The most important fact about “RWAs” in 2026 is that the market is not one market.

It is two structurally different stacks that share vocabulary but not outcomes: (a) distributed assets whose tokens can leave an issuer platform and move peer-to-peer (often with whitelist controls)

(b) represented assets that sit on a ledger but cannot be moved outside the issuer platform or transferred peer-to-peer.

The latter is primarily about operational efficiency and internal market infrastructure rather than open, composable capital markets. This distinction is now explicit in industry-standard data, with definitions based on token mobility and transferability rather than marketing categories.

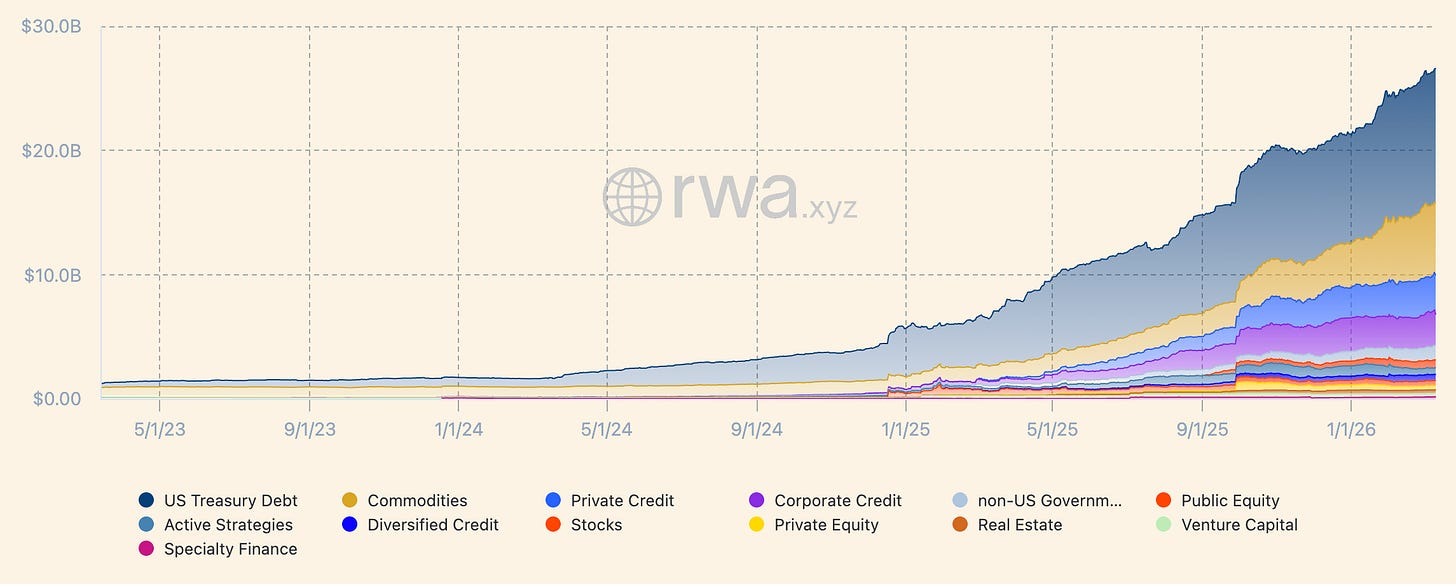

Using RWA.xyz as the reference dataset, distributed RWA value across public blockchains is $26.66B, while represented RWA value is $342.60B. Reliable interpretation: the “big number” is dominated by represented assets and walled gardens, which matter for back-office transformation but do not constitute open capital markets.

Total RWA Value (Source: RWA.xyz)

RWA market by category (Source: RWA.xyz)

To answer “what is real” versus “what is cosmetic” for sophisticated readers, a three-tier taxonomy is more decision-useful than a single AUM headline:

Assets merely represented onchain (Tier 1). Tokens function as records on a shared ledger, but are not transferable externally (or not transferable in practice). These are “represented assets” in the RWA.xyz framework.

Assets actively used onchain (Tier 2). Tokens are transferable and show sustained onchain activity: recurring transfers, multiple holders, and credible usage as collateral or liquidity in trading, lending, or structured products. This is a subset of distributed assets. The relevant question is not whether an asset is tokenized, but whether it performs as programmable collateral with reliable settlement.

Assets truly integrated into open capital markets (Tier 3). Tokens are (i) transferable, (ii) have credible secondary liquidity beyond a single venue, and (iii) are legally and operationally interoperable with broader markets (corporate actions, rights, enforceability, robust disclosures, and regulatory clarity). Today this set is small and concentrated, and in many cases “open” still means “open to a whitelisted set” rather than permissionless retail access.

Macro context matters because scale comparisons reveal how early this still is. Global fixed income outstanding and global equity market capitalisation are both measured in the hundreds of trillions. SIFMA reports global fixed income markets outstanding at $145.1T (2024) and global equity market capitalisation at $126.7T (2024). In the U.S. alone, money market fund assets were $7.82T as of the week ending 4 March 2026 (a relevant benchmark because tokenized Treasury funds compete with MMFs operationally as “cash collateral”). Investment Company Institute Tokenized RWAs are still measured in tens of billions, but the microstructure direction of travel is now observable.

Tokenized Treasuries and cash-equivalent funds

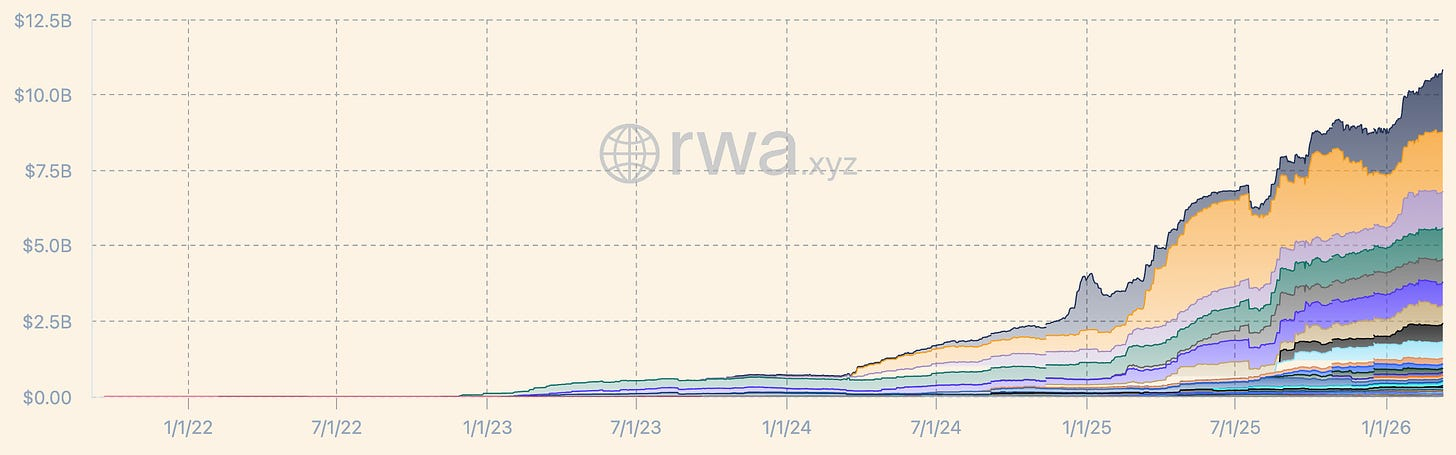

Tokenized U.S. Treasuries are the clearest example of a Tier 2 market that is starting to behave like institutional collateral. Total value is about $10.00B with a displayed 7-day APY of 3.15% on the RWA.xyz Treasury dashboard (as of March 2026). This segment is large enough to support multiple incumbent asset managers and multiple tokenisation rails, and it is now directly referenced in exchange collateral programmes and onchain liquidity initiatives.

Total Value - Tokenized U.S. Treasuries (Source: RWA.xyz)

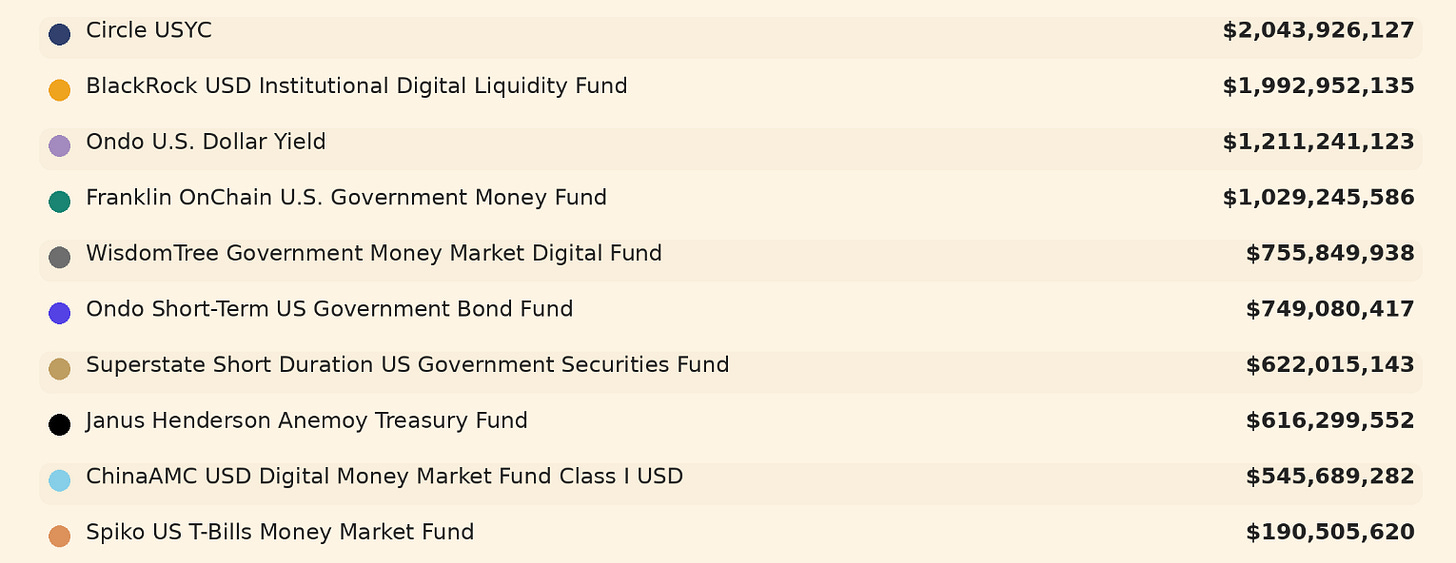

Tokenized U.S. Treasuries - Top 10 (Source: RWA.xyz)

Market structure: concentration is high, but not yet monopolistic

Platform market share in tokenized Treasuries is led by a small set:

Ondo (~21.91%), Securitize (~19.86%), and Circle (~16.76%), followed by Franklin Templeton, WisdomTree, and Superstate.

The top products illustrate why “tokenized Treasuries” is currently more a tokenized fund share market than a direct onchain Treasury security market. The largest products and their structures (selected highlights from the Treasury product table) include:

- The BlackRock USD Institutional Digital Liquidity Fund (BUIDL) at roughly $1.88B, distributed across multiple chains, with eligibility limited to U.S. Qualified Purchasers, a minimum investment of $5,000,000, and a disclosed management fee range of 0.20–0.50%.

- USYC at roughly $1.68B, offered to Non-U.S. Investors (Reg S) with a minimum of 100,000 USDC and a very small onchain holder count relative to AUM.

- USDY at roughly $1.40B, offered to Non-U.S. Investors with extremely low minimums in the token wrapper, and a materially larger holder count.

- BENJI / FOBXX at roughly $892.6M, available to U.S. retail and institutional investors, with a low minimum and an SEC-registered mutual fund wrapper (Form N‑1A referenced in-product).

The top four products (BUIDL, USYC, USDY, BENJI) are about $5.85B, or roughly 58.5% of the $10B Treasury category. This is meaningful concentration, but the competitive field is not a single-issuer winner-take-all, which is important for long-run institutional confidence and regulatory risk dispersion.

What is real and what is overstated in tokenized Treasuries

What is real is the operational value proposition, not the “onchain Treasury” narrative. Tokenized Treasury funds are used as:

- always-on collateral for crypto market participants who want yield while remaining inside a digital-asset workflow; and

- a bridge product for traditional institutions experimenting with onchain settlement and collateral mobility without taking directional crypto exposure.

This is no longer hypothetical. Binance has integrated BUIDL as an off-exchange collateral asset for institutional users, explicitly framing the benefit as earning yield on collateral while trading.

What is overstated is the implication that these products already function like open-market Treasuries. Most of the biggest funds remain gated by eligibility (qualified purchaser, accredited, non-U.S.) and by transfer whitelists, meaning they do not yet behave like globally accessible, permissionless Treasury bills.

Where value accrues in tokenized Treasuries

Value accrues chiefly to: (i) the fund manager via management fees (still small in absolute dollars compared with traditional fund complexes because AUM is small), and (ii) the tokenisation and distribution rail (transfer agent, KYC/AML, whitelisting, multi-chain issuance), plus (iii) exchanges and liquidity venues that monetise collateral utility.

Illustratively, management fees disclosed in the tokenized Treasury product table imply revenue that is currently modest at the system level. For example, BUIDL’s disclosed fee range on about $1.88B implies low single-digit millions of annual fee revenue, while BENJI’s 0.15% fee on about $0.89B implies low single-digit millions as well. The strategic value is therefore less near-term fee dollars and more distribution and collateral entrenchment.

Institutional adoption in practice: hybrid DeFi

The strongest signal of institutional adoption so far is not that institutions are trading Treasuries on AMMs. It is the emergence of permissioned lanes that preserve compliance while giving onchain settlement and programmability.

BUIDL’s integration with Uniswap Labs via UniswapX, for example, is framed as enabling onchain trading and liquidity options, but it remains mediated via whitelisting and issuer infrastructure. Similarly, Aave describes an institutional RWA market (Aave Horizon) enabling qualified institutions to borrow stablecoins against tokenized securities.

In short, tokenized Treasuries are scaling because they solve a real collateral and settlement problem in crypto market structure, but their “openness” is still constrained by securities law and transfer controls.

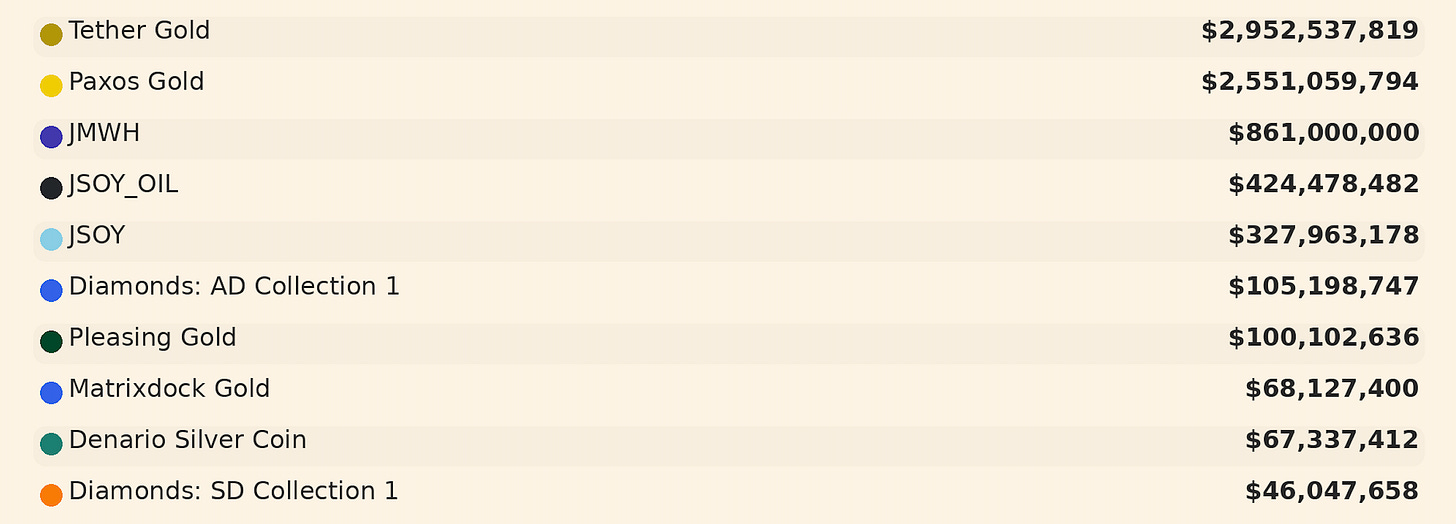

Tokenized gold and commodities

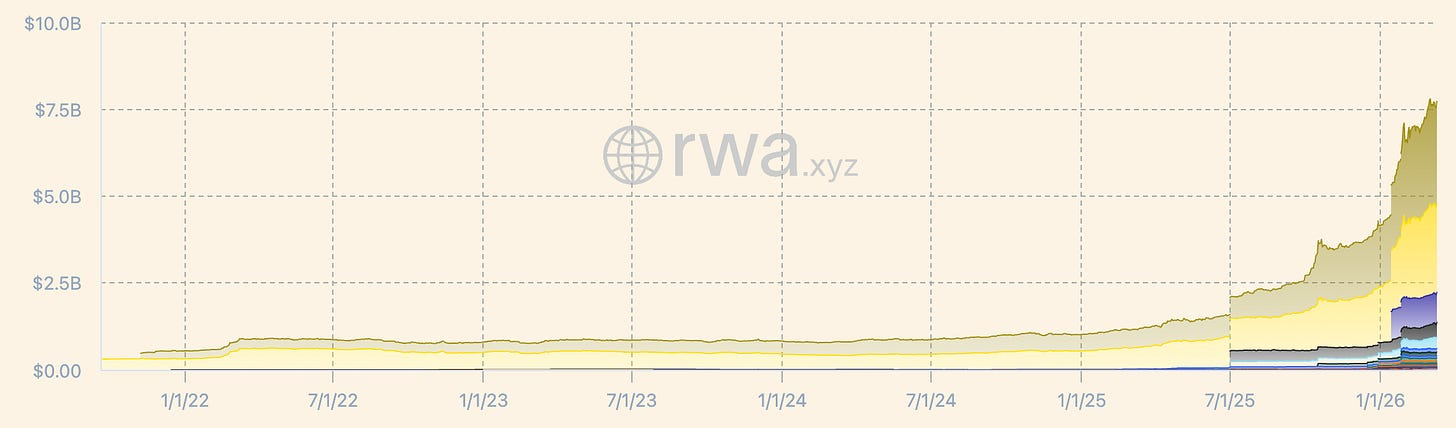

Tokenized commodities are now a second pillar of distributed RWAs, with a market cap around $7.59B and extreme issuer concentration. The market is effectively dominated by tokenized gold.

From the RWA.xyz commodity league table, the top platforms are Tether Holdings at ~2.9B(40.892.5B (35.37%), and Justoken at ~$1.6B (22.51%). The top two tokens, XAUT and PAXG, are roughly 72% of commodity token market cap by value on the dashboard.

Total Value - Tokenized commodities (Source: RWA.xyz)

Tokenized commodities - Top 10 (Source: RWA.xyz)

What is real in tokenized gold

Tokenized gold is “real” in a market-structure sense because it delivers a unique combination: gold exposure with crypto-native transferability. It is closer to Tier 3 than most tokenized securities categories because tokens can move peer-to-peer and trade broadly on crypto venues, even if redemption is still ultimately mediated through issuer processes.

On reserves transparency, Paxos Trust Company maintains a public portal for monthly reserve reports for PAXG. Tether publishes a general transparency portal for its tokens and has publicly leaned into gold as a strategic reserve asset supporting its ecosystem.

What is overstated and where risks are underpriced

The biggest underpriced risks in tokenized gold are not price risk but issuer and legal risk:

- Issuer concentration and correlated governance risk. The commodity token market is highly concentrated by platform share.

- Reserve opacity versus market impact. Reuters reports Paolo Ardoino stating that Tether holds about 130 metric tons of physical gold and plans to allocate 10–15% of its investment portfolio to gold, with ongoing buying. This makes tokenized gold increasingly linked to the balance sheet strategy of one dominant issuer rather than a neutral market structure.

- Jurisdictional and custody concentration. Reuters and the Financial Times both highlight that Tether’s gold is stored in Switzerland and that the mark-to-market value of these holdings has become large relative to some national gold reserves, amplifying political and regulatory salience.

Tokenized commodities also remain less integrated into DeFi than their headline market caps suggest. In practice, gold tokens often behave as exchange-traded collateral and as a portable “risk-off” asset within crypto portfolios, but broad, deep DeFi-native gold money markets remain thinner than for stablecoins and Treasury tokens. The gap is a function of (i) oracle design, (ii) liquidation mechanics for a 24/7 token referencing a global OTC and exchange-traded underlying, and (iii) the limited willingness of large issuers to support permissionless leverage.

Tokenized public equities and ETFs

Tokenized public equities have crossed the psychological “$1B” threshold but remain structurally fragmented between (a) economically backed tokens issued via custodians and SPVs, and (b) regulated “canonical share” approaches that aim to preserve shareholder rights onchain.

RWA.xyz reports $1.05B total value for tokenized stocks, with monthly transfer volume around $2.05B, about 189K holders, and a sharp decline in monthly active addresses versus the prior month (a useful signal that much activity is episodic and venue-driven rather than continuously organic).

Tokenized stocks by Platform (Source: RWA.xyz)

Tokenized stocks by Network (Source: RWA.xyz)

Tokenized stocks - Top assets (Source: RWA.xyz)

Who is winning: distribution-first platforms

The market is concentrated: platform share is led by Ondo (~60%), followed by xStocks (~23.5%) and Securitize (~9%), with a long tail.

Ondo’s strategy is distribution and breadth. The Solana Foundation announced that Ondo Global Markets expanded to Solana with access to 200+ tokenized U.S. stocks and ETFs, framing this as the largest tokenized stock platform by TVL and emphasising backing by licensed custodial broker-dealers.

xStocks, distributed via Kraken, is explicit about its structure: fully backed one-to-one, held with a licensed custodian in a bankruptcy-remote structure, but token holders often have creditor rights rather than direct shareholder rights, depending on the specific instrument and wrapper. The issuer entity for xStocks is described in its legal overview as a Jersey SPV registered with the Jersey Financial Services Commission, again illustrating that a large part of current tokenized equity market structure is “securities engineering” to achieve cross-border distribution.

What is real and what is overstated in tokenized equities

What is real:

- Demand for “always-on” global market access to U.S. equities and ETFs in jurisdictions where the products can be offered in compliant wrappers.

- Growing regulatory engagement with the idea that tokenized securities should not be penalised purely for their technology form. Reuters reported U.S. banking regulators (the Federal Reserve, Federal Deposit Insurance Corporation, and Office of the Comptroller of the Currency) signalling a “technology neutral” stance in capital treatment for tokenized securities relative to traditional securities.

- A credible path for exchange operators to move from derivative-like “stock tokens” to integrated post-trade designs. The Wall Street Journal reports Nasdaq partnering with Kraken to develop tokenized stock trading plans by early 2027, framed around governance rights and integration with existing settlement identifiers and depository infrastructure.

What is overstated:

- The claim that today’s tokenized stocks are already “open capital markets equivalents” to listed shares. Reuters has repeatedly flagged investor protection questions and the risk that some “tokenized shares” behave more like derivatives, with missing rights and fragmented liquidity.

- The idea that DeFi can simply absorb equities as collateral tomorrow. Equity market structure depends on corporate actions, trading halts, and regulated venue obligations that do not map cleanly onto permissionless AMM trading without significant redesign.

In practical terms, tokenized equities are currently a Tier 2.5 market: the tokens move and trade, but legal and rights architecture is heterogeneous, and that heterogeneity is the key blocker to Tier 3 integration.

Private credit, institutional funds, corporate and sovereign debt, and real estate

This is where the RWA narrative is most often misread. The “$342B represented value” headline exists largely because credit tokenisation in institutional pipelines is enormous in notional terms, but much of it is not distributed or DeFi-composable.

Credit: the sharpest split between represented and distributed

RWA.xyz reports tokenized credit with $4.90B distributed value versus $19.54B represented value, across 875 assets. That ratio is the cleanest quantitative measure of the market’s central tension: tokenisation has scaled faster as internal infrastructure than as open finance.

On the distributed side, credit is dominated by two platforms by market share: Maple (~47.13%) and STOKR (~37.35%). Maple’s lead product, syrupUSDC, is described on RWA.xyz as a yield-bearing vault token that appreciates as pooled capital is lent to vetted institutional borrowers, and it carries about $1.56B in asset value with thousands of holders. STOKR’s largest instruments include tokenized corporate-bond-like notes such as BMN2 on the Liquid Network with a Luxembourg securitisation wrapper and MiFID II framing on the RWA.xyz asset page.

On the represented side, the best illustration of “tokenized value that is not an open market” is the Figure HELOC token category. In the global asset list, Figure HELOC Token appears as a represented private credit asset with value around $15.7B. Figure Technology Solutions This is meaningful industrial scale, but it is not the same thing as an open, composable RWA market.

Institutional funds: a small but credible bridge category

Tokenized institutional alternative funds total about $2.60B, with the platform layer led by Securitize (~29.87%) and Centrifuge (~29.16%). The top fund on the list, Janus Henderson Anemoy AAA CLO Fund (JAAA), is around $743M, domiciled in BVI, and distributed across multiple chains via Centrifuge rails.

The reality here is that tokenized funds are functioning as regulated wrappers for onchain settlement and custody flexibility, but still with small holder counts and high minimums in many cases. That is consistent with an early-stage institutional product lifecycle: first solve settlement and operational friction, then pursue liquidity and broader distribution.

Corporate and sovereign debt: pilots exist, secondary liquidity is thin

Non-U.S. government debt tokenisation is about $1.16B total, but it is almost entirely one product family: Spiko (~78.89% share). Spiko Spiko’s EU T-bills fund is shown as a France-domiciled UCITS structure with onchain representations across several chains and close to $900M in value. This is one of the cleanest examples of Europe’s regulated fund wrapper meeting onchain distribution.

For corporate debt tokenisation, the most institutionally credible examples today are still bespoke issuances under specific national legal frameworks rather than globalised onchain bond markets. A prominent case is NRW.BANK’s €100m digital bond issued under Germany’s Electronic Securities Act (eWpG) with Cashlink as registrar, reported by NRW.BANK itself and covered by industry press. NRW.BANK Cashlink This is “real” as modernisation of issuance and registry, but it remains closer to Tier 1 and Tier 2 than Tier 3, because broad onchain secondary liquidity is not yet the core objective.

Real estate: still a rounding error, with activity spikes not depth

Tokenized real estate is about $438.88M total value across 64 assets, with around 11.74K holders and reported monthly active addresses of 870. Market share is split mainly between RedSwan (~30.80%) and Ctrl Alt (~28.54%).

In March 2026, real estate tokenisation is best understood as an intermittent capital-formation channel plus a registry experiment, not a scalable onchain market. The binding constraints are offchain: servicing, tenant and property management, jurisdictional property law, and investor eligibility. The onchain token is not the hard part, enforceable and standardised property rights are.

DeFi integration, regulation, and what must happen next

Why so much tokenized value is idle

The simplest explanation for “idle” in tokenized RWAs is that many of the largest assets are Tier 1 represented assets by design. If a token cannot be transferred peer-to-peer or withdrawn to external wallets, it cannot be used as collateral across protocols, traded widely, or inserted into DeFi legos. That is the point of the distributed/represented distinction.

Even inside distributed assets, idleness remains common because most products are constrained by one or more forms of gating:

- Investor eligibility constraints (qualified purchaser, accredited, non-U.S.), which sharply limits the organic holder base in the early years. This is visible directly in Treasury product holder counts, where large AUM products can have very few holders.

- Whitelisting and transfer-agent controls, which reduce the set of venues that can legally custody and transfer tokens. This is a core reason BUIDL’s DeFi trading is mediated via Securitize’s whitelisting and via UniswapX integration rather than a simple permissionless pool.

- Secondary market microstructure gaps: credible price discovery, corporate actions, and regulatory status for trading venues remain unsettled for many tokenized securities. Reuters notes regulators and institutions have raised concerns that “tokenized stocks” can lack protections and fragment liquidity.

Can RWAs and DeFi genuinely converge?

Convergence is happening, but in a specific form: permissioned DeFi and composable collateral, not fully permissionless global securities markets.

Aave’s institutional RWA market (Horizon) explicitly represents this model: verified participants, pre-approved collateral, and onchain borrowing and settlement. BUIDL’s route into DeFi liquidity similarly reflects a hybrid: onchain trading enabled for eligible holders through issuer-controlled rails rather than a general permissionless pool.

The structural frictions that prevent “full convergence” today are not ideological, they are mechanical:

- Redemption and settlement mismatch: many RWAs redeem during banking hours with traditional settlement, while DeFi liquidations are 24/7. This creates stress points in crises, when the need for liquidity is highest.

- Legal finality and enforceability: traditional capital markets rely on clear property rights and regulated market infrastructure; DeFi relies on smart contract finality. The bridge between them is still bespoke legal engineering (SPVs, notes, fund shares), and that heterogeneity blocks standardised DeFi risk models.

- Oracles and market data: equities, credit, and structured products require robust, manipulation-resistant reference pricing. Market structure participants are already debating what should be an acceptable “source of truth” as tokenized securities proliferate.

Which RWA vertical matters most over the next 24 months

The highest-conviction “matter most” vertical for 2026–2028 is tokenized cash and collateral, specifically short-duration government exposure (Treasury and Treasury-like MMF tokens) plus adjacent structures (repo-like wrappers, institutional collateral programmes). The reasons are observable in today’s data and integrations:

- It is already the largest distributed RWA segment at around $10B.

- It has the clearest product-market fit in crypto market structure: yield-bearing collateral and instant settlement.

- It attracts incumbent asset managers, which increases standard-setting pressure around custody, controls, and reporting.

Tokenized equities may grow faster in percentage terms (they are still small), but their path to Tier 3 integration is longer because corporate actions, shareholder rights, and regulated trading obligations create higher structural complexity.

Which geography is best positioned to lead

Leadership depends on what “lead” means:

- For scale of the underlying collateral asset, the United States dominates because U.S. Treasuries and USD-centric products are the base collateral of crypto markets and of most tokenized cash-equivalent funds.

- For regulated distribution wrappers with cross-border reach, Europe is structurally advantaged via regimes such as UCITS (as reflected by France-domiciled Spiko structures scaling into onchain representations).

- For market infrastructure experimentation, the United Kingdom is building controlled testing through the Digital Securities Sandbox, supported by the Financial Conduct Authority and Bank of England.

- Singapore remains a key hub for permissive but institution-first frameworks (visible in tokenized Treasury fund products domiciled there under the Securities and Futures Act). Monetary Authority of Singapore

The practical answer for “best positioned to lead RWAs into global capital markets” is a multi-jurisdiction stack: U.S. assets and managers for scale, EU/UK for deployment of regulated secondary market models, and Singapore for cross-border institutional rails. Today’s leading products already reflect this hybrid, with BVI, Bermuda, and Cayman domiciles recurring in fund wrappers, highlighting that legal arbitrage remains part of the scaling playbook.

Underpriced risks and the conditions for RWAs to become a meaningful slice of global capital markets

Issuer and platform concentration is the market’s core underpriced systemic risk. Concentration is visible across asset classes: tokenized commodities are dominated by a few issuers, tokenized stocks are dominated by two distribution platforms, and credit is dominated by Maple and STOKR in distributed form. Even where tokenized Treasuries are less concentrated than commodities, the top platforms still control the majority of value.

Legal wrapper fragmentation is the second core risk. The same “tokenized equity” label can mean: a Luxembourg securitisation token, a Jersey SPV note, a U.S. mutual fund share, or an offshore private fund share. These are not fungible in enforceability, transfer restrictions, investor rights, or insolvency treatment. This heterogeneity blocks standardised collateral frameworks and slows Tier 3 integration.

Infrastructure risk is not theoretical. In practice, the key failure modes are: (i) transfer-agent or whitelist control failure, (ii) custody and bankruptcy-remoteness disputes, (iii) oracle failure or market manipulation during off-hours, and (iv) redemption suspension or settlement gridlock during stress. The more tokenized assets are used as leverage collateral, the more these operational risks become systemic rather than idiosyncratic.

For RWAs to become a meaningful part of global capital markets rather than a specialised crypto collateral niche, the market needs progress on four non-negotiables:

- Standardised rights and disclosure primitives for tokenized securities (corporate actions, voting, dividends, and claims hierarchy), converging toward a small number of templates that regulated venues and DeFi risk managers can price and stress-test.

- Interoperable identity and compliance, enabling regulated transfer without collapsing composability. The current pattern is permissioned pools attached to existing DeFi rails, but scalable capital markets require more standardisation than bespoke whitelists per issuer.

- Institutional-grade secondary market infrastructure, including credible price discovery and acceptable market data feeds for tokenized assets. The debate around sources of truth for prices as tokenized securities multiply is already active in regulatory-facing market structure discussions.

- A settlement asset that is as programmable as the security, meaning tokenized cash or tokenized deposits with clear legal status. Without delivery-versus-payment at scale, tokenisation remains an overlay rather than a replatforming of capital markets.

Conclusion

The RWA market in March 2026 is not a single market, but two overlapping systems with very different implications for capital formation and market structure: assets that are merely represented onchain, and assets that are genuinely distributed, transferable, and capable of functioning as programmable collateral. That distinction remains the single most important filter for separating infrastructure modernisation from actual open-market progress. Public blockchain RWAs are growing, but the largest headline values still sit disproportionately inside represented or tightly controlled systems rather than in fully open capital markets.

What is already real is not the wholesale migration of traditional finance onto permissionless rails, but the rise of specific tokenized verticals where blockchain materially improves settlement speed, collateral mobility, and operational efficiency. Tokenized Treasuries and cash-equivalent funds remain the strongest example because they have already reached meaningful scale and have begun to integrate into exchange and collateral workflows. Tokenized gold also has real market-structure relevance because it offers transferable commodity exposure in crypto-native form. Parts of private credit are also operationally real, but much of the largest credit tokenization remains represented infrastructure rather than open, composable finance.

Tokenized equities are now important enough that they can no longer be treated as a fringe experiment. As of March 2026, the category had just crossed the $1B mark, and the latest public data now shows $1.08B in tokenized public stocks, confirming that the market has reached a new scale threshold. But the deeper takeaway is not the size alone. It is that the market is splitting into two paths: a near-term path dominated by wrapper-based, distribution-first products such as Ondo and Kraken’s xStocks, and a longer-term path aimed at canonical tokenized shares with preserved shareholder rights and integration into regulated infrastructure.

That distinction is crucial because most of today’s tokenized equities still do not give investors the same legal position as owning listed shares through traditional market infrastructure. xStocks, for example, are structured through a Jersey SPV as tracker certificates and do not confer voting rights; Kraken’s own risk disclosures state that holders do not have legal claims to the underlying shares. This means that a substantial share of current tokenized equity activity is still best understood as programmable wrapper exposure rather than true onchain equity ownership. The legal wrapper, not the token itself, remains the defining source of risk.

At the same time, the category is clearly moving into a more serious institutional phase. Ondo’s expansion to Solana with more than 200 tokenized U.S. stocks and ETFs shows that broad crypto-native distribution is scaling. More importantly, the Nasdaq-Kraken initiative points toward a future model in which tokenized equities preserve corporate actions, governance rights, and interoperability with existing securities infrastructure. That is the development worth watching most closely. If that model works, tokenized equities could start moving from synthetic or structured access products toward regulated onchain securities that matter to institutions not only for distribution, but for post-trade modernization itself.

For the next 24 months, however, the highest-conviction vertical remains tokenized cash and collateral, not equities. Treasuries and Treasury-like funds still have the clearest product-market fit because they solve an immediate institutional need: yield-bearing collateral that settles faster and works inside digital-asset workflows. Equities may grow quickly from here, but their path to full institutional relevance is longer because they must solve for shareholder rights, corporate actions, venue regulation, and enforceability across jurisdictions.

Institutional adoption, therefore, should not be mistaken for a sudden move to permissionless trading of regulated securities. In practice it means hybrid rails: permissioned access, whitelisted transfer, regulated wrappers, tokenized collateral in prime and exchange workflows, and controlled experimentation through legal and regulatory frameworks. The convergence between RWAs and DeFi is real, but the convergence path is narrower and more structured than many narratives imply. The market is not yet becoming a fully open tokenized version of traditional finance. It is becoming a layered system in which compliance sits at the perimeter and programmability increasingly sits at the core.

The bottom line is that RWAs are now clearly beyond the purely cosmetic phase, but they are still early in terms of true capital-market transformation. The most durable progress today is in programmable collateral. The most important open question is whether tokenized equities can evolve from wrapper-based exposure products into rights-preserving, institutionally credible market infrastructure. That is the next threshold that will determine whether tokenization remains a useful overlay, or becomes a genuine replatforming of global capital markets.

Sources:

Cover Artwork

Ancient Rome

Giovanni Paolo Panini, c. 1757

Risk Disclaimer:

insights4.vc and its newsletter provide research and information for educational purposes only and should not be taken as any form of professional advice. We do not advocate for any investment actions, including buying, selling, or holding digital assets.

The content reflects only the writer’s views and not financial advice. Please conduct your own due diligence before engaging with digital assets or related technologies, as they carry high risks and values can fluctuate significantly.

Note: This research paper is not sponsored by any of the mentioned companies.