Cards are one of the few financial products that still control both the front end of commerce and the back end of money. The scale alone explains why the category still matters. In 2025, Visa reported $14.2 trillion in payments volume and 257.5 billion processed transactions; Mastercard said its network linked issuers and acquirers in more than 220 countries and territories; American Express reported $1.67 trillion of worldwide billed business on its proprietary cards; and the New York Fed said U.S. credit card balances ended 2025 at $1.28 trillion. Cards persist not because they are familiar, but because they still organise trust, liquidity, acceptance, and settlement at global scale.

The history of cards is best read as a sequence of institutional breakthroughs. Merchant tabs, department-store charge systems, charge plates, oil-company cards, and travel accounts all offered forms of deferred payment. What they did not solve was portable trust: the ability to carry spending power across merchants without rebuilding the relationship each time. That is why the major advances in card history were structural, not cosmetic. The winners were the systems that made trust portable, credit scalable, acceptance broad, and settlement governable.

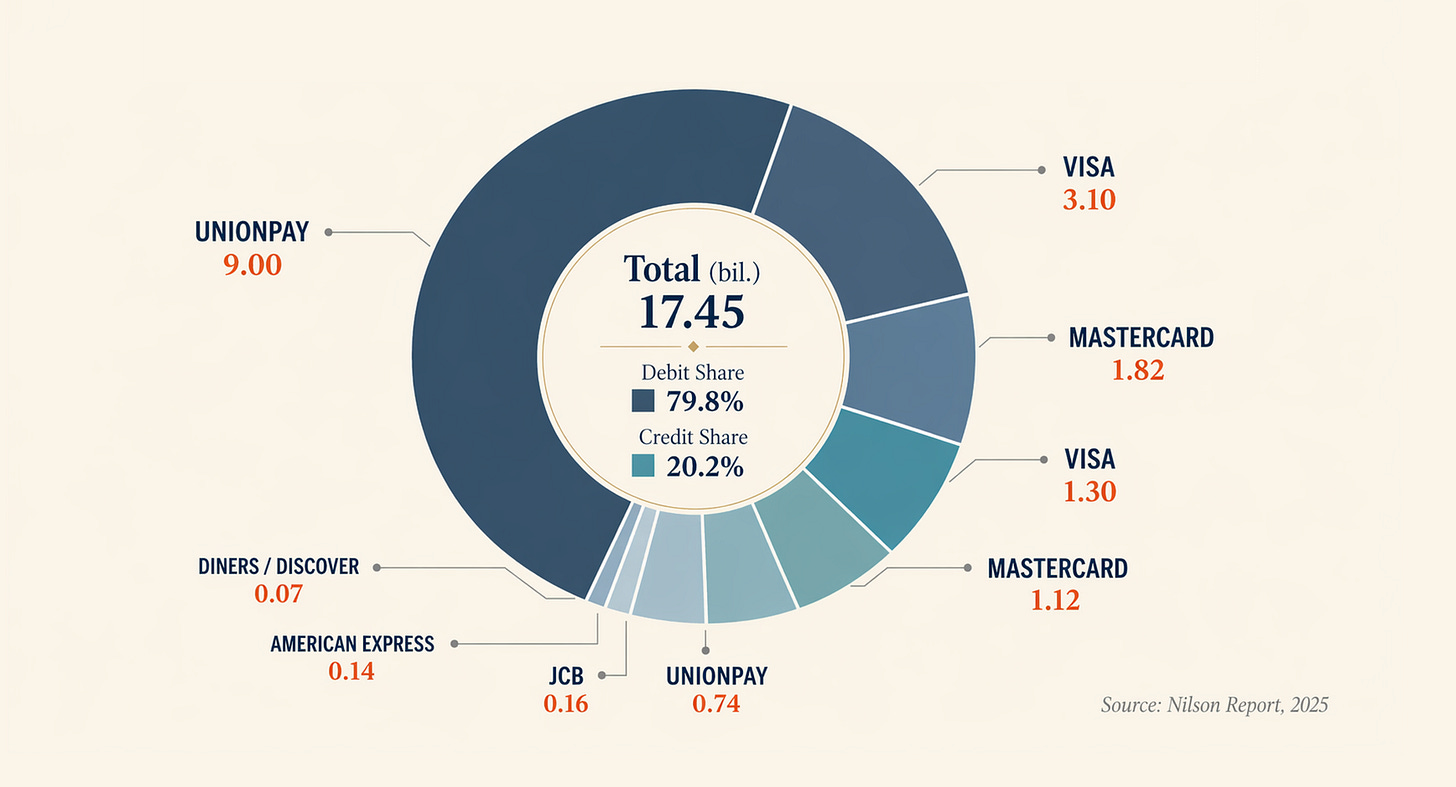

Global Network Cards in Circulation

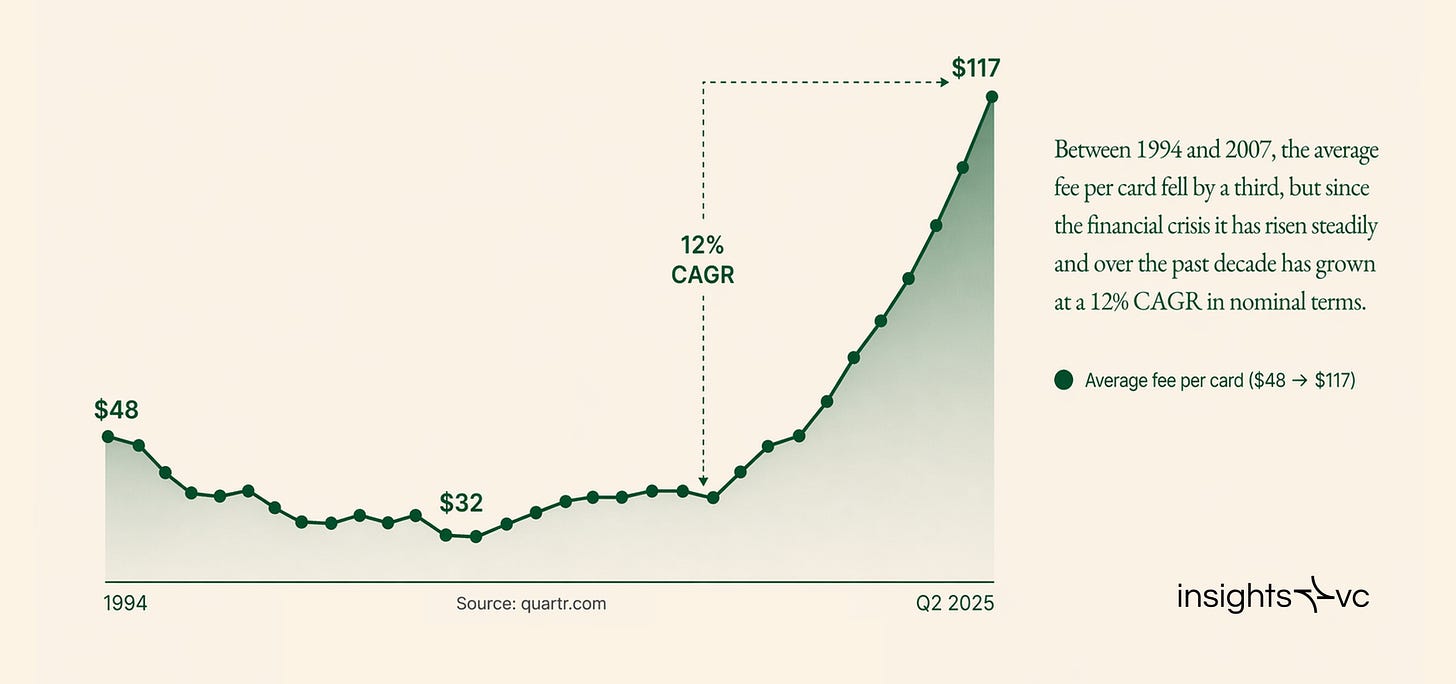

Premium cards show that the category’s economics remain deeper than simple payment processing. The strongest franchises do more than move transactions: they screen for desirable customers, generate subscription-like fee income, reinforce brand identity, and capture rich spending data. American Express remains the clearest example. In 2025, more than 70% of its new accounts were acquired on fee-paying products, average fee per proprietary card rose to $117, and net card fees approached $10 billion. That is not a fading prestige niche. It is a durable membership model.

This is why the stablecoin debate should be framed below the checkout experience, not at the card surface. Much of the first crypto-card wave changed the funding source but not the architecture: the merchant still saw a conventional card transaction, the network rules stayed in place, and in the U.S. the user could still face a taxable disposition when spending digital assets. In other words, many early crypto cards wrapped existing rails rather than replacing them.

The more serious development is now happening in the settlement layer. Visa has explicitly positioned stablecoins as infrastructure for back-end money movement and launched U.S. stablecoin settlement for select partners; Mastercard has framed its recent stablecoin push around interoperability, treasury, and programmable payments. That is the real analytical test. Stablecoins matter in cards only if they improve settlement timing, liquidity management, prefunding, reconciliation, receivables finance, or cost of capital. The back end changes first. The product category changes later.

Why Cards Still Matter

Cards still matter because they remain the most successful modern mechanism for combining identity, short-term liquidity, and universal merchant reach in one consumer-facing instrument. They are not only widely used; they remain deeply embedded in balance sheets, merchant operations, and household cash management. Visa, Mastercard, and American Express all reported large-scale growth into 2025, while U.S. revolving balances remained historically large. This combination is important. It shows that cards are not simply legacy payment symbols persisting out of habit. They remain central because they continue to intermediate both commerce and consumer finance at scale.

What looks mature on the surface is still economically rich beneath. Visa and Mastercard have become network powers, with revenue models based on switching, assessments, and value-added services rather than primarily on directly owning consumer lending exposure. American Express, by contrast, still shows the durability of the integrated premium model: a closed loop with direct merchant and cardholder relationships, meaningful fee income, and unusually strong spending per card.

Premium cards are especially revealing. Their resilience demonstrates that the category’s power does not depend only on revolving balances. Premium cards monetise aspiration, service, convenience, and status while also screening for customers with attractive spending profiles and generally stronger credit performance.

American Express’s 2025 results are illustrative: over 70 percent of new accounts were on fee-paying products, roughly 65 percent of new consumer account acquisitions came from Millennials and Gen Z, and net card fees grew for the thirtieth consecutive quarter.

That is why the most interesting present question is not whether cards are about to disappear. It is whether the back end beneath a highly familiar front end is beginning to move again. Visa’s stablecoin materials explicitly describe the need to modernise the back-end settlement layer, and Mastercard’s recent stablecoin push is similarly aimed at interoperability and programmable money movement. The surface product may stay card-like for a long time. The economics beneath it may not.

A Framework for Reading Card History

Card history is easy to misread when every visible product refresh is treated as a stage change. Many things improved the user experience without changing the architecture. A better framework is to track four layers: identity and membership, credit and underwriting, acceptance and network scale, and settlement, treasury, and back-end money movement. The key historical question is simple: what changed, and in which layer?

Identity and membership determine who belongs to the system and on what social terms. Credit and underwriting determine whether spending can scale impersonally. Acceptance and network scale determine whether a card’s promise is actually portable. Settlement and treasury determine whether the system can operate at scale without delayed funds, fragmented reconciliation, operational losses, or capital trapped in prefunding.

Some mechanisms cut across all four. Rewards reinforce identity, steer demand, and shape merchant economics. Fraud control is part trust technology, part cost management, and part network governance. Funding and receivables finance determine how far credit can scale and on what terms. Merchant economics link acceptance to discount rates, interchange, and data. That is why not every innovation deserves to be called a new stage. A prettier card, a new app, or a tokenised wrapper may improve distribution while leaving the system’s logic intact. The meaningful shifts are the ones that change who can be trusted, how spending is financed, how broadly the instrument is accepted, or how money actually settles.

This framework also sharpens the stablecoin debate. If a product still depends on the same sponsor banks, the same network rules, the same merchant experience, and the same substantive credit logic, then digital assets alone do not mark a stage change. The analytical question remains the same: which layer has actually changed?

Partner Highlight

At insights4vc, we pay attention to teams that are not just shipping products, but shaping categories.

Moto is one of them. The company is building a premium card experience positioned as an alternative to traditional incumbents such as Amex, combining a high-end user interface with more modern financial infrastructure.

Moto is currently expanding access to a limited testing group. If you would like to test the product and typically spend more than $5,000 per month, please contact us at: [email protected]

Before the Modern Card: Credit Existed, but Trust Was Trapped

Deferred payment long predates the modern general-purpose card. Local merchants ran tabs; department stores offered house accounts; charge plates mechanised account identification; oil companies and travel operators built branded payment instruments for repeat customers in specific use cases. The Smithsonian notes that the Charga-Plate, introduced in 1928, mechanised payment on a store account, while bank charge-account plans in the 1950s allowed customers to shop across multiple local merchants using a single bank card. The point is not that earlier systems lacked credit. They plainly had it. The problem was that credit remained trapped inside specific merchants, local geographies, or narrow travel verticals.

Charga-Plate

The travel sector offers a revealing prehistory. The airline industry’s Air Travel Card, developed in 1936, allowed passengers to “buy now, pay later” for air travel, and later became internationally accepted through what became the Universal Air Travel Plan. Oil-company cards and early travel-and-entertainment products similarly reflected repeat-use categories where the merchant valued predictable customers and the customer valued convenience within a bounded network. These products mattered because they showed that deferred settlement, branded access, and account-based billing could work. But they did not yet solve general-purpose portability.

Post-war consumer life made those limits harder to tolerate. Increased suburbanisation, automobile use, air travel, and business mobility all raised the value of taking one’s spending capacity beyond a single merchant or city. Small banks saw this pressure and experimented with charge-account banking in the 1950s, not initially as a pure lending business but as a service to merchants that were struggling to compete with department stores’ proprietary credit systems. Yet these early bank efforts remained operationally awkward and locally bounded. The trust still had to be assembled and serviced through cumbersome arrangements, with slow authorisation and weak economies of scale.

The prehistory therefore clarifies the central bottleneck. The problem was not the absence of credit. It was the absence of portable trust. Until third parties could stand behind the buyer across many merchants, and until merchants believed they would be paid without running their own credit departments, the modern card could not fully emerge.

Diners Club and the Birth of Portable Trust

Diners Club matters not simply because it arrived early, but because it turned local trust into portable trust. The Federal Reserve still describes Diners Club, launched in 1950, as the first general-purpose charge card. That is the real break in card history. Earlier charge plates and merchant accounts allowed deferred payment, but only inside a single store or tightly bounded commercial relationship. Diners Club inserted a third party between buyer and merchant, aggregated charges, billed the member later, and paid participating establishments itself. In doing so, it transformed trust from something trapped inside one merchant ledger into a service that could travel.

The origin story became part of the product. Diners Club still tells the famous tale that Frank McNamara forgot his wallet at a New York restaurant and decided there had to be a better way to pay. But Matty Simmons, who helped publicize the company in its early years, later said the story had been polished for effect and recalled the famous first use at Major’s Cabin Grill as a planned lunch rather than a spontaneous rescue from embarrassment. That tension is historically useful. The anecdote made the innovation legible, but the deeper breakthrough was institutional: a third party could stand behind the buyer across multiple merchants and sell convenience, centralized billing, and payment assurance as a business model.

Diners Club’s initial success came not from industrialized consumer lending, but from travel-and-entertainment spending, where convenience, record-keeping, and status mattered. The company says membership reached 42,000 by 1951, that it became the first internationally accepted charge card in 1953, and that it reached one million Clubmembers by 1959. That scaling pattern matters. Diners Club did not begin by democratizing revolving credit. It began by proving that merchants would pay for access to desirable spenders and that cardholders would pay for a portable, centrally billed spending instrument that worked across cities and eventually across borders.

Diners Club Credit Card

What is often missed is that Diners Club kept pioneering long after the famous origin anecdote. Its own history records the industry’s first corporate card program in 1975 and the industry’s first rewards program, Club Rewards, in 1984. That shift was strategic. As BankAmericard and Master Charge evolved into the dominant open-loop bankcard systems for mass consumer credit, Diners Club increasingly leaned into premium travel, expense management, and corporate T&E, where service, reporting, and brand identity still mattered. In other words, Diners Club did not remain important by winning the biggest lending war. It remained important by moving toward high-value spenders, business travel, and managed commercial payments.

By 2026, Diners Club is best understood not as the center of the mass card market, but as a premium global issuing brand and commercial-payments network that survived by moving up the value stack. Discover Global Network says Diners Club has issuers in 35+ countries and acceptance in more than 185 countries and territories. Its current materials emphasize commercial products, expense-management solutions, premium travel benefits, and global acceptance, while North American materials from BMO position the brand around corporations, professionals, rewards, and consumer cards that run with broad Mastercard acceptance. The strategic arc is clear: Diners Club began by making trust portable across restaurants, then extended that same logic into corporate travel, rewards, premium service, and cross-border network utility. Its lasting legacy is not the cardboard card itself. It is the idea that trust could be intermediated, branded, and scaled.

BankAmericard, Master Charge, and the Industrialization of Consumer Credit

The next decisive transformation came when banks entered at scale and turned the card from a travel-and-entertainment membership instrument into a mass consumer-credit machine. Bank of America’s 1958 Fresno test remains the most famous episode. Multiple historical sources, including David Stearns’ history of Visa and journalistic reconstructions of the “Fresno drop,” describe the mailing of roughly 60,000 unsolicited BankAmericards to households in Fresno. The strategy attacked the chicken-and-egg problem directly: merchants would not accept the card without cardholders, and consumers would not care without acceptance. Bank of America solved the problem by creating cardholders first.

BankAmericard

What changed here was the credit-and-underwriting layer, followed closely by the acceptance layer. Unlike Diners Club, BankAmericard was built for revolving credit and mass retail use. But this industrialisation arrived brutally. Unsolicited mailings exposed the system to fraud, delinquency, and operational chaos, while creating the scale merchants needed in order to justify acceptance. The same historical literature that records the genius of the Fresno strategy also records its losses. Consumers received preapproved spending power before risk tools were remotely adequate, and the industry later moved away from such mailings, which Congress eventually prohibited in 1970. The historical lesson is not that BankAmericard was reckless instead of visionary. It is that scalable consumer credit required a painful period of institutional learning in underwriting, fraud control, collections, authorisation, and merchant servicing.

The deeper transformation, however, was organisational. Dee Hock did not simply help expand BankAmericard; he helped convert a licensing scheme into a governed network. Stearns’ history describes the creation of National BankAmericard Inc. in 1970 as a response to operational breakdowns and governance failures in the licensed programme, while Visa’s own memorial notes that National BankAmericard Inc. was the pre-1976 name of the organisation that became Visa. This mattered because Visa’s power was not primarily that of an issuer. It was the power of a network administrator that standardised operating rules, interchange, participation, branding, and settlement across competing banks.

Master Charge evolved in parallel through reciprocal bank alliances. Mastercard’s own brand history records that in 1967 seventeen bankers met in Buffalo to formalise the Interbank Card Association, that the Master Charge brand was adopted in 1968, and that the name became Mastercard in 1979. Mastercard’s current 10-K still describes the network in recognisably four-party terms: it links issuers and acquirers globally, facilitates authorisation, clearing, and settlement, and typically leaves cardholder relationships to its customers rather than owning them directly. This is the mature form of what Visa and Master Charge became. They ceased to be “credit card companies” in the narrow sense and became network powers.

The synthesis is that the bankcard era solved two problems Diners could not. It made credit scalable through underwriting, delinquency management, and standardised processing, and it made acceptance broad through interoperable open-loop networks. In doing so, it shifted the industry’s centre of gravity from card issuing alone to network governance and settlement discipline.

American Express, Platinum, and the Strategic Meaning of the Black Card

American Express matters because its real business did not begin with plastic. It began with trusted movement: parcels, valuables, money orders, traveler’s cheques, and international travel services. That history is strategically important because it explains why Amex has long been strongest in categories where reassurance, service, and cross-border usability matter more than price alone. In that sense, American Express did not simply enter cards. It extended an older franchise built on trusted intermediation. The company became a card giant not by copying a bankcard utility model, but by turning reputation, affluent customers, and network control into a reinforcing system.

When the card business scaled, Amex also chose a structurally different model from Visa and Mastercard. Its closed-loop system let it act as issuer, network, and merchant acquirer, which meant it could observe both sides of the transaction and capture economics from both sides. That architecture still defines the franchise. In 2025, American Express reported $1.67 trillion of worldwide billed business, 86.6 million proprietary cards in force, more than 170 million merchant locations accepting its cards, and another $227.2 billion of processed volume from third-party-issued cards on its network. This is why Amex should not be read as a smaller version of Visa or Mastercard. It is an integrated payments and membership platform whose data advantage is inseparable from its economic model.

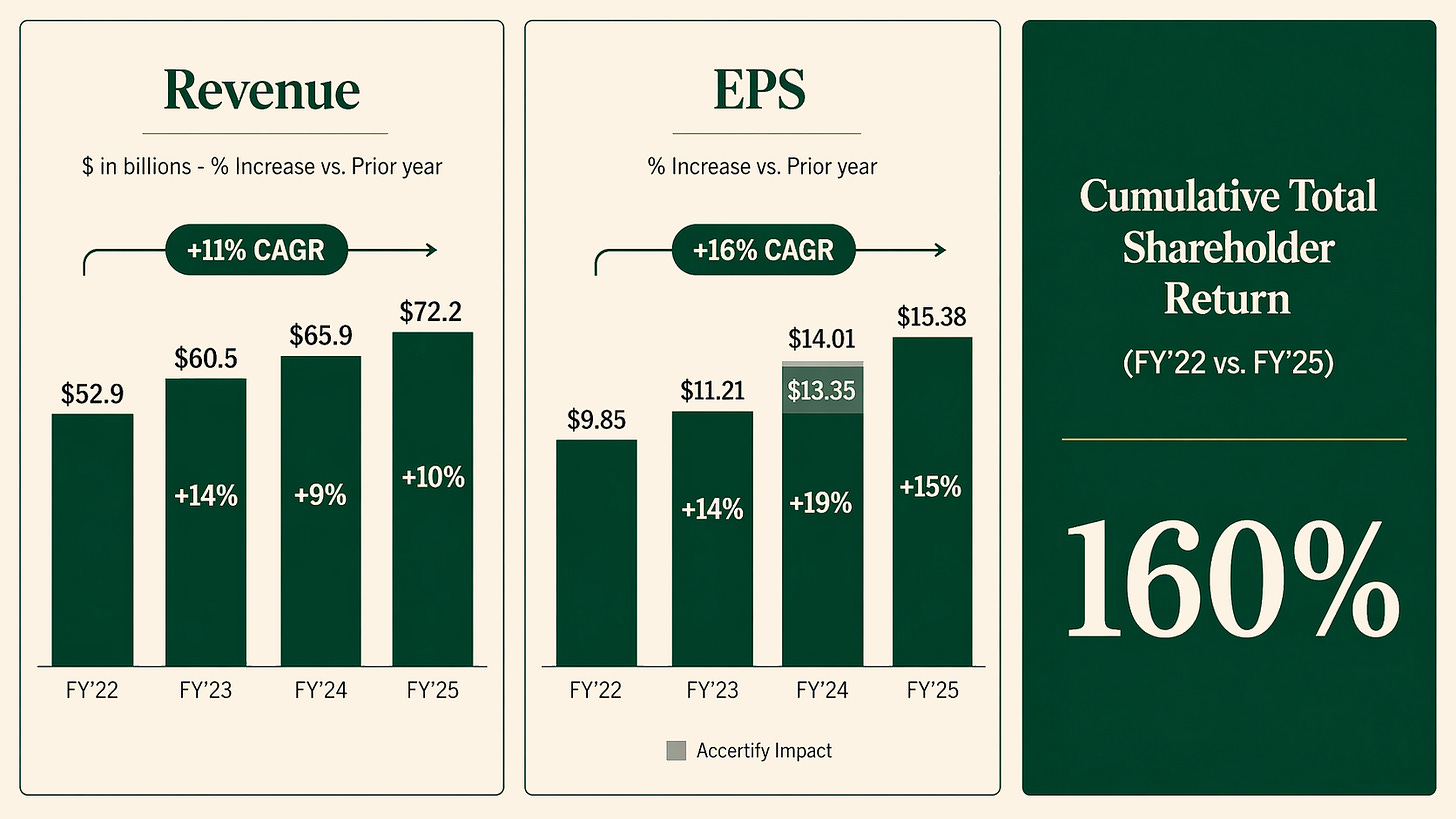

American Express 2022-2025 Financial Performance

The critical economic distinction is that Amex is spend-centric before it is credit-centric. The salad oil scandal is the clearest historical proof that American Express’s core asset was trust rather than any single product line. In 1963, an Amex warehousing subsidiary had vouched for warehouse receipts tied to inventory that turned out to be largely fictional, part of a fraud that exposed how powerful the American Express name had become as a certification device. The important point for card history is not the commodity fraud itself.

It is that the company chose to protect the credibility of the brand even at significant cost, because a franchise built on travelers cheques, charge cards, and premium service could not afford doubt around its promise to pay. Buffett’s later investment in Amex captured that exact insight: the scandal had damaged the stock far more than it had damaged the underlying consumer trust.

In 2025, American Express generated $54.9 billion of non-interest revenue against $17.4 billion of net interest income, reported nearly $10.0 billion of net card fees, and said average annual spending on its cards was approximately three times that of cards on other networks. Average proprietary basic Card Member spending reached $25,453, while average fee per card rose to $117. The point is not that lending is irrelevant. It is that the franchise is built primarily on spend, discount revenue, annual fees, and retention rather than on maximizing revolve. It wins by attracting customers who spend heavily, pay meaningful annual fees, remain highly engaged, and are valuable enough that merchants will tolerate higher economics to reach them.

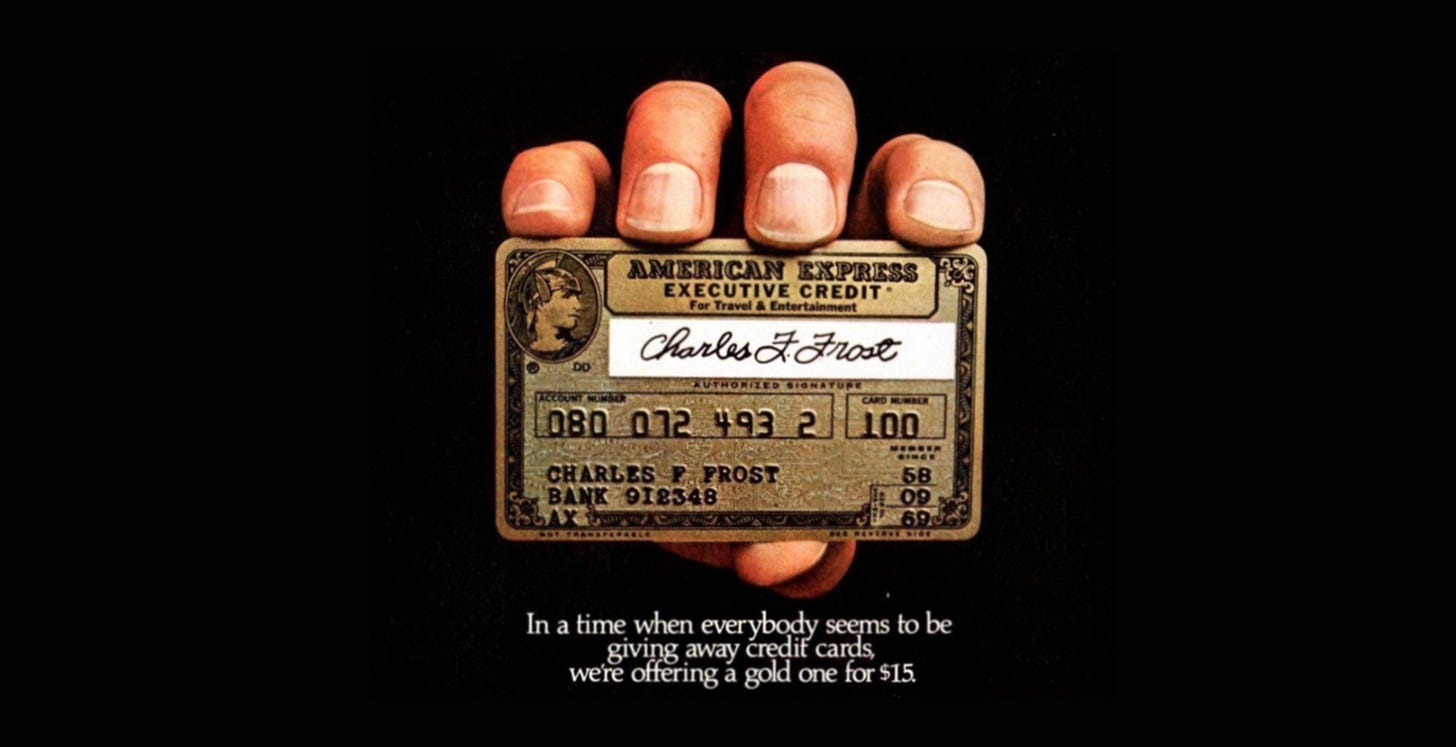

In 1968, the Amex Gold Card was introduced, and cost $15

That is the real strategic meaning of Platinum. Official Amex history places the Platinum Card’s launch in 1984, initially as an invitation-only product. That matters because Platinum was not just a premium travel card. It formalized a scalable membership thesis. It converted prestige into recurring fee revenue, benefits into retention infrastructure, and service into a justification for concentrating more spend inside the Amex ecosystem. Platinum also helped transform premium from a narrow executive niche into a structured product ladder. Gold widened the funnel, Platinum deepened the relationship, and Centurion created a credible apex above both.

The deeper point is that annual fees at Amex function as selection as much as monetization. They screen for customers who expect enough utility, status, convenience, or service to remain inside the system, which improves both spend quality and merchant value. This is why the model has remained powerful even in a mature card market. In 2025, Amex added 12.5 million new proprietary cards, acquired more than 70 percent of new accounts on fee-paying products, and said roughly 75 percent of new U.S. Gold and Platinum consumer acquisitions came from Millennials and Gen Z. That is not a fading prestige franchise. It is evidence that Amex has successfully repositioned premium cards as a subscription-like membership product for younger affluent consumers, not just for legacy business travelers.

Soaring Card Fees

The charge-card architecture also matters more than the marketing language suggests. American Express defines charge cards as products that generally carry no pre-set spending limits and are designed primarily as a payment instrument rather than a financing product, with each transaction authorized based on the likely economics of that spend and the cardmember’s most recent credit information and spending patterns. That means “no pre-set spending limit” is not a symbolic promise of infinite credit. It is a data-rich form of controlled elasticity. Amex is effectively selling monitored spending freedom to customers it understands unusually well, which is one reason the closed-loop model is so strategically valuable.

Centurion, or the Black Card, is best read through that same lens. Amex’s own history records its introduction in 1999 for a select group of its best customers in the U.K. and U.S., and the company leaned into the mystique that had already formed around an invitation-only ultra-premium card. Strategically, Centurion is not important because of volume. It is important because it gives the Amex hierarchy an upper boundary that cannot be commoditized. It is the institutional proof that the company does not simply issue payment products; it curates rank inside a governed service ecosystem. That, in turn, has a halo effect on Platinum and Gold below it, making the entire ladder feel more aspirational, more coherent, and harder to replicate with cashback alone.

Another underappreciated point is that American Express has defended premium card economics not only through branding and benefits, but through legal architecture. The company spent years fighting the U.S. government’s challenge to its anti-steering rules, which barred merchants from nudging customers toward cheaper cards at checkout. In 2018, the Supreme Court sided with Amex.

The value of affluent cardholders, high spend, rewards funding, and premium service only holds if merchants cannot systematically harvest Amex demand while rerouting transactions onto lower-cost rails at the last second. Premium cards, in that sense, are also a governance system.

The broader lesson is that American Express solved a problem that many challengers still have not: how to industrialize premium without flattening it into a commodity. It scaled exclusivity selectively, using closed-loop data, merchant relationships, fee-based membership, high-spend customers, and a carefully managed product ladder to build a business that is part network, part lender, part service brand, and part status architecture.

Rewards, Co-Brands, and the Financialization of Spend

Rewards changed cards by turning ordinary spend into a routed economic asset. At American Express, rewards are not only a marketing tool but an actuarial and balance-sheet discipline. The company describes Membership Rewards as its largest card-based rewards programme and estimates the liability using statistical and actuarial models built around the ultimate redemption rate and weighted average cost per point.

As of year-end 2025, the ultimate redemption rate for current participants was 96 percent, and even small assumption changes could move rewards expense materially. That matters because rewards are not just consumer-facing perks layered on top of spend. They are a managed financial obligation whose economics depend on redemption behavior, partner agreements, product design, and the quality of the cardholders the company attracts.

Diners Club records that it launched what it calls the industry’s first rewards programme in 1984. Over time, however, the biggest development was not rewards as a perk but rewards as a two-sided mechanism. On one side, issuers used points, miles, cashback, and elite benefits to influence consumer choice. On the other, those costs were underwritten through interchange economics, merchant discount structures, partner payments, and cross-subsidies from interest and fee income. Rewards made spend behaviour programmable before anyone used that word.

That system is not neutral. An IMF study on the redistribution effects of credit card rewards concludes that rewards generate transfers between consumers, while the CFPB has documented rising consumer complaints and friction around rewards administration and devaluation. In practice, rewards systems often favour households with stronger credit, larger spend, and greater ability to pay in full, while lower-income or debit-oriented consumers may still bear part of the cost through merchant pricing. Rewards are therefore not just marketing. They are distributional finance.

Co-brands took this logic further by connecting spend to external loyalty currencies. American Airlines’ long-running partnership with Citi, which the airline has described as dating back nearly four decades and extending through a renewed exclusive arrangement from 2026, shows how deeply banking and loyalty economics have fused. Reuters reported that in 2025 Delta received $8.2 billion from American Express and American Airlines received $6.2 billion from co-brand and related partners, while American also reported 8 percent growth in co-branded card spend in 2025. At that scale, the card is no longer a sidecar to the airline. It is one of the airline’s major economic engines.

The funding side evolved in parallel. Credit card receivables became widely securitised, allowing issuers to recycle capital and fund growth through master trusts and asset-backed structures. The Federal Reserve still separately tracks securitised credit card receivables, and issuer filings from Discover, Synchrony and Capital One show the continued centrality of credit card securitisation trusts and shelf registrations. Once spend, rewards, and receivables were financialised in this way, cards became more than a lending product. They became systems for routing demand, monetising loyalty, and scaling balance-sheet turnover.

The synthesis is that rewards and co-brands did not merely sweeten the card proposition. They made spend itself an engineered revenue stream whose behavioural, merchant, partner, and funding dimensions could all be optimised.

Private-Bank and Elite Cards: The Card as a Relationship Artifact

At the top end of wealth, the card stops looking like a standalone consumer-finance product and starts looking more like a portable expression of a much larger relationship. The economic objective is usually not to maximize revolving balances or card-only profitability. It is to deepen wallet share, extend the institution’s identity into everyday spending, and make a private-banking relationship feel present in the client’s daily life. That distinction matters because the real balance sheet often sits elsewhere, in advisory mandates, deposits, securities-backed lending, estate planning, and broader wealth management. J.P. Morgan Private Bank, for example, managed more than $2.9 trillion in client assets by mid-2025, while NatWest reported £58.5 billion of wealth assets under management and administration in 2025 and said in early 2026 that, with its planned Evelyn Partners acquisition, the combined business would reach roughly £127 billion of AUMA. In both cases, the card sits inside a much larger economic system.

The J.P. Morgan Reserve Card

The J.P. Morgan Reserve card is best understood through that lens. It is not positioned like a mass-market acquisition product, and that is the point. The relevant franchise is the private bank itself, which serves high-net-worth individuals and families globally and, in at least one disclosed market, described its typical client as holding at least 10 million Swiss francs of investable assets. What the card appears to do is carry a private-bank relationship into travel, payments, and daily liquidity management without forcing the bank to present itself as an ordinary card issuer competing on public signup bonuses or mass-market rewards marketing. Even its formal benefits architecture, presented through an official Visa Infinite guide, underscores a premium travel-and-protection logic rather than a broad consumer-credit growth story. The card’s strategic role is therefore closer to a relationship-maintenance instrument than to a scaled card P&L line in the usual retail sense.

This is an important distinction from American Express. Amex scaled premium by building a visible ladder from Gold to Platinum to Centurion and by monetizing annual fees, spend, and merchant discount across a broad mass-affluent base. A private-bank card scales differently. It scales as the underlying wealth franchise scales. The card is valuable because it creates continuity between the client’s balance sheet and the institution’s brand, because it turns a private-banking relationship into an everyday object, and because it can reinforce loyalty in a segment where the economics of the total relationship are often far larger than the economics of the card alone. In that sense, private-bank cards are not “smaller Amexes.” They are more like relationship artifacts issued by institutions whose core profit pools sit outside the card itself.

The Coutts Silk card shows the same logic in a more explicit retail-private-banking format. Coutts offers both a Silk Credit Card and a Silk Charge Card to private-banking clients, and the official product page makes the positioning unusually clear: no non-sterling transaction fees abroad, LoungeKey airport access, rewards and event privileges through the Thank You From Coutts programme, additional cardholders with tailored spending limits, and a single monthly statement for the primary cardholder. The card is also available to Coutts clients over 18 as part of the bank’s standard quarterly banking tariff, with no separate annual fee for the card itself. That combination is revealing. Coutts is not trying to mimic the economics of a fee-maximizing premium card franchise in the American Express mold. It is using the card as a service layer inside private banking, one that supports travel, family or household spending delegation, client treatment, and day-to-day convenience without forcing the customer to think of the product as a standalone financial proposition.

This helps explain why elite private-bank cards matter for the later stablecoin and onchain-collateral discussion. If a future premium digital-asset card succeeds, it may resemble the logic of J.P. Morgan Reserve or Coutts Silk more than that of a mainstream retail credit card. The relevant customer may care less about APR arbitrage or headline cashback and more about asset visibility, liquidity flexibility, service quality, global usability, discretion, and trust. In other words, the right comparison for some future collateral-backed premium products may not be the ordinary rewards market at all. It may be the private-banking tradition, where the card is strategically important precisely because it is not the whole relationship. That is the deeper lesson of elite banking. At the highest end of the market, the card is not just a payment method. It is a daily-life extension of balance-sheet intimacy.

Fintech Improved the Interface, Not Always the Rails

The fintech wave of the 2010s and early 2020s improved the card interface dramatically. Firms such as Brex, Ramp and Marqeta made card issuance, spend control, embedded distribution, virtual cards, and finance workflow integration vastly more flexible. Marqeta’s 10-K presents the company as a cloud-native issuing and processing platform with APIs, dynamic spend controls, just-in-time funding, and a global card-issuing stack. That is real progress. It reduced the cost and time required to launch card programmes and allowed cards to become programmable inside software products.

But most of this innovation occurred above the deepest rails. Ramp’s disclosures make plain that its various card products are issued by sponsor banks including Celtic Bank, Column, Sutton Bank, and Lead Bank, all pursuant to Visa licences. Brex’s legal terms similarly disclose issuance by banks such as Emigrant, Fifth Third, or Sutton. Marqeta’s own filings emphasise that it bridges customers to issuing banks and card networks, shares interchange economics, and manages complexity with sponsor banks and network rules. In other words, fintech transformed controls, distribution, and user workflow, but much of the old architecture remained in place. Sponsor-bank dependence, network economics, merchant acceptance rules, and settlement structures mostly persisted.

That is why “modern card issuing” and “new rails” should not be conflated. The fintech stack often gave operators more software-defined control over an old card machine. That was commercially meaningful, especially in B2B spend management. But it did not necessarily rewrite the economics of acceptance, settlement timing, or treasury funding. The layer that changed most was the interface between business user and programme manager. The hidden money movement layer changed much less.

Crypto Cards

The first major wave of crypto cards mostly changed what funded the card, not what the card was. Coinbase’s official materials describe the Coinbase Card as a Visa debit card, issued by Pathward and powered by Marqeta, that allows users to spend cash or crypto wherever Visa debit cards are accepted. Crypto.com’s Visa card materials similarly disclose mechanics that look more prepaid-like than novel-credit-like: cryptocurrency cannot be loaded directly on to the card; instead it is converted into local currency and loaded for spending or ATM withdrawal. Merchants, meanwhile, generally continue to receive ordinary fiat settlement through existing card rails.

That structure matters analytically. If the merchant sees a normal Visa or Mastercard transaction, if the network remains in place, if underwriting is unchanged or absent, and if settlement still ends in fiat on the merchant side, then the product has not created a new card architecture. It has created a funding-source wrapper around an existing one. Useful wrappers can still matter commercially. They can attract users from exchanges, support spend from digital balances, or offer rewards in tokens. But their stage significance should not be overstated.

In the United States, tax treatment compounded the problem. The IRS continues to treat digital assets as property, and paying for goods or services with digital assets can trigger capital gain or loss recognition. That means the everyday use case of “spend your crypto” often carried an accounting burden that regular cardholders were never asked to bear. It is difficult to build a truly frictionless mainstream payment category on top of a taxable-disposition regime.

The conclusion is not that crypto cards were pointless. It is that most of them did not yet change the decisive layers. They changed the source balance and sometimes the rewards wrapper. They did not fundamentally rewrite underwriting, merchant acceptance, network governance, or settlement architecture.

Moto and the Emerging Boundary Between Premium Cards and Onchain Collateral

Moto is interesting not because it is just another crypto card, but because it is trying to import the economics of premium charge cards and private banking into an onchain balance-sheet model. The team is explicit that Moto should not be framed as a debit card or a generic “stablecoin card,” but as a secured credit product in which users are debited at the end of the month, and where the closest useful comparisons are American Express and private banking rather than crypto spending apps. That distinction is strategically important. Most earlier crypto cards simply changed the funding source at the point of sale. Moto’s thesis is more ambitious: digital collateral and DeFi capital efficiency may be able to support a better premium spending relationship without forcing the user into constant liquidation or into thinking like a trader every time they pay.

Moto Card

MoonPay’s April 2026 announcement helps clarify where some of the real innovation sits, and it is not on the card face. Through Virtual Accounts powered by Iron, Moto added dedicated named accounts and fiat funding rails, including ACH, Fedwire, and SEPA Instant, allowing users to move from bank money into the Moto system with less friction and faster settlement. That matters because it points to a deeper category shift beneath a familiar card surface. The relevant question is not whether a user can spend with a Visa Infinite product, but whether the funding, treasury, and collateral stack behind that experience becomes materially more fluid than in traditional card programs. If that layer improves, then Moto is not merely wrapping legacy rails in crypto language. It is testing whether premium card economics can be rebuilt on a more flexible money movement architecture.

Shimon Newman’s vision, as CEO of Moto, appears sharper than the usual crypto-card pitch because it is aimed upward, not outward. From day one, Moto has prioritised high-net-worth users, deposits, and monthly spend, with a clear ambition to win mindshare as a genuine competitor to American Express and Atlas rather than as a niche crypto tool. This frames Moto as a product for the next generation of wealth, where capital efficiency is converted into better user economics, stronger service quality, and a more credible premium experience. In that sense, Moto is best read not as a payments novelty, but as an attempt to build an onchain version of relationship finance, one in which collateral, liquidity, and lifestyle benefits are designed to reinforce each other.

The real analytical question, then, is not whether Moto proves that “stablecoin cards” have arrived. It is whether onchain collateral, programmable credit facilities, and upgraded funding rails can support a premium spending relationship that feels closer to private banking than to crypto payments. That is a much more serious ambition, and a more useful way to read the company. If Moto works, it will matter less because it put digital assets behind a card, and more because it may show how the next premium card model can be built with balance-sheet design first and interface second.

Stablecoins and the Settlement Layer

Stablecoins become strategically interesting when they are treated not as a retail spectacle but as settlement infrastructure. Visa now says so explicitly. In 2025 it described stablecoins as improving the efficiency and utility of back-end financial and money movement infrastructure, and outlined a settlement pilot under which select clients could satisfy VisaNet obligations in USDC. Visa’s public materials further state that select programmes can use seven-day-a-week stablecoin settlement, reducing operational friction for issuers while preserving the consumer card experience. By December 2025, Visa announced U.S. stablecoin settlement with seven-day windows and bank participants including Cross River Bank and Lead Bank.

This is where the economics begin to matter. Traditional card settlement still carries timing frictions, weekend gaps, prefunding requirements, reconciliation burdens, and trapped working capital. If obligations can be met in a stablecoin on a seven-day basis, then issuers and programme managers may be able to improve liquidity timing, reduce idle balances, and automate treasury operations. That does not necessarily change the merchant experience. In many stablecoin-linked card arrangements, merchants still receive fiat. But it can change the capital and treasury experience of the institutions behind the programme. The back end changes first.

Mastercard’s recent initiatives point in a similar direction. Its April 2025 stablecoin announcement spoke of end-to-end capabilities from wallets to checkouts, merchant settlement options, and the broader ability to connect stablecoins, tokenised deposits, and traditional money through the Mastercard Multi-Token Network. Mastercard’s current 10-K remains rooted in the four-party payments network, authorisation, clearing, and settlement. What is changing is not the company’s abandonment of card rails, but its attempt to add programmable money movement beneath them.

Newer infrastructure firms show the same pattern. Visa and Bridge announced in March 2026 that Bridge’s stablecoin-backed Visa cards, issued through Lead Bank, would have the capacity to settle card transactions onchain with Visa. Rain’s March 2026 announcement said its expanded Visa membership would enable consumer and corporate card programmes powered by stablecoin infrastructure in Asia-Pacific. Visa’s own stablecoin paper goes further by highlighting Credit Coop as an example of tokenised private-credit infrastructure: through Credit Coop, Rain borrows USDC secured by its card receivables. That detail is unusually important. It points beyond simple payment funding and towards tokenised receivables finance, where collateral visibility and liquidity access could improve together.

MoonPay’s Virtual Accounts, powered by Iron, suggest another piece of the same puzzle. MoonPay markets them as native virtual accounts in users’ names, enabling fiat deposits in USD, EUR and GBP with API-based conversion to stablecoins. Iron, now a MoonPay company, presents itself as API infrastructure for virtual accounts, payment flows, and fiat-to-stablecoin services. Even where no new consumer card category emerges, this sort of infrastructure can improve how programmes move between bank rails and stablecoin liquidity, and how treasuries manage prefunding and reconciliation.

The synthesis is precise. Stablecoins may matter in cards if they improve settlement timing, treasury mobility, prefunding, receivables finance, collateral transparency, or cost of capital. They do not need to replace cards, and they may never replace the merchant-facing card experience. Their plausible importance lies beneath the experience, in how the system is funded and settled.

Constraints and the Burden of Proof

Serious analysis also demands a serious downside case. The Bank for International Settlements has been clear that stablecoins perform poorly against key requirements of a sound monetary system and that issues of integrity, elasticity, and singleness remain unresolved. Even industry-sponsored documents are cautious. Visa’s own lending and stablecoin materials warn that cross-border transfer capabilities vary, are subject to regulatory restrictions that differ by jurisdiction, and require users to understand legal and compliance implications. There is therefore no warrant for assuming that stablecoin settlement will glide frictionlessly into scaled card infrastructure.

There are at least four categories of constraint. The first is legal and prudential ambiguity. Stablecoins touch money transmission, payments law, securities questions in some contexts, custody, reserve management, and potential bank-like oversight. The second is operational complexity. Running twenty-four-hour settlement, managing wallet and custody risk, and reconciling onchain and offchain records are not trivial upgrades. The third is cross-border fragmentation. A card network can be globally recognisable while the legal status of stablecoin activity varies by country, by institution type, and by use case. The fourth is economic capture by incumbents. Even if stablecoins reduce funding friction, the benefits may be taken by networks, sponsor banks, dominant infrastructure providers, or large programme managers rather than being passed through to end users.

The burden of proof is therefore high. Advocates must show not only that a stablecoin can sit behind a card, but that the resulting system is safer, cheaper, or more capital-efficient in practice once compliance, custody, prefunding, and operating complexity are accounted for. Some gains may prove real. Others may simply represent a new funding layer attached to the familiar economics of cards. Stablecoins do not escape the structural disciplines of payments merely by being programmable.

A Taxonomy of the New Card Stack

Analytical precision matters because the same metal rectangle can conceal very different economics. A charge card is best understood as a spending instrument usually designed for pay-in-full behaviour, often with no pre-set spending limit and dynamic authorisation logic, as American Express’s filings explicitly describe. A revolving credit card is a product in which balances can persist and incur interest under defined terms, which is also explicitly distinguished in Amex’s product definitions. A debit card draws from a linked account balance, as Coinbase’s product language and Visa-debit framing make plain. A prepaid card is loaded in advance or funded through conversion into a stored balance, which aligns more closely with how Crypto.com describes its Visa card mechanics.

A crypto-funded card is not necessarily a new category at all. It is often an existing debit or prepaid card whose source balance is a digital asset account that is converted into fiat during or before the transaction. A stablecoin-settled card is something narrower and more infrastructural: a card programme whose obligations or treasury movements may settle in stablecoin even if the merchant still experiences ordinary card acceptance and fiat payout. A collateral-backed premium spend or credit product is something else again: a product in which digital assets or other collateral support spending privilege, potentially without requiring the user to liquidate first, and where the key economics may sit closer to private banking or securities-backed liquidity than to ordinary retail card lending.

These distinctions are not semantic niceties. They determine how one should analyse risk, underwriting, settlement, regulation, and competitive threat. A product can look novel at the interface while remaining conventional in its balance-sheet and settlement logic. Conversely, a product can look familiar to the user while hiding meaningful back-end change. Good analysis has to separate those cases.

Conclusion

The history of cards is not a story of a static product surviving on habit. It is a history of repeated institutional upgrades across trust, credit, acceptance, and settlement. Merchant tabs and house accounts offered deferred payment but trapped trust inside local relationships. Diners Club made trust portable. BankAmericard and Master Charge scaled credit and merchant acceptance through governed networks. American Express proved that cards could also function as durable membership systems, where spending, service, data, and status reinforced one another economically. Fintech later improved issuance, controls, and user experience, but in many cases left the deepest balance-sheet and settlement architecture largely unchanged.

That is why the next chapter should not be judged by whether the card in a wallet looks different. The more important question is whether the financial machinery beneath it is becoming more efficient, more programmable, and more capital-light. Stablecoins matter only if they improve something fundamental in the back end: settlement timing, treasury mobility, prefunding, reconciliation, collateral use, receivables finance, or cost of capital. If they do not materially change those economics, then they remain an interesting wrapper around an old system rather than a true stage change in card history.

From insights4vc’s perspective, the most important signal is that serious experimentation is now moving below the checkout experience and into the hidden layers of money movement and balance-sheet design. Visa, Mastercard, and a new generation of infrastructure firms are all pointing in that direction. Moto is one example worth watching, not as proof that crypto cards have arrived, but as a test of whether premium card economics can be rebuilt around onchain collateral and more flexible funding rails.

The most plausible future is therefore not a world in which cards disappear, but one in which the familiar card interface increasingly sits on top of a different settlement and treasury stack. The front end may remain recognisable for years. The back end may change much faster. If that transition holds, the next important card companies will likely look less like simple issuers and more like hybrids: part premium membership system, part software-defined financial programme, and part infrastructure layer for tokenised money. That future is still unproven, but its outline is becoming visible.

Sources

- Visa Inc. Visa Annual Report 2025

- Mastercard Incorporated. Fiscal Year 2025 Form 10-K Annual Report

- American Express Company. Annual Report 2025

- Federal Reserve Bank of New York, Research and Statistics Group, Center for Microeconomic Data. Quarterly Report on Household Debt and Credit, 2025: Q4.

- Visa Inc. “Visa Launches Stablecoin Settlement in the United States, Marking a Breakthrough for Stablecoin Integration.”

- Mastercard. “Mastercard Unveils End-to-End Capabilities to Power Stablecoin Transactions – from Wallets to Checkouts.”

- Bank for International Settlements. “III. The Next-Generation Monetary and Financial System.” In BIS Annual Economic Report 2025.

- Moto https://www.moto-card.com/

- Quartr: American Express: An Empire of Plastic https://quartr.com/insights/edge/american-express-an-empire-of-plastic

Cover Artwork

A Café in Copenhagen

Frants Henningsen, c. 1906

Risk Disclaimer:

insights4.vc and its newsletter provide research and information for educational purposes only and should not be taken as any form of professional advice. We do not advocate for any investment actions, including buying, selling, or holding digital assets.

The content reflects only the writer’s views and not financial advice. Please conduct your own due diligence before engaging with digital assets or related technologies, as they carry high risks and values can fluctuate significantly.