Robinhood’s move is easy to misread if one looks only at the surface. At the surface, the story is attractive: a large retail broker has launched a public, Ethereum-compatible, Arbitrum-based Layer 2; it supports wallets, ETH gas, bridging, tokenised market exposure and DeFi integrations; and it wants to make financial products cheaper, more portable and more globally accessible. That is all broadly true.

The real strategic question sits underneath. Robinhood is building a permissionless financial chain, but the assets that make the chain strategically interesting are not truly permissionless financial objects. They are wrapped claims that remain legally mediated. The chain may be open to deploy on. The token may be transferable across supported wallets. But the economically meaningful instrument still rests on an issuer, a prospectus, a custodian, an authorised participant network, sanctions and KYC controls, jurisdictional exclusions, oracle design, and legal recourse that looks nothing like direct share ownership.

That is the brokerage chain paradox. Robinhood’s opportunity is to hide this complexity well enough that the product feels simple, global and useful. Robinhood’s risk is that users, developers and regulators refuse to ignore the complexity underneath. If users think “tokenised stock” means “stock”, the gap between language and legal reality becomes a product-liability issue. If regulators think the wrapper is clear and fairly disclosed, the structure may scale. If they think the wrapper encourages misunderstanding, scale could stall precisely where the story becomes interesting.

Seen in that light, Robinhood Chain is neither a pure crypto experiment nor a simple extension of the brokerage app. It is an attempt to manufacture a new layer in between: a consumer-facing financial stack where the interface feels straightforward but the mechanics underneath are deeply structured, heavily controlled and jurisdiction-specific. That is commercially plausible. It is also inherently fragile. No part of the strategy works if Robinhood cannot maintain the illusion of simplicity without overstating what the user actually owns.

Robinhood Today and the Super-App Ambition

A strong business looking for the next growth surface

Robinhood is not launching Robinhood Chain as a defensive manoeuvre. The company is doing so from a position of unusual operating strength for a broker that, only a few years ago, was still treated by many investors as a cyclical retail-trading platform.

Robinhood (NASDAQ: HOOD) is scheduled to release its Q2 2026 financial results on Wednesday, July 29, 2026, after the market closes.

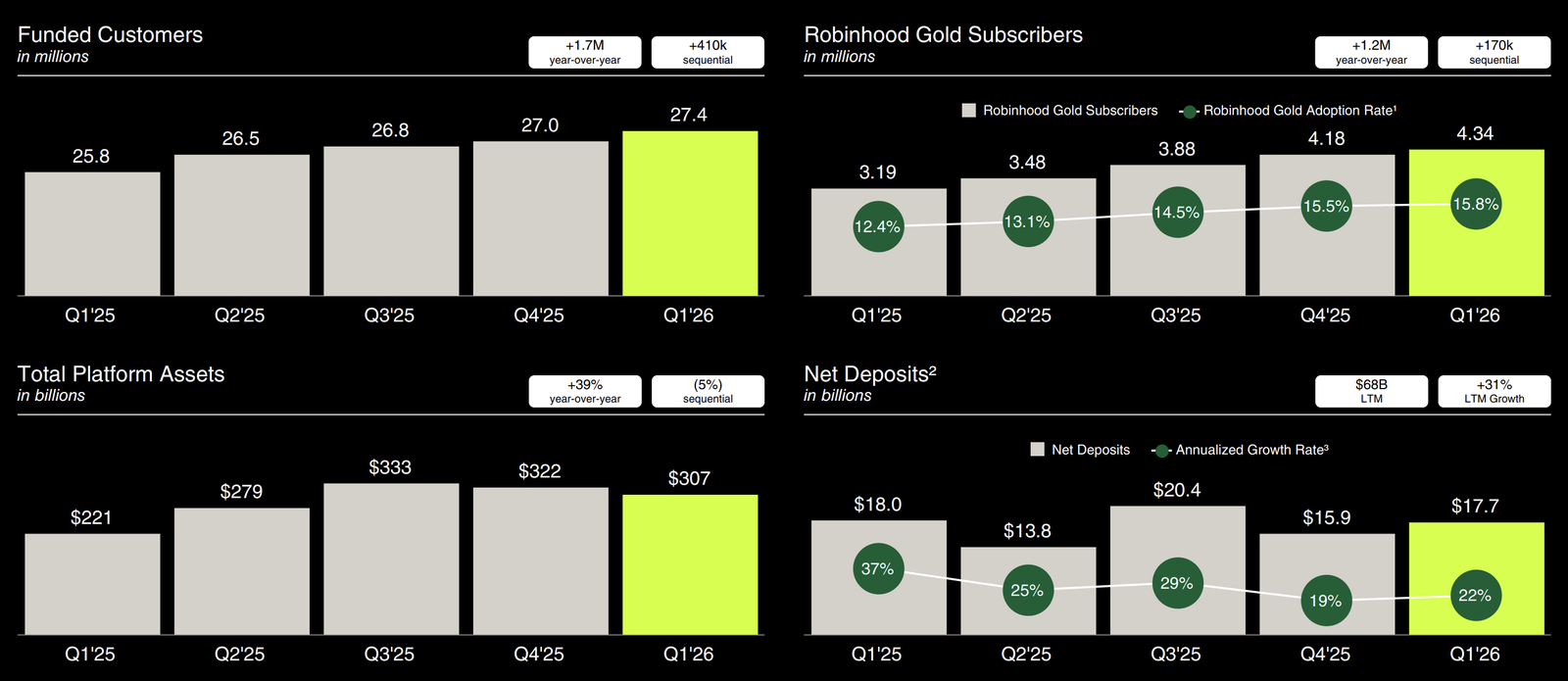

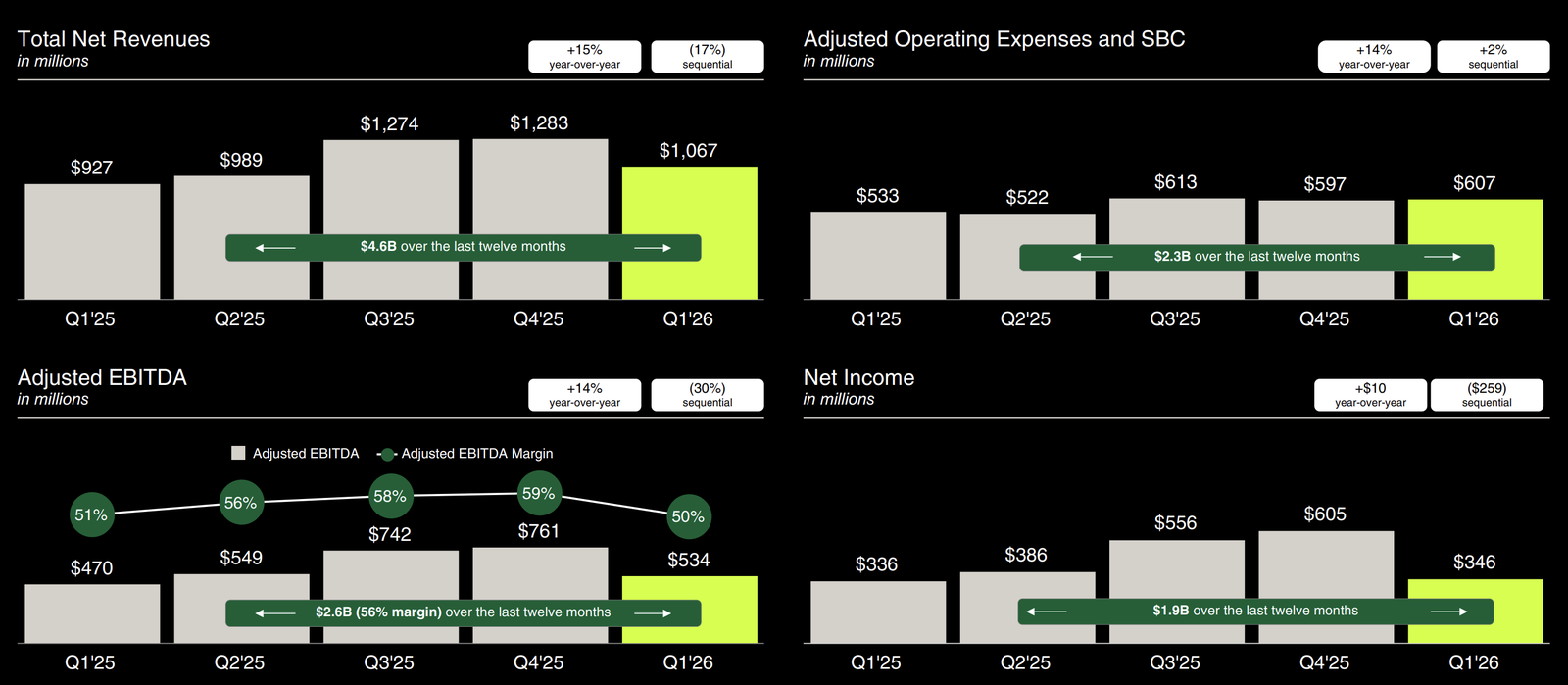

In Q1 2026, it delivered $1.07 billion of net revenue, $623 million of transaction-based revenue, $359 million of net interest revenue, $346 million of net income and $534 million of adjusted EBITDA. Total platform assets reached $307 billion, funded customers 27.4 million, ARPU $157 and Gold subscribers 4.3 million.

Q1 2026 Business Results Highlights

Q1 2026 Financial Results Highlights

The revenue mix matters because it shows where the business is actually monetising today. Options generated $260 million of transaction-based revenue in Q1 2026, equities $82 million, event contracts $104 million, other transaction revenue $43 million and crypto $134 million. The standout growth line was event contracts, which rose from $3 million in the prior-year quarter to $104 million, while crypto revenue fell from $252 million to $134 million. Robinhood Chain is therefore being launched at a time when the company’s earnings are still primarily driven by active retail trading, margin-rich products and balance-sheet monetisation, not by any existing onchain business line.

This distinction is important for both strategic and valuation purposes. Robinhood Chain is not rescuing the business. It is trying to create a new surface above a business that is already working. That makes the initiative more credible, because the company can afford to experiment. It also makes the initiative easier to overstate, because the existing earnings engine remains rooted in mature brokerage economics.

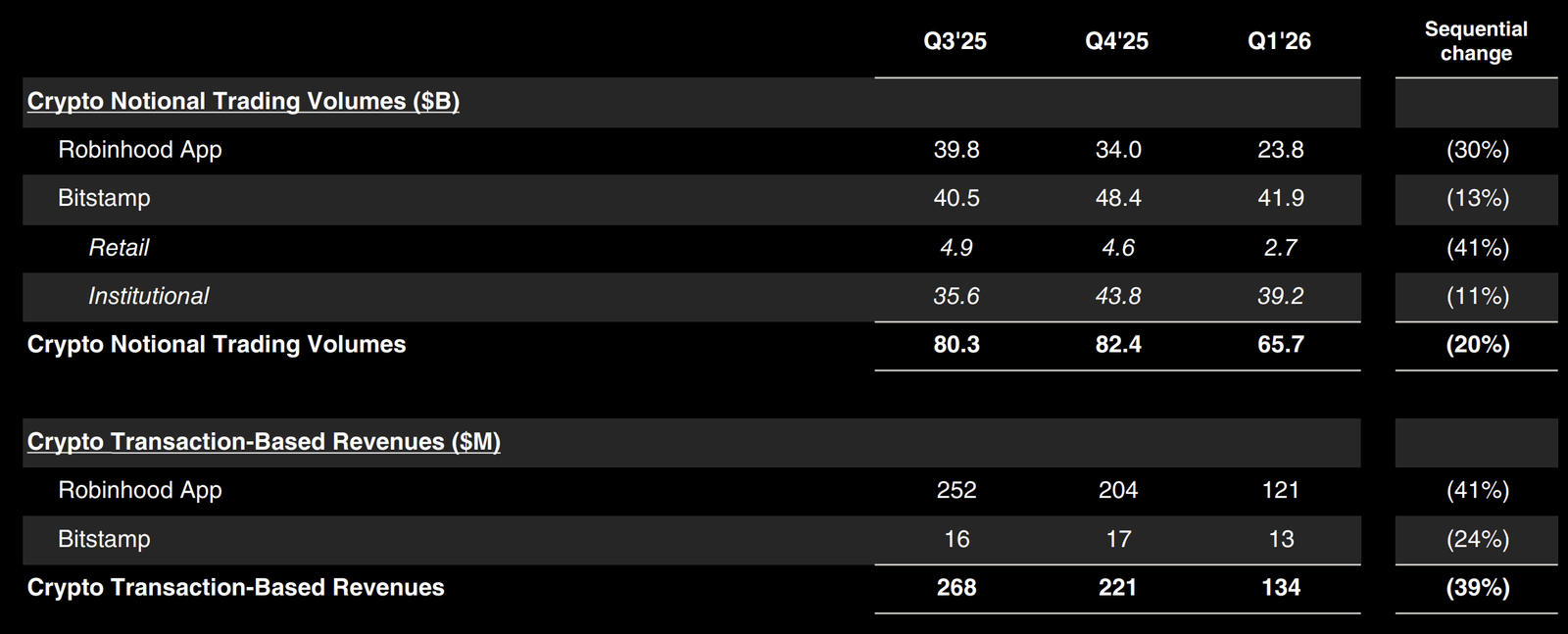

The rest of the balance-sheet and engagement picture points in the same direction. Robinhood disclosed a $17.0 billion margin book, $16.7 billion of cash and deposits, $27.4 billion of retirement assets under custody and $66 billion of crypto notional volume in Q1 2026, including $42 billion from Bitstamp and $24 billion from the Robinhood app. That last figure is especially relevant. Bitstamp is already making Robinhood’s crypto footprint look more like infrastructure and less like an isolated retail trading feature.

From brokerage app to financial super-app

Robinhood’s strategic logic now looks more coherent than it did when the company first began adding disparate products around its core brokerage. In Q1 2026 and subsequent public materials, the company was no longer simply describing product expansion. It was sketching a fuller operating model: brokerage, options, futures, event contracts, banking, Gold, retirement, crypto, wallet, private-markets access, AI tools, global licensing, tokenised assets and DeFi-linked yield. Management’s language about building a “global financial ecosystem” is not just corporate flourish. It is an attempt to explain how the various layers fit together.

That broader stack now includes several pieces that would have looked disconnected in isolation. Robinhood Banking and higher cash engagement matter because they deepen deposit and balance relationships. Robinhood Gold matters because it improves subscription attachment and supports the premium-wrapper model. Retirement matters because it extends the lifecycle of assets and reduces pure trading cyclicality. Futures and event contracts matter because they increase engagement and monetisation intensity. Crypto matters because it provides 24/7 markets, self-custody rails and global funding flexibility. Bitstamp matters because it expands institutional and international reach. The wallet matters because it gives Robinhood a credible non-custodial interface. Robinhood Chain matters because it offers a programmable settlement layer where all of those financial behaviours can, in principle, start to converge.

The company’s international vector reinforces the same point. Robinhood has expanded into Canada via WonderFi, disclosed Singapore regulatory progress, and described UK crypto plans. Those steps matter not simply as new territories, but because they create a test bed for products that do not fit neatly inside the U.S. retail brokerage rule set. Tokenised wrappers and wallet-native products are easier to introduce at the edge of the group than at the regulated core of the U.S. app.

The strategic sentence, then, is simple: Robinhood Chain matters because it may let Robinhood extend its consumer distribution advantage into programmable finance without turning the core U.S. brokerage into a crypto-native venue overnight. That is why the chain should be read as infrastructure strategy, not launch collateral.

What Robinhood Chain Actually Is

Robinhood Chain’s documentation describes it as an Arbitrum Layer 2 chain built on Ethereum, using Ethereum blobs for data availability and ETH as the native gas token. Robinhood Wallet supports it natively, and other EVM wallets can add it manually. Assets can be moved onto the chain using the canonical Arbitrum bridge or partner routes. Public materials also emphasise that the chain is open and permissionless, EVM-compatible and designed for tokenised real-world assets.

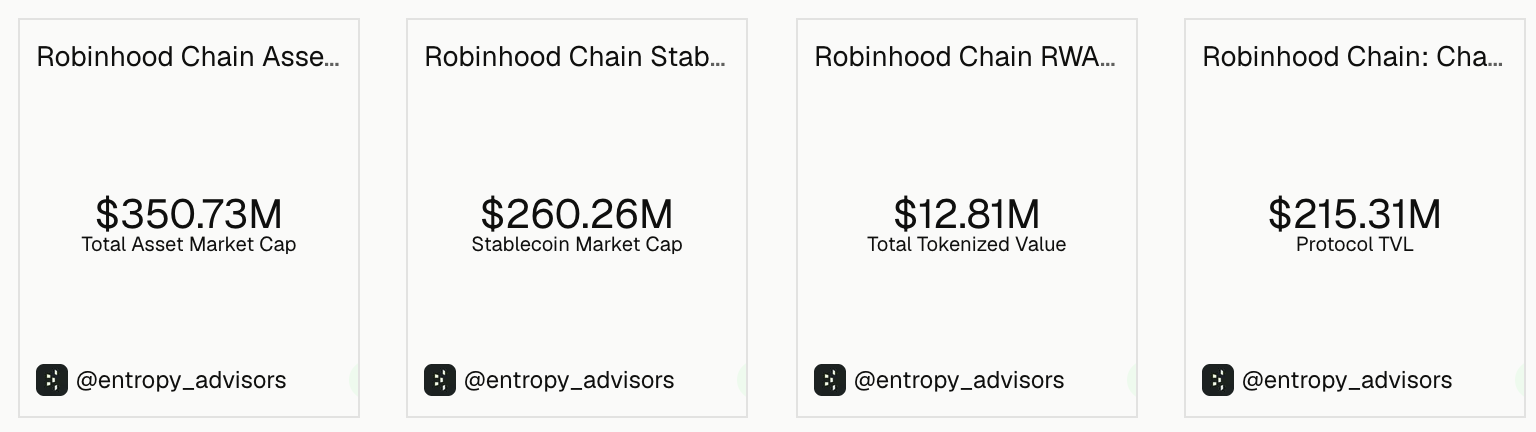

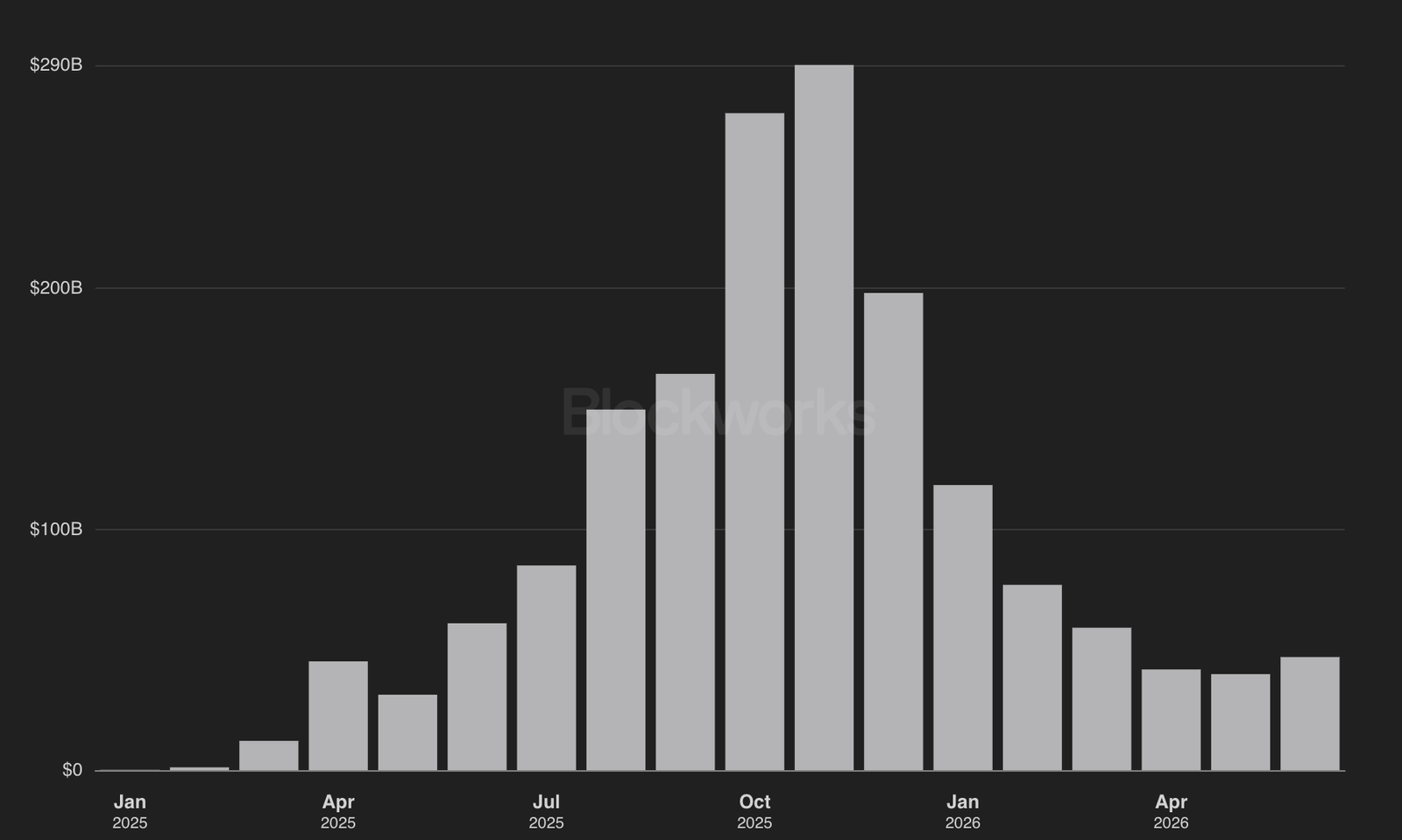

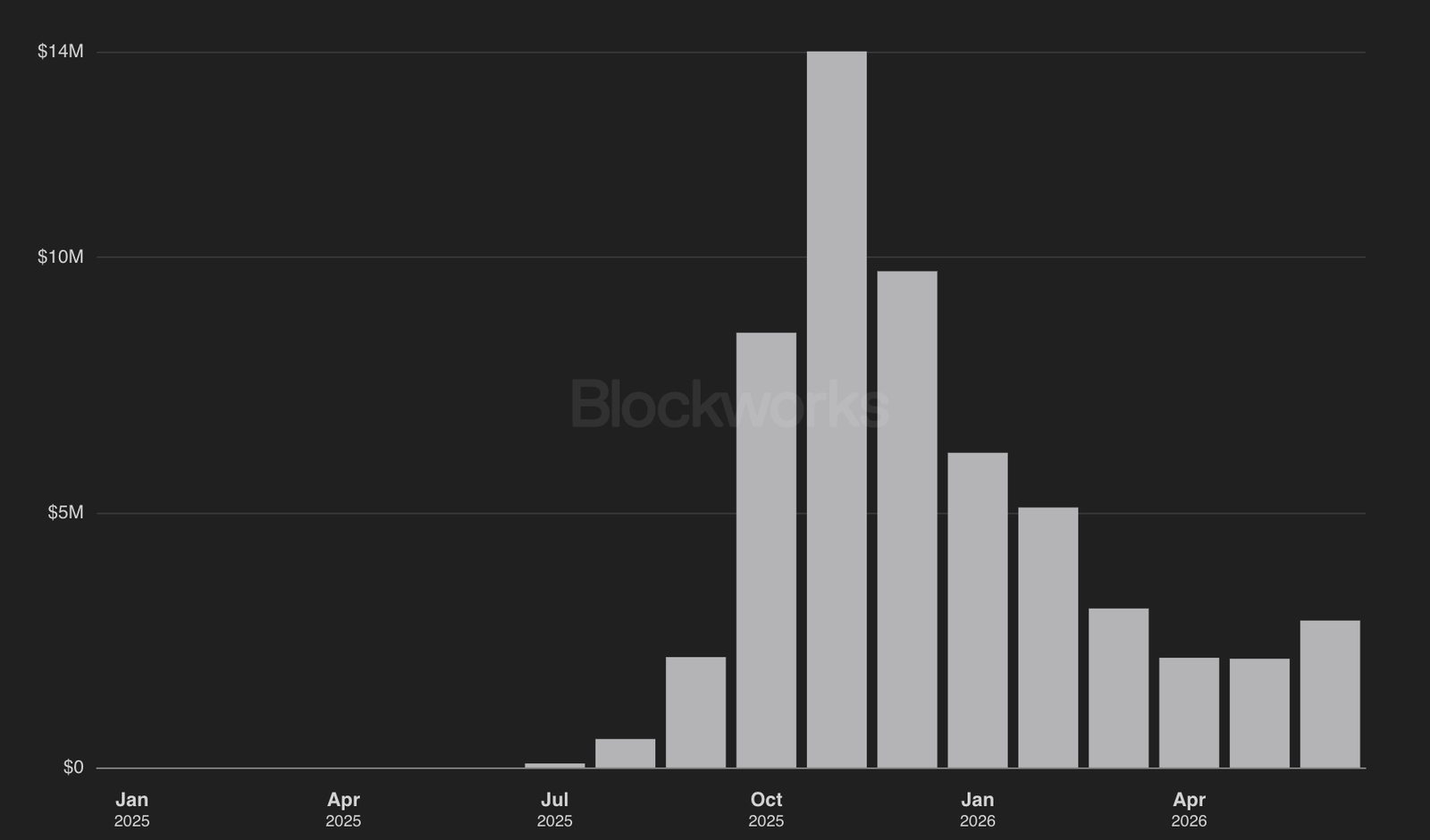

Robinhood Chain - Key Metrics (Source: EntropyAdvisors)

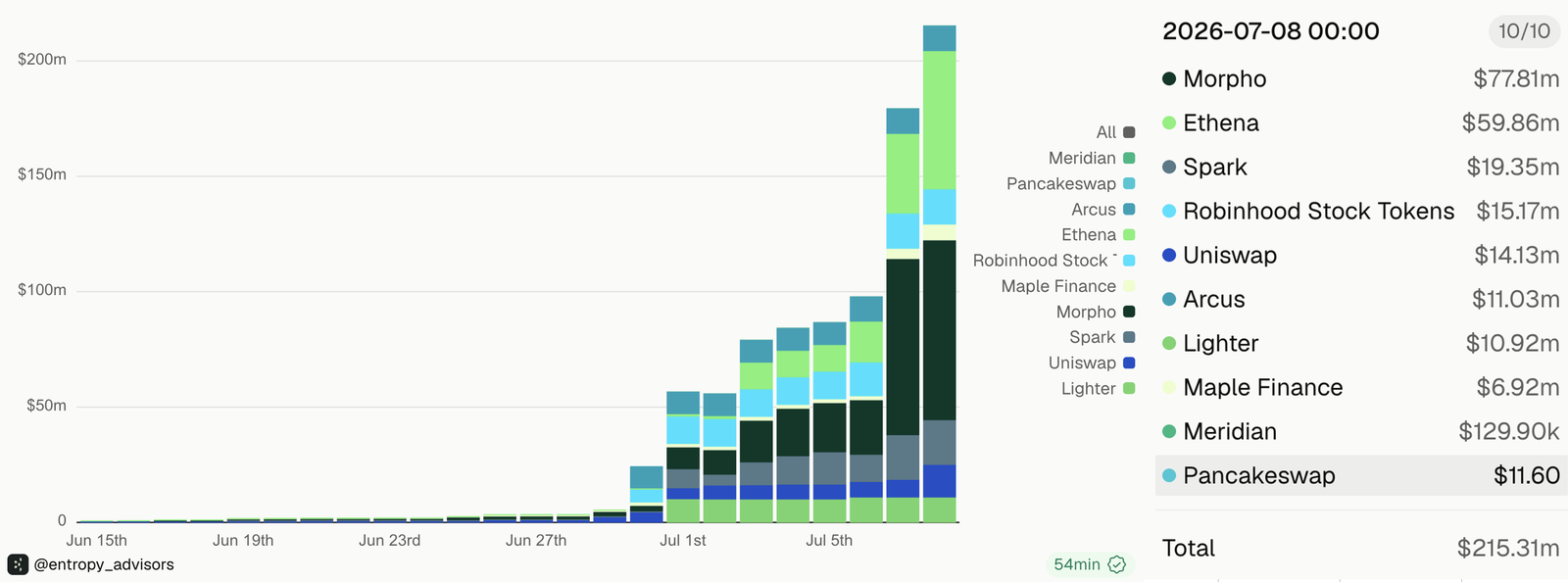

Robinhood Chain - Protocol TVL

Robinhood’s July 2026 launch materials say the chain is built using the Arbitrum platform “to institutional standards” and name Uniswap as a day-one AMM and Pleiades as a proprietary AMM / prop-trading venue. Robinhood’s technical documentation adds that Stock Tokens are standard ERC-20s and that each token has a Chainlink price feed, with corporate actions reflected through an onchain multiplier rather than a rebasing balance change.

The public docs, however, are not equally complete across all infrastructure questions. We found clear documentation on connectivity, gas, bridging, token format and oracle design, but less explicit public explanation of sequencing decentralisation, governance path, fault-proof status, or the precise current production roles of every named infrastructure partner. That does not mean the system is weak; it means some institutional-grade diligence questions still require more disclosure than the public docs currently provide.

The main takeaway is straightforward. Robinhood Chain is real, but still early. It has infrastructure, partners and live products attached to it. What it does not yet have is proof of durable liquidity, broad developer adoption, seamless regulatory portability or material revenue contribution. The distinction matters. A public mainnet and a few live products are enough to make the strategy serious. They are not enough to make it proven.

Stock Tokens and the Legal Reality of Onchain Equities

The most important sentence in this paper is also the simplest: Robinhood’s Stock Tokens should not be described as stocks onchain. They are tokenised economic exposure to securities through legal wrappers.

Robinhood’s onchain Stock Tokens are described in public materials and prospectus documents as tokenised debt securities issued by Robinhood Assets Jersey Limited. They provide economic exposure to the referenced stock or ETF, but users do not obtain direct legal title to the underlying securities, beneficial ownership of those shares or ordinary shareholder rights such as voting. The product documentation is explicit on this point, and the prospectus framework is clearer than much of the marketing shorthand around “stock tokens” would suggest.

Robinhood Europe’s earlier “Classic Stock Tokens” are legally different again. Those products are described as derivative contracts between the user and Robinhood Europe, UAB. They are not transferable to external wallets and can only be entered into or terminated through the Robinhood Europe platform. The legal perimeter there is even less ambiguous: the customer is dealing with a derivative exposure, not a tokenised bearer claim.

The newer onchain product is more radical in distribution, but conservative in legal architecture. That is precisely why it may work. The token can behave like a crypto asset at the interface layer: transferred onchain, held in compatible wallets, referenced in DeFi and priced by oracles. But the claim underneath stays conservative: a Jersey-issued, prospectus-governed, secured, limited-recourse debt security referenced to underlying shares. Robinhood is not dismantling securities law. It is packaging around it.

That legal packaging has consequences. “Backed 1:1” does not mean “you own the share”. The token holder’s exposure depends on the issuer, authorised participants, custody arrangements, collateral framework, secondary-market liquidity, jurisdictional permissions and redemption mechanics. The base prospectus states that only authorised participants subscribe directly from the issuer, while ordinary investors generally acquire exposure in the secondary market. Direct redemption by ordinary investors exists only under specified conditions; otherwise, investors are expected to sell or redeem through market intermediaries. Redemption is cash-based and conditional, not equivalent to pulling a share certificate out of a vault.

The structure also depends on named service providers and legal control points. The documents reviewed in the underlying research identify Robinhood Assets Jersey Limited as issuer and tokenizer, Bitstamp Global Ltd. as authorised offeror in the relevant terms reviewed, and Alpaca Securities LLC as custodian and broker for the referenced series. Those roles matter because tokenised exposure that aspires to be globally portable is, in practice, still held together by highly traditional financial plumbing.

Even the asset-backing story is more complex than the phrase suggests. Robinhood’s materials say each token is backed 1:1 by the underlying equity. The prospectus framework describes segregated accounts for each series, but also permits securities lending. During the life of a securities-loan transaction, the issuer’s economic exposure runs through collateral and contractual rights, rather than through untouched shares sitting inertly in custody. In stressed conditions, that difference can matter. It introduces borrower, collateral, operational and recovery-value risks that are foreign to the simple intuition a retail user may draw from the product name.

Corporate actions and dividends are similarly mediated. Robinhood’s materials explain that dividends are handled through a multiplier mechanism that adjusts the token’s reference economics, rather than by giving users direct shareholder distributions. The prospectus also flags withholding and section 871(m) considerations around dividend equivalents. Again, this does not make the product defective. It makes the product structured. Users should be buying that structure with open eyes.

Transferability is real but not absolute. Robinhood says onchain Stock Tokens can be held and transferred on supported blockchains and compatible wallets. At the same time, the documentation permits pauses, freezes and restrictions in certain circumstances, and purchases or redemptions remain subject to KYC, AML, sanctions compliance and jurisdictional exclusions. This is closer to a programmable, wrapped, conditional product than to an unrestricted bearer instrument.

The commercial conclusion is blunt. The product is radical in distribution but conservative in legal architecture. That combination is not a flaw. It is probably the only viable route to market. But it also means Stock Tokens should be valued as a legal and market-structure experiment in making economic exposure portable, not as an onchain substitute for actual share ownership.

Digital Assets as Infrastructure, Not Just Trading Revenue

Robinhood’s digital-asset strategy is now too broad to fit inside the old frame of “crypto trading revenue”. Crypto still matters as a revenue line, but it increasingly matters as infrastructure. That shift is the deeper significance of Robinhood Chain.

Crypto trading revenue remains meaningful but no longer tells the full story. In Q1 2026, Robinhood generated $134 million of crypto transaction revenue, down materially from the prior-year quarter, even as total crypto notional volume reached $66 billion. Of that notional volume, $42 billion came through Bitstamp and $24 billion through the Robinhood app. In other words, Robinhood’s digital-asset footprint is already broader than its consumer crypto tab.

Crypto Notional Trading Volumes

Bitstamp is central here. Robinhood closed the Bitstamp acquisition in June 2025 for approximately $200 million in cash and explicitly framed the deal around global exchange capability, institutional customers, white-label infrastructure, staking, institutional lending and broader licensing coverage. By later filings, Robinhood was already describing Bitstamp as expanding the institutional side of the business into services such as on-exchange lending, off-exchange settlement, post-trade settlement and institutional perpetual futures. That is not what a company says if it still thinks of crypto as a retail side pocket.

Robinhood Earn makes the same point from the consumer side. Public materials describe a simple flow: the user buys USDG on Robinhood Crypto, moves it into a self-custody wallet and lends it via Morpho. Robinhood is careful to disclose that the wallet is non-custodial and that withdrawal timing depends on vault liquidity. Morpho, for its part, describes Robinhood Earn as a progressive rollout for eligible U.S. users. This is not just adding yield to a cash balance. It is teaching the Robinhood user base that DeFi can sit behind the interface without demanding crypto-native behaviour from the customer.

The stablecoin angle matters because it is likely to be more durable than any single speculative trading cycle. If Robinhood can turn stablecoin balances into invisible funding rails, it gets a portable, programmable financing layer for wallet-native activity, international flows and future collateral use cases. In that model, the stablecoin is not the product. It is the settlement medium beneath the product. That is a more strategically important role.

Robinhood Wallet is the user-facing bridge into this stack. Support materials show the wallet already spans multiple major chains and now includes Robinhood Chain itself. That matters because wallet strategy is where brokerage distribution and crypto infrastructure meet. A broker can custody. A wallet can compose. Robinhood increasingly wants both in the same customer relationship.

Why Lighter matters

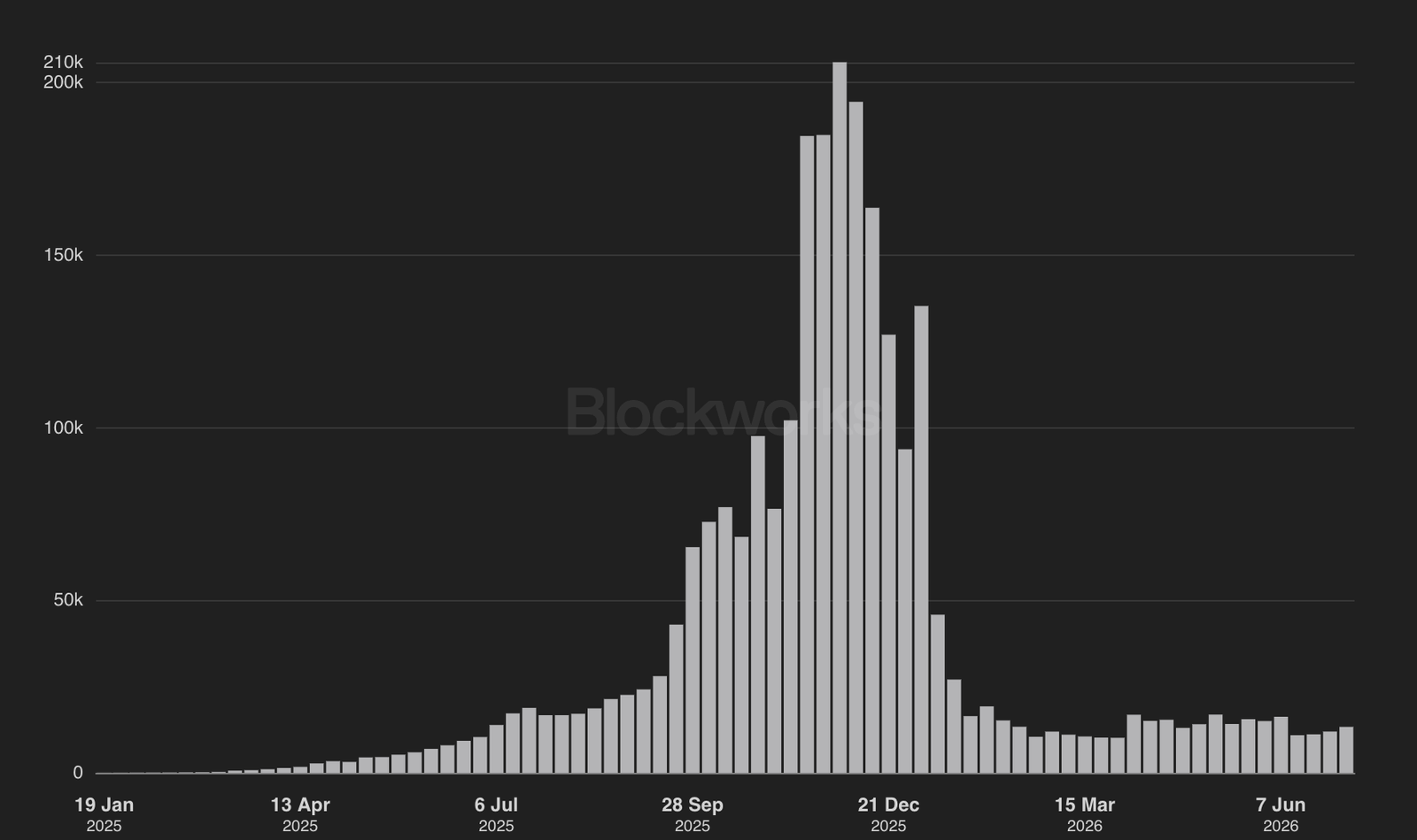

Lighter is one of the clearest examples of Robinhood’s infrastructure posture. Lighter gives Robinhood access to advanced onchain trading design without requiring Robinhood to build a crypto-native perps exchange from zero. Public materials describe Lighter as a custom zero-knowledge rollup with proofs of order matching and liquidations, price-time-priority execution and an escape-hatch design if certain operations are not processed in time. Robinhood Wallet materials, in turn, describe perpetual futures inside the wallet, including liquidation mechanics and funding dynamics, with the underlying decentralised protocol handling liquidations.

Lighter: Perpetual Futures Notional Volume (Source: Blockworks)

Lighter: Revenue (Source: Blockworks)

Lighter: Traders (Source: Blockworks)

That is strategically useful for several reasons. It enlarges the wallet’s engagement surface. It lets Robinhood test high-frequency, high-engagement trading demand in a self-custody setting. It reduces time-to-market. And it gives Robinhood exposure to the economics and user behaviour of global, always-on trading without moving the full burden into the regulated U.S. broker-dealer stack.

But Lighter also sharpens the brand challenge. Perpetual futures bring leverage, liquidations, incentive-sensitive liquidity and retail-loss risk closer to the Robinhood ecosystem. Lighter’s own documentation makes clear that RWA markets trade around the clock and use margin mechanics. That may be commercially attractive. It is also precisely the sort of product layer that can create political, regulatory and reputational friction for a mass-market broker.

The right conclusion is therefore narrower than the market may want. Lighter is not proof that Robinhood can own perps economics the way Hyperliquid does. It is proof that Robinhood can plug crypto-native trading infrastructure into its consumer wallet funnel. That is strategically meaningful. It is not the same thing as owning the venue.

Where the money could be

The money, at least initially, is unlikely to come from chain fees. Robinhood is too large for modest L2 fee generation to move the listed-company story meaningfully, and public dashboard data currently show small fee run-rates relative to group scale.

The real monetisation path is more indirect and more familiar. Stock Tokens can create spreads, turnover and wallet activity. They may help acquisition outside the United States by giving customers a differentiated way to access U.S. market exposure. Stablecoin balances and Earn may deepen wallet funding behaviour and reduce friction between brokerage, crypto and cash-like uses. Perpetuals can raise engagement intensity for a subset of users. Wallet-native finance can also strengthen Gold attachment, margin relevance and the overall value of the customer relationship.

The key point is that the economics are likely to show up first as better customer-system metrics, not as a new explicitly disclosed revenue line called “Robinhood Chain”. If onchain products improve deposits, activity, retention, non-U.S. acquisition or subscription attachment, the strategy can become financially important before chain fees ever matter. The converse is also true. If the products remain niche, even impressive infrastructure will not rescue the investment case.

Regulation, Competition and the HOOD Equity Angle

Regulatory reality check

The main regulatory question is not whether Robinhood can launch wrappers in selected jurisdictions. It already has. The question is whether those wrappers can scale without confusing users, provoking regulators or losing the simplicity that makes Robinhood commercially powerful.

Robinhood’s own product restrictions show how bounded the current opportunity set remains. The onchain Stock Tokens are not available in the United States and are also excluded from other jurisdictions, including Canada, the UK and Switzerland in the materials reviewed. That is not a footnote. It is the clearest evidence that the product sits inside a narrow regulatory lane rather than an open global market.

MiCA does not solve this. European Commission materials make clear that crypto-assets qualifying as financial instruments or derivatives fall outside MiCA’s core scope and remain governed by existing sectoral rules. That is why Robinhood Europe’s earlier stock-token product is presented as a derivative structure rather than as a generic crypto asset. MiFID II, investor-disclosure rules and local supervisory frameworks remain central.

The role of the Bank of Lithuania is relevant in exactly that sense. Robinhood Europe, UAB is authorised and regulated there as a financial brokerage firm and crypto-asset service provider. That gives Robinhood a European perimeter for offering classic stock-token exposure and other activities, but it does not magically reclassify tokenised securities into simple crypto products. In commercial terms, the regulatory route remains a patchwork.

Perpetual futures add another layer of scrutiny. ESMA stated in February 2026 that derivatives marketed as perpetual futures are likely to fall within existing CFD-style intervention rules if they meet the legal definition, bringing leverage limits, negative balance protection and disclosure safeguards into scope. That does not necessarily block the product, but it does reinforce the point that “crypto rails” do not exempt a financial product from conventional investor-protection logic.

The OpenAI and private-company token controversy is the reputational version of the same issue. Reuters reported that OpenAI publicly said it had not partnered with Robinhood and did not endorse the tokenised exposure, while Robinhood’s structure referenced special purpose vehicle exposure rather than direct equity ownership. The legal details may matter enormously in the documentation. To the user, the headline risk is that the product name can run ahead of what is actually owned. That is exactly the sort of gap regulators and consumer-protection officials tend to focus on.

Competitive reality

Robinhood’s advantage is not that its token wrapper is obviously superior to every rival structure. Its advantage is consumer distribution. It can put a complicated financial object in front of a mass-market user base that already trusts the app for trading, balances and increasingly other financial behaviour. That is unusual.

Coinbase Base is the closest analogue in strategic ambition, but not in product identity. Base increasingly presents itself as infrastructure for global finance, backed by a large retail and developer ecosystem. Its centre of gravity is broader onchain activity and app-layer growth. Robinhood Chain is narrower and more financialised. Its most visible wager is not “build everything” but “make mainstream users comfortable using programmable finance when the wrapper feels familiar”.

Kraken xStocks is the closer comparison on tokenised equities. Kraken also offers 1:1-backed tokenised stock exposure across major chains, and its own materials clarify that buying xStocks is not the same as holding real shares in the underlying issuer. Kraken’s design therefore points to the same structural truth Robinhood faces: tokenised-equity distribution can expand access without delivering direct corporate ownership. The difference is less in legal philosophy than in customer funnel and ecosystem strategy.

Ondo, Securitize, BlackRock’s BUIDL and Franklin Templeton’s Benji occupy a more institutional RWA lane. Traditional brokers such as Interactive Brokers, Schwab and Fidelity continue to offer what many investors actually want most: trusted custody, familiar governance, direct ownership and relatively little wrapper ambiguity. Robinhood sits in the middle. It is more mainstream than crypto-native venues and more aggressive on tokenisation than traditional brokers. That middle position can be powerful, but it is not guaranteed to be durable if users either demand cleaner ownership or drift toward broader onchain ecosystems.

What would prove the strategy works

The right KPI frame is not technological vanity. It is customer-value creation. The most important indicators to monitor are:

- growth in non-U.S. funded customers and funded wallets, especially where Stock Tokens are actually available;

- Robinhood Wallet adoption and the share of wallet-funded users interacting with Robinhood Chain applications;

- Stock Token circulating float, turnover, bid-ask spreads and DEX or RFQ liquidity depth;

- USDG balances, Robinhood Earn participation and Morpho vault activity as indicators of stablecoin-funded financial behaviour;

- Lighter-linked perpetual futures activity and the extent to which that activity remains controlled, liquid and reputationally manageable;

- bridge inflows, authorised participant breadth and the number of economically relevant applications beyond Robinhood-linked assets;

- Gold attachment, deposit growth or retention uplift among users who engage with onchain products; [source needed]

- evidence of product pauses, freezes, legal warnings, supervisory friction or user misunderstandings around ownership and redemption.

The underlying principle is simple: do not track what flatters the chain, track what makes the customer relationship more valuable. If Robinhood Chain does not improve acquisition, engagement, retention or wallet share, the strategic story remains elegant but economically thin.

Bull case and bear case

The strongest credible bull case is that Robinhood becomes the default consumer gateway into tokenised public-market exposure outside the U.S., while stablecoins, DeFi yield and wallet-native trading fade into the background as infrastructure. In that outcome, Robinhood does not need users to become crypto enthusiasts. It only needs them to value always-on access, cross-border funding flexibility, composable collateral and a clean interface. Stock Tokens solve a real access problem for some international users. Stablecoins become invisible settlement rails. Lighter increases engagement. DeFi remains behind the scenes. Robinhood then emerges not as a crypto venue, but as the consumer RWA gateway.

The strongest credible bear case is equally clear. Stock Tokens do not offer true ownership, regulation caps expansion, liquidity remains thin, developers prefer Base, Solana, Arbitrum or Ethereum directly, and users simply do not care enough about onchain settlement for public equities to change their behaviour. In that version, Robinhood still has a working brokerage and wallet, but the chain remains a controlled distribution wrapper rather than a true piece of market infrastructure. The OpenAI-style controversy becomes a template for reputational drag, and traditional brokers replicate the useful UX features without importing the wrapper complexity.

The HOOD equity angle

For public-market investors, the answer is disciplined rather than dramatic. Robinhood Chain does not change the near-term HOOD model. The company is still driven by brokerage engagement, options, event contracts, net interest income, Gold, margin and platform assets. None of the available evidence suggests chain-linked activity is yet large enough to alter how the next several quarters should be modelled.

What the chain changes is the range of strategic outcomes available to Robinhood. It gives the company a credible route into tokenised-market infrastructure, international consumer finance and wallet-native financial behaviour without requiring the core U.S. brokerage to become a crypto exchange. In that sense, Robinhood Chain is better thought of as a call option than as a new segment. The analogy to Coinbase Base is useful only up to a point. Base sits atop a crypto exchange and a broad developer economy. Robinhood sits atop a broker and a consumer-finance relationship. That difference matters because Robinhood’s monetisation is likely to come less from raw chain activity and more from what the chain does to the broader customer system.

The most important investor question is therefore not “how big are chain fees?” It is “is Robinhood using the chain to make its distribution sharper?” If the answer becomes yes, through better international acquisition, deeper wallet usage, stickier deposits, stronger subscription attachment or more profitable product adjacency, the market will have a reason to assign strategic value before direct revenue is obvious. If the answer stays no, then the chain remains an interesting experiment that flatters the narrative more than the income statement.

Conclusion

Robinhood Chain is real enough to matter strategically, but not yet large enough to matter financially. That is the cleanest conclusion supported by the current evidence.

What is already proven is meaningful. Robinhood can launch an Arbitrum-based public mainnet. It can support wallet-native financial products. It can package tokenised economic exposure to public equities into live, transferable onchain instruments. It can integrate DeFi yield and perpetual futures into a broader wallet strategy. It can do all of this while the listed company remains in strong operating health.

What is not yet proven is just as important. There is no evidence yet of durable, broad liquidity in Stock Tokens. There is no proof that mainstream customers care enough about onchain settlement to change the economics of the Robinhood relationship. There is no proof that Robinhood Chain can attract broad developer adoption in a market already crowded with Base, Ethereum, Arbitrum, Solana and more crypto-native venues. There is no proof that tokenised stock wrappers can scale across jurisdictions without recurrent confusion about ownership, redemption and rights. And there is no sign yet that the chain is a materially important revenue contributor to HOOD.

That leaves Robinhood in an unusual strategic position. The company may be one of the few firms capable of making blockchain rails useful to mainstream finance users without asking those users to become blockchain enthusiasts. That is a real advantage. But the asset layer underneath remains more permissioned, more structured and more fragile than the word “onchain” implies. Robinhood’s success will depend less on decentralisation purity than on distribution discipline, disclosure discipline and liquidity discipline.

The decisive point, therefore, is not technological. It is commercial. The chain is not the moat. Robinhood’s distribution is the moat. Robinhood Chain matters because it may make that distribution programmable.

Sources

- https://robinhood.com/us/en/newsroom/robinhood-accelerates-global-expansion-robinhood-chain-mainnet-stock-tokens-agentic-trading/

- https://docs.lighter.xyz/trading/real-world-assets-rwas

- https://defillama.com/chain/robinhood-chain

- https://dune.com/entropy_advisors/robinhood-chain-network-overview

Partner Highlight

At insights4vc, we pay attention to teams that are not just shipping products, but shaping categories.

Moto is one of them. The company is building a premium card experience positioned as an alternative to traditional incumbents such as Amex, combining a high-end user interface with more modern financial infrastructure.

Moto is currently expanding access to a limited testing group. If you would like to test the product please contact us at: [email protected]

Cover Artwork

The Stone Bridge

Jan van der Heyden c. 1637

Risk Disclaimer:

insights4.vc and its newsletter provide research and information for educational purposes only and should not be taken as any form of professional advice. We do not advocate for any investment actions, including buying, selling, or holding digital assets.

The content reflects only the writer’s views and not financial advice. Please conduct your own due diligence before engaging with digital assets or related technologies, as they carry high risks and values can fluctuate significantly.