theses, comments, web access and perps accumulated. That distinction prevents a successful trading wedge from being mistaken for proof of the broader network.

The Founders and the Product Philosophy

FOMO was founded by Paul Erlanger, Se Yong Park and Prashan Dharmasena. Their backgrounds combine market structure, business development, ecosystem work and consumer mobile engineering. That mix helps explain why FOMO feels less like a protocol console and more like a social consumer application sitting above protocols.

Erlanger's public profile shows more than three years at dYdX, from July 2021 to October 2024, most recently as head of business development. Before crypto, he worked in private credit at Deutsche Bank and studied at New York University, where his profile notes summa cum laude honors. At dYdX he operated close to decentralized derivatives, partnerships and institutional market structure rather than as a retail product engineer.

Park worked with Erlanger first at Deutsche Bank and later at dYdX, a relationship Index describes as spanning roughly five years. Public biographies associate him with Yale and with ecosystem roles at dYdX and later Eclipse. The exact title and full dates of every dYdX role were not consistently recoverable from primary records, so descriptions such as "about four years" should be treated as rounded founder context rather than exact employment history.

Dharmasena supplies the mobile product and engineering lineage. His public profile lists Android engineering at Square, head of mobile at OpenSea and head of mobile and frontend platform at dYdX in 2024. A Berkeley alumni profile identifies a BA in electrical engineering and computer science. Public sources identify him as FOMO's engineering co-founder, although they do not document individual authorship of the first application build.

FOMO's product embodies a tension between the experienced trader and the consumer who does not know what a wallet or gas fee is. The former demands speed, asset coverage and credible execution; the latter needs a cash-like balance, understandable language and minimal configuration. That tension appears in observable choices: USDC is presented as cash, wallet creation is embedded in account signup, the application sponsors gas, and public flows emphasize a single buy or sell action rather than chain selection and manual execution parameters.

The team remained small at the Series B. Fortune reported 17 employees in June 2026. Public profiles identify finance and operations, growth and user-generated-content leadership alongside a heavily technical hiring plan. In a public interview, Erlanger described the organization as deliberately flat, with an early core team working on equity-heavy terms. No clearly identified in-house compliance or regulatory executive was found in the reviewed public profiles, although absence from public search is not proof that the function is absent.

This team is well suited to rapid product assembly on outsourced infrastructure. It understands perpetual market structure, partner ecosystems and consumer mobile design. The inverse risk is also visible: an engineering and growth-heavy organization can expand faster than its public governance, measurement and regulatory apparatus. FOMO's next stage requires not only product velocity but stronger proof systems around user quality, social integrity and jurisdictional controls.

The Core Thesis: Crypto Is Infrastructure, Not a Consumer Category

FOMO's most consequential idea is that consumers should not have to choose to become "crypto users." Blockchain is treated as a back-end technology offering two properties: globally distributable assets and publicly inspectable activity. On this view, the consumer category is trading or investing, while chains, wallets and bridges are implementation details.

The first property, global distribution, is already useful. A token can become tradable on a permissionless venue before a traditional broker would list it, and an embedded-wallet application can route a consumer to that venue. FOMO exploited this with long-tail Solana assets and later added multiple chains. The second property, transparent activity, is strategically more ambitious. If transactions can be attributed to persistent user identities, the application can turn entry, exit, holding behavior and realized performance into a continuous information feed.

The often-invoked comparison to Robinhood, Instagram and X is directionally helpful but incomplete. Robinhood contributes simplified execution, Instagram contributes profile-led visual consumer design, and X contributes a follower-based information graph. Yet FOMO does not fully inherit any of their strengths. It lacks Robinhood's regulated multiasset brokerage, Instagram's mature creator culture and X's vast interest graph. Its distinctive contribution is narrower: execution and social identity are joined by default, so a user need not manually publish every trade.

This makes the proposition more precise: Twitter can record a claim about a position, while FOMO can record a position opened through FOMO. That is stronger evidence, not complete financial truth. A trader may split capital across several FOMO accounts, use outside wallets or exchanges, hedge with options, short elsewhere, or display a small visible position while holding a larger offsetting exposure. A pseudonym may also be misattributed, transferred or coordinated with other accounts. Public execution narrows the scope for selective disclosure inside one account but cannot reveal a whole portfolio.

The company therefore should be understood as building an authenticated activity graph, not a comprehensive financial identity system. This distinction is central to assessing both product value and risk. Even partial activity can be useful for discovery if the interface clearly defines its boundaries. It becomes misleading when followers interpret a public account's history as the trader's complete wealth, conviction or risk-adjusted record.

Product: Hiding the Blockchain

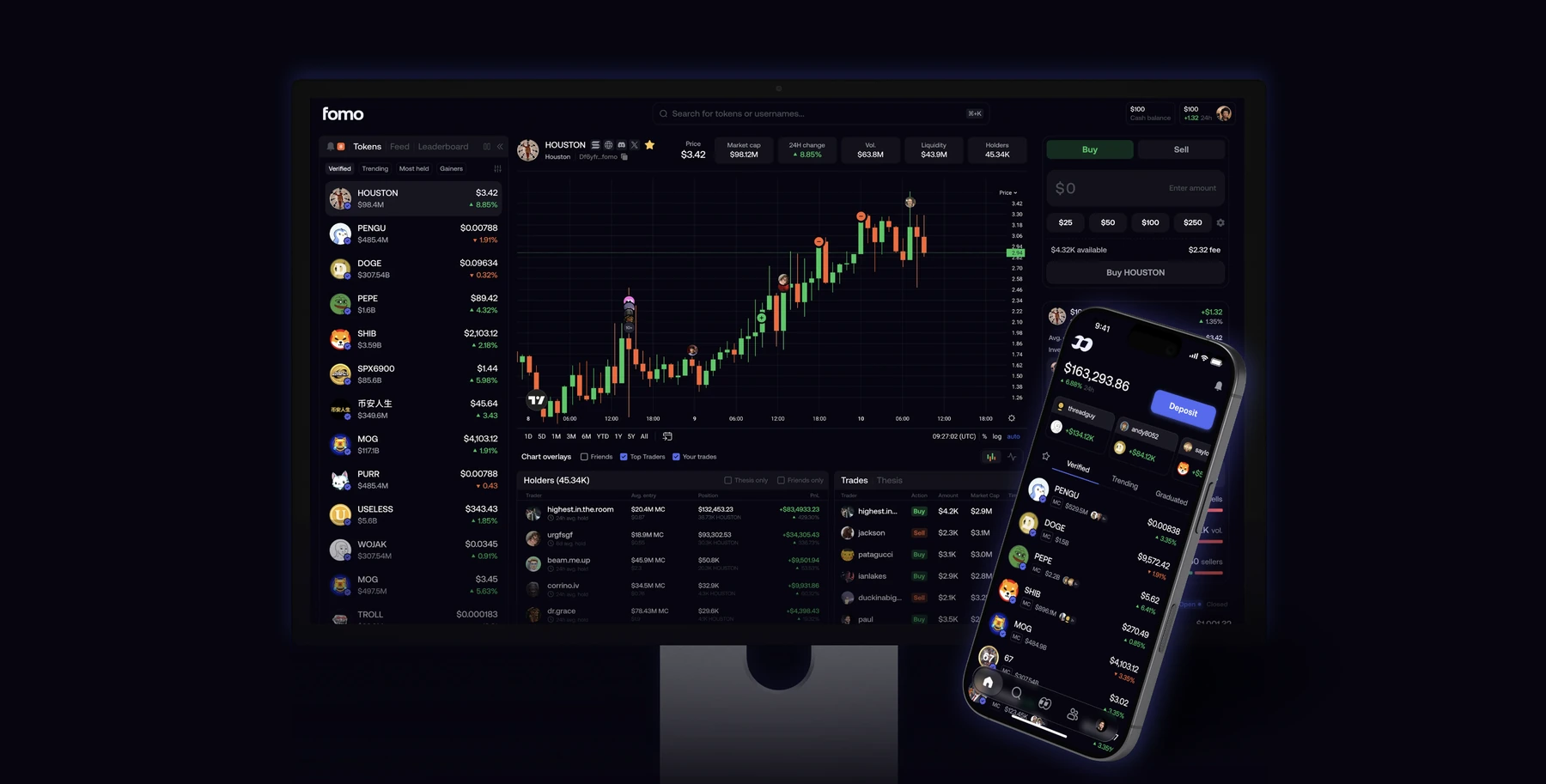

For a new user, FOMO's intended journey resembles a consumer brokerage. The user downloads the iOS or Android application, or opens the web product, signs in with email or an Apple account, and receives an embedded wallet. Funding can occur through Apple Pay or debit card on mobile, subject to availability, or through supported crypto deposits. The application presents a USDC-denominated balance and a cross-chain asset catalog. A user can search for a token, inspect activity and holders, enter an amount and trade without manually selecting a venue or paying gas in a native token.

The account is noncustodial in the technical sense described by FOMO and Privy. Privy creates an embedded wallet using key-sharding and secure execution technology; FOMO says users can export keys. On EVM networks, the company describes smart-account features such as gas sponsorship. This removes a seed phrase from onboarding but does not remove wallet risk. The terms state that exported private-key material is transmitted by Privy and place responsibility for key security on the user. The architecture is therefore better called embedded self-custody than a traditional custodial brokerage account.

Official product guides consistently identify Solana, Base, BNB Chain and Monad as the core spot networks. A separate May 2026 company article also lists Ethereum, suggesting a recent or limited addition whose feature parity is not publicly documented. The web and mobile applications share accounts, balances and positions. Crypto funding instructions specify USDC deposits on supported networks, while mobile onramps can abstract the conversion. Withdrawals can be made to external crypto addresses, and cash withdrawal availability varies by region.

USDC as the visible cash balance is a meaningful product decision. It prevents a consumer from having to hold SOL or ETH merely to transact and makes profit and loss easier to understand in dollar terms. It does not eliminate stablecoin, issuer, smart-contract or depegging risk, nor does it eliminate exposure created during routing. Gas sponsorship also shifts rather than erases cost: FOMO absorbs or bundles network and priority fees, improving conversion but exposing the company to spikes, abuse and thin unit economics on small trades.

The trading surface is intentionally constrained. FOMO's own comparison with Phantom says users receive less granular control over routing and slippage than they would through a direct DEX interface. That reduces cognitive load but transfers responsibility to the application's routing and protection defaults. Public documentation does not disclose audited execution-quality statistics or a comprehensive policy for favorable price improvement. In illiquid or volatile tokens, users still face price impact, stale quotes, MEV and failed transactions even when the controls are hidden.

FOMO's current terms disclose a spot fee of at least 0.50 percent per buy or sale and a $0.95 minimum, while reserving the possibility of alternative rates. Earlier TechCrunch reporting described the minimum as applying only to Solana, but the later terms use broader language and are the more relevant current source. The minimum creates a sharp small-ticket effect: a $10 order paying $0.95 bears a 9.5 percent explicit fee before price impact. This is the clearest example of blockchain complexity being replaced by consumer simplicity at a potentially high economic price.

The central interface is a token or position sheet. Public guides show price charts, holder and safety information, trending or verified filters, recent social activity and transaction controls. Profiles can display portfolio and transaction history, volume, followers, performance and an equity curve. Feed items can identify a buy, sale or fully closed position, the amount, price movement and realized profit or loss. A user can follow a trader, turn on notifications, inspect the position history and then execute independently.

Perpetuals are a separate, higher-risk experience available outside the United States. FOMO connects to Hyperliquid and Trade[XYZ] markets, exposing crypto, pre-IPO, equity, index and commodity-linked perpetual contracts where available. The application displays long or short direction, leverage, notional exposure, margin, take-profit and stop-loss controls. The fee is 0.05 percent in addition to protocol, gas and funding costs. The user-facing abstraction is elegant, but the economic exposure remains a leveraged derivative with liquidation, funding and oracle risk.

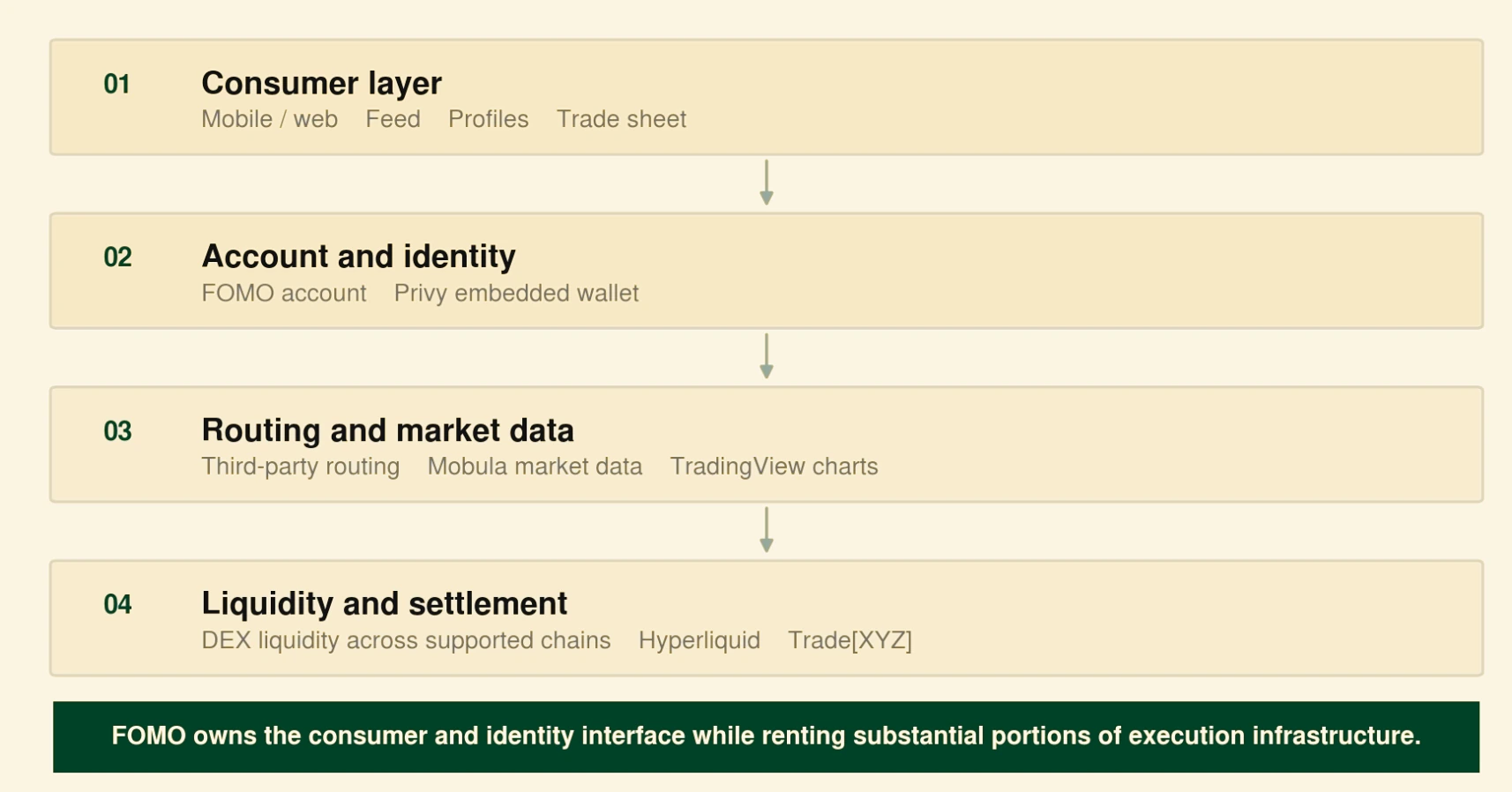

Simplified architecture

Source: insights4vc analysis based on FOMO, Privy, Mobula, TradingView, Hyperliquid and Trade[XYZ] documentation

FOMO is genuinely making onchain execution more understandable. It is also hiding, rather than abolishing, custody, market-impact and protocol risks. The appropriate standard is not whether a user sees the blockchain, but whether fees, execution quality, asset risk and loss mechanics remain intelligible after abstraction. Public app reviews offer anecdotal warnings about delayed orders, inaccurate P&L and login or deposit problems. They do not establish prevalence, but they show where the promise of a seamless brokerage can break.

When Trading Becomes Content

Most new social applications face a cold-start problem: no audience means little incentive to post, and little content means no reason to build an audience. FOMO partially changes that equation because the transaction can generate content automatically. A buy, partial sale, closed position, holding period or realized result can become a feed event even when the trader writes nothing. A trade thesis adds interpretation but is not required for the graph to move.

This is a real structural difference from FinTwit, Stocktwits or a conventional investing forum. Those networks begin with speech and may add unverifiable position claims. FOMO begins with an action executed through its own wallet surface and adds speech around visible activity. This automatic generation of trade events increases content density. In principle, each visible trade improves asset discovery, gives followers another behavioral observation and creates material for external share cards.

The information quality nevertheless varies. A large profit can reflect skill, leverage, early access, illiquidity, luck or the follower response itself. A profile-level win rate can be distorted by position sizing and by the treatment of open losses. Average holding time may distinguish fast speculation from longer conviction, but it does not reveal hedges. Percentage returns without dollar exposure can overstate economic importance; dollar exposure without total wealth can overstate risk. FOMO's terms reserve discretion to correct leaderboard manipulation, which acknowledges that even platform-recorded data can be gamed.

The available product evidence supports a substantial feature set: feeds, comments, follower notifications, activity profiles, share cards, trade theses, performance views and leaderboards. The June Series B announcement said some creators had more than 100,000 followers and cited trader Rohun Vora as an example. It also claimed 110 million unique social interactions. Neither the definition of an interaction nor the distribution of followers is public. There is no independently accessible table showing how many profiles have meaningful audiences, how concentrated the graph is, or how often followers act on a signal.

One passage in a June 2026 public interview is especially useful because it cuts against promotional inference. Erlanger said FOMO remained substantially more trading-heavy than social and argued that the company needed to build the social product intentionally. That admission is consistent with the evidence. FOMO has solved part of the content cold start, but it has not publicly proved the engagement, relationship depth or creator economics of a mature network.

Building a Financial Social Graph

The prospective flywheel is straightforward. Strong traders generate credible activity; consumers follow them; followers expand the trader's distribution and reputational capital; that audience attracts more traders; and the resulting graph improves discovery. The key insight is that mainstream users and sophisticated traders need not contribute symmetrically. A small supply of high-information accounts can serve a much larger audience.

There is early evidence for each component, but not yet for the closed loop. FOMO has attracted crypto-native traders, reported six-figure follower accounts, and distributed trade events to a consumer base. What is missing is longitudinal evidence that follower growth changes creator behavior in a healthy way, improves consumer decisions, lowers customer acquisition cost or keeps both sides active through a downcycle.

The graph's potential defensibility lies in data that is not simply onchain. Raw swaps are public. FOMO can still own the association between a wallet and a persistent human-facing identity, follow relationships, notification settings, written theses, comments, discovery paths and the sequence from impression to trade. These contextual links can become proprietary even when settlement is observable. They are also the inputs required to rank relevance rather than merely display activity.

Switching costs are currently modest. A popular trader may lose followers, profile history and engagement context by leaving, but the underlying transaction history remains visible onchain and the trader can maintain parallel identities on X, Robinhood, Coinbase, Telegram or other wallets. FOMO's terms say users do not own their usernames and grant only a revocable right to accounts, while no public export mechanism for followers or reputation was found. That may increase platform lock-in if the network succeeds, but it also gives creators a reason to diversify.

The most serious conceptual limitation is incomplete financial identity. A visible account can be only one sleeve of a strategy. Sophisticated users have the greatest incentive and ability to separate public trades from private hedges. Adverse selection may therefore weaken the graph: the best traders can decline visibility, delay activity or post only positions that benefit from attention. FOMO can authenticate what occurred through its interface, not why it occurred or what offsetting exposures exist.

Social accountability helps but does not eliminate manipulation. An established trader may have more long-term reputational value to lose than can be earned from one abusive trade, particularly in liquid markets. That discipline is weaker for pseudonymous accounts, newly popular creators, small-cap assets and coordinated groups, where a single exit can be lucrative and reputations can be restarted. Securities regulators repeatedly warn that apparent online consensus can be manufactured and that social investment information may be incomplete or misleading.

FOMO's product-specific guide says following a trader does not trigger automatic execution: the follower reviews the activity and decides whether to trade. A separate company education article uses "copy trading" in its conventional automated sense, creating a terminology inconsistency in FOMO's own materials. The product is therefore more accurately described as manual social trading. Preserving a decision point can reduce mechanical front-running and the chance that the service is characterized as discretionary portfolio management, but it does not remove advice, promotion or suitability risk. Social urgency can still make nominally independent execution highly imitative.

The appropriate description is therefore an emerging authenticated discovery graph. It is more credible than a feed of unsupported screenshots, but less complete than the phrase "financial identity" implies. Its value will depend on transparent statistics, manipulation controls and the ability to distinguish repeatable judgment from crowd-induced performance.

Users: Mainstream Scale, Crypto-Native Information

FOMO reports growth through several overlapping definitions. At the Series A in November 2025, it claimed 120,000 users and 35,000 traders, a 29 percent trader-to-user ratio, nearly 15,000 net-new crypto users and $5 million funded through the onramp. By June 2026, company and investor announcements cited more than 600,000 users and $4 billion of cumulative volume; USV used 625,000 users. These figures can be chronologically compatible, but they have not been audited and "user" may mean registration rather than funded or active account.

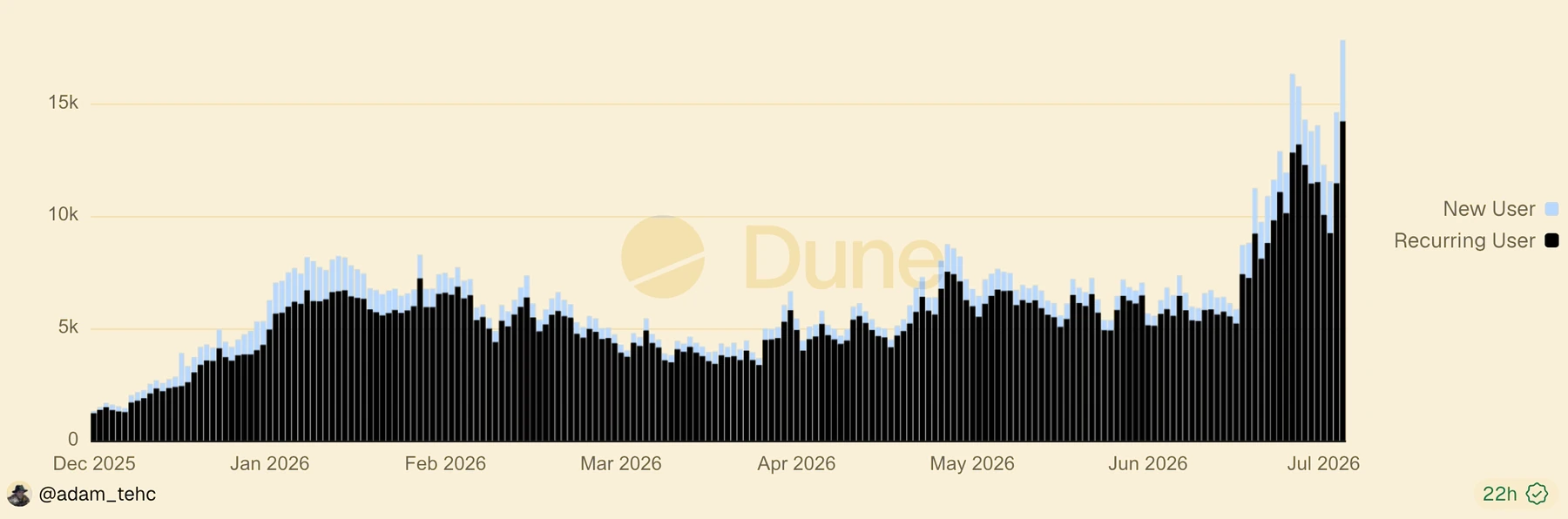

Daily Traders (Source: Dune)

The public figures support reach but do not establish the composition asserted in FOMO's broader thesis. The November trader-to-user ratio of roughly 29 percent is the only disclosed funnel ratio that can be calculated cleanly, and it reflects one observation point rather than a retained cohort. The 68,000 first-time crypto buyers suggest genuine mainstream onboarding, while six-figure creator audiences suggest a supply of higher-information accounts. FOMO has not publicly segmented volume, balances or retention between crypto-native and mainstream users, so the proposed two-sided network remains strategically plausible rather than quantitatively demonstrated.

Public app signals establish reach but not economic quality. Google Play showed more than 100,000 downloads and hundreds of reviews; the US App Store showed roughly 2,500 ratings and a high Finance-category rank at the observation point. These are volatile storefront measures. They do not disclose balances, geography, age, retention or whether one individual uses multiple accounts.

The company has not published a reliable geographic or demographic breakdown. The product is global in distribution, but perpetuals exclude US persons and sanctions restrictions are extensive. The first-time-crypto onramp data supports the claim that FOMO has reached beyond crypto-native power users, while the depth and durability of that consumer base remain uncertain.

Product-First Growth

FOMO's clearest publicly documented growth inflection followed the addition of Apple Pay shortly after launch. TechCrunch reported company figures showing that weekly revenue rose from roughly $5,000 to $150,000 and daily volume reached about $3 million after the integration. By November 2025, the company was reporting $20 million to $40 million of daily volume and roughly $150,000 of daily revenue. These are company figures relayed by a reputable publication rather than independently audited accounts, but they identify a credible product-market-fit mechanism: removing wallet funding friction converted external market interest into transactions.

This frames FOMO less as a creator of trading demand than an intent-capture and retention product. A consumer encounters an asset or trader elsewhere, opens FOMO to investigate, follows an account without depositing, and returns when a market event creates urgency. The product can therefore act as an information surface before it becomes a transaction venue, although FOMO has not published evidence separating informational users from funded traders.

Subsequent distribution combines referral economics, user-generated share cards, app-store discovery, sponsored creator media and product-triggered word of mouth. FOMO's affiliate page says more than $1.1 million has been paid to creators, with no public cap on payouts. In a June public interview, Erlanger described an in-house network of roughly 30 to 40 creators and an ambition to build a media capability around markets and financial education. The company also maintains a growing Learn library of explainers and trader interviews.

This strategy can create two loops. The first is transactional: trade, visible result, share card, external curiosity, profile visit, signup and future trade. The second is informational: follow a trader, receive notifications, learn an asset, then fund when intent rises. The second loop is strategically more valuable because it lets FOMO serve a user before monetization and can reduce dependence on constant paid acquisition.

Neither loop is publicly proven. FOMO has not disclosed the fraction of sign-ups from referrals, the percentage of share-card viewers who register, or the incremental retention of followers versus non-followers. The affiliate page's claim of more than $1.1 million paid also exceeds the approximately $746,000 of cumulative referral cost visible in DefiLlama's public quarterly table at the observation point. Different timing, coverage, bonuses or accounting scope could explain the gap, but the public sources do not reconcile it. Low protocol cost of revenue therefore cannot be equated with low customer-acquisition cost.

Creator sponsorship introduces governance obligations. Paid relationships should be conspicuously disclosed, and performance content should not imply that a visible account represents a complete portfolio. FOMO's distinction between paying creators to publish media and paying traders to trade may reduce direct signal distortion, but no complete public sponsorship roster, spend schedule or disclosure audit was found. Owned media could deepen education and brand, or it could become a high-cost acquisition channel whose economics disappear when speculative attention falls.

Trading Traction

DefiLlama provides the most useful public transaction snapshot, with important coverage limits. On July 15, 2026, its FOMO adapters showed $356.02 million of 30-day Solana DEX volume and $510.04 million of 30-day Hyperliquid perpetual notional. Because one adapter measures spot swaps and the other leveraged derivative notional, a simple non-overlapping sum is approximately $866.06 million. This is not verified total platform volume: the DEX adapter covers Solana rather than every supported chain, tracking start dates differ, and leveraged notional is not economically identical to spot turnover.

Perpetuals represented 58.9 percent of the 30-day sum and 51.5 percent cumulatively. The apparent anomaly that 30-day perps were 96.4 percent of cumulative perps is largely mechanical: perps launched on June 11, only about a month before observation. The comparable DEX ratio of 71.6 percent likely reflects recent adapter coverage and acceleration, not the whole history. Neither series reconciles directly with FOMO's company-reported $4 billion cumulative volume.

In a June 2026 public interview, Erlanger said FOMO had roughly 50,000 to 60,000 daily active users. That figure is not directly comparable with DefiLlama's trader addresses or the company's cumulative user count because the interview did not publish the event definition, bot filtering, platform coverage or measurement window. A public Dune dashboard exists, but its raw query results were not accessible during this review. The available evidence therefore supports growing activity without permitting an independent retention or recurring-trader calculation.

Business Model and Financial Economics

FOMO monetizes transactions. Current terms disclose at least 50 basis points per spot buy or sale, subject to a $0.95 minimum, and 5 basis points for perps plus external costs. Referral partners receive a discretionary share; FOMO also earns Hyperliquid builder-code fees by tagging orders that users authorize. Hyperliquid's design records the maximum approved builder fee and applies it at the order level onchain.

This pricing is neither directly comparable with a zero-commission broker nor uniformly expensive. Coinbase Advanced's lowest public tier was 40 basis points maker and 60 basis points taker, Phantom charges 85 basis points on selected swaps, and Robinhood's crypto routing compensation is embedded in market-maker spreads. FOMO's long-tail fee sits within consumer-crypto norms, but its minimum is punitive for very small orders and may face compression as routing commoditizes.

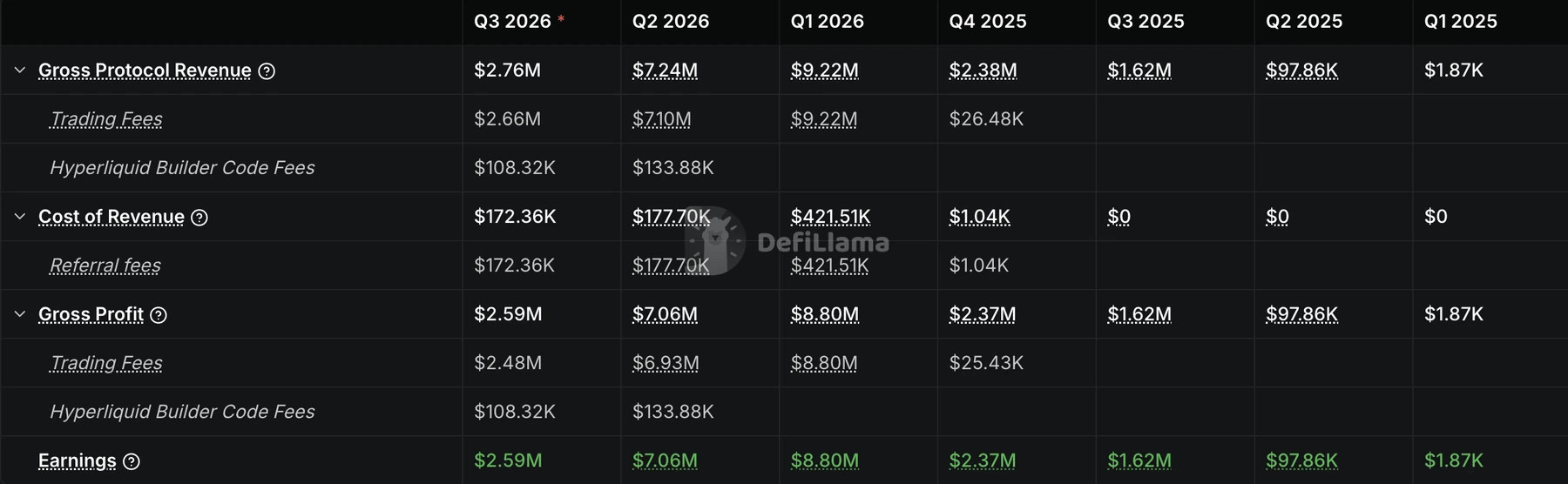

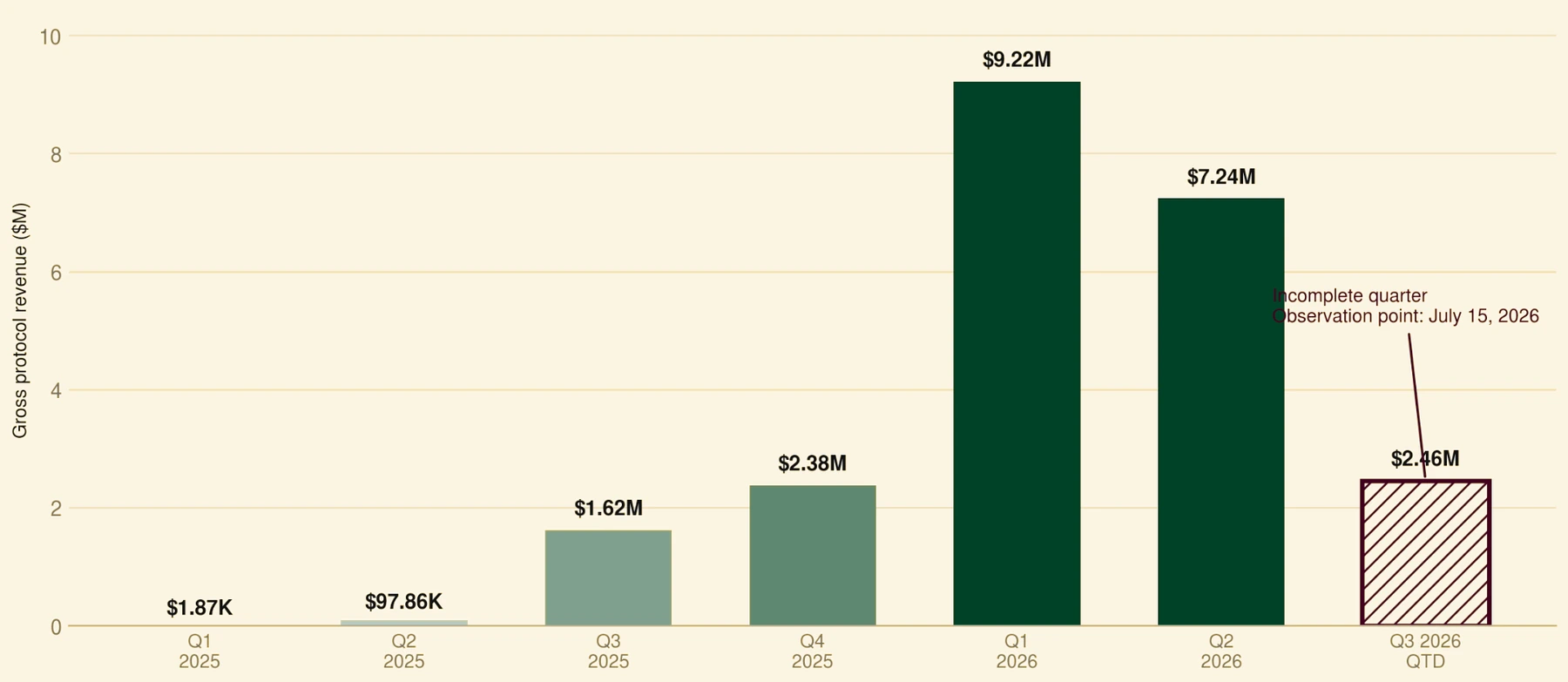

DefiLlama's public quarterly table reports $23.02 million of gross protocol revenue, $746,400 of referral cost and $22.26 million of protocol earnings across Q1 2025 through Q3 2026 to date, an aggregate gross margin near 96.7 percent.

Quarterly protocol economics

Protocol earnings are not GAAP net income. Payroll, legal, marketing, infrastructure and compliance expenses are not deducted in DefiLlama's protocol economics definition. Source: DefiLlama

Revenue grew roughly 16.6 times in Q3 2025, 46.9 percent in Q4 and 287.4 percent in Q1 2026, then fell 21.5 percent in Q2. Builder-code revenue contributed 1.85 percent of Q2 revenue and 4.09 percent of Q3 QTD; referral cost was 4.57, 2.45 and 5.94 percent in Q1, Q2 and Q3 QTD respectively. At the same July snapshot, 30-day protocol revenue divided by the two-volume sum implied roughly 43 basis points, but the adapters have different scopes.

The Q1 breakout occurred despite a weak broad crypto quarter: CoinGecko estimated a 20.4 percent fall in total market capitalization, while Galaxy reported declining Solana DEX activity. That divergence suggests company-specific user or monetization gains rather than simple market beta. Public data cannot isolate the Q2 decline among seasonality, asset mix, retention and fee effects.

DefiLlama defines protocol revenue as the portion of user fees retained by a protocol, closer to gross income than net profit. Payroll, legal, marketing, infrastructure and compliance are not deducted. "Earnings" in this dataset is therefore not GAAP net income, and company operating profitability cannot be established without audited or management accounts. Q3 is partial through the observation date and should not be annualized.

Hyperliquid and the Rented Infrastructure Strategy

FOMO owns the consumer interface while renting key rails. Privy supplies embedded wallets, Mobula supplies discovery data, Coinbase supports onramping, TradingView supplies charts, and Hyperliquid with Trade[XYZ] supplies perpetual markets. Spot orders are routed through third-party infrastructure and settle on underlying chains rather than a proprietary FOMO exchange.

This architecture speeds releases and limits capital intensity. The June 2026 launch of a broad perpetual product shortly after the web application illustrates the release velocity. The cost is dependency: partners control uptime, asset coverage, fee schedules and parts of execution quality. FOMO also lacks the direct liquidity, spread economics and operational control of an integrated exchange. Strategically, it can own the consumer while renting finance only if identity, discovery and service quality remain harder to replace than the routers below.

Fundraising and the Investor Network

FOMO has announced roughly $94 million in total financing. The $2 million pre-seed included more than 140 angels, designed as a cold-start network of traders, builders, testers and connectors. Publicly named participants included Raj Gokal, Balaji Srinivasan, Aaron Harris, Bryan Pellegrino, Marc Boiron, Amy Wu and Paul Veradittakit, among many others. Benchmark then led a $17 million Series A in November 2025, with Chetan Puttagunta joining the board. TechCrunch reported it was the round's only institutional check.

Index Ventures led the $75 million Series B announced June 22, 2026, with USV and Benchmark participating. Julia Andre sponsored Index's investment. Fortune reported a $550 million valuation but not whether it was pre- or post-money. If pre-money, a wholly primary $75 million investment would equal about 12 percent post-round ownership; if post-money, about 13.6 percent. Actual ownership cannot be inferred without round structure.

SEC filings corroborate but refine the narrative. The Series A-era filing reports $19.30 million sold, including $2.30 million converted, to 77 investors. A June 2 Series B filing showed $67.32 million sold of a $74.00 million offering before the public close. The investor roster favors generalist consumer-network and fintech expertise over an exclusively crypto-native syndicate. That can broaden distribution and governance, while creating high growth expectations and less tolerance for a prolonged fee-cycle downturn.

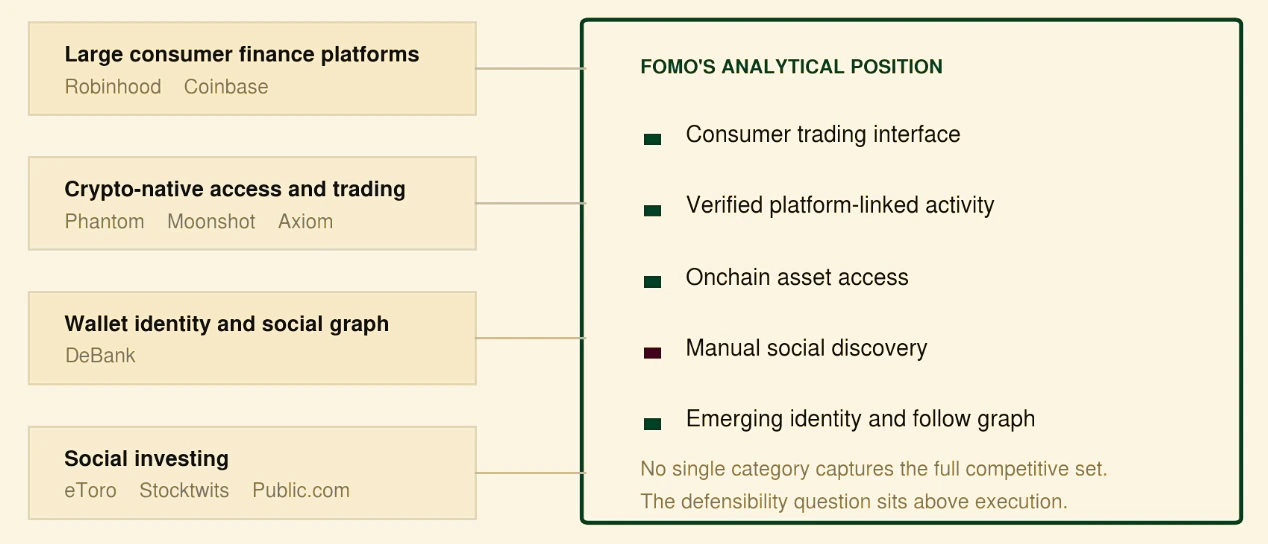

Competitive Landscape

FOMO competes across layers rather than against one product. Robinhood and Coinbase combine consumer trust, regulatory resources and large installed bases; both now offer social feeds with verified trading context. Robinhood Social began beta with 10,000 customers, while Coinbase's Base experience lets users follow creators and act on trade content. These launches show that FOMO's concept is replicable at the feature level.

Crypto-native wallets and terminals compete on access and speed. Phantom brings a reported 15 million users, swaps and perps; Moonshot targets simple memecoin and tokenized-asset trading; Axiom serves advanced onchain traders. They can add social functions but generally lack FOMO's integrated reputation emphasis. DeBank starts from public wallet identity and portfolio data, proving that an onchain social graph need not own execution.

Social-investing incumbents solve different problems. eToro automatically copies positions proportionally and pays qualifying popular investors based on copied assets. Stocktwits organizes discussion and sentiment without verifying full execution. Public.com combines regulated brokerage and community. FOMO's manual-execution approach sits between speech and copying: it authenticates activity but leaves the follower to decide.

The competitive question is therefore not whether rivals can reproduce profiles, feeds or copy buttons. They can. FOMO must establish a denser cross-venue identity graph, better relevance ranking or a culturally distinct creator community before incumbent distribution overwhelms its early lead.

Is the Social Graph a Moat?

FOMO has a plausible future moat, not a demonstrated one. Network effects are possible because each skilled trader can improve discovery for many followers, and each follower increases the trader's distribution. Proprietary context exists in identity links, follows, theses, notifications and intent. Brand and shareable activity may lower acquisition cost.

Countervailing evidence is substantial. Settlement data is public; identities can be maintained on several platforms; no follower export or strong contractual switching cost is visible; and the best traders can hide exposures elsewhere. Erlanger's public acknowledgement that social usage still trails trading is particularly important. The graph also faces local-network risk: an audience built around Solana memecoins may not automatically transfer to tokenized equities or prediction markets.

The moat should be considered demonstrated only when FOMO publishes or credibly substantiates retained funded cohorts, nontrading social engagement, diversified follower concentration, discovery-to-trade attribution, creator retention and cross-asset relationship persistence. Until then, the social graph is an intelligent strategic architecture supported by early signals, not proof of durable excess returns.

The Path Beyond Crypto Spot Trading

Perpetuals already show how a stable identity can span products, and their recent volume suggests they could exceed spot activity. Yet notional inflated by leverage should not be confused with user capital or revenue quality. Tokenized equities are the most strategically coherent next market because global distribution and familiar underlying assets could widen the audience, but securities, promotion and jurisdictional rules are materially harder than permissionless token swaps.

The company has publicly identified equities, perpetuals and prediction markets as expansion areas, with the Series B announcement framing the product as an interface for additional asset classes. Prediction markets fit the discovery graph because beliefs can become trackable positions; yield could improve account retention by giving idle balances a use. Neither public announcement nor current product documentation reviewed for this report establishes a launched subscription, proprietary stablecoin or native yield account. Such products remain analytical possibilities, not part of the base case. They would also add securities, promotion, affiliate, reserve and counterparty risks.

Risks and the Bear Case

The bear case begins with cyclicality. Transaction fees depend on retail urgency, long-tail asset interest and leverage. The Q2 revenue decline followed a Q1 peak, and app-store or creator spikes may not survive quiet markets. High explicit fees invite compression, while the $550 million reported valuation requires growth well beyond the $23 million of protocol revenue reported by DefiLlama through the observation point.

The social graph could magnify noise rather than information. Popular accounts may herd users into illiquid assets, use followers as exit liquidity or display incomplete portfolios. The most capable traders may avoid visibility. Manual execution reduces automatic-copy regulation and mechanical front-running, but it does not eliminate advice, promotion, suitability or manipulation concerns. European regulators note that copy services can constitute advice or portfolio management depending on design, while FOMO bars US persons from perps and broadly reserves KYC and geoblocking rights.

Operationally, FOMO depends on wallet, routing, onramp, market-data and derivatives partners. A failure can damage FOMO's brand even when the company does not control the venue. Large brokerages can bundle similar social features with stronger compliance, balance sheets and asset breadth. Finally, headline registrations and CEO-reported daily users do not establish funded-account retention, meaningful balances or trading habit. The company has not published cohort data that reconciles those layers.

The Bull Case

The bull case is that onchain finance commoditizes execution while making behavior legible. FOMO has early consumer distribution, transaction-generated content, rapid product velocity and protocol gross margins that can fund experimentation. Its generalist investors add consumer-network and fintech experience, and outsourced infrastructure lets a 17-person team extend into new assets quickly.

For FOMO to become a multi-billion-dollar platform, three things must occur. First, social consumption must retain users when trading intent is low. Second, respected traders must gain reputational or economic value that is costly to rebuild elsewhere. Third, the graph must survive migration from speculative tokens into perps, tokenized securities, yield and prediction markets without losing trust. If those conditions hold, FOMO could own the discovery and relationship layer even while venues own execution.

Conclusion

FOMO is not simply a polished router. Its embedded identity, platform-linked trade activity, follow graph, theses and notifications create a product whose information layer is inseparable from execution. Company-reported scale and public protocol data show that the application has moved beyond a niche experiment. The rapid launch of perps and evidence of first-time crypto onboarding provide credible early support for a two-sided financial-information network, although the composition of each side is not publicly quantified.

The same evidence does not yet establish defensibility. Headline metrics are company-reported, adapter scopes differ, protocol earnings omit operating costs, and Erlanger says social engagement remains behind trading. FOMO can verify activity in one account, not complete financial identity. Robinhood, Coinbase, wallets and wallet-social networks can reproduce many visible features, while FOMO rents most of its execution stack.

The central answer is therefore conditional. FOMO is a fast-growing trading interface that has built the beginnings of a differentiated discovery layer. Its social graph is an emerging moat candidate, not a moat already earned. Evidence that would change that judgment includes durable funded cohorts through a weak speculative cycle, high nontransactional feed retention, low follower concentration, independently measured discovery-to-trade conversion, trusted creator persistence and cross-asset continuity. Failure on those tests would leave FOMO as an effective but replaceable consumer front end. Success would support the more ambitious thesis: as assets move onchain, the scarce layer may be the network that knows who trades, what they believe and whose attention their behavior commands.

Sources and Methodology

This paper was prepared as of July 15, 2026 and relies exclusively on public sources listed in the bibliography. Primary evidence included FOMO's website, terms, product guides, release notes, financing announcements, public interviews, investor essays and SEC filings. Product availability was checked against app-store pages. Protocol volume and revenue came from DefiLlama, retaining its definitions and adapter boundaries. A public Dune dashboard was located, but raw query output was unavailable, so visually estimated daily-trader values were excluded.

Company metrics remain unaudited. Public sources do not disclose follower concentration, cohort retention, geographic demographics, operating expenses or the valuation basis. Comparisons avoid treating wallet addresses as individuals, protocol earnings as net income, or spot turnover as equivalent to leveraged perpetual notional. Where official materials conflict, the inconsistency is identified.

Bibliography

Company, corporate and investor sources

[1] FOMO homepage. FOMO. [https://fomo.family/](https://fomo.family/)

[2] Fundraising Announcement. FOMO. [https://fomo.family/blog/fundraising-announcement](https://fomo.family/blog/fundraising-announcement)

[3] FOMO Raises $17M Series A Led by Benchmark. FOMO. [https://fomo.family/blog/series-a](https://fomo.family/blog/series-a)

[5] Fomo Raises $75 Million Series B Led by Index Ventures. FOMO / GlobeNewswire. [https://www.globenewswire.com/news-release/2026/06/22/3315279/0/en/fomo-raises-75-million-series-b-led-by-index-ventures-to-scale-global-consumer-trading-app.html](https://www.globenewswire.com/news-release/2026/06/22/3315279/0/en/fomo-raises-75-million-series-b-led-by-index-ventures-to-scale-global-consumer-trading-app.html)

[7] On-chain trading goes mainstream: Fomo's $75M Series B. Index Ventures. [https://www.indexventures.com/perspectives/on-chain-trading-goes-mainstream-fomos-75-million-series-b/](https://www.indexventures.com/perspectives/on-chain-trading-goes-mainstream-fomos-75-million-series-b/)

[8] Fomo. Union Square Ventures. [https://blog.usv.com/fomo](https://blog.usv.com/fomo)

[9] Form D, FOMO Labs Inc., filed February 10, 2026. U.S. Securities and Exchange Commission. [https://www.sec.gov/Archives/edgar/data/2097616/000123191926000127/xslFormDX01/primary_doc.xml](https://www.sec.gov/Archives/edgar/data/2097616/000123191926000127/xslFormDX01/primary_doc.xml)

[10] Form D, FOMO Labs Inc., filed June 2, 2026. U.S. Securities and Exchange Commission. [https://www.sec.gov/Archives/edgar/data/2097616/000209761626000001/xslFormDX01/primary_doc.xml](https://www.sec.gov/Archives/edgar/data/2097616/000209761626000001/xslFormDX01/primary_doc.xml)

[11] Terms of Use, effective June 8, 2026. FOMO. [https://fomo.family/terms](https://fomo.family/terms)

[13] FOMO Debuts Social Crypto Trading Platform. FOMO / Yahoo Finance. [https://finance.yahoo.com/news/fomo-debuts-groundbreaking-social-crypto-160000884.html](https://finance.yahoo.com/news/fomo-debuts-groundbreaking-social-crypto-160000884.html)

[15] September 2025 Recap. FOMO. [https://fomo.family/blog/september-2025-recap](https://fomo.family/blog/september-2025-recap)

[16] October 2025 Recap. FOMO. [https://fomo.family/blog/october-2025-recap](https://fomo.family/blog/october-2025-recap)

[17] November 2025 Recap. FOMO. [https://fomo.family/blog/november-2025-recap](https://fomo.family/blog/november-2025-recap)

[19] January 2026 Recap. FOMO. [https://fomo.family/blog/january-2026-recap](https://fomo.family/blog/january-2026-recap)

[20] February 2026 Recap. FOMO. [https://fomo.family/blog/february-2026-recap](https://fomo.family/blog/february-2026-recap)

[21] Announcing Fomo Web. FOMO. [https://fomo.family/blog/announcing-fomo-web](https://fomo.family/blog/announcing-fomo-web)

[22] Perpetuals Are Now on Fomo. FOMO. [https://fomo.family/blog/perpetuals-now-on-fomo](https://fomo.family/blog/perpetuals-now-on-fomo)

[27] Fomo Security and Wallet Architecture. FOMO. [https://fomo.family/blog/learn/fomo-security-wallet-architecture](https://fomo.family/blog/learn/fomo-security-wallet-architecture)

[28] A Guide to Deposits and Withdrawals. FOMO. [https://fomo.family/blog/learn/a-guide-to-deposits-and-withdrawals](https://fomo.family/blog/learn/a-guide-to-deposits-and-withdrawals)

[29] Navigating Your Fomo App. FOMO. [https://fomo.family/blog/learn/navigating-your-fomo-app](https://fomo.family/blog/learn/navigating-your-fomo-app)

[30] Leveraging Fomo's Social Features. FOMO. [https://fomo.family/blog/learn/leveraging-fomos-social-features](https://fomo.family/blog/learn/leveraging-fomos-social-features)

[31] How to Buy Crypto by Following Top Traders. FOMO. [https://fomo.family/answers/buy-crypto-following-top-traders](https://fomo.family/answers/buy-crypto-following-top-traders)

[40] Fomo Affiliates. FOMO. [https://fomo.family/affiliates](https://fomo.family/affiliates)

[64] Fomo x TradingView. FOMO. [https://fomo.family/blog/tradingview-partnership](https://fomo.family/blog/tradingview-partnership)

[72] Fomo Labs open roles. Ashby. [https://jobs.ashbyhq.com/fomo-labs](https://jobs.ashbyhq.com/fomo-labs)

[74] Fomo vs. Phantom Wallet. FOMO. [https://fomo.family/blog/learn/fomo-vs-phantom-wallet](https://fomo.family/blog/learn/fomo-vs-phantom-wallet)

[75] What Is Copy Trading?. FOMO. [https://fomo.family/blog/learn/what-is-copy-trading](https://fomo.family/blog/learn/what-is-copy-trading)

[76] Risk-Reward Ratio: How to Size Every Crypto Trade. FOMO. [https://fomo.family/blog/learn/risk-reward-ratio-how-to-size-every-crypto-trade](https://fomo.family/blog/learn/risk-reward-ratio-how-to-size-every-crypto-trade)

Founder, team and financing reporting

[4] Why Benchmark made a rare crypto bet on trading app Fomo. TechCrunch. [https://techcrunch.com/2025/11/06/why-benchmark-made-a-rare-crypto-bet-on-trading-app-fomo-with-17m-series-a/](https://techcrunch.com/2025/11/06/why-benchmark-made-a-rare-crypto-bet-on-trading-app-fomo-with-17m-series-a/)

[6] Fomo raises $75 million at reported $550 million valuation. Fortune. [https://fortune.com/2026/06/22/fomo-series-b-fundraise-index-ventures-union-square-ventures/](https://fortune.com/2026/06/22/fomo-series-b-fundraise-index-ventures-union-square-ventures/)

[24] 20VC interview transcript with Paul Erlanger. 20VC. [https://20vc.substack.com/api/v1/file/4d259209-78d5-4412-ac61-f73d9089ffa1.pdf](https://20vc.substack.com/api/v1/file/4d259209-78d5-4412-ac61-f73d9089ffa1.pdf)

[65] Paul Erlanger professional profile. LinkedIn. [https://www.linkedin.com/in/paul-erlanger](https://www.linkedin.com/in/paul-erlanger)

[66] Se Yong Park professional profile. LinkedIn. [https://www.linkedin.com/in/se-yong-park-634782120/](https://www.linkedin.com/in/se-yong-park-634782120/)

[67] Prashan Dharmasena professional profile. LinkedIn. [https://www.linkedin.com/in/prashandharmasena](https://www.linkedin.com/in/prashandharmasena)

[68] Built by Berkeley: Prashan Dharmasena. Built by Berkeley. [https://built-by-berkeley.beehiiv.com/p/built-by-berkeley-dccb](https://built-by-berkeley.beehiiv.com/p/built-by-berkeley-dccb)

[69] Daniel Lian professional profile. LinkedIn. [https://www.linkedin.com/in/daniel-lian-3bbb9817](https://www.linkedin.com/in/daniel-lian-3bbb9817)

[70] Ren Yu Kong professional profile. LinkedIn. [https://www.linkedin.com/in/ren-yu-kong](https://www.linkedin.com/in/ren-yu-kong)

[71] Charlie Katsikaris professional profile. LinkedIn. [https://www.linkedin.com/in/charliekatsikaris](https://www.linkedin.com/in/charliekatsikaris)

[73] Fomo's Se Yong Park: Building a User-Friendly Trading App. Apple Podcasts. [https://podcasts.apple.com/ae/podcast/fomos-se-yong-park-building-a-user-friendly-trading-app/id1872720878?i=1000758611484](https://podcasts.apple.com/ae/podcast/fomos-se-yong-park-building-a-user-friendly-trading-app/id1872720878?i=1000758611484)

Product infrastructure, analytics and independent research

[14] Fomo to track KOL moves with upcoming SocialFi app. Blockworks. [https://blockworks.com/news/fomo-to-track-kol-moves](https://blockworks.com/news/fomo-to-track-kol-moves)

[25] Fomo: Never Miss Out. Apple App Store. [https://apps.apple.com/us/app/fomo-never-miss-out/id6741115427](https://apps.apple.com/us/app/fomo-never-miss-out/id6741115427)

[26] Fomo. Google Play. [https://play.google.com/store/apps/details?id=family.fomo.app](https://play.google.com/store/apps/details?id=family.fomo.app)

[32] Turning trading into a social experience with Fomo. Privy. [https://privy.io/blog/turning-trading-into-a-social-experience-with-fomo](https://privy.io/blog/turning-trading-into-a-social-experience-with-fomo)

[33] Fomo case study. Mobula. [https://mobula.io/casestudy-fomo](https://mobula.io/casestudy-fomo)

[34] Trade[XYZ] documentation. Trade[XYZ]. [https://docs.trade.xyz/](https://docs.trade.xyz/)

[35] Builder Codes. Hyperliquid Documentation. [https://hyperliquid.gitbook.io/hyperliquid-docs/trading/builder-codes](https://hyperliquid.gitbook.io/hyperliquid-docs/trading/builder-codes)

[36] Social Trading: FOMO and the Financial Graph. Galaxy Research. [https://www.galaxy.com/insights/research/social-trading-fomo](https://www.galaxy.com/insights/research/social-trading-fomo)

[37] FOMO dashboard. Dune. [https://dune.com/socialgraphventures/fomo](https://dune.com/socialgraphventures/fomo)

[38] Fomo protocol dashboard. DefiLlama. [https://defillama.com/protocol/fomo](https://defillama.com/protocol/fomo)

[39] Data Definitions. DefiLlama. [https://defillama.com/data-definitions](https://defillama.com/data-definitions)

[41] 2026 Q1 Crypto Industry Report. CoinGecko Research. [https://www.coingecko.com/research/publications/2026-q1-crypto-industry-report](https://www.coingecko.com/research/publications/2026-q1-crypto-industry-report)

[42] Solana Q1 2026: DEX, RWA and Stablecoin Market Share. Galaxy Research. [https://www.galaxy.com/insights/research/solana-q1-2026-dex-rwa-stablecoins-market-share](https://www.galaxy.com/insights/research/solana-q1-2026-dex-rwa-stablecoins-market-share)

Competition and regulatory context

[43] Coinbase Exchange fees. Coinbase. [https://help.coinbase.com/en/exchange/trading-and-funding/exchange-fees](https://help.coinbase.com/en/exchange/trading-and-funding/exchange-fees)

[45] Swap crypto in Phantom. Phantom. [https://help.phantom.com/hc/en-us/articles/5985106844435-Swap-crypto-in-Phantom](https://help.phantom.com/hc/en-us/articles/5985106844435-Swap-crypto-in-Phantom)

[46] Crypto order routing. Robinhood. [https://robinhood.com/us/en/support/articles/crypto-order-routing/](https://robinhood.com/us/en/support/articles/crypto-order-routing/)

[47] Robinhood Social Beta. Robinhood. [https://robinhood.com/us/en/newsroom/robinhood-social-beta/](https://robinhood.com/us/en/newsroom/robinhood-social-beta/)

[48] Robinhood Reports First Quarter 2026 Results. Robinhood Investor Relations. [https://investors.robinhood.com/news-releases/news-release-details/robinhood-reports-first-quarter-2026-results](https://investors.robinhood.com/news-releases/news-release-details/robinhood-reports-first-quarter-2026-results)

[49] System Update: The Future of Finance Is on Coinbase. Coinbase. [https://www.coinbase.com/blog/system-update-the-future-of-finance-is-on-coinbase](https://www.coinbase.com/blog/system-update-the-future-of-finance-is-on-coinbase)

[50] Base social feed. Coinbase Help. [https://help.coinbase.com/base/social-feed/intro](https://help.coinbase.com/base/social-feed/intro)

[51] CopyTrader: How It Works. eToro. [https://www.etoro.com/en-us/copytrader/how-it-works/](https://www.etoro.com/en-us/copytrader/how-it-works/)

[52] Popular Investor Program. eToro. [https://www.etoro.com/copytrader/popular-investor/](https://www.etoro.com/copytrader/popular-investor/)

[53] Community and portfolio education. Public.com. [https://public.com/learn/how-to-diversify-a-stock-market-portfolio](https://public.com/learn/how-to-diversify-a-stock-market-portfolio)

[54] Stocktwits. Stocktwits. [https://stocktwits.com/](https://stocktwits.com/)

[55] Phantom Perps. Phantom. [https://phantom.com/learn/blog/phantom-perps](https://phantom.com/learn/blog/phantom-perps)

[56] Best Crypto Wallets. Phantom. [https://phantom.com/learn/crypto-101/best-crypto-wallet](https://phantom.com/learn/crypto-101/best-crypto-wallet)

[57] Moonshot. Moonshot. [https://moonshot.money/](https://moonshot.money/)

[58] Axiom. Axiom. [https://axiom.trade/](https://axiom.trade/)

[59] Official Account Introduction. DeBank Cloud. [https://docs.cloud.debank.com/en/official-account/introduction](https://docs.cloud.debank.com/en/official-account/introduction)

[60] Copy trading. UK Financial Conduct Authority. [https://www.fca.org.uk/firms/copy-trading](https://www.fca.org.uk/firms/copy-trading)

[61] Supervisory Briefing on Copy Trading. European Securities and Markets Authority. [https://www.esma.europa.eu/sites/default/files/2023-03/ESMA35-42-1428_Supervisory_Briefing_on_Copy_Trading.pdf](https://www.esma.europa.eu/sites/default/files/2023-03/ESMA35-42-1428_Supervisory_Briefing_on_Copy_Trading.pdf)

[62] Social Media and Investment Fraud. U.S. Securities and Exchange Commission. [https://www.sec.gov/resources-for-investors/investor-alerts-bulletins/social-media-investment-fraud-investor-alert](https://www.sec.gov/resources-for-investors/investor-alerts-bulletins/social-media-investment-fraud-investor-alert)

Cover Artwork

An Experiment on a Bird in the Air Pump

Joseph Wright of Derby, c. 1768

Research notice

This publication has been prepared by the insights4vc Team for informational and research purposes only. It does not constitute investment, financial, legal, tax or other professional advice, nor does it constitute an offer, solicitation, recommendation or endorsement to buy, sell, hold or otherwise transact in any security, digital asset, financial instrument or investment product.

The information contained in this publication is based on public sources and data believed to be reliable at the time of publication. insights4vc does not make any representation or warranty, express or implied, as to the accuracy, completeness or timeliness of the information presented. Company-reported metrics, estimates and other third-party data may be unaudited and have not necessarily been independently verified by insights4vc.

Any opinions, estimates, projections or forward-looking statements reflect the analytical judgment of the authors as of the publication date and are subject to change without notice. Forward-looking statements are inherently uncertain and should not be regarded as guarantees of future results, performance or events.

Digital assets and related financial products may be highly volatile, speculative and subject to significant market, liquidity, technological, regulatory, counterparty and operational risks. The value of an investment may decline substantially, and investors may lose some or all of the capital invested.

Readers should conduct their own independent research and due diligence and, where appropriate, consult qualified financial, legal, tax or other professional advisers before making any investment or financial decision. insights4vc does not advocate or encourage any specific investment action.