Hyperliquid began with a contradiction crypto had never properly solved.

The industry promised markets without custodial gatekeepers, opaque balance sheets or trusted intermediaries. Yet the venues where serious traders actually went for liquidity, leverage and execution were still centralised exchanges. They offered speed and depth, but required users to give up custody and trust the operator.

Hyperliquid attacked that contradiction directly. It did not try to make DeFi more ideological. It tried to make it good enough for traders who normally do not care about ideology at all. The result was an onchain derivatives venue that felt close enough to a serious centralised exchange to attract real volume, while preserving the self-custody, transparency and programmability that DeFi had long promised.

By mid-2026, Hyperliquid was no longer just a DEX in the old sense. It had become the reference case for onchain order-book trading, expanded beyond crypto perpetuals into commodities, equity-linked and pre-IPO synthetic markets, and begun moving into outcome and options-style instruments. What started as a better trading venue had become a purpose-built chain with an embedded exchange and a growing market-deployment layer.

The founder story matters because Hyperliquid looks like Jeffrey Yan’s biography translated into market structure. He was raised in Redwood Shores by a single mother who taught him to think “beyond the sky”; discovered elite mathematics late, failed, redirected himself into physics and won International Physics Olympiad gold; studied mathematics and computer science at Harvard; then joined Hudson River Trading, where he found markets intellectually pure but personally limiting. Yan did not leave because he disliked quantitative finance. He left because he wanted to build something where his own leverage over outcomes was larger.

Jeffrey Yan (Source: Colossus)

That question led first to a failed 2018 prediction-market project, then to Chameleon Trading, and finally to Hyperliquid. It was not born from a venture deck or token launch. It was born from an operator’s frustration with the gap between what crypto claimed to be and where real liquidity actually lived.

This paper argues that Hyperliquid matters not only because it became one of crypto’s most successful trading venues, but because it is one of the clearest attempts to rebuild market structure from inside crypto’s own constraints. The central question is no longer whether onchain trading can work. Hyperliquid has answered that. The harder question is whether an exchange-funded network can become neutral infrastructure for a broader share of global finance.

Before Hyperliquid

Jeffrey Yan’s background is not interesting because it is conventionally inspirational. It is interesting because the pattern of his decisions before Hyperliquid helps explain the pattern of the system after it.

He grew up in Redwood Shores, surrounded by the Bay Area’s technology wealth but not born into its affluent core. After his parents divorced, his mother, an accountant, raised Yan and his younger sister largely on her own. The family situation matters less as biography than as operating psychology. Yan’s later insistence on self-direction, discomfort with performative status and indifference to conventional corporate markers all fit someone who grew up near Silicon Valley’s promise without inheriting its security.

His mother’s phrase, “beyond the sky”, appears to have given him both ambition and permanent anti-complacency. That duality, extreme competitiveness paired with scepticism toward celebration, reappears throughout Hyperliquid’s culture.

The most predictive detail from Yan’s adolescence is not simply that he was gifted. It is that he entered elite competition late and then tried to compress years of preparation into months of self-study. He discovered serious mathematics only in eighth grade, after following a friend from a private school to a competition, then began waking at five in the morning to work through old olympiad papers alone. Within a year he had reached the U.S. Math Olympiad training camp, but failed to make the national team. Instead of treating that failure as final, he redirected himself into physics, taught himself from upperclassmen’s textbooks and Feynman lectures, and within roughly a year rose to the top tier of U.S. high-school physics, eventually winning International Physics Olympiad gold.

Jeffrey Yan

The relevant point for Hyperliquid is not merely that Yan was smart. It is that he appears to specialise in identifying the distance between himself and an elite frontier, then closing it through concentrated, self-imposed work. Hyperliquid’s rapid movement from testnet concept to custom chain and institutional-scale venue looks like the adult version of the same pattern.

Harvard reinforced that orientation. Yan studied mathematics and computer science, took on difficult technical work early, and finished first in a notoriously difficult algorithms course as a freshman. More important than the credential was the peer group. He formed close ties with other olympiad-calibre students, including Scott Wu, later a founder of Cognition AI. Their conversations centred on what it means to be the best in a field and what constitutes the “essence” of high performance. That line matters because Hyperliquid does not read like a product built by people optimising for messaging or fundraising. It reads like a product built by people obsessed with the purest structural version of a problem. Yan’s later aversion to half-measures, especially his reluctance to accept AMM or hybrid-order-book compromises, makes more sense in that context.

His internships also foreshadowed the synthesis. At Google X and Nuro, he worked around autonomous systems. At Tower and then Hudson River Trading, he moved closer to a world where latency, routing and execution quality define economic reality. He joined HRT full-time in late 2017, liked trading intensely, and saw markets as a pure real-world game in which smart people compete while producing useful liquidity and efficient prices. Yet he left after only about eight months. The issue was not that the work felt trivial. It was that he felt too replaceable inside a machine that would already run well without him.

That dissatisfaction is conceptually important. Hyperliquid is partly a response to market-structure flaws, but it is also a response to Yan’s desire to build a system in which his own leverage over outcomes would be larger than it had been at HRT.

That desire produced his first major crypto project. In 2018, after becoming convinced by Ethereum’s broader implications, Yan left HRT with his Harvard roommate Brian Wong and built Deaux, a prediction-market startup. Deaux pursued offchain matching with onchain settlement because Ethereum itself was too slow to run a serious exchange. Yan later said the team had many things right on the infrastructure side, but was not yet ready as builders and had launched into the wrong market backdrop.

Deaux appears to have taught four lessons that later shaped Hyperliquid. First, architecture does not rescue a product nobody wants to use. Second, neutral rails do not remove regulatory reality, especially in anything resembling event markets. Third, user experience matters as much as idea purity. Fourth, some financial primitives only become viable once surrounding market infrastructure is already strong enough to support them. When Yan later returned to outcome markets, he was not repeating 2018. He was returning with a chain, a user base, a liquidity pool, deployer tooling and real fee flow already in place.

After Deaux failed, Yan returned more than half of the roughly $450,000 raised, waited out his HRT non-compete and eventually moved to Puerto Rico in late 2019. This became the Chameleon Trading period, and it is hard to understand Hyperliquid without it. Chameleon began with about $10,000 of Yan’s savings and developed into a substantial anonymous trading operation. It was initially run from a one-bedroom apartment near the beach, with Yan writing Python scripts, monitoring exchange APIs and iterating relentlessly.

The key point is not the exact return profile. It is that Chameleon trained Yan and his collaborators directly on the weaknesses of centralised crypto exchange infrastructure. They learned from the inside how fragmented, inefficient and strategically gameable those markets were. That is founder-market fit in the strictest sense.

Chameleon also explains why Hyperliquid could be bootstrapped. The trading operation appears to have created enough personal capital for Yan to fund Hyperliquid’s incubation without relying on venture financing. That mattered because it removed an ordinary startup constraint. Hyperliquid did not have to accept venture money to survive, and it did not have to sell token inventory to subsidise early market makers. Those absences, especially in crypto, shaped everything downstream: ownership, go-to-market, credibility and the cultural force of the eventual HYPE launch.

Why shut down Chameleon if it was profitable? The answer appears philosophical as much as economic. By 2022, Yan had become frustrated that crypto had recreated many of the same centralised trust structures it had promised to eliminate. Chameleon let him extract value from market inefficiencies. Hyperliquid offered the possibility of redesigning the infrastructure that created those inefficiencies in the first place.

In that sense, the move from Chameleon to Hyperliquid was not a shift from finance to ideology. It was a shift from trading against bad rails to trying to build better ones. That decision, more than any token launch or valuation mark, is the actual founding act of Hyperliquid.

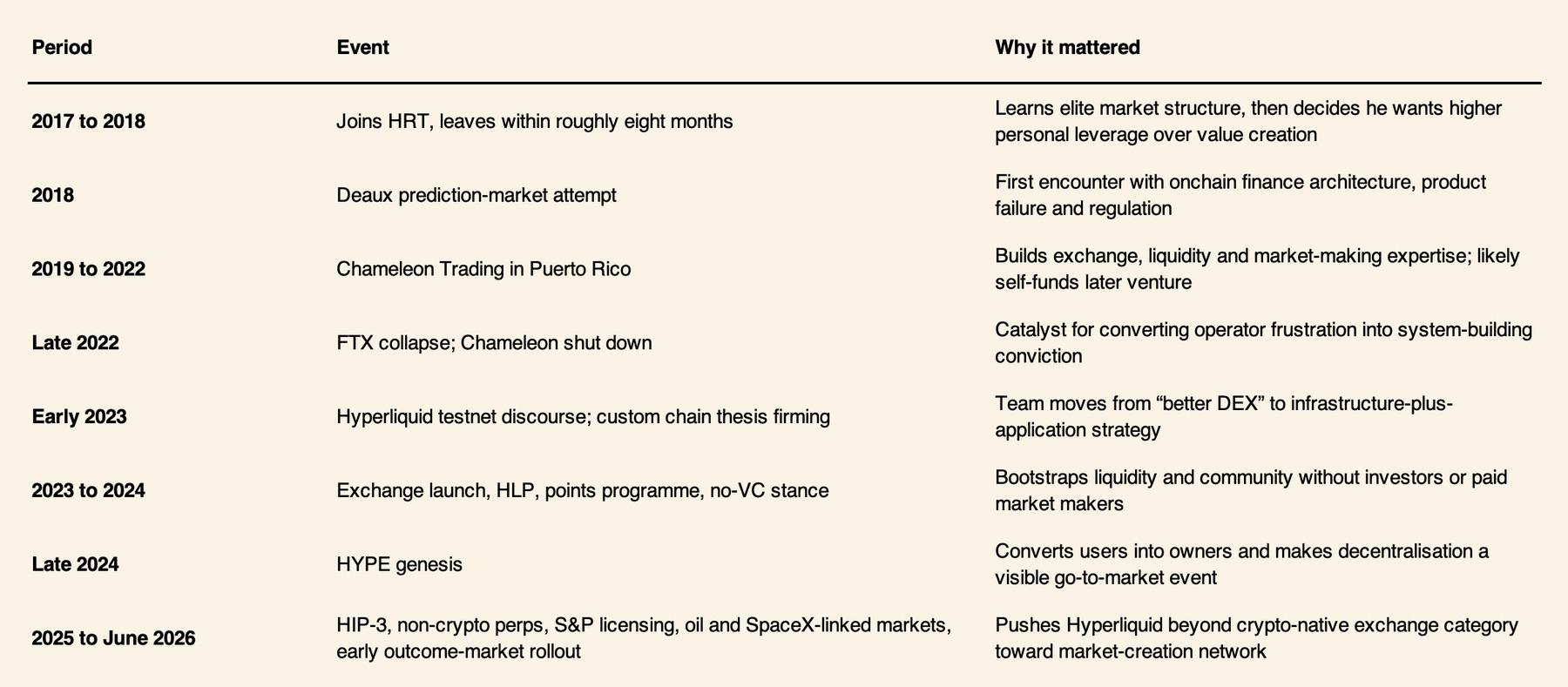

Condensed timeline from Yan’s formation to Hyperliquid’s June 2026 position

Why Hyperliquid had to exist

To understand why Yan believed Hyperliquid had to be built, one has to start with the structure of crypto derivatives before Hyperliquid. In crypto, perpetual futures became the dominant speculative instrument because they are easier to hold than dated futures and more capital-efficient for traders who want continuous exposure. The broader product idea traces back to Robert Shiller in the 1990s, but in crypto it became practical through BitMEX and then spread across major centralised venues. By 2025, the global perpetuals market had become enormous: Reuters reported $61.7 trillion of annual trading volume, while offshore venues had normalised leveraged, always-open directional speculation for a global customer base.

Centralised exchanges such as Binance and FTX therefore solved one problem while exacerbating another. They gave traders tight spreads, familiar order books, high leverage and reliable execution. But they required trust: trust in custody, trust in solvency, trust in liquidation handling, trust in internal conflict management, and trust that the infrastructure was not being run for insiders. Yan’s team had direct exposure to that world first through bot-running and market making, then through DeFi. Their conclusion was that crypto’s most liquid venues had reintroduced the intermediation problem that Bitcoin and Ethereum were supposed to remove. FTX’s collapse did not create that view, but it made it impossible to treat it as theoretical. In Yan’s own framing, FTX was the call to arms, not the original idea.

The obvious alternative, early DeFi, was not good enough. Yan’s early explanations of the team’s reasoning were unusually clear in market-structure terms. They were not committed to order books for ideological reasons. They started from what traders actually wanted: low latency, visible liquidity, low slippage and a clean user experience. On that standard, the first-generation DEX stack failed in several ways. Constant-product AMMs were clever bootstrapping tools, but from a market maker’s perspective they often meant being arbitraged back and forth, especially once liquidity mining faded. Yan’s critique of AMMs was therefore structural, not tribal. They distributed execution against passive liquidity providers in ways that could be unsustainable for serious market making unless heavily subsidised.

Oracle-based and hybrid designs fixed some of those problems but introduced others. Yan’s comments on GMX are telling. He treated oracle-dependent systems as ingenious band-aid solutions: more capital-efficient than simple AMMs, but still dependent on trusted oracle logic, arbitrary rules and exploit-sensitive boundaries. A design that required constant fine-tuning around oracle manipulation was not, in his view, a final answer for the core market venue. He applied an even sharper criticism to dYdX v3. Its then-live order book, in his view, was effectively run offchain in a centralised manner, with settlement onchain but order placement and cancellation dependent on a privileged server. In economic terms, that meant the most latency-sensitive part of the venue, the part that most determines market quality and fairness, remained outside transparent public consensus. Hyperliquid’s original product thesis was built around eliminating precisely that split.

That helps explain why Hyperliquid decided not merely to build a new interface, but to build a new chain. The team initially experimented on Arbitrum and considered more modest approaches, including hybrids and batch auctions. The conclusion after the testnet period was that existing infrastructure could not support the experience they wanted. Order placement, order cancellation, matching, margining and liquidation all had to live close enough together, and move fast enough, that the user would not feel they were trading on a compromised imitation of a centralised venue. That meant sacrificing the convenience of deploying on a general-purpose chain and instead building a purpose-built execution environment. Yan has said plainly that if a performant L2 had existed that could handle the required order throughput, they would have used it. The custom chain was therefore not recursive crypto empire-building. It was a technical necessity created by the product specification.

This is the central strategic point. Hyperliquid did not build its own chain because having an L1 was fashionable, or because a token needed a home. It built its own chain because Yan and the team believed the only way to make order-book trading, liquidations, margin and user experience work together under transparent, non-custodial constraints was to treat the whole system as a unified state machine. The chain was originally framed as a means to support the exchange, not as a universal-purpose platform. That narrowness was a strength early on. It let the team optimise for one high-value use case instead of pretending to solve all blockchain problems at once.

The timing matters too. FTX was the emotional catalyst because it proved that trusted intermediaries could vaporise customer confidence overnight. But Hyperliquid’s founding frustration predated the collapse. The team had already been building for months. Their regret, as Yan later put it, was that they had not started earlier. That distinction is analytically important. If Hyperliquid had been merely an anti-FTX product, it might have remained a niche custody-safe exchange. Instead, it was built from the beginning around a stronger claim: that DeFi had the right values but had not yet produced the right execution environment. FTX sharpened the mission. It did not invent it.

The order-book decision then had second-order implications. Putting the book onchain improves auditability, data availability and the ability to reconstruct every order, cancellation and liquidation. That creates a transparency advantage, but it also imposes harsh performance requirements and exposes the venue to a different kind of scrutiny. The later debates around October 2025 liquidations and the JELLY incident show both sides of that trade-off. Hyperliquid can be audited in ways centralised exchanges cannot, yet its visible stress episodes also become headline material because the data are actually there. The platform’s broader strategic bet is that over time, the transparency dividend will outweigh the optics penalty. The June 2026 academic work on Hyperliquid’s microstructure points in that direction, finding that visible TWAP orders can reduce execution costs relative to comparable hidden metaorders and attract liquidity provision while shifting adverse-selection costs toward those who choose not to preannounce. In market-structure terms, Hyperliquid’s openness is not just moral theatre. It changes execution.

That is why Hyperliquid had to exist in Yan’s eyes. Not because crypto lacked another exchange, but because it lacked a non-custodial venue that treated order-book performance, transparent execution and self-custody as parts of one problem rather than separate modules. In that sense, Hyperliquid’s intellectual origin is simpler than the mythology around it. Yan and his colleagues believed traders wanted what institutional traders had always wanted, and believed crypto’s existing stack either could not or would not provide it without putting trust back in the middle. Hyperliquid began as the attempt to remove that contradiction.

From a perpetual DEX to a financial network

Hyperliquid’s first important strategic move after launch was not the token. It was liquidity bootstrapping. The exchange launched publicly in late February 2023 and, for a time, attracted mainly experimental users, including NFT traders testing perpetuals for the first time. The professional liquidity the venue needed did not appear automatically, and Yan refused to solve that with the standard crypto toolkit of paying market makers in cash, equity or token entitlements. Instead, in May 2023, he pushed Chameleon-style strategies into the Hyperliquidity Provider vault, or HLP. Users could deposit capital into a transparent onchain market-making and backstop-liquidity vehicle and receive the economic results directly, with no management fee or carry. This was not only a clever bootstrap. It was also a political statement: one of the most lucrative activities in crypto microstructure would be opened, in principle, to ordinary users rather than reserved for a closed set of firms.

HLP also solved a reputational problem. Hyperliquid needed liquidity, but did not want to depend permanently on a house market maker analogous to the way Alameda had been intertwined with FTX. Yan explicitly wanted HLP not to become essential to Hyperliquid’s functioning. The vault therefore acted as a bridge between a zero-liquidity startup and an exchange that could attract independent market makers without paying them directly. This is one of the clearest examples of the Hyperliquid pattern: use a tightly integrated internal primitive to solve a launch problem, then try to decentralise the economically important function outward over time.

The next strategic turn was spot trading, and its significance is often underappreciated. Perpetuals can be settled economically without anyone holding the underlying asset. Spot markets cannot. When Hyperliquid moved into spot, it collided with the hardest custodial question in finance: who actually owns and settles the asset? This appears to be the moment when Yan stopped thinking of Hyperliquid merely as an exchange on a chain and began thinking of it as a chain with an exchange built into it. That conceptual inversion is crucial. It opened the path to HyperEVM, external builders and the broader ambition to house more of finance on the network. Spot was not an adjacent product. It was the forcing function that pushed Hyperliquid from application to platform.

The HYPE genesis in November 2024 then did several jobs at once. Roughly 31% of total supply was airdropped to about 94,000 early users, while the team’s own allocation was 23.8% and vested over years. The public record supports the broad direction of travel: no venture investors received a private allocation, no insiders received a preferential public-market entry, and the airdrop handed meaningful ownership to the user base. Strategically, that was at least four things simultaneously. It was a decentralisation event, because it widened token ownership. It was a go-to-market event, because it rewarded use rather than marketing reach. It was a cultural legitimacy event, because crypto participants interpreted it as unusually fair. And it was a loyalty mechanism, because users who had previously been customers suddenly owned part of the network’s future economics. It was not pure altruism, and it did not need to be. It was the most efficient way Hyperliquid could buy long-term legitimacy with an asset it controlled.

The airdrop also changed the chain’s governance and security trajectory. Yan has described the token generation event less as an operating milestone than as a decentralisation milestone that enabled native proof-of-stake consensus and a more distributed validator set. The implication is that HYPE was never meant to be only a speculative asset. It was security collateral, deployment collateral, alignment collateral and, increasingly, a meta-asset around which other network functions could be organised. That matters for valuation debates. If HYPE were only a fee-abstracting exchange token, Hyperliquid would look like a high-margin trading venue with a popular loyalty asset. Because HYPE also sits in staking, deployment and potentially application-layer composability, the token’s economic meaning is broader, though still not broad enough by mid-2026 to sever its dependence on trading activity.

This is where HyperEVM enters. Yan has described HyperEVM not as another EVM chain, but as a programmable portal into Hyperliquid’s native primitives. That framing is important. HyperEVM’s strategic utility is not simply that developers can port Solidity contracts. It is that those contracts can access balances, liquidity, staking and exchange-state primitives already native to Hyperliquid. If that architecture works, then applications built in the EVM environment do not need to recreate a separate liquidity universe. They can plug into the one that already exists. This is the operating-system analogy in its most credible form. Hyperliquid is not aspiring to be a better app store full of random dApps. It is trying to be a financial substrate with an immediately useful liquidity core.

Builder codes were the first step in exporting distribution. They allowed third-party developers to build user-facing trading apps on top of Hyperliquid’s liquidity and keep a cut of the fees their users generated. By 2026, those builders had reportedly earned more than $70 million since October 2024. Matt Huang’s description of this as franchising out the user experience is analytically useful because it captures the organisational difference from Binance or Coinbase. Hyperliquid is trying to separate infrastructure ownership from interface ownership. If that model scales, the core protocol becomes harder to displace because it no longer needs to win every end-user relationship directly. The risk, of course, is fragmentation and lower quality control. But the strategic direction is clear: Hyperliquid wants outside entrepreneurs to own businesses on top of the network.

HIP-3 extended that principle from interfaces to markets themselves. It created a mechanism through which anyone staking sufficient HYPE could deploy perpetual markets, choose parameters and retain half the trading fees. Yan’s comments on the model make the philosophy explicit: finance is too large and too specialised for one team to list, source and operate everything internally. A centralised listing desk may move faster at first, but a permissionless deployer network can be more robust and globally scalable if it works. This is one of Hyperliquid’s most consequential design choices. HIP-3 is not merely a new market category. It is a decentralised listing system, a fee-sharing model and a distribution model for domain expertise. It turns the exchange from a venue with a catalogue into a platform that lets specialists create the catalogue.

By early 2026, that thesis had clearly moved beyond crypto. Trade[XYZ], the leading deployer, had launched markets in silver, crude oil, stock indices and foreign exchange, while independent deployer markets had reportedly grown to a significant share of total volume. Yan also said HIP-3 silver markets had reached about 2% of global silver price-discovery volume. Even if that figure is treated as a founder statement rather than a fully audited exchange comparison, it captures the ambition correctly. Hyperliquid is no longer trying only to put crypto derivatives onchain. It is trying to make perpetuals the generic market wrapper for anything liquid enough to support them.

The March and June 2026 Wall Street Journal reporting makes clear why this matters. During the Iran-related oil shock, Hyperliquid’s 24/7 oil perps gave global traders a venue for continuous positioning while mainstream futures markets were closed, and cumulative oil-futures volume on the exchange reportedly jumped from roughly $339 million to about $7.3 billion within days. Shortly after, S&P Dow Jones Indices licensed the S&P 500 to Trade[XYZ] for what the WSJ described as the only licensed S&P 500 perpetual contract. By June, Hyperliquid’s SpaceX-linked perpetuals had become one of the platform’s most actively traded instruments, and pre-IPO contracts were being treated as real-time speculative valuation signals for one of the world’s most anticipated flotations. The significance is not that Hyperliquid has solved equity ownership or commodities clearing. It has not. The significance is that it has already created a credible market-creation layer for synthetic exposure where legacy market hours, access rules and listing processes are slower or narrower.

HIP-4 represents the next extension. Yan and the Colossus profile both frame it as the route back into options and prediction-style, or more accurately outcome-linked, markets. The distinction is useful: spot and perps express linear exposure, while outcome markets let users express bounded or nonlinear beliefs. By mid-2026, the WSJ was already describing Hyperliquid as having recently introduced outcome prediction markets and options trading. That is enough to say the product line had moved from proposal into public-facing rollout. It is not enough to treat HIP-4 as a mature or deeply liquid business line. The current public record supports viewing CPI, Fed or sports-linked markets as plausible early use cases rather than proven growth pillars.

The collateral story is strategically important, but still less fully documented than the exchange and HIP-3 businesses. Yan has described an aligned stablecoin model associated with Native Markets, lower fees for users of the aligned stablecoin and protocol-level revenue-sharing logic. Later June 2026 materials suggest a transition from USDH toward USDC as the aligned quote asset, involving Coinbase and Native Markets, though the final legal and operational structure remains unclear. The narrower conclusion is still meaningful: Hyperliquid clearly views quote-asset design as strategic infrastructure, not as a neutral afterthought. Whether the final form proves to be a cleaner institutional on-ramp or a new dependency on a regulated U.S.-linked issuer remains open.

So what category does Hyperliquid belong to by June 21, 2026? The answer is that it spans several, but not equally. Economically, it is still primarily an exchange whose revenues and attention are driven by leveraged trading. Architecturally, it is a blockchain with a native exchange and a programmable layer. Organisationally, it is moving toward a market-creation network in which external deployers and interfaces own more of the product surface. The most useful label today is probably not “exchange” or “L1”, but “financial network with an embedded flagship exchange”. The strongest version of the financial-operating-system claim remains aspirational. The network has the right architectural shape; it does not yet have enough non-perps economic weight to make the thesis fully earned.

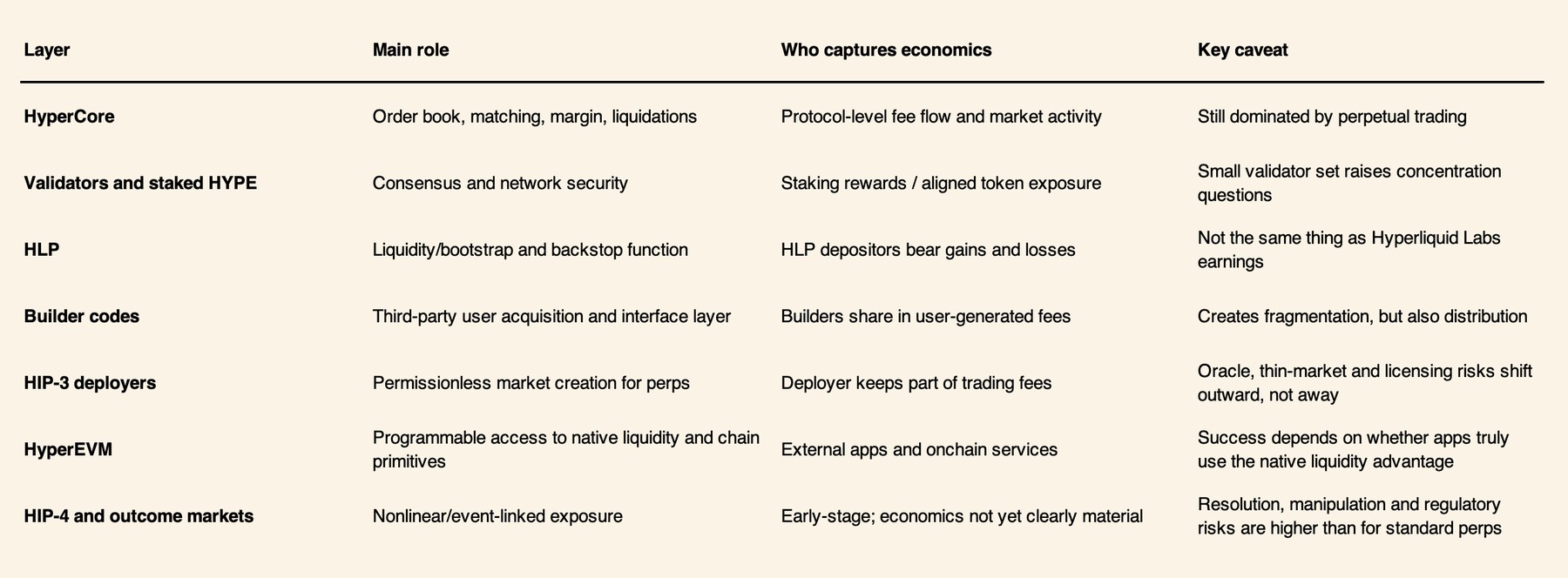

Hyperliquid system map in economic rather than purely technical terms

The company that does not want to be a company

Hyperliquid Labs, Hyperliquid the protocol, the Hyper Foundation, validators, HLP, deployers and builders should not be collapsed into “the company”, because the system is designed not to be reducible to a single corporate box. Yan has said this directly: Hyperliquid itself is not a company in the traditional sense, and Hyperliquid Labs is only a small contributor group responsible for a critical part of the broader ecosystem. That distinction is not semantic. It determines where fees go, how product expansion happens and how the platform’s famous productivity metrics should be understood.

The small-team model is real, but it is often caricatured. Colossus reported a team of 11 at the time of its profile and noted that two more people had been added since the visit, while Yan has continued to describe the core group as unusually small. The temptation is to turn that into trivia. The more important point is the operating model behind it. Hyperliquid recruits heavily from olympiad and elite engineering circles, prefers exceptional generalists, subjects candidates to long working interviews, and treats integrity as a hard requirement. Yan’s view is that if something can be built externally, it should be. That means the small payroll number is not simply a productivity marvel. It reflects a deliberate refusal to absorb every adjacent function under one roof. Hyperliquid Labs is small partly because the product boundary is intentionally narrow.

This design creates both edge and risk. The edge is lower overhead, less bureaucracy and faster integration between product intuition and implementation. Colossus portrays a daily stand-up culture with long silences, deeply technical discussion and a leadership style oriented around hard thinking rather than big-company coordination theatre. Yan’s comments on team-veto hiring, trust and autonomy reinforce the same picture. Such an environment is countercultural in a sector full of bloated business-development teams and token-marketing departments. It also fits the founding story: Yan built Chameleon largely alone or with a very small team, and seems temperamentally uncomfortable with organisational sprawl.

The risk is that the same structure produces key-person dependence and hidden bottlenecks. Hyperliquid’s strategic coherence comes substantially from Yan’s taste: what is worth building, what remains external, what principles are non-negotiable, and which compromises are unacceptable. That coherence is valuable. But it also means the system remains culturally and strategically centralised even as it tries to decentralise economically. A key question for 2027 and beyond is whether that founder-guided coherence can survive the success of the external-builder model. Put differently: can Hyperliquid decentralise without becoming incoherent, and can it stay coherent without remaining highly dependent on one person? The public record does not yet resolve that tension.

On work culture, the myth is harsher than the reality. Colossus presents Yan as intensely disciplined to the point of austerity: repetitive clothing, self-administered haircuts, exercise as cognitive maintenance, and very little celebration. But the same source material also suggests that he does not require everyone else to mimic his exact schedule. Yan has explicitly rejected “flexing” all-nighters and framed output quality as the governing metric. That distinction matters because it separates Hyperliquid from companies that romanticise overwork as identity. The better description is that Yan is personally extreme, but tries to institutionalise standards, not his own lifestyle. That is still hard to scale, but it is less brittle than the founder-cult version.

The no-VC decision is even more foundational than the headcount. Colossus reports that in early 2024 Hyperliquid was burning significant cash, VCs were circling, and one offer would have brought around $100 million into the project at a $1 billion valuation. Yan ultimately decided not to take it. The practical effect was profound. Without investors, Hyperliquid had no obligation to reserve token supply for private backers, no need to run a points-farming scheme optimised around likely fund interests, and no reason to frame the organisation as a venture-backed software company seeking conventional exits. The HYPE launch therefore looked credibly different to the market because it actually was different. “No investors” was not just branding. It removed one of the most common sources of cynical token overhang in crypto.

The trade-off is that bootstrapping limits what can be internalised. Venture capital is not only money. It is also staffing cushion, legal spend, lobbying capacity and distribution networks. Hyperliquid compensated by narrowing the internal mission and leaning on external builders. That was part principle and part necessity. A better-capitalised Hyperliquid might have moved faster into certain institutional products or regulatory strategies. It is equally possible that taking venture money would have weakened the ownership story that made Hyperliquid culturally distinct. On balance, the no-VC decision appears to have strengthened the network’s legitimacy more than it weakened product execution, but the counterfactual remains unknowable.

Singapore sits at the intersection of regulation, focus and safety. Colossus reports that the move followed concern over the U.S. regulatory climate for derivatives and a comparative review of Hong Kong, Switzerland and Singapore. Yan’s own description is revealingly simple: Singapore is safe, modern and “boring”, which for him means low distraction. That boringness is not incidental. Hyperliquid’s culture seems actively designed against noise, and Singapore offered a place where the team could build without the psychological and regulatory churn of the United States.

The darker side is personal security. Colossus reports that increased visibility led to stalking concerns, office relocation, a bodyguard in Singapore and additional travel security as violent crypto-related extortion incidents rose globally. This is relevant not for shock value, but because it illustrates an under-discussed fact about building public financial infrastructure in crypto: success itself can create operational risk. Hyperliquid’s founders chose a route that rejected conventional corporate shielding while creating a very visible, highly liquid token. That combination may strengthen community legitimacy, but it weakens personal anonymity. It is not obviously a problem that a larger HR department or legal team can solve.

The most revealing organisational question is theoretical: is Hyperliquid Labs trying to become a big company at all? The answer appears to be no. Yan’s repeated distinction between a finance super app and a financial system suggests that Labs wants to remain the maintainer of a small set of critical primitives rather than the owner of every business line. That is why builder codes, HIP-3 and HyperEVM hang together. They are not expansion by headcount. They are expansion by surface area. Hyperliquid’s system can grow while Labs stays small only if outsiders find it worthwhile to build businesses on top of the rails. That is the real test of the organisation. Not whether it can hire 200 people, but whether it can avoid having to.

The economics of Hyperliquid

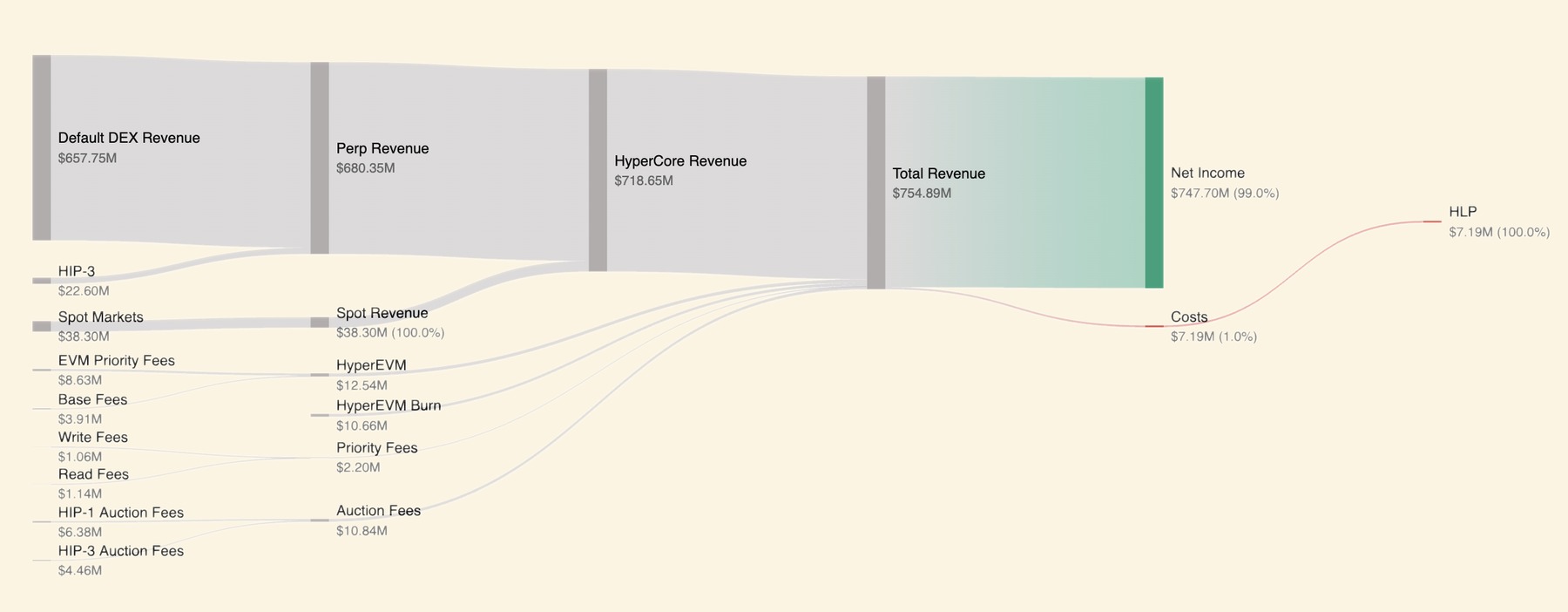

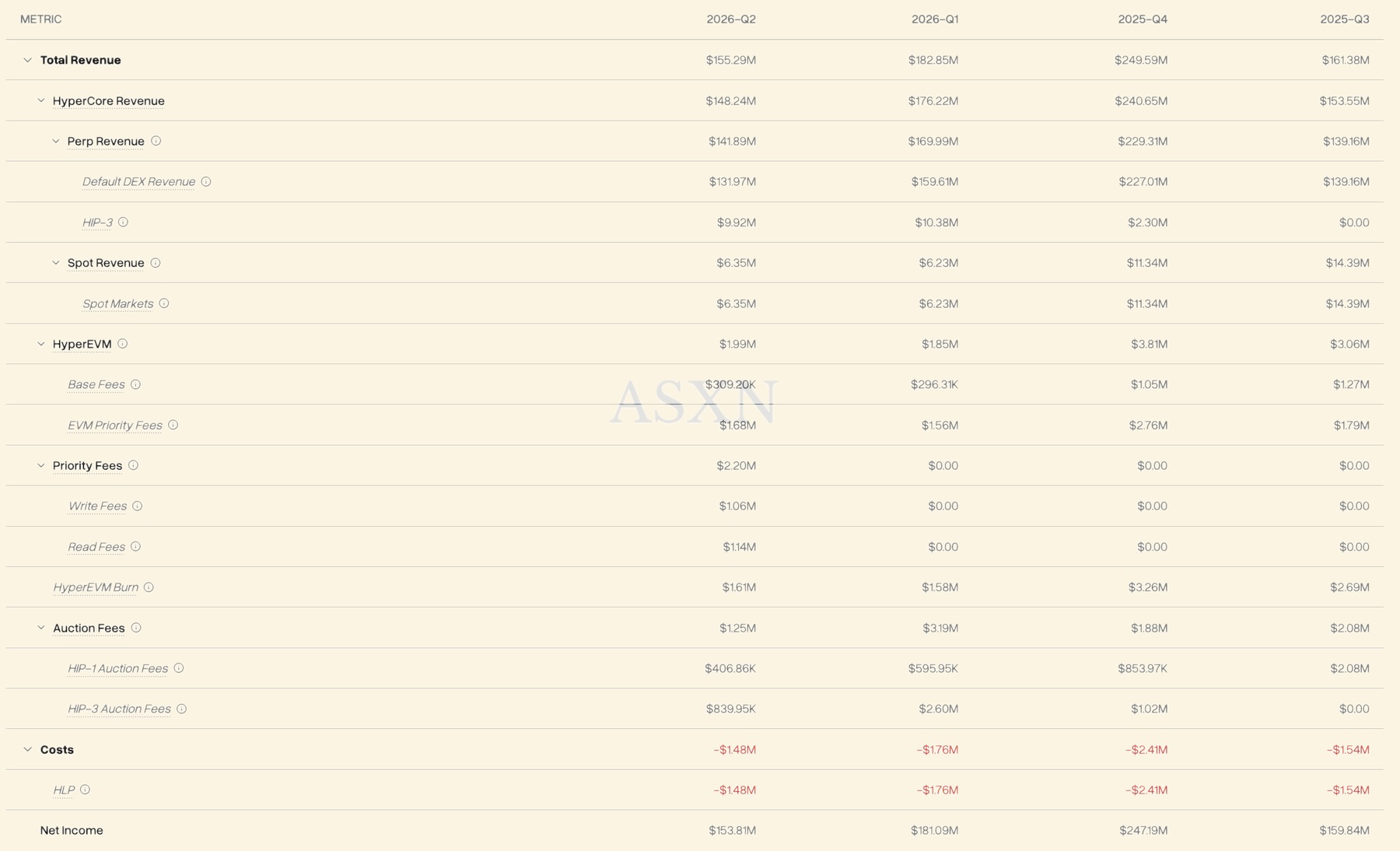

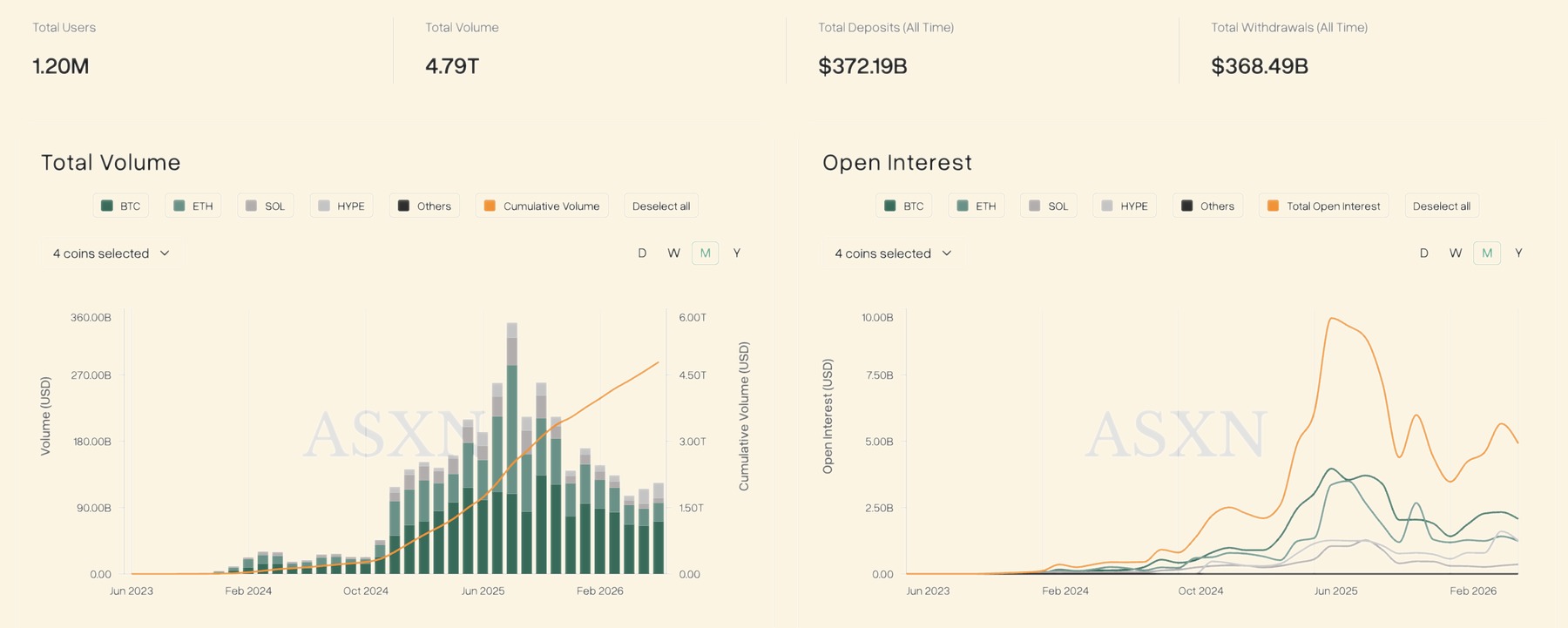

Hyperliquid’s economics require careful vocabulary. The available dataset records 1.20 million total users, $4.36 trillion in cumulative volume, $372.19 billion in cumulative deposits, $368.49 billion in cumulative withdrawals, and a quarterly revenue table running from 2025 Q3 through 2026 Q2 quarter-to-date. The Q2 QTD structure aligns with an 82-day window from April 1 through mid-2026, which makes the quarterly table best understood as a mid-2026 quarter-to-date snapshot. The 24-hour market data should be treated separately as a late-June point-in-time snapshot rather than live market data.

The first analytical discipline is terminology. In this dataset, reported cumulative “revenue” includes HyperCore buybacks, HyperEVM burns and auction fees. The “costs” line consists entirely of HLP costs. On that basis, the cleanest label is protocol revenue and value accrual, not company revenue. Hyperliquid Labs is not shown as directly receiving trading fees in the visible protocol-level accounting, and Yan has stated that Hyperliquid does not operate a discretionary buyback programme and that Hyperliquid Labs is not the same thing as the protocol. Colossus separately reports that none of the protocol fees flowed to the team and that Yan still personally funded many team costs. The implication is straightforward: the visible onchain accounting is a protocol-level ledger, not an income statement for a conventional software company.

Quarterly protocol revenue and value-accrual breakdown

Protocol revenue

Hyperliquid’s economics remained overwhelmingly tied to HyperCore and, within HyperCore, to perpetual futures. In every quarter shown, perps accounted for more than 86% of total protocol value accrual; by 2026 Q1 and Q2 QTD, that figure was about 93% and 92%. Second, HIP-3 mattered quickly. It contributed almost nothing in 2025 Q4, then jumped to 5.7% of protocol value accrual in 2026 Q1 and 6.3% in 2026 Q2 quarter-to-date. Third, spot and HyperEVM remained real but secondary. Together they were not the core unit economics of the network.

The available data therefore support a balanced conclusion: Hyperliquid is evolving architecturally beyond an exchange, but economically it still looks like a highly successful perpetuals venue with emerging adjacent lines.

Q2 needs its own caveat because it is incomplete. At the attached Q2 quarter-to-date pace, Hyperliquid was generating about $1.70 million per day of protocol value accrual. A simple straight-line extrapolation would imply roughly $154.8 million for the full quarter and an annualised pace of about $620.9 million. That extrapolation is mechanically useful but analytically fragile. Trading activity on Hyperliquid is event-driven and volatile; war-related flows, non-crypto market launches and memetic bursts can distort annualised run rates dramatically. The right interpretation is not “Q2 proves a $621 million annual revenue business”. It is “late-June pace remained very high even after the 2025 and early-2026 growth step-change”.

The attached cost line produces the famous near-99% surplus margin, but that figure is easily abused. The file’s visible costs are only HLP costs. That means the line excludes most things an equity analyst would normally classify as operating expense: salaries, equity compensation, cloud/refactor spending, legal advice, travel, security, tax structuring, external audits, policy work and founder-funded burn. Hyperliquid was burning hundreds of thousands of dollars per month in 2024 and that Yan still paid many team costs himself as of the profile. So the 99% figure is real inside the narrow accounting frame of the attached dataset, but it is not the right answer to “how profitable is Hyperliquid Labs as a company?”. It is the right answer only to “how much of visible onchain protocol value accrual is consumed by visible onchain HLP costs?”.

Users and capital flows also require restraint. On the attached snapshot, cumulative net deposits equal about $3.70 billion, because cumulative deposits of $372.19 billion are almost fully offset by cumulative withdrawals of $368.49 billion. On a per-user basis, that arithmetic yields more than $310,000 of cumulative deposits and about $3.63 million of cumulative volume per user, with volume amounting to roughly 1,178 times net deposits. None of those averages should be treated as representative user behaviour. They are distorted by professional traders, routing bots, repeated deposit/withdraw cycles, market makers and large accounts. What they do show is how capital-efficient the venue is from the platform’s perspective: a relatively modest net capital base can support enormous churn. They also show why cumulative deposits are not the same as TVL and why withdrawal ratios near 99% are not evidence of stress by themselves. They are evidence of users treating the platform as a trading venue, not as a passive balance sheet.

User and capital-flow dashboard from the attached snapshot

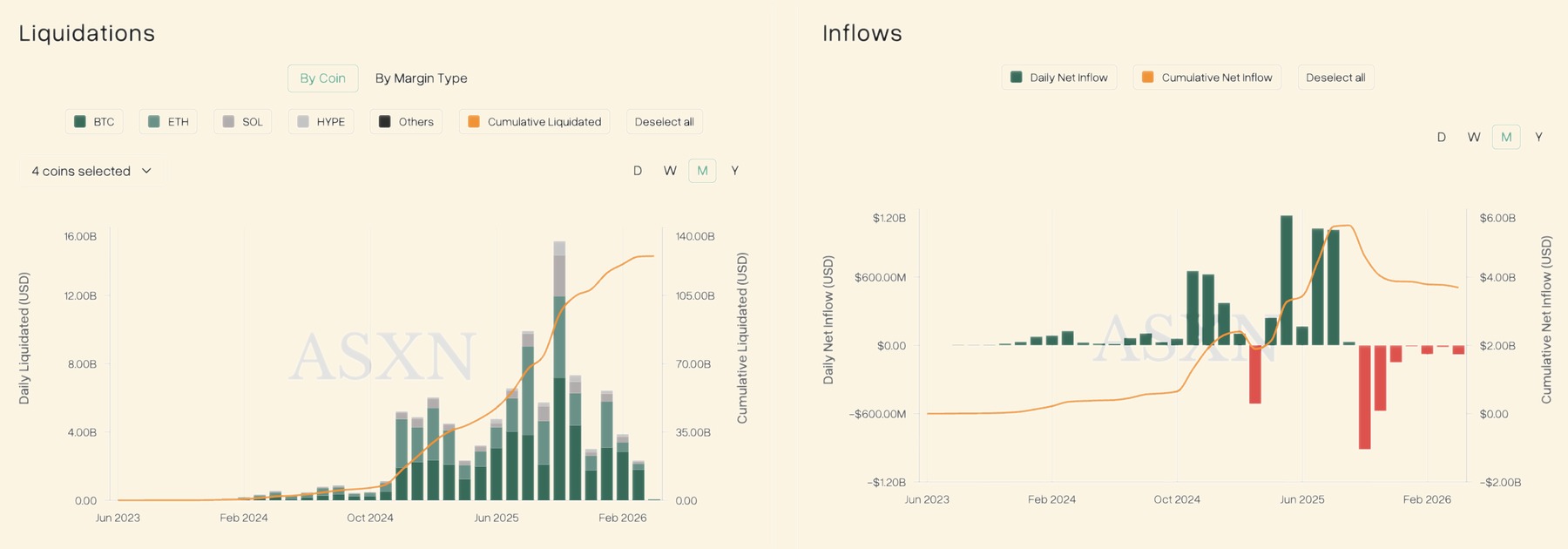

Liquidations and Inflows on Hyperliquid

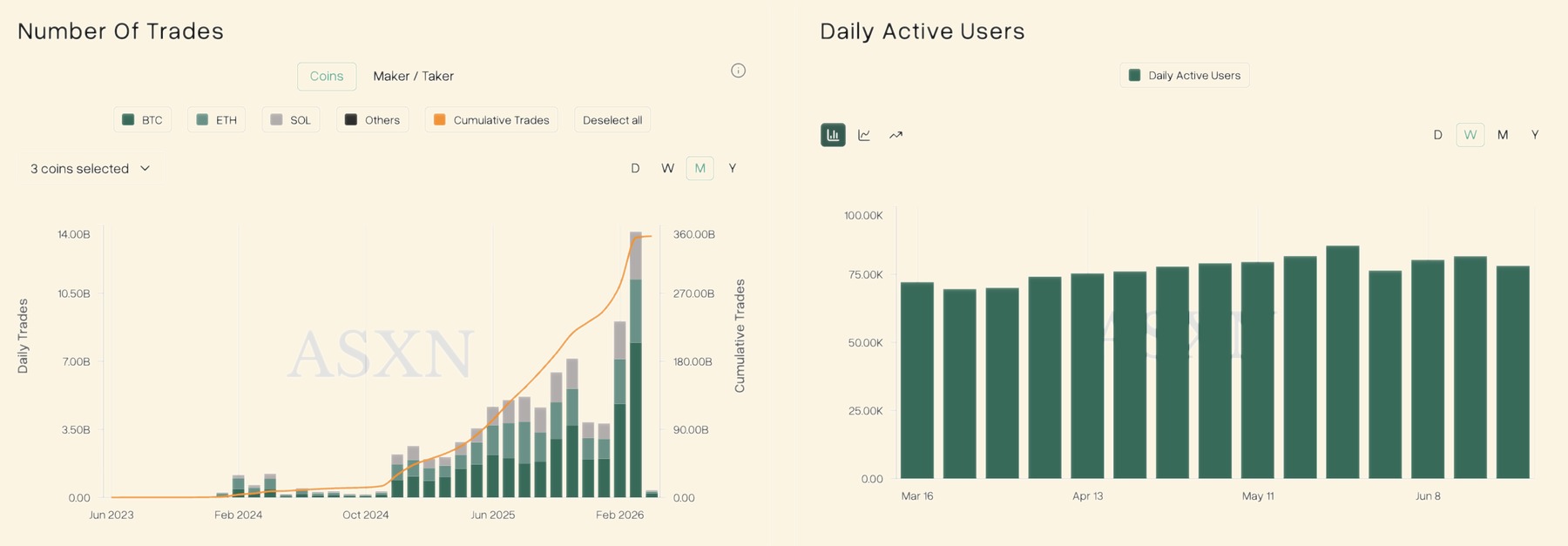

Number Of Trades and Daily Active Users on Hyperliquid

The buyback, purchase and burn story is the least clean part of Hyperliquid’s public economic picture. The dataset shows cumulative protocol revenue and value accrual of $980.65 million, cumulative buybacks of $954.12 million, 27.51 million HYPE purchased, a 45.23 million HYPE Assistance Fund balance, and an annualised buyback figure of $768.55 million versus annualised revenue of $470.35 million. By simple arithmetic, the implied average purchase price is roughly $34.68 per HYPE. But the supply-percentage fields do not reconcile neatly with a one-billion total-supply framing: 27.51 million HYPE equalling 4.53% of total supply implies a denominator of about 607 million, not 1 billion. The most likely explanations are methodological differences in denominator choice, circulating-supply treatment, or a window mismatch between annualised purchase pace and annualised revenue pace. The responsible conclusion is not to force a clean reconciliation where the underlying figures do not yet provide one.

Yan’s own language adds another tension. In February 2026, he repeatedly rejected the idea that Hyperliquid runs a discretionary buyback programme and instead compared the mechanism to Ethereum’s fee burns, describing the fee-to-HYPE conversion as rules-based and embedded in chain logic. That may be directionally true while still leaving open exactly where purchased HYPE is routed across modules. The Assistance Fund balance suggests that at least some HYPE is accumulated in protocol-controlled or protocol-directed form rather than instantly disappearing from circulation. The more precise analytical framing is therefore automated fee conversion and token value accrual, not a management-timed corporate buyback. It should not be assumed that every purchased token is immediately burned unless a more explicit primary reconciliation shows the full flow.

HLP economics must also stay separate from Labs economics. HLP depositors receive the strategy’s economic results, and the quarterly table shows HLP costs as the visible cost line. When HLP loses money, that is not Hyperliquid Labs paying operating expenses. It is the economic cost of the vault function showing up onchain. Likewise, when HLP earns money, that is not the same thing as management fee income for Labs. This is the broader accounting mistake many observers make with Hyperliquid: they translate protocol-level state changes into corporate finance language and then wonder why the categories feel slippery. The categories are slippery because the system was intentionally designed to blur some of the boundaries a shareholder model would normally fix.

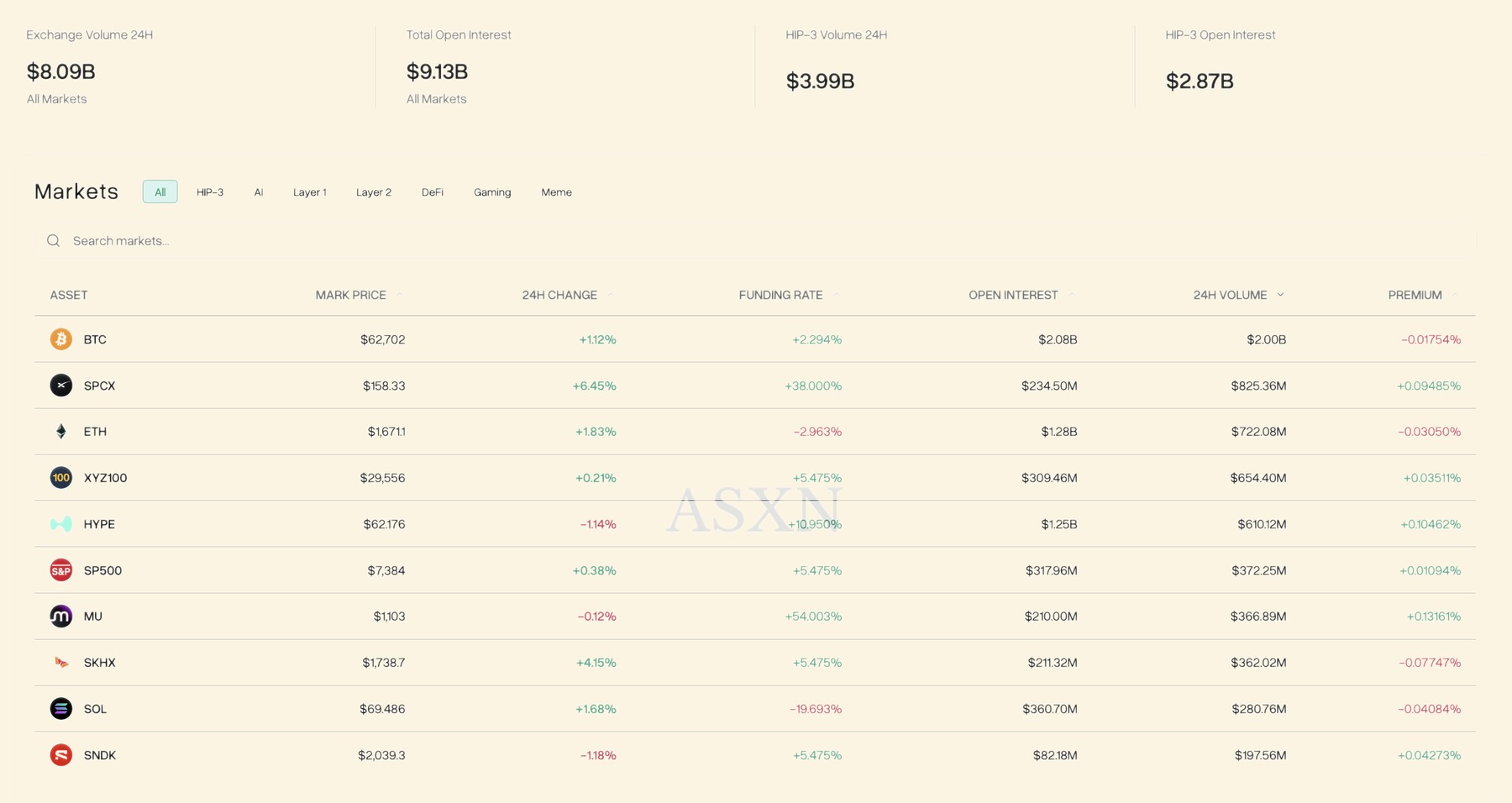

The late-June 24-hour market snapshot offers a useful view of concentration. It shows total exchange volume of $8.90 billion and total open interest of $9.86 billion across all markets, with HIP-3 contributing $3.42 billion of 24-hour volume and $2.97 billion of open interest. That implies HIP-3 accounted for about 38.4% of volume and 30.1% of open interest in the snapshot. Those are large enough shares to matter strategically, but not large enough to say the network has already diversified away from core crypto markets. HIP-3 is no longer marginal. It is not yet the centre of mass.

Top markets by 24-hour volume and open interest

That composition is revealing. BTC and ETH remained the deepest anchors. HYPE itself carried major open interest, which means Hyperliquid’s native token is not only a governance and security asset, but also a prominent speculative instrument inside the venue. SPCX, meanwhile, had a much larger share of volume than of open interest, suggesting fast-turnover speculative price discovery rather than particularly sticky directional positioning. That aligns with June 2026 Wall Street Journal coverage of Hyperliquid’s role in SpaceX pre-IPO and IPO-related speculation. In other words, the SPCX case supports the idea that Hyperliquid can create globally tradable synthetic attention markets for assets that ordinary investors cannot easily access directly. What it does not demonstrate is legally clean tokenised equity ownership. SPCX is a speculative instrument, not a claim on SpaceX shares themselves.

That distinction matters for the broader HIP-3 thesis. The strongest case for HIP-3 is that it is not just new listings. It is a market-creation network that allows specialists to define instruments faster than a centralised exchange committee can. The SpaceX example shows the power of that model in practice. Before and around the IPO, Hyperliquid users could trade a continuous synthetic view on valuation, with the WSJ reporting more than $200 million in 24-hour turnover in the pre-IPO market and more than $1.3 billion in 24-hour turnover once SPCX became one of the exchange’s most-traded assets. That is useful price discovery. But it also exposes the limits. Settlement depends on a synthetic design, not underlying share transfer. Oracle, legal-characterisation and user-understanding risks are materially higher than in an ordinary listed-equity venue. The right verdict on SPCX is that it demonstrates Hyperliquid’s ability to create markets legacy finance does not serve in real time, while also proving that such markets can become economically powerful before they are institutionally tidy.

The microstructure evidence is one of Hyperliquid’s strongest institutional arguments. The June 2026 academic paper “Trading in the Sunshine or in the Shade” studies Hyperliquid’s onchain order book and finds that visible TWAP execution on Hyperliquid tends to face lower execution costs than comparable hidden metaorder execution, with smaller permanent price impact and stronger liquidity provision while the visible order is active. The paper’s deeper implication is subtle: transparency does not reduce trading costs equally for everyone. It appears to benefit those who preannounce through protocol-native visible mechanisms while shifting some adverse-selection burden onto traders who remain hidden. For institutional execution, that is potentially important. Hyperliquid’s transparency is not just a governance virtue. It may alter where informational rents are earned and by whom.

The October 2025 liquidation episode complicates the picture. Colossus reports that over $19 billion in leveraged positions were liquidated across the industry in 24 hours after Trump’s tariff threat, and that Hyperliquid had no downtime and no withdrawal halt. But later academic work argues that Hyperliquid’s ADL queue overused autodeleveraging relative to optimised counterfactual policies. One paper estimates that Hyperliquid’s production queue overutilised ADL by around eight times relative to the authors’ optimal policy, while a related online-learning paper finds large unnecessary haircuts to winning traders, though still suggests Binance’s practices may have been worse. These are working papers rather than regulatory findings, and should be treated accordingly. Even so, they matter because they show that “fully transparent” is not the same as “fully solved”. Hyperliquid’s design makes the trade-offs measurable, which is a major improvement over opaque venues, but measurement can still reveal suboptimal policy.

The employee-productivity story is similarly true and misleading at the same time. The FT reported roughly $960 million of 2025 revenue for Hyperliquid, while Colossus framed the organisation as producing more than $900 million of profit with 11 employees. A naive division gives around $82 million to $87 million of 2025 protocol revenue or profit per core team member; even using a 13-person assumption reduces that only to roughly $69 million to $74 million. Those are astonishing ratios. But they are not corporate productivity ratios in the usual sense because the network’s output depends on validators, market makers, deployers, stablecoin issuers, frontend builders, oracle sources, external researchers and users themselves. The less misleading interpretation is that Hyperliquid Labs is a very small control layer over a much larger economic organism, not that 11 salaried workers alone produced all the platform’s value.

The bottom line on economics, then, is not that Hyperliquid is simply “the most profitable startup per employee on earth”, though that line captures something real about the system’s leverage. The deeper truth is that Hyperliquid has found a way to turn one product, perpetuals, into an unusually efficient engine for bootstrapping adjacent layers: a token, a chain, a builder ecosystem and a market-deployment network. The available data demonstrate that the flywheel is working. They do not demonstrate that the flywheel has yet diversified enough to survive a severe and prolonged decline in leveraged-trading demand. That is the central economic test still ahead.

Competition and historical context

Hyperliquid was built against four reference points rather than against an undifferentiated “market”. BitMEX mattered because it proved perpetuals could become the native crypto derivatives product. Binance mattered because it industrialised scale, liquidity and global reach. FTX mattered because it showed how attractive integrated trading UX could be and how catastrophic opaque custody could become. dYdX and GMX mattered because they were the most serious DeFi attempts at the derivatives problem before Hyperliquid, but each embodied, in Yan’s view, a compromise he did not want to accept: dYdX v3 because the most latency-sensitive part of the venue was still offchain, and GMX because oracle-dependent liquidity did not provide the same market structure as a deep central-limit-order book.

That historical context explains why Hyperliquid was built differently. It did not try to be an AMM with better incentives, an oracle-perps venue with better risk rules, or a hybrid design with more decentralised rhetoric. It treated exchange quality as the core problem and then built a custom execution environment around it. That is the durable competitive advantage if one believes that serious trading liquidity still clusters around visible books, reliable matching and low-friction execution. The June 2026 microstructure work strengthens that argument by showing economic consequences from onchain visibility, not just ideological appeal.

Current competition is more nuanced. Centralised exchanges still dominate globally. U.S.-regulated venues such as Coinbase, Kalshi and ICE now have a policy opening for perpetuals that did not exist before May 2026, and that will matter over time. Among onchain or crypto-native alternatives, dYdX remains historically important, GMX still serves a distinct oracle-based user segment, and newer players such as Aster are trying their own variants of decentralised perpetuals and private or hybrid market design. But Hyperliquid’s combination of liquidity, fully visible book, embedded chain, external deployer model and increasingly non-crypto market catalogue remains unusual. Its most durable moats appear to be liquidity, integrated architecture, brand credibility earned through the no-insider launch, and the early lead in market creation for non-crypto perpetuals. Less durable advantages include pure headline growth, token-market enthusiasm and the assumption that no regulated competitor will eventually offer a sufficiently good perpetuals product.

Risk, regulation and conclusion

The technical and market risks are substantial. Hyperliquid’s own history already demonstrates the fault lines. Colossus describes the March 2025 JELLY incident as a thin-liquidity manipulation that forced validators to intervene and settle at a pre-manipulation price, preserving legitimate users while raising immediate questions about credible neutrality. That is the strongest argument against Hyperliquid’s current decentralisation story: in extremis, a relatively small validator set could and did override the apparent market result. The strongest defence is that doing nothing would have rewarded an attacker exploiting a design hole in a thin market. Both statements can be true at once. The incident showed that Hyperliquid still lives in the uncomfortable space between exchange integrity and neutral protocol finality.

The October 2025 and API-congestion episodes point to a second risk: operational bottlenecks in a high-performance system run by a very small team. Colossus reports several-second latency in API infrastructure during a period of market-maker growth and notes that Yan effectively stopped sleeping while the team rebuilt the relevant servers. The fact that the chain stayed up is a strength. The fact that supporting infrastructure became a material bottleneck is a warning. A venue aspiring to house meaningful financial activity needs not just resilient consensus, but resilient data dissemination, routing and market-access layers. Small teams can move very fast, but they can also become single-threaded in crises.

Governance and decentralisation risk remain open questions rather than solved features. Hyperliquid’s validator set was intentionally small because frequent upgrades are easier to coordinate that way, according to Colossus. That makes engineering sense. It also means the system’s decentralisation is narrower in practice than the rhetoric of neutral rails might imply. Concentrated stake, concentrated validator performance requirements and concentrated cultural authority in the core team may all be acceptable in an early growth phase. They are harder to justify if Hyperliquid wants to present itself as neutral infrastructure for global finance rather than simply a well-run crypto venue.

Economic risk is just as important. Available protocol data show that more than 90% of recent protocol value accrual still derives from perpetuals, and even the platform’s most impressive new use cases, oil, S&P 500 and SpaceX, remain derivative trading stories. If risk appetite falls, if leverage is curtailed, if fees compress, or if liquidity fragments across regulated and unregulated competitors, Hyperliquid’s current economics could look much less extraordinary. HIP-3 helps by broadening the venue’s market catalogue. It does not eliminate the fact that the core cash engine is still leveraged speculation. That is not a moral criticism. It is a business-model fact.

Regulation is the largest external swing factor. The FT reported in late May 2026 that the CFTC’s approval of U.S.-regulated bitcoin perpetuals at Kalshi and Coinbase came after offshore Hyperliquid’s rapid growth had changed the competitive landscape. Reuters then reported that CME sued the CFTC over that approval, arguing that perpetuals should be treated as swaps rather than futures. This dispute is bigger than a fight over a single product. It is a sign that the legal classification of perpetuals is now an active market-structure battleground inside the United States, with incumbents, crypto-native platforms and regulators all trying to shape the terms. For Hyperliquid, that can cut both ways. On one hand, regulated U.S. perpetuals validate the product category Hyperliquid helped popularise. On the other, they create domestic competition and a clearer route for institutional users to avoid offshore or geofenced venues.

The same is true for outcome markets and synthetic traditional-asset exposure. Hyperliquid may benefit from being early, but that breadth invites more legal scrutiny around licensing, market abuse, commodities versus securities classification, and what kinds of event-linked products will be tolerated on permissionless rails. The June 2026 WSJ coverage that celebrated Hyperliquid’s range, from oil to SpaceX to outcome-style products, is also the reason the venue is hard to fit into one existing legal box. That ambiguity is currently a growth advantage. Over a longer horizon, it could become a drag or force the ecosystem into stronger interface-level compliance and geofencing.

No high-quality public postmortem or press report appears to indicate that the 20 June 2026 L1 network upgrade was an outage or exploit. It should therefore be treated as scheduled maintenance unless stronger evidence emerges. That distinction matters because Hyperliquid is now prominent enough for routine upgrades, market launches and genuine stress events to blur together in secondary commentary. Research quality depends on not collapsing those categories.

The conclusion is therefore mixed, and that is what makes Hyperliquid analytically interesting. It has already proven five big things. It has proven that an onchain order-book venue can become economically important. It has proven that a small, self-funded team can build something that venture-backed rivals and incumbents must respond to. It has proven that a token launch can function as genuine ownership transfer rather than mere exit liquidity for insiders. It has proven that external builders can contribute meaningful business lines, especially through HIP-3. And it has proven that perpetuals are not just a crypto niche but a broader financial product category now forcing action from regulators and incumbents alike.

What remains unproven is just as important. Hyperliquid has not yet shown that its economics can meaningfully diversify beyond high-turnover leveraged trading. It has not shown that the validator and governance structure can scale toward stronger neutrality without harming performance. It has not shown that outcome markets or options will become durable product lines rather than narrative extensions. It has not resolved the full tension between protocol ideology and crisis intervention. And it has not shown how a system designed to be outside conventional corporate categories will navigate a world in which conventional regulators, courts and institutional allocators increasingly care about exactly those categories.

So is the real product an exchange, a blockchain, a liquidity layer, a market-creation network or a financial operating system? As of mid-2026, the most accurate answer is that it is an exchange-funded financial network. The exchange still pays the bills, in protocol terms. The chain makes the exchange defensible and composable. HIP-3 turns it into a market-creation layer. HyperEVM gives it a plausible application surface. If the thesis is right, by 2028 or 2030 Hyperliquid should show three things: first, a materially larger share of non-crypto and non-perps activity; second, a broader and more independent builder economy; and third, a governance and security model that looks credibly neutral outside the founder’s shadow. If the thesis is wrong, Hyperliquid will still matter, but mainly as the best-designed leveraged-trading platform of its era rather than as infrastructure for global finance. The evidence available today supports respect for the first possibility and real caution about assuming it has already arrived.

Sources

- https://colossus.com/article/beyond-the-sky-jeffrey-yan-hyperliquid/

- https://hyperscreener.asxn.xyz/

- https://www.ft.com/content/7aeef922-6d26-4a65-97b1-751c36440bf0

- https://www.wsj.com/finance/currencies/this-crypto-trading-platform-is-emerging-as-wall-streets-convenience-store-012e050c

- https://arxiv.org/abs/2512.01112

- https://arxiv.org/abs/2606.15715

Partner Highlight

At insights4vc, we pay attention to teams that are not just shipping products, but shaping categories.

Moto is one of them. The company is building a premium card experience positioned as an alternative to traditional incumbents such as Amex, combining a high-end user interface with more modern financial infrastructure.

Moto is currently expanding access to a limited testing group. If you would like to test the product please contact us at: [email protected]

Cover Artwork

Farmers and their herd near a fountain in front of a panoramic landscape

Francesco Zuccarelli, R.A. c. 1702–1788

Risk Disclaimer:

insights4.vc and its newsletter provide research and information for educational purposes only and should not be taken as any form of professional advice. We do not advocate for any investment actions, including buying, selling, or holding digital assets.

The content reflects only the writer’s views and not financial advice. Please conduct your own due diligence before engaging with digital assets or related technologies, as they carry high risks and values can fluctuate significantly.