Few private fintech companies have combined scale, growth, and profitability as convincingly as Revolut. With more than 70 million customers, rising balance-sheet capacity, and an increasingly diversified revenue mix, the company is beginning to resemble a global digital bank more than a traditional challenger fintech.

In this report, we examine Revolut’s evolution, the strengths and constraints of its current model, and the role digital assets play within its broader strategic direction.

Revolut - Key 2025 Metrics

Executive Summary

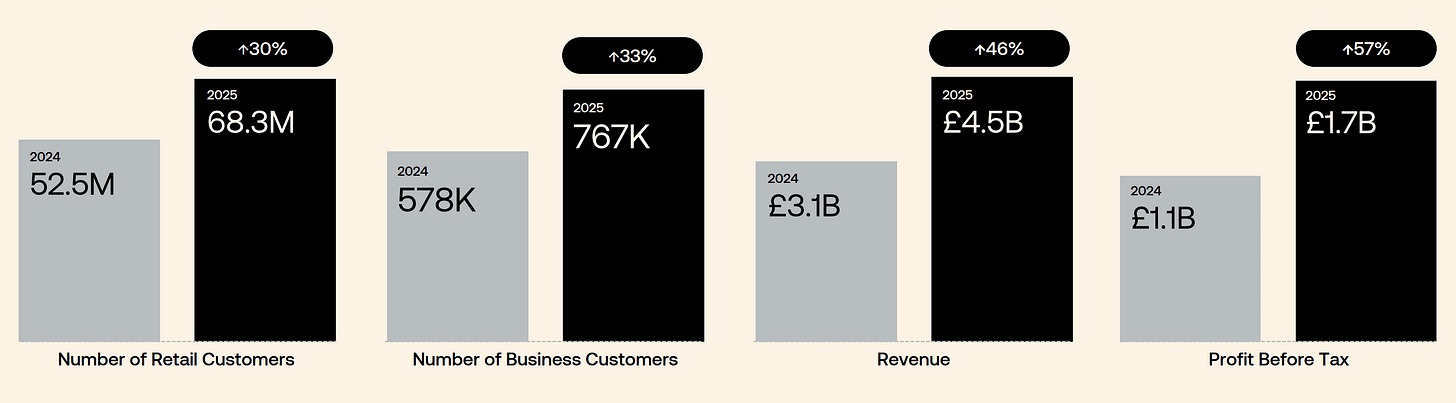

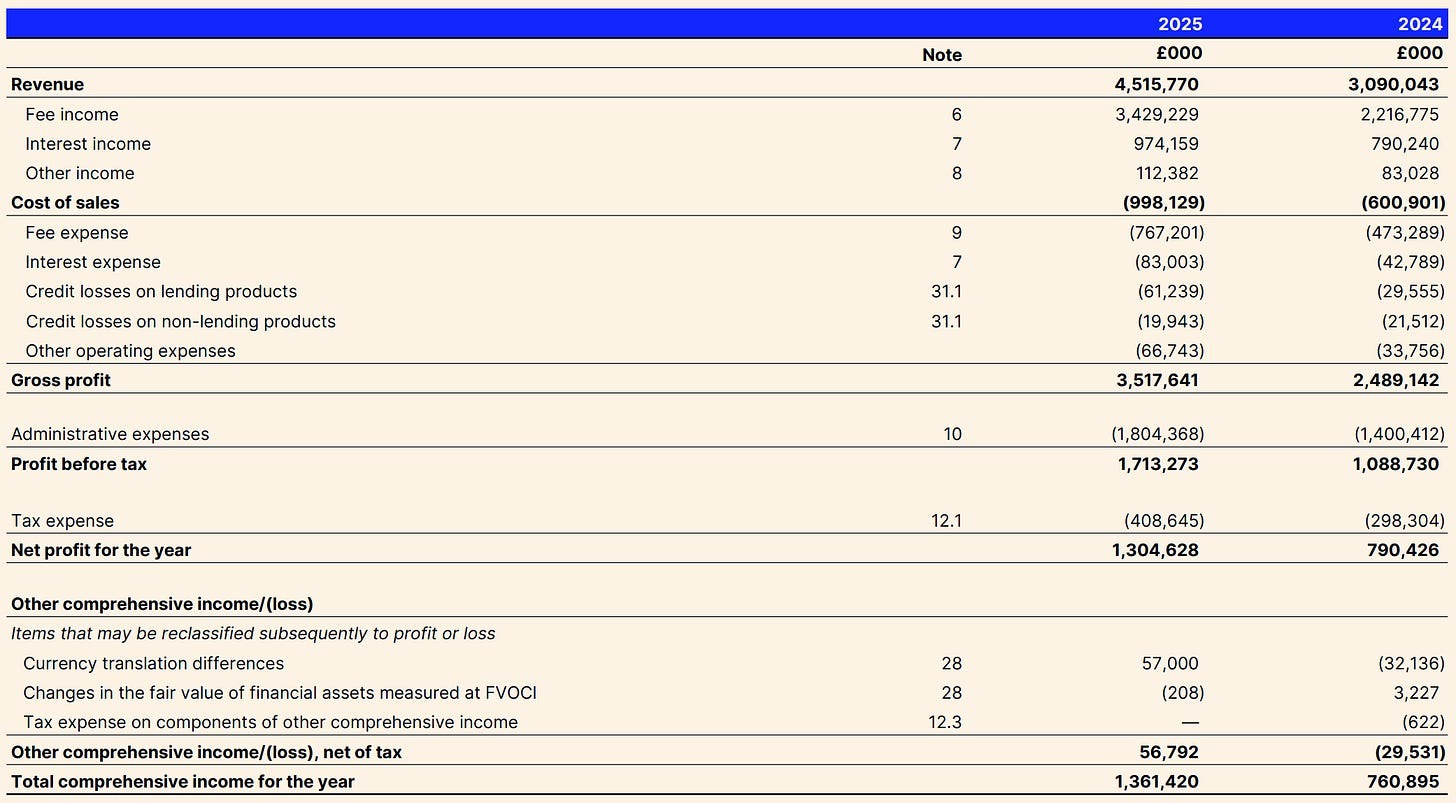

- Scale: Revolut now serves over 70 million retail customers and ~0.8 million businesses, up 30% and 33% respectively in 2025. 2025 revenue was $6.0 billion (up 46% YoY) and profit-before-tax $2.3 billion (+57%). Total customer balances rose 66% to $67.5 billion, outpacing customer growth.

- Diversified Model: 11 distinct product lines each generate >$135 million annually, with roughly balanced contributions from subscriptions, payment fees, foreign exchange, wealth services and interest income. Crucially, Revolut Business (corporate banking) now contributes ~16% of total income. The lending portfolio has grown 120% to $2.9 billion in 2025, and interest income ($974 million) is rising (23% YoY) as lending scale expands. These shifts begin to tilt Revolut toward more stable, interest-based income, though fee income (cards, FX, etc.) remains the largest component.

- Customer Engagement: Product innovation and network effects are driving deep engagement. In Europe, roughly 1-in-5 working-age adults now use Revolut. In 2025, Revolut added 16 million new users (total 68.3 m by Dec 2025), and 63% of new retail customers came via organic referrals. Paid plan (subscription) adoption grew 42% YoY, and the RevPoints loyalty program jumped to 17 m users (from 6.6 m), reflecting cross-selling success. These metrics indicate Revolut is capturing more “share of wallet” per user, not just adding one-off accounts.

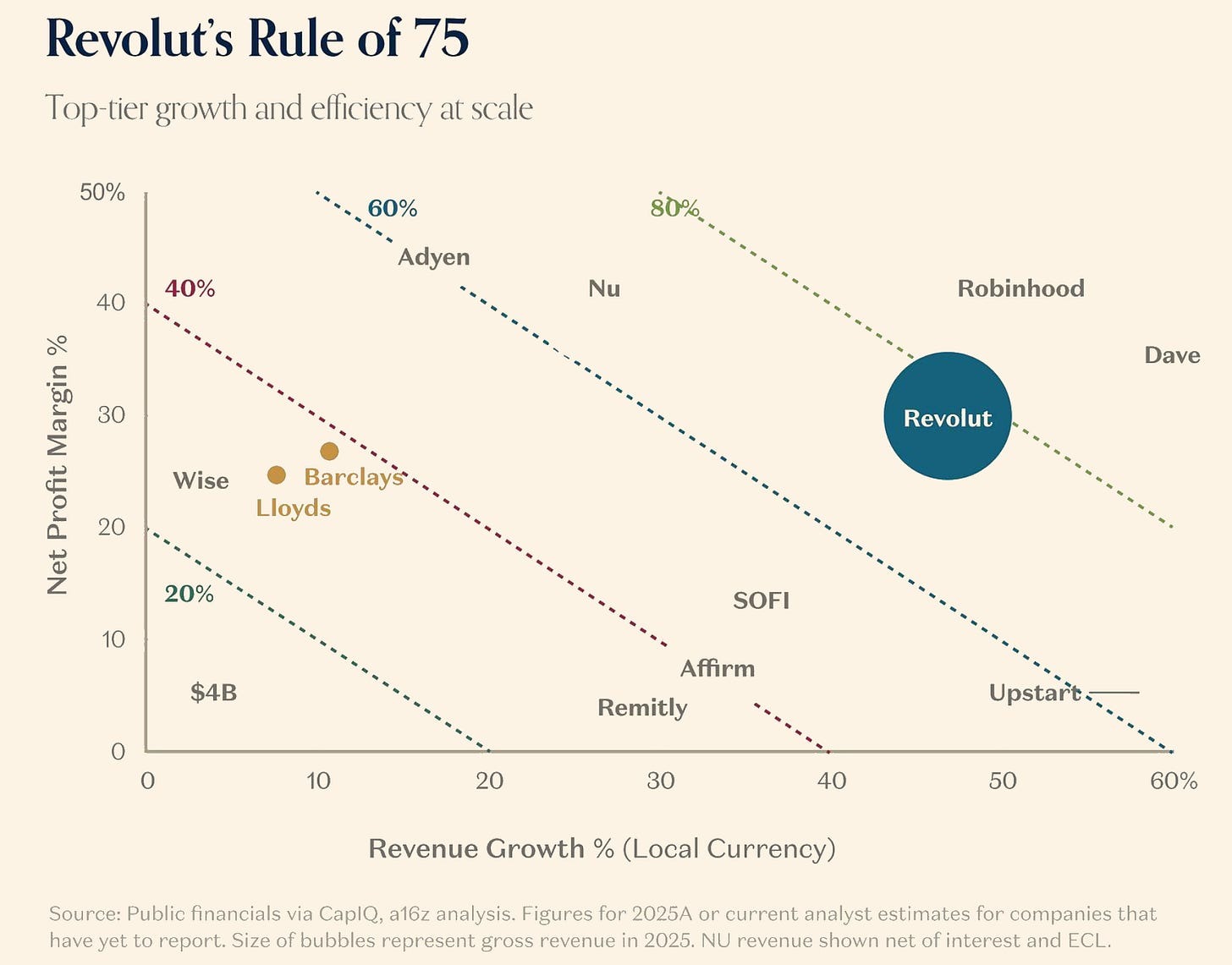

- Strategic Strengths: Revolut’s advantages include its broad product suite (banking, payments, wealth, crypto) and agile tech platform. It has won scale in its core markets (e.g. UK, Europe) and is successfully launching new services (e.g. mortgages, mobile telecom) to entrench users. Low-cost digital delivery and 24/7 chat support help keep costs down. The business has hit strong operating leverage – 2025 PBT margin was 38%, up from 35% in 2024 – suggesting its model can fund continued growth. As an evidence point, management repeatedly emphasizes a “diversified, resilient model” powering its record results.

- Key Risks: Rapid growth brings regulatory and execution risks. European regulators fined Revolut’s EU bank €3.5 m in 2025 for AML compliance gaps. UK regulators have scrutinized its cross-border risk controls, delaying its full UK banking rollout. Average per-customer balances remain low, and only ~45% of users now use Revolut as their primary account, so deposit funding and retention must improve. Market-dependent fees (foreign-exchange, card spend) and crypto-linked revenues are cyclical – as admitted by analysts – so profitability depends on maintaining rapid user/product growth. Execution of new bank licenses (e.g. US charter in process) and expanded lending are unproven at scale.

- Digital-Assets Context: Revolut’s crypto strategy is integrated but not central. It began offering cryptocurrency trading as early as 2017, and has since built a regulated digital-assets platform (EU CASP license obtained). Today Revolut offers custodial crypto trading (over 250 tokens on the Revolut X exchange) with advanced features (0% maker fees, API access). However, crypto trading represents one line in the wealth/investment product family (alongside stocks, ETFs, staking), and management has not singled it out in 2025 results. Analytical inference: Crypto likely remains a modest part of overall revenue today, serving mainly as a user-activation and engagement tool. A recent FCA sandbox trial (GBP stablecoin pilot) hints at future innovation. Overall, crypto assets are a strategic growth area for Revolut – they enhance its super-app positioning and give it a regulated bridge into digital finance – but they bring volatility and regulation risk, and should be viewed as complementing, not overshadowing, the core banking story.

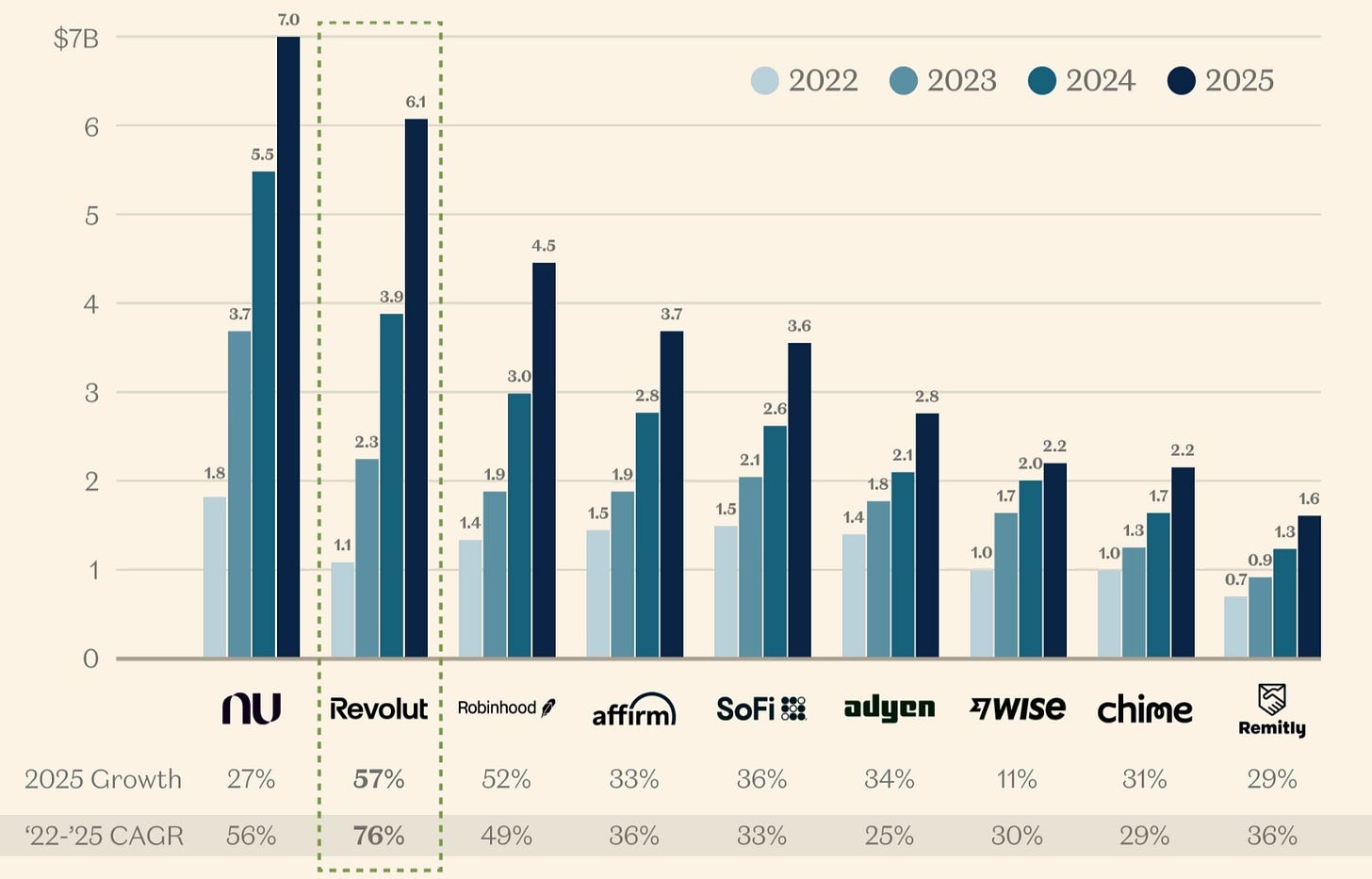

Revolut is One of the Fastest Growing Financial Institutions (Source: Revolut 2025 Annual Report, a16z analysis)

Strategic Snapshot

- Founded/Headquarters: 2015 in London by Nik Storonsky and Vlad Yatsenko. Originally a travel/FX fintech, Revolut quickly expanded its banking and payment services worldwide.

- Customer Base: ~70 million retail customers (up from ~50 m in 2024), plus ~767 k businesses (up 33% YoY). Strong growth continues: ~16 m new users in 2025 (equivalent to ~1 m every 17 days in late 2025). In Europe 1-in-5 working-age adults use the app, and Revolut is a top finance app in multiple countries, indicating broad reach and adoption.

- Core Geographies: Europe (EU and UK) remains the heartland, supplemented by launched operations in Asia-Pacific (Singapore, Australia), and ongoing expansion in Americas (full UK banking launched Mar 2026; US bank charter applied; Mexico banking license achieved Jan 2026). It now operates as a licensed bank in 30+ of its 40 target markets. Regulatory access (e.g. EU passport via Lithuanian bank license, UK PRA license, CySEC CASP license) defines its footprint.

- Business Lines: Revolut bills itself as an integrated financial platform. Key segments: Personal Banking (multi-currency accounts, debit cards, FX transfers, e-money wallets); Lending (unsecured personal loans, credit cards, and recently mortgage refinancing in Lithuania); Wealth & Investing (stock trading, ETFs, crypto trading through Revolut X, and crypto staking in certain markets); Premium Subscriptions (Plus/Premium/Metal plans with added benefits); Corporate Financial Services (Revolut Business accounts, payments, corporate cards like Titan) – ~750k companies use it, with $365 billion business transactions in 2025.

- Regulatory Footprint: In Europe it operates under a full banking license via Bank of Lithuania (EU passport) and holds a CySEC “Crypto Asset Service Provider” license (the first under MiCA) for its EU crypto arm. In March 2026 it secured full UK banking permission (PRA) – enabling FSCS-protected deposit accounts and loans for ~13 m UK users. It is also pursuing a French banking license and a U.S. national bank charter. Revolut Ltd is FCA-regulated (e-money, crypto AML) in the UK, and Revolut Bank UK was authorized in 2026.

- Strategic Identity: Revolut straddles several roles. It began as a low-fee, travel-focused neobank, but has transformed into a “financial super-app” blending banking, payments, and investment. Management itself speaks of “transitioning into a truly global bank”. Its scale and license – now rivaling mid-tier banks (13m UK customers) – set it apart from typical small challenger banks. However, its product velocity, digital UX, and customer-driven growth pattern also differentiate it from incumbents. In practice, Revolut can be seen as a hybrid: a digital-first bank platform (neobank) with expanded offering (wealth management, crypto, connectivity services), all delivered via one app ecosystem.

How Revolut Got Here

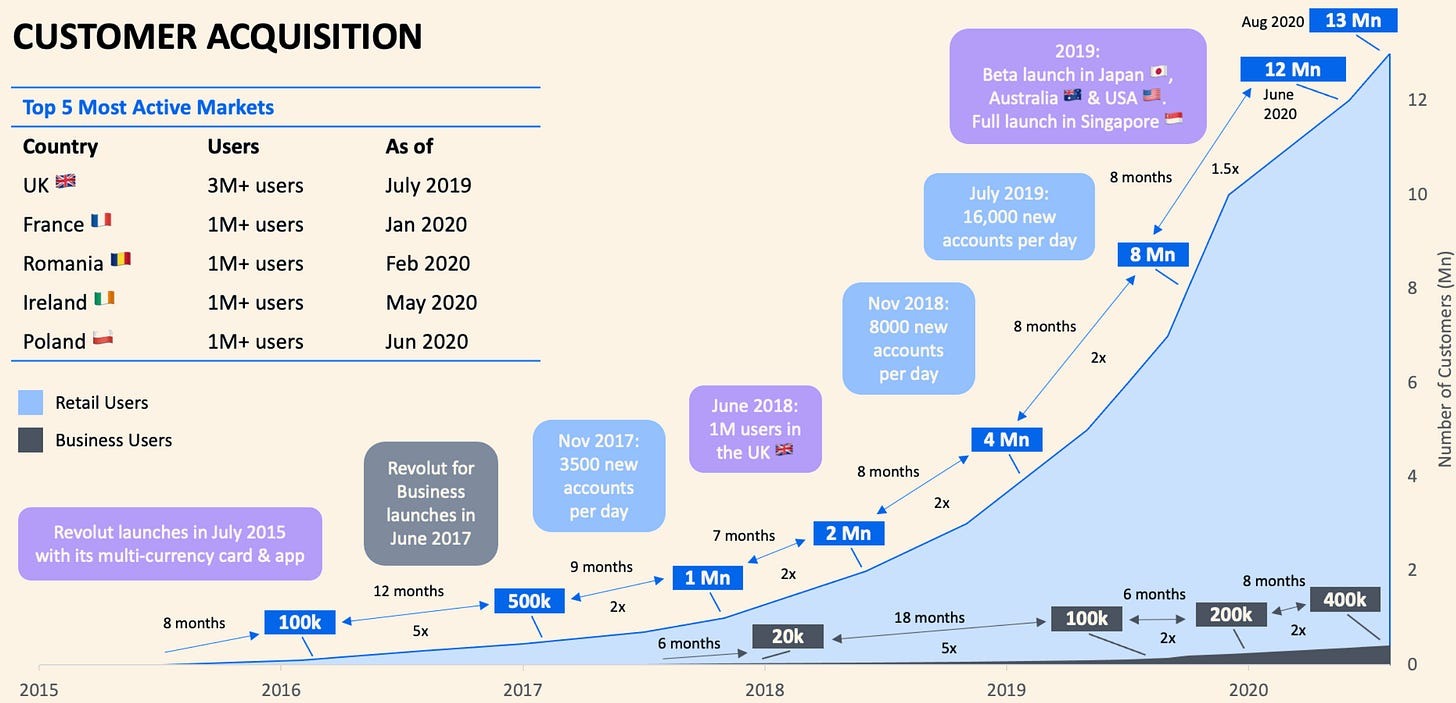

Revolut started in 2015 as a prepaid multi-currency debit card aimed at travelers and expats, offering real-time FX at interbank rates (solving a common pain of high exchange fees). Early growth was rapid: by 2016 it had ~300k users. From 2017 onward, Revolut aggressively layered new features – e.g. peer-to-peer payments, budget tools, and paid subscription tiers (Premium/Metal) – to boost engagement and create recurring revenue. Crucially, in late 2017 Revolut launched cryptocurrency trading for users (adding Bitcoin, Litecoin and Ether trading directly in-app), an early move among fintechs that began diversifying its revenue streams.

Revolut 2015-2020, Source: Whitesight

An important strategic milestone was obtaining a European banking licence in late 2018 (via Bank of Lithuania) – one of the first fintechs to do so. This allowed Revolut to hold client deposits and offer IBAN accounts in the EU, underwriting ambitions beyond pure e-money. With that license in hand, Revolut pushed expansion into new markets (Asia, US, Latin America) and added banking features. For example, it launched Revolut Business (2017) for corporate accounts, stock trading in partnership with DriveWealth (~2019), and digital wealth products (zerocommission ETFs in 2022-23 across the EEA). By constantly iterating – often via mobile app updates – Revolut kept organic momentum; indeed, by 2020-21 it was achieving the majority of growth via word-of-mouth.

Regulatory moves shaped its trajectory. Initially UK-based, Revolut’s Brexit pivot meant it operated under its Lithuanian licence for EU users. It secured a restricted UK banking licence in mid-2024 and only in March 2026 received full UK approval, allowing it to offer deposit accounts and loans in its home market. Each new license expanded trust: EU deposits became protected by Lithuanian schemes, and now ~13m UK users will be covered by the UK’s deposit insurance (FSCS).

Throughout its history Revolut leveraged product bundling as a competitive edge (the “multiengine platform”). Launching one new feature often reinforced others: e.g. adding travel insurance to premium plans increased card usage; integrating crypto and stock trading within the app boosted engagement. By 2025 the company touted 11 different product lines each generating >£100m (c.$135m) in annual revenue – a testament to its feature-led growth strategy.

Early on, focus on low-cost international payments and card usage gave Revolut a clear niche and fast growth. Adding fintech services (investing, insurance, roaming SIMs, etc.) turned it into a stickier “super-app” that could upsell existing users. Banking licenses in EU/UK converted fintech convenience into mainstream trust and balance-sheet capabilities. In short, each stage – from FX card to crypto wallet to licensed bank – served to lock customers deeper into the platform and open new revenue engines.

Current State of the Business

By end-2025, Revolut is a large, profitable fintech bank. Key metrics from 2025 include: ~68.3 m retail users (30% YoY growth) and 767k business clients (+33%). It earned $6.0 billion in revenue (+46%) and $2.3 billion PBT (+57%). Profit margins are strong (38% PBT margin, up from 35% prior year), reflecting scale economies. These figures represent five consecutive years of net profit – a contrast to many private fintechs – indicating that Revolut’s model is beginning to look like a scaled financial institution.

User engagement and adoption

Growth remains robust. Revolut added 16 m new retail customers in 2025. More importantly, engagement is deepening. Roughly 45% more customers each year choose Revolut as their primary bank, and usage per customer is rising: total transaction volume surged 65% to $1.7 trillion in 2025, and transactions per customer grew 24% YoY. The RevPoints loyalty scheme now has 17 m users (1 in 4 of the user base), and 42% more customers have paid subscriptions (Plus/Premium/Metal) than a year ago. These trends suggest Revolut is moving beyond a “sidecar” payment app to become a core finance hub for many users.

Geographic footprint

Growth is broad but still EU-centric. Europe (including UK) remains dominant – 1-in-5 Europeans use Revolut – but Asia-Pacific and the Americas showed momentum too. In 2025, business volume in Singapore, Australia, and the U.S. grew over 140% YoY (albeit off a smaller base). The group reports having banking or payments authorization in 30+ markets. Full UK banking status now extends deposit protection to ~13 m UK accounts, and the company is primed to expand services (current accounts, credit cards, personal lending) in its home market.

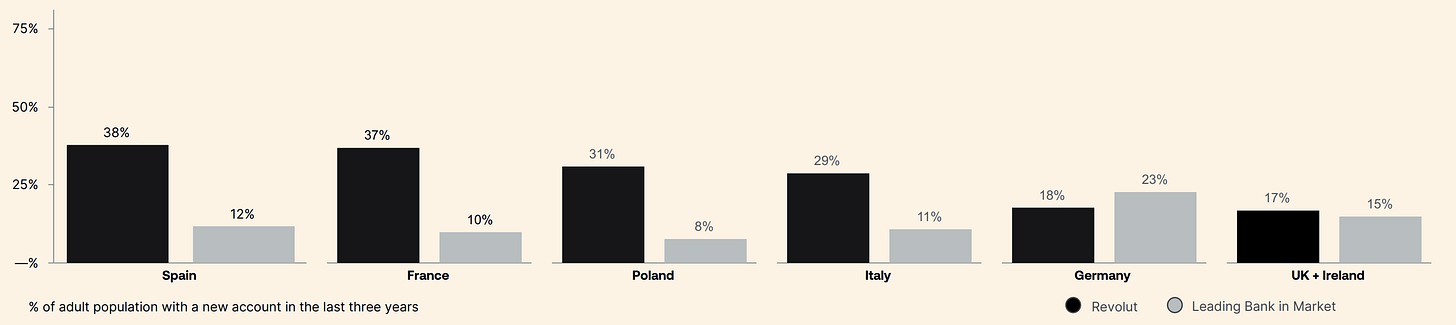

Nearly 1 out of every 3 new accounts is a Revolut account

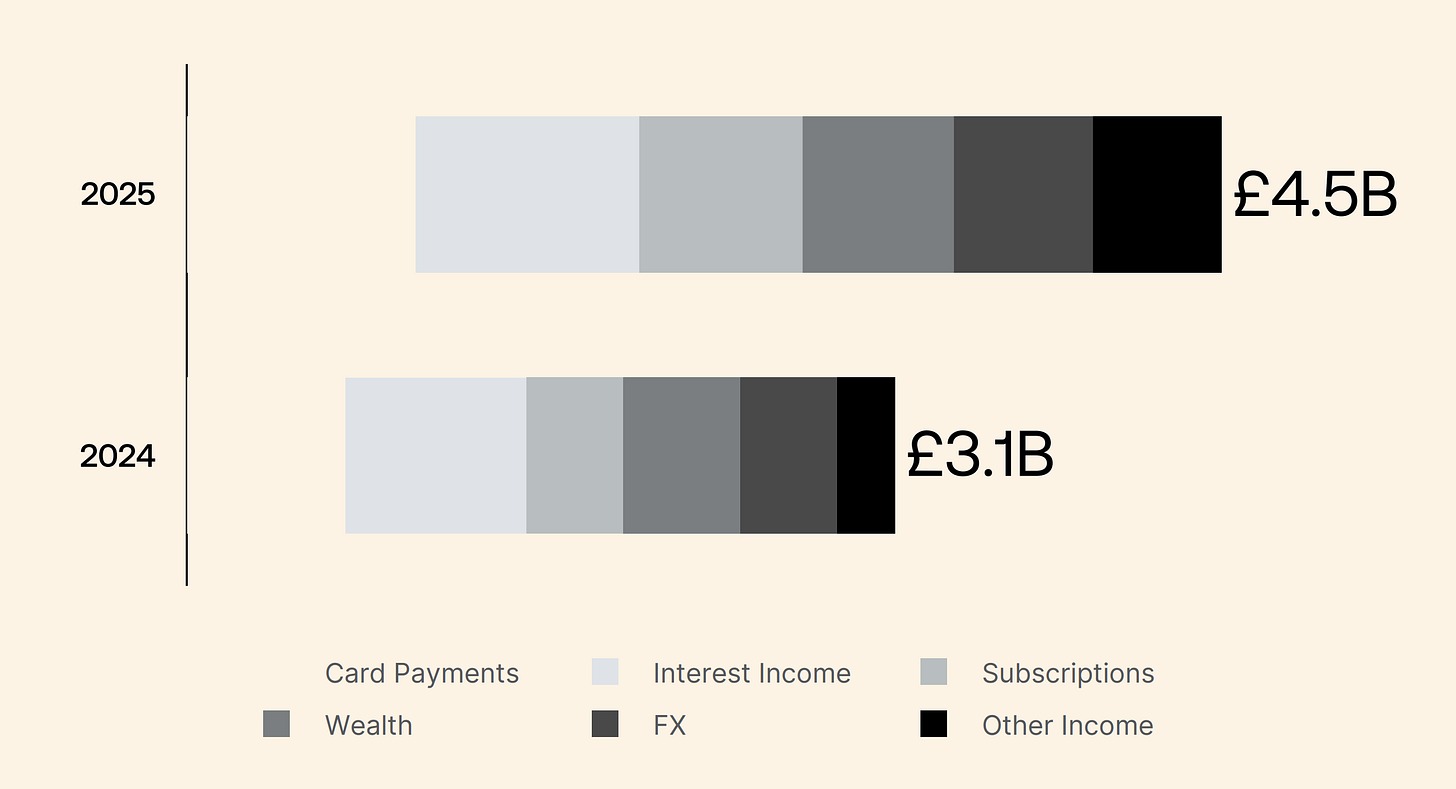

Revenue mix

The business is broadly diversified. Of 2025 revenue (~£4.5bn), roughly half came from transactional fees (card fees, FX) and subscriptions, and the rest from financial services (investment, interest). For example, subscriptions generated ~£708m, card fees ~£1.0bn, wealth/FX ~£1.3bn combined. The business segment (corporate accounts) contributes ~16% of income, while lending/interest (from personal loans and credit) is growing fast: lending balances reached $2.9 bn (+120% YoY) and interest income was $1.3 bn. In other words, Revolut is still fee-heavy today, but gradually shifting toward interest earnings as a complement.

Revenue Mix

Operating leverage

Indicative of scale, cost efficiency is improving. The 38% profit margin in 2025 suggests that new revenue largely outstripped fixed-cost growth. Management emphasizes disciplined cost management (e.g. 90% of its assets held in cash/treasury investments) and technology-driven operations. There is evidence of rising efficiency: for instance, customer support times were cut 40% in 2025 even as the user base swelled. However, continuing expansion (new markets, licenses, and a £10 billion planned capex over five years) means absolute costs will still rise.

Maturity versus growth

Revolut today straddles growth and scale. It no longer burns cash; profits and strong metrics show it is a scaled institution. Yet it is still growing rapidly (over 20% user growth, much higher in newer markets) and investing heavily in new products and geographies. In our view, it remains a growth platform, but with the beginnings of banking stability. The key question is how well it can leverage its scale – e.g. converting customers to primary users and deploying balance-sheet products (loans, mortgages) – to sustain both growth and margins.

Business Model and Economic Quality

Revolut’s business model relies on a combination of fee/commission income, subscription fees, and interest income – a mix that has become more balanced over time. In 2025, roughly 80% of revenue was non-interest (card fees, FX spreads, trading commissions, subscriptions, wealth fees) and ~20% was net interest (chiefly from consumer lending).

Key revenue streams:

- Transaction and subscription fees: Card payment fees (interchange/share of merchant fee) and foreign-exchange fees remain sizeable (around $1.0 bn and $0.8 bn in 2025 respectively). Paid subscription plans (Plus/Premium/Metal) are another stable source (708 m USD in 2025, +67% YoY). These revenues grow roughly with customer count and spending levels; they are partly cyclical (tied to consumer spending and travel) but also recurring.

- Wealth management fees: Investment services (stock trading, ETFs, CFD spreads) brought in $876 m (663 m GBP) in 2025, a 31% increase. This is still a modest fraction of revenue, but it demonstrates an important diversification – Revolut gains commission from stock/ETF trading and crypto transaction fees. Zero-commission ETFs (launched 2025) may attract more users, but currently wealth products constitute under 20% of revenue.

- Interest income (lending): Revolut’s lending business is nascent but rapidly growing. It had $2.9 bn in outstanding loans (mostly unsecured personal) by end-2025, driving interest income of $1.3 bn (GBP 974 m) which grew 23% YoY. This marks the first time Revolut is earning nearly a billion USD a year in net interest – roughly 20% of its total revenue. As it transitions toward a bank (with mortgages in Lithuania and upcoming UK credit products), interest could eventually become a top-2 revenue stream. Importantly, interest income is relatively stable and ties Revolut’s profits to net interest margins rather than volatile fees.

- Business/SME segment: Corporate accounts, payments, and fintech services form ~16% of income. This business stream is lower-risk (large companies, B2B volumes) and sticky (account relationships). It also boosts scale – in 2025 Revolut Business facilitated $365 bn in transactions. Continued growth in this segment (e.g. adding 30k companies/month in 2025) would improve the customer base diversity and fee stability.

Economic quality

The model appears robustly profitable at scale, but not immune to cycles. The organic growth in high-margin revenues (cards, FX) and rapid uptake of lending has so far delivered double-digit net margins. However, some caution is warranted: fee revenues correlate with consumer spending and travel (cyclical), and crypto trading (when it boomed) contributed significantly to profits in 2024. With crypto markets now calmer, past performance was partly cyclical. On the other hand, the growing loan book provides more steady yield, and recurring subscription fees underpin a “flywheel” effect as users add more services. The breadth of 11+ revenue streams suggests resilience: a downturn in one line (e.g. travel cuts) can be partly offset by another (e.g. card use or lending). In summary, Revolut’s economics have matured from a narrow fintech punch to a diversified bank-like mix – still growth-oriented, but less lumpy than early years.

Product, Platform, and Competitive Positioning

Revolut’s competitive edge lies in its breadth of features and speed of innovation. It offers a wide product stack – banking accounts, multi-currency wallets, instant FX transfers, global debit cards, loans, crypto and stock trading, insurance, mobile eSIM service, etc. – mostly within one app. Local market adaptation adds strength: for example, Revolut now issues local IBANs in multiple EU countries, offers mortgages (currently Lithuania), and even has a telecom MVNO (Revolut Mobile in UK/Poland). This localization helps fit local needs better than a one-size app.

User experience and technology

The UX/UI is often cited (by surveys and media) as a key differentiator – simple onboarding, budgeting tools, instant notifications and peer payments have high user appeal. Revolut’s technical platform also uses AI and automation: for instance, it has deployed advanced AI across its systems to improve fraud detection, enabling up to 10× as many fraud checks daily. Internally, this reduces manual intervention and helps maintain security at scale. Analytics and APIs (e.g. Revolut X API for pro crypto traders) offer further value-adds.

Platform model

Revolut calls itself a “multiengine” platform, and its strength partly comes from cross-selling within that platform. For example, RevPoints rewards integrate card spending across travel and payments, encouraging continued use. The 17 m users of RevPoints likely translate to more active engagement across products. Similarly, allowing crypto and stock trading in the same interface as bank accounts lowers customer acquisition costs relative to standalone brokers. A large customer base (68m) provides a distribution advantage: Revolut reports that 63% of new users join via referrals – a virtuous growth loop.

Cost structure

As a digital-first firm, Revolut has much lower fixed overhead than legacy banks (no branch network) and can iterate features more quickly. This helps sustain the high PBT margin (38%) by keeping costs in check. However, compliance and cybersecurity costs are rising, and the business invests heavily in tech and hiring (7.9k staff by mid-2025). Competitive pricing (e.g. 0% maker fees on Revolut X) may pressure unit economics in crypto and trading if volumes slow.

Competition

Compared to incumbents (Barclays, Santander, etc.), Revolut’s advantages are agility and product range. It competes directly in core banking: e.g. its launch of UK current accounts (Mar 2026) positions it as a challenger bank to HSBC/Barclays. Against other fintechs (Monzo, N26, Wise), its edge is global scale and multiple verticals. N26 and Monzo are strong in single markets, whereas Revolut’s 70m base spans dozens of countries. Compared to pure crypto exchanges (Coinbase, Binance), Revolut is regulated and integrated with broader finances – appealing to users who want one app for all money needs.

In sum, Revolut’s competitive positioning is built on distribution and product breadth. It may not have a proprietary tech moat beyond its large user community, but the combination of seamless UX, constant innovation, and global regulatory footprint makes it uniquely hard for any one competitor to match. (We note that claims of being a “super-app” are marketing language, but certainly Revolut’s product mix is broader than a vanilla neo-bank.)

Risks, Constraints, and Open Questions

Rapid growth has drawn close scrutiny. In April 2025, the Bank of Lithuania (supervising Revolut’s EU bank arm) fined Revolut Bank €3.5 million for anti-money-laundering shortcomings. The fine highlighted “violations and shortcomings in the monitoring of business relationships”. Similarly, UK regulators (FCA/PRA) cited concerns about Revolut’s cross-border risk controls, which delayed its full UK bank rollout. These incidents underscore that weak compliance or control lapses could lead to further fines or restrictions. Open question: Will Revolut’s governance and AML systems scale in line with its growth?

Licensing and operational execution

Each new banking license is a multi-year effort. While the UK license now won, moving customers to the new bank will take months. Revolut is also awaiting its U.S. charter decision and expanding in LatAm (Mexico, Peru) and Europe (France license application). Delays or unexpected conditions (as seen in 2024) could slow growth. Operationally, integrating new regulations (e.g. branch presence, local capital requirements) could hamper the speed advantage.

Credit and funding risk

As it builds lending, Revolut faces credit risk unknowns. The $2.2 bn unsecured loan book is growing quickly, but future defaults (especially if an economic downturn) could strain earnings. So far Revolut’s conservative balance sheet (90% cash/Treasury) suggests prudence, but risk remains as it expands mortgages and consumer loans. Funding is also a factor: most Revolut users still keep small balances (Analysts note typical deposits are lower than traditional banks). If Revolut wants to fund loans internally, it needs either more deposits (raising customer stickiness) or external funding sources.

Margin sustainability

Currently, high fee volumes and fast-growing interest are lifting margins. But these could compress. Transaction volumes are partly driven by consumer spending patterns; any slowdown (e.g. reduced travel or economic stress) could cut fee income. Competition from banks or other fintechs on fees is also intensifying (e.g. banks introducing their own multi-currency cards). Further, some of Revolut’s fee income – notably crypto trading – is inherently cyclical (revenues rose sharply in bull markets). A sustained bear market in crypto or stocks would directly dent trading fee revenue. Management’s plan to rely more on lending (a more stable stream) is intended to mitigate this, but that is unproven at Revolut’s scale.

Geographic/market complexity

Expanding into diverse markets (Mexico, APAC, etc.) entails local competition and regulatory nuance. The UK and EU are relatively homogeneous tech-savvy markets; elsewhere consumer behavior differs. Revolut’s one-size-app approach may face cultural or banking-system challenges (e.g. insurance regulation in some countries, digital ID requirements). Balancing product standardization with local adaptation is a constraint.

Operational/compliance burden

Managing 70m users across ~100 jurisdictions is complex. Customer service scalability is a recurring issue; Revolut has improved support times (–40% in 2025) but any future service failures (e.g. prolonged outages, fraud events, or the past episodes of unexplained account locks) could damage trust. Maintaining robust tech and security is vital. Also, involvement in crypto and novel products invites new compliance regimes (MiCA in EU, FCA rules in UK, SEC rules in US). Regulatory changes (like UK stablecoin regulation or enhanced consumer protections) could force product reengineering.

Product complexity vs focus

Revolut’s breadth is a strength, but it risks diluting focus. Managing so many lines (banking, wealth, crypto, mobile, loyalty, etc.) can lead to complexity and divert resources. If new offerings don’t achieve scale, they could distract from core banking. The company appears aware of this risk – it speaks of incubating “new bets” within a diversified platform – but execution discipline will be key.

Digital Assets Strategy and Outlook

Crypto was introduced as an on-ramp in 2017. Revolut began offering cryptocurrency trading in late 2017, allowing users to buy/sell Bitcoin, Ethereum, Litecoin and other tokens within the app. At the time, this was positioned as a convenience (including an auto-conversion for purchases) with low flat fees. By 2021, Revolut had added crypto to 15+ markets and grown that user base substantially (reports indicated millions of users in crypto). In 2022, UK regulator FCA formally authorized Revolut’s crypto service under AML rules, and Revolut expanded to allow staking of proof-of-stake coins in UK/EEA (e.g. Ethereum 2.0 staking).

Compared to pure crypto exchanges, Revolut’s offering was simpler (no private keys held by user, just an interface to buy/sell at set prices) and natively integrated with its banking app. Historically, crypto trading fees have been a material but volatile profit source – Reuters notes a “crypto boom” in 2024 significantly boosted profits. However, fluctuating regulations and market cycles meant Revolut maintained a pragmatic stance: e.g. it de-listed certain crypto products in the US amid SEC scrutiny in 2023.

Current Positioning and Metrics

Revolut now runs crypto trading through two channels: the main Revolut app (for average users) and Revolut X, a separate advanced trading platform for power users. Revolut X offers a full-featured crypto exchange interface – 0% maker fees, deep liquidity, TradingView charts and API access – under the Revolut brand (billboard: “the crypto exchange for pros”). Assets on Revolut X are custodially held 1:1 (no lending out) and mostly in cold storage. Meanwhile, the in-app crypto wallet serves casual traders with instant on/off ramps.

EU customers trade via Revolut Digital Assets Europe Ltd (a CySEC-licensed CASP under MiCA). UK users access crypto via Revolut Ltd (FCA-registered under AML regs). Asset breadth covers ~250+ tokens (spot trading, and e.g. limited staking on ETH). Stablecoins: Revolut does not yet offer a Revolut-branded stablecoin, but in Feb 2026 it entered the UK FCA sandbox to trial a GBP-backed crypto token, indicating future stablecoin ambitions. In terms of segmentation, crypto is a feature of its Wealth & Invest suite – positioned alongside stocks and ETFs – not an isolated profit center. Notably, Revolut does not provide unhosted self-custody wallets (so it does not compete on hardware/DeFi); it remains in the “regulated crypto brokerage” camp.

Publicly available data on Revolut’s crypto usage is limited. Management has not disclosed the number of crypto traders or crypto revenue share. However, the evidence suggests crypto is a meaningful engagement driver but a small slice of revenues: all major revenue lines (subscriptions, card fees, FX fees, lending interest) each exceed $600m, whereas “cryptocurrency” is not broken out as a standalone figure in disclosures.

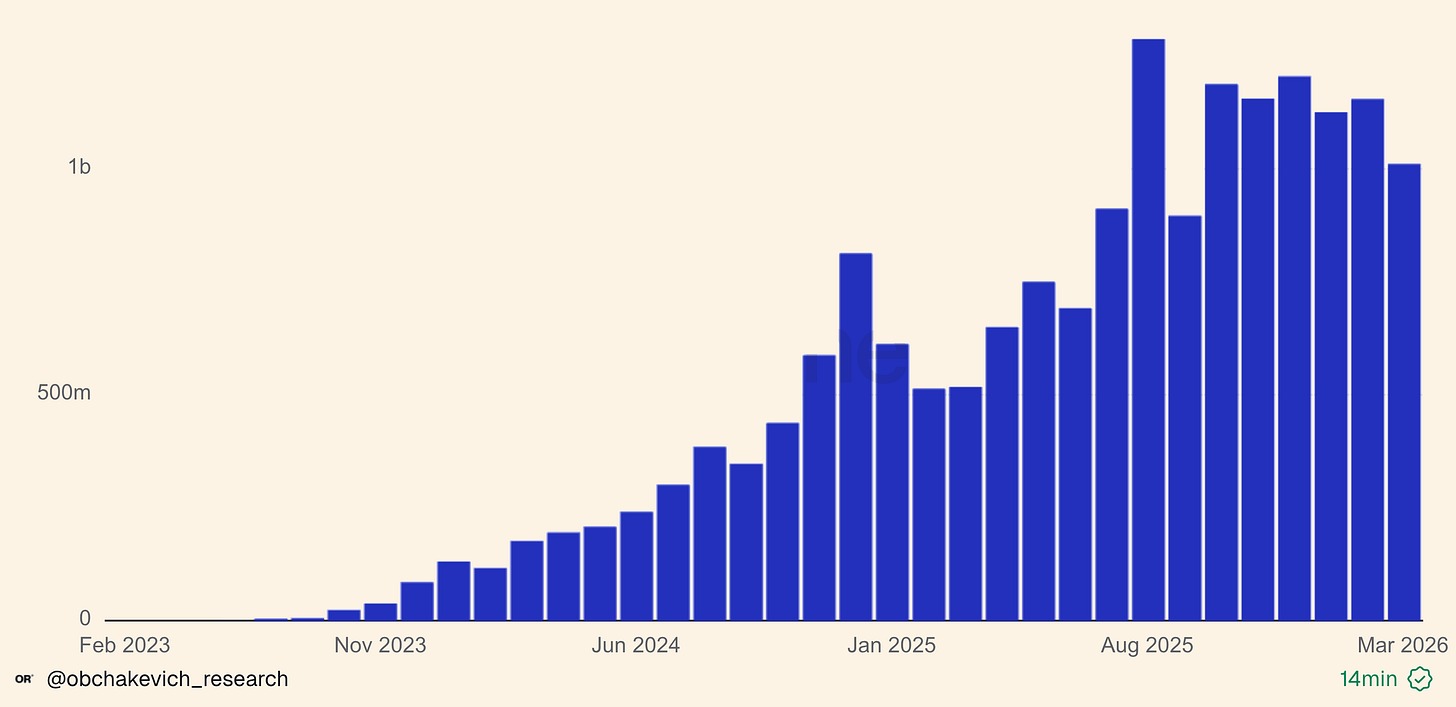

Revolut stablecoins monthly volume

Anecdotal metrics hint at moderate usage: for example, 17m users are in the RevPoints program (which can be earned via crypto-related spending), and Revolut X’s customer count (advertised) is a subset of the total. Crypto trading volumes presumably track market cycles: 2021-22 bull runs saw surges in usage, whereas 2023-25 saw relatively lower crypto volatility. The fact that the 2025 Annual Report highlights 45% YOY growth in primary bank adoption and nearly all product lines, but does not highlight crypto growth, implies that crypto was likely not a standout growth area last year.

Revolut appears to be positioning its crypto capabilities as a regulated distribution layer rather than a speculative sideline. By securing a CySEC CASP license under MiCA, it is one of the first major fintechs to meet EU crypto regulation, enabling it to offer crypto services to all EEA retail investors. This could make Revolut a one-stop digital-asset aggregator – effectively bridging traditional finance customers into the regulated crypto sphere. It is reasonable to infer that crypto enhances Revolut’s stickiness (users engaging in multiple financial activities in one app) and serves as a lead-generation/retention tool. However, crypto’s share of total revenues is likely modest. Rather than a primary profit pillar, it acts as a value-added feature that keeps Revolut’s product suite competitive with pure-play fintech wallets.

Crypto does strengthen Revolut’s “super-app” positioning by giving users quick access to digital assets without leaving the platform. It potentially draws in younger or more tech-oriented segments that might otherwise use exchanges. Nevertheless, Revolut’s core narrative remains banking and payments. Unlike an exchange, Revolut does not rely on crypto market-making or lending (it claims assets are not lent out). This limits revenue but reduces risk. The company’s move into a stablecoin trial and talk of own token (as reported by media) suggest it is experimenting with new rails, but these ventures carry risks (regulatory and reputational) and are currently small-scale.

Forward View

Looking ahead, Revolut’s crypto roadmap seems aligned with regulation and incremental feature expansion. A plausible path: finalize testing of a GBP stablecoin (or other token) in 2026, and consider issuing it if regulatory approval is obtained. Expand Revolut X globally (subject to local rules) to capture more trading volume, and possibly roll out crypto derivatives or DeFi gateways (if regulations allow). Continue layering crypto into loyalty programs or as collateral (e.g. allowing crypto-collateral loans someday). Constraints include: evolving MiCA requirements (consumer protection, stablecoin reserves), likely stricter UK rules on stablecoins, and intense competition from purpose-built exchanges. For crypto to become material to Revolut’s business (versus just complementary), there would need to be a meaningful structural shift – for example, major adoption of a Revolut-issued stablecoin, or integration of digital asset custody into everyday banking services. This would require both heavy regulatory approval and user demand. As of now, crypto seems poised to grow steadily with the market, but its economic contribution will likely remain modest relative to Revolut’s broader banking and payments operations.

Key Metrics to Watch:

- Retail Primary-Account Ratio: share of users using Revolut as main bank (45% YoY growth in 2025) – a proxy for stickiness.

- Customer Balances vs Loans: total deposits ($67.5 bn in 2025, +66%) and loan book ($2.9 bn, +120%) – indicating funding base and shift to interest income.

- Revenue Growth & Mix: total revenue ($6.0 bn, +46%) and segment contributions (e.g. business = 16%; fees vs interest mix).

- Transaction Volume: total volumes ($1.7 trn in 2025, +65%) and business vs retail breakdown (business $365 bn).

- Profitability Margins: PBT margin (38% in 2025) and return on equity – to gauge operating leverage.

- Crypto Engagement: share of customers who trade crypto, and crypto revenue (unpublished) – monitor product announcements (e.g. new tokens, staking) for signals of investment.

- Regulatory Milestones: licensing updates (full UK deployment, US charter progress, MiCA compliance) and compliance outcomes (e.g. AML audit results) – these govern growth scope.

Reported Fact vs Analytical Inference

Throughout this analysis we distinguish reported figures from inferences. For example, “68.3 m customers by end-2025” and “£1.7 bn profit-before-tax” are facts from official sources. By contrast, statements about how crypto fits into Revolut’s strategy (“crypto is primarily a retention and engagement feature”) are analytical interpretations based on available clues (e.g. licensing, product integration) and not explicitly stated by management. Where evidence is lacking (e.g. unknown crypto revenue share), we have signaled uncertainty. Importantly, management’s own bullish language (e.g. targeting 100m users by 2027) is noted as ambition – though we balance it with the practical pacing of results.

Conclusion

Revolut today is a global fintech powerhouse: much more than the travel-card startup of 2015, it is now a scaling bank platform with diversified products. It boasts record profitability and vast scale, driven by an “all-in-one” app strategy that combines payments, banking, wealth, and crypto. The business has reached a pivotal point: it is transitioning from a pure growth fintech into a mainstream financial institution (evidenced by full UK bank status and breakeven on 70m users). Its strengths lie in product breadth, customer loyalty, and a technology-first cost base. However, its rapid expansion invites real risks – from regulatory compliance (AML, capital rules) to macro-sensitive revenue cycles.

The digital-assets strategy, while strategically visible, should be kept in perspective. Crypto features reinforce Revolut’s platform and attract savvy users, but they constitute only one part of a larger mosaic. Revolut’s focus remains on traditional banking services: getting more deposit accounts, extending consumer credit, and consolidating in every market. In that light, crypto and stablecoins are interesting “bets” on future finance, but not game-changers for Revolut’s core. In sum, Revolut is becoming a true global challenger bank, and its crypto initiatives are a strategic complement – enhancing engagement and future optionality – rather than the centerpiece of its evolution.

Revolut - Statements

Consolidated Statement of Comprehensive Income

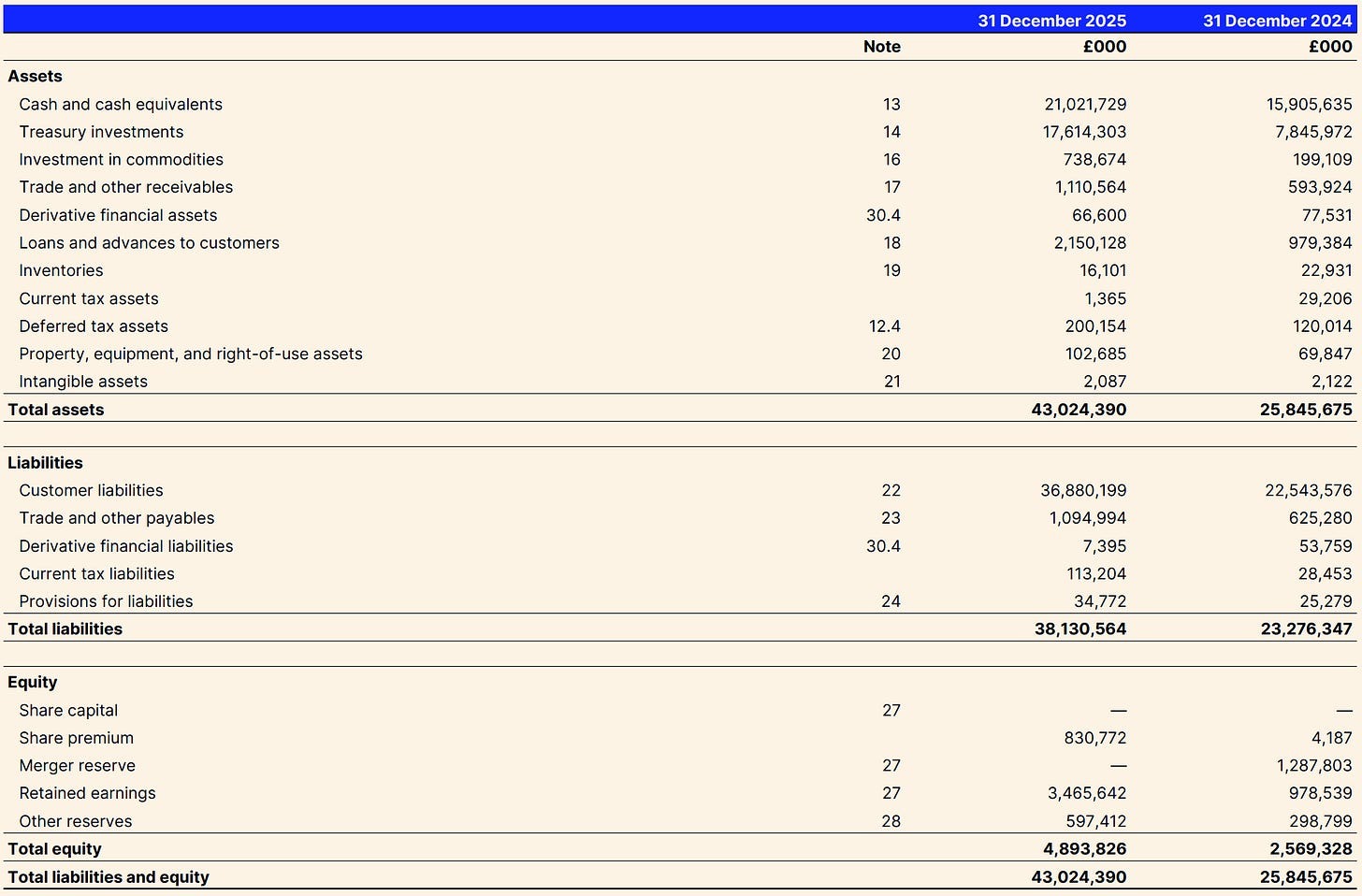

Consolidated Statement of Financial Position

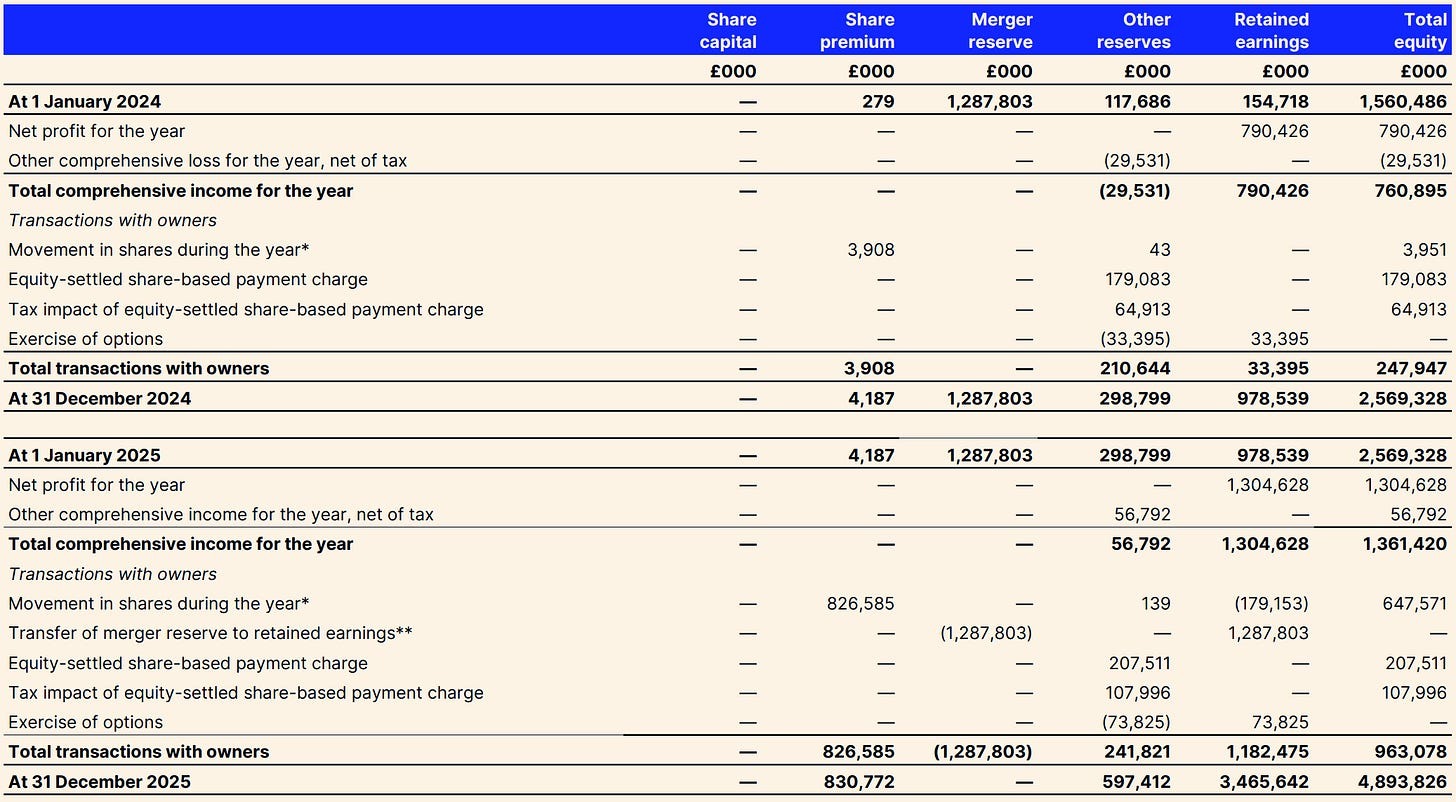

Consolidated Statement of Changes in Equity

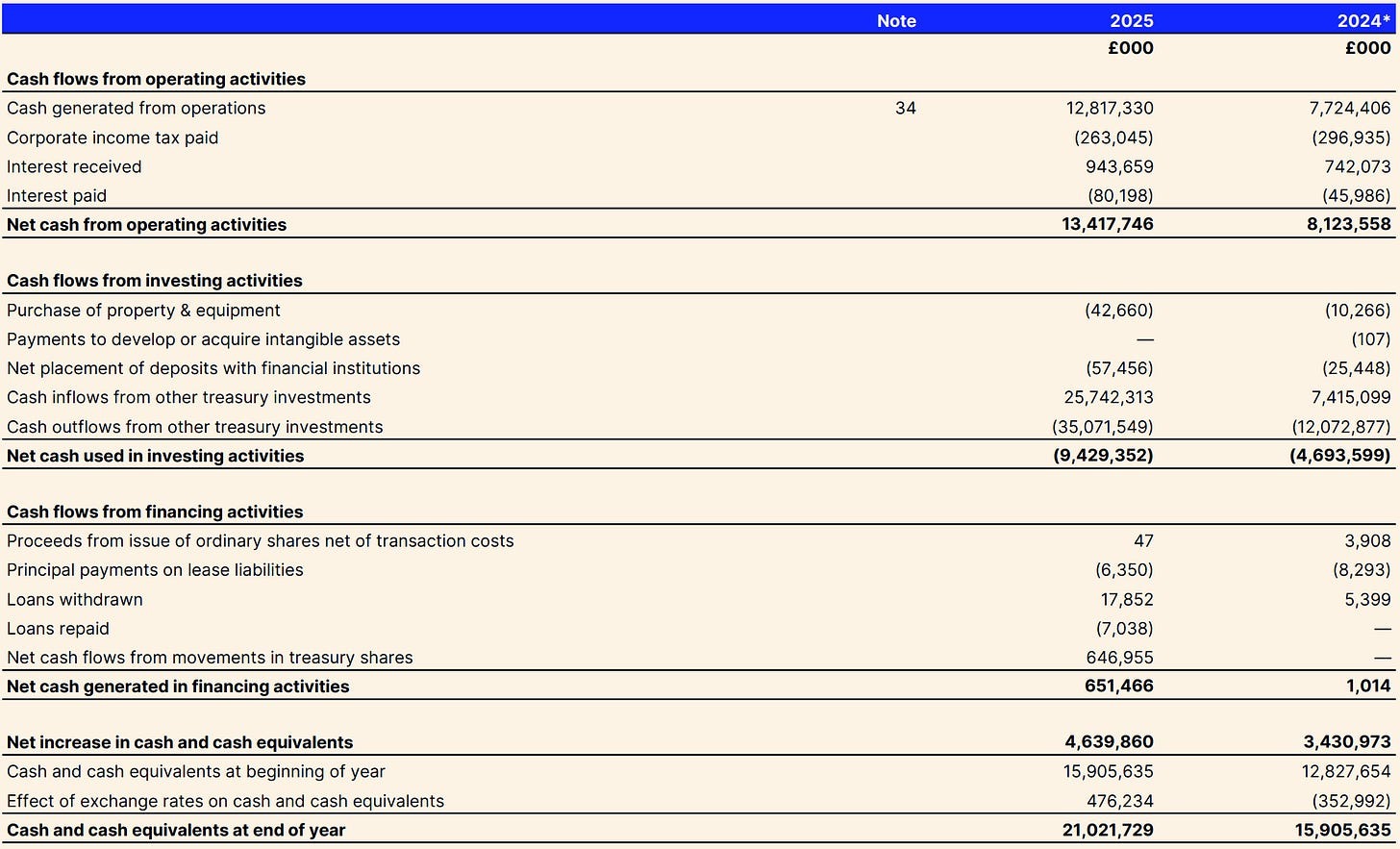

Consolidated Statement of Cash Flows

Sources:

Cover Artwork

Harbour scene

Salvator Rosa, c. 1641

Risk Disclaimer:

insights4.vc and its newsletter provide research and information for educational purposes only and should not be taken as any form of professional advice. We do not advocate for any investment actions, including buying, selling, or holding digital assets.

The content reflects only the writer’s views and not financial advice. Please conduct your own due diligence before engaging with digital assets or related technologies, as they carry high risks and values can fluctuate significantly.

Note: This research paper is not sponsored by any of the mentioned companies.