Switzerland’s role in digital assets is often misread as a story of early crypto friendliness. The more important story is institutional sequencing. Before most jurisdictions had settled the legal status of tokens, Switzerland had already provided protocol foundations, supervised crypto banks, tokenised securities law, DLT market infrastructure, and live experiments in digital Swiss-franc settlement.

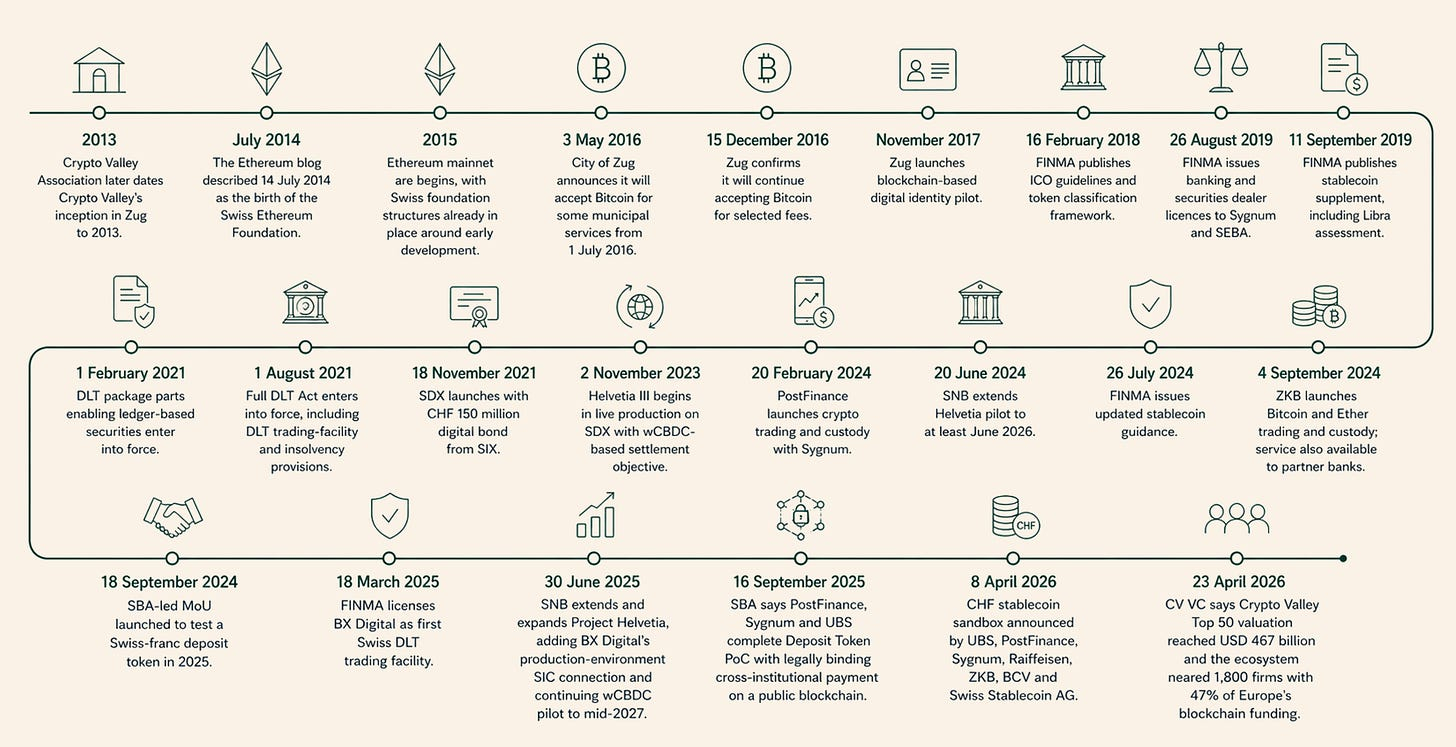

The first institutional layer was the rise of Zug as Crypto Valley. Zug’s low-tax, business-friendly environment, decentralised Swiss politics, and unusually accessible local government made it attractive to globally distributed early-stage blockchain teams. The city’s acceptance of Bitcoin for certain municipal services from July 2016, followed by experiments such as blockchain-based digital identity, gave symbolic and practical evidence that Swiss public authorities were willing to engage early with the technology rather than treat it as a fringe anomaly.

The second layer was the foundation model. Early protocol ecosystems needed more than code and communities. They needed legal entities that could hold assets, contract with developers and vendors, manage grants, and provide governance credibility to external counterparties. Switzerland’s foundation structures proved unusually well suited to that need. The best-known case remains the Ethereum Foundation, whose Swiss foundation structure became part of the institutional scaffolding around Ethereum’s early development and token sale. Switzerland did not create Ethereum’s success, but it provided a credible legal home for part of the early protocol era.

The third layer, and the most important for 2026, is regulated financial infrastructure. Switzerland’s real edge was clarity. FINMA moved early on token classification in 2018, clarified stablecoin treatment in 2019 and again in 2024, and coupled openness with strict anti-money-laundering expectations. In 2019 it granted banking and securities dealer licences to two pure-play blockchain institutions, and in 2025 it licensed the first Swiss DLT trading facility. In other words, Switzerland was not an offshore workaround. It was an early attempt to fit crypto inside financial law.

That legal clarity mattered because it enabled banks and market infrastructures to build. The country’s regulated digital-asset stack now includes institutions such as Sygnum Bank, AMINA Bank, Crypto Finance and Taurus, alongside mainstream bank distribution from PostFinance and Zürcher Kantonalbank. PostFinance launched regulated crypto trading and custody in February 2024, while ZKB added integrated Bitcoin and Ether trading and custody in September 2024. Those moves mattered because they shifted digital assets from specialist platforms towards ordinary Swiss banking channels.

Institutionalisation has also pushed Switzerland beyond crypto-assets and towards tokenised capital markets. SIX Digital Exchange launched with a CHF 150 million digital bond in 2021 and had passed CHF 1 billion in digital-asset issuance by May 2024. The Swiss National Bank has used Project Helvetia to test settlement of tokenised securities in wholesale CBDC on SDX, while in 2025 it expanded the programme to include an RTGS-link model for BX Digital via the Swiss Interbank Clearing system. This makes Switzerland important not only to crypto firms, but also to bond issuers, custodians, exchanges, and post-trade operators.

Switzerland’s second crypto moment

By 2026, the most interesting Swiss digital-asset story is no longer whether Zug helped legitimise early crypto networks. It is whether Switzerland is becoming the first major financial centre to run a coherent stack that links tokenised assets, regulated custodians, banking distribution, DLT trading venues, programmable commercial-bank money and central-bank settlement. The April 2026 CHF stablecoin sandbox, the 2025 Deposit Token proof of concept, the continuing expansion of Project Helvetia, FINMA’s licensing of BX Digital, SDX’s digital-bond activity, and mainstream bank launches from PostFinance and ZKB all point in the same direction. Crypto in Switzerland is moving from perimeter experimentation into the plumbing of finance.

That matters because the institutional questions have changed. The first cycle asked whether tokens could exist, whether specific blockchain networks could raise funds, and whether regulated entities could touch crypto at all. The current cycle asks different questions: how should tokenised bonds settle, what form of Swiss-franc digital money is fit for which use case, and what mixture of public and private infrastructures is credible enough for institutional scale. Switzerland is not the only jurisdiction asking those questions, but it is one of the few where they are already being tested simultaneously in production-like environments.

The country’s importance therefore lies less in size than in sequencing. Switzerland established early legal wrappers for protocols; then it allowed specialist crypto banks and service providers to become supervised institutions; then it adapted securities and market-infrastructure law; and now it is testing tokenised money forms that could support settlements, corporate treasury flows and tokenised asset markets. That sequencing matters because each layer built on the credibility of the prior one. The result is not a single Swiss model, but an institutional pathway from foundations to banking to market infrastructure.

Why Zug became Crypto Valley

Zug became Crypto Valley because early blockchain teams needed more than cheap office space. They needed speed, legal certainty and a local administration that could be reached and persuaded. The Crypto Valley Association’s own explanation remains instructive: Zug benefits from a decentralised Swiss political system, a pro-business philosophy, low taxes, and easy accessibility of local government. In a sector where many projects were still trying to work out what kind of legal thing they were, that combination mattered.

Public signals reinforced private clustering. On 3 May 2016, the city announced that it would accept Bitcoin for certain municipal services from 1 July 2016, initially up to CHF 200. Later that year it decided to continue the arrangement. In 2017 the city moved beyond symbolism and launched a blockchain-based digital identity pilot, and in 2018 it ran a blockchain-based consultative vote. None of those pilots created a mass retail blockchain economy, but they did something more important for an emerging cluster: they signalled that local authorities were willing to learn by doing.

Zug’s rise also had a path-dependent quality. Once one or two visible projects settled there, others found it easier to do the same. Lawyers, service providers, fiduciaries, accountants and bankers learned the category. Entrepreneurs found peers, investors and advisors already on the ground. In game-theoretic terms, Zug became a coordination point because enough early actors believed other actors would also recognise it as one. That is the deeper meaning of Crypto Valley: it was not simply a place with good marketing; it became a shared answer to the question of where a legally ambiguous global protocol should stand institutionally.

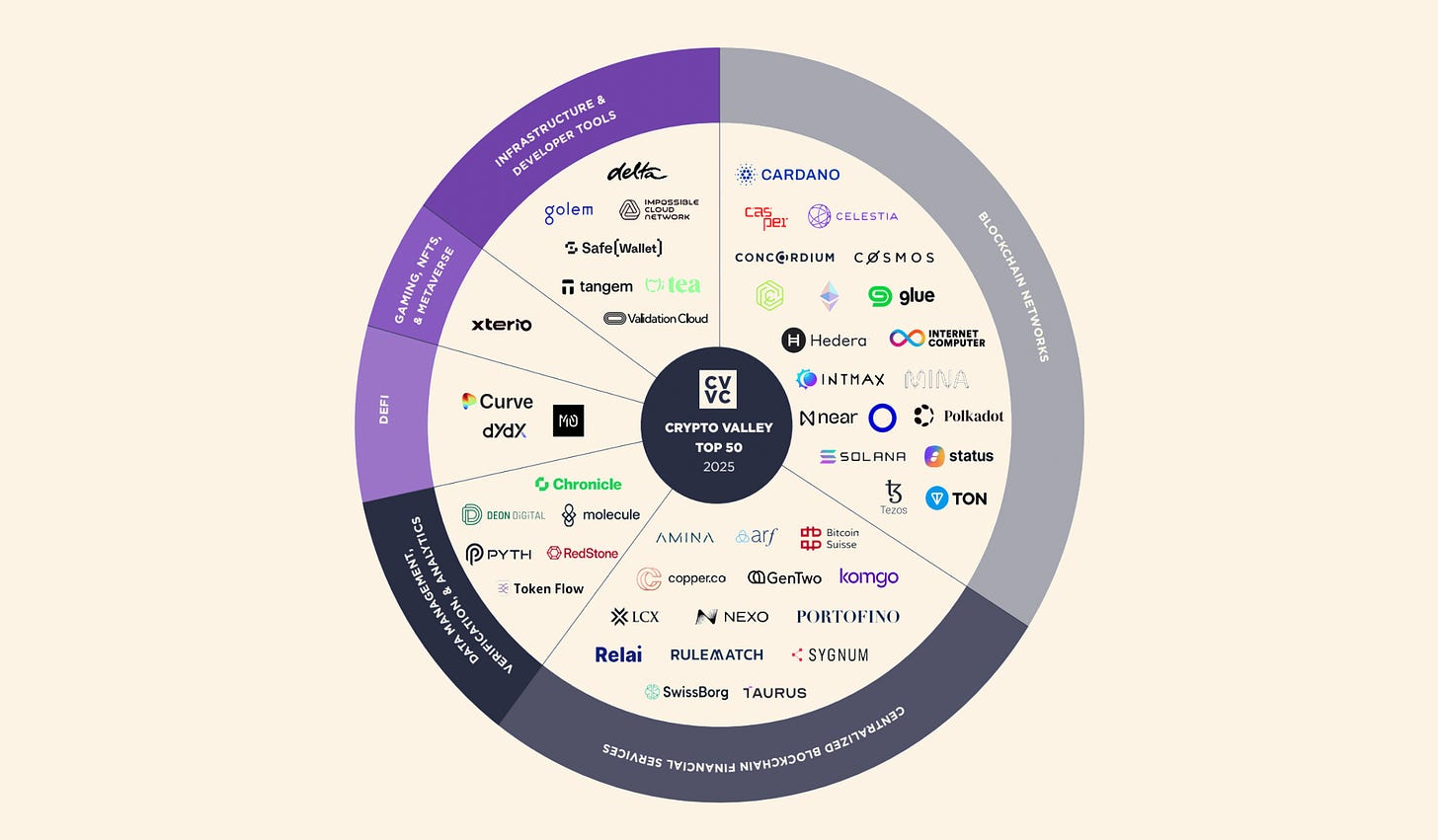

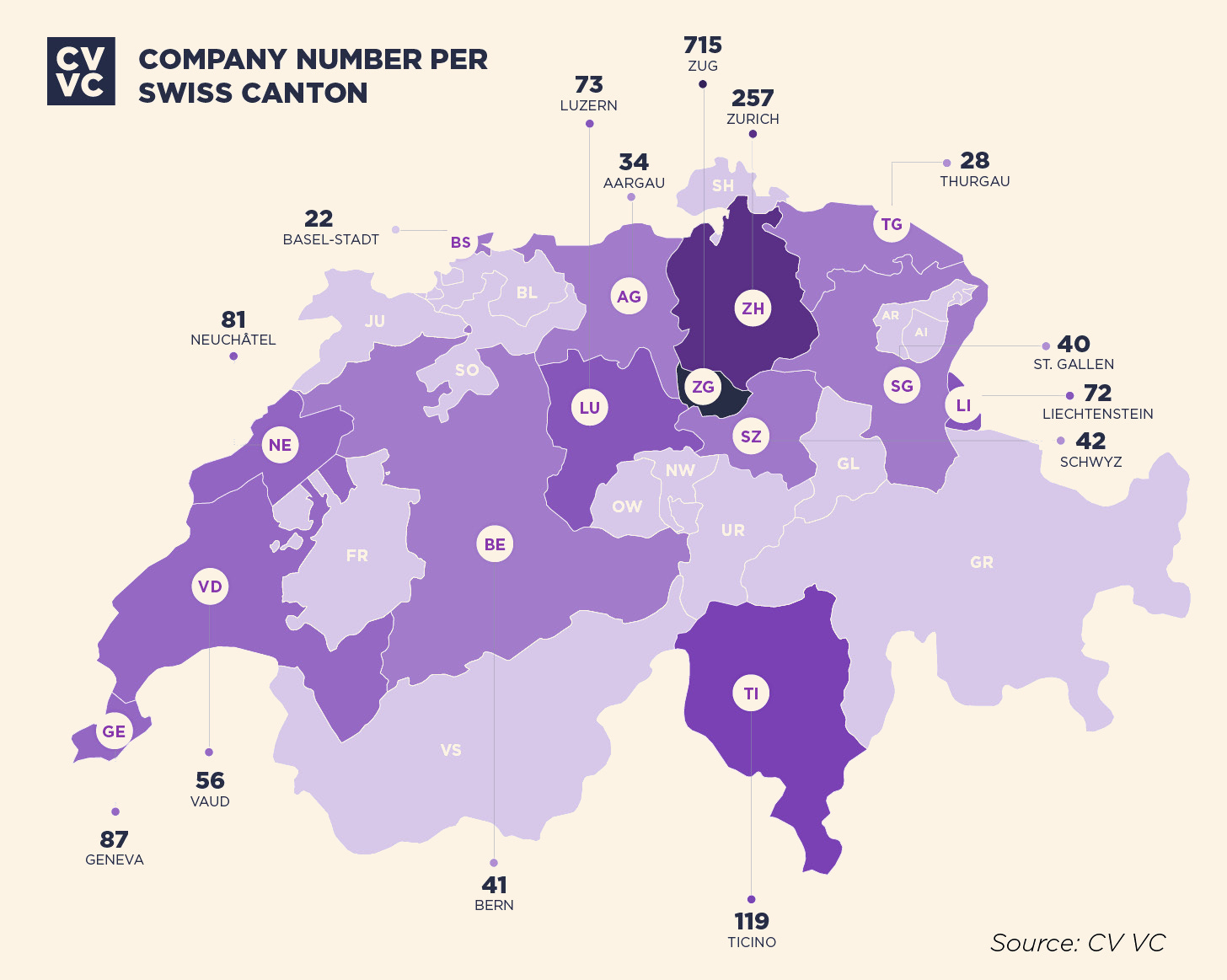

The cluster eventually broadened beyond Zug. CV VC’s 2025 company report counted 1,749 active blockchain companies across Switzerland and Liechtenstein, with Zug still the nucleus at 41 percent and Zurich second at 15 percent. By April 2026, CV VC said Crypto Valley was nearing 1,800 firms and capturing 47 percent of European blockchain funding. In other words, Zug was the ignition point, but the Swiss ecosystem had become national in reach.

Ethereum, foundations and legal wrappers

The early protocol era needed legal wrappers because protocol communities, however decentralised in theory, still had to interact with the off-chain world. Someone had to receive proceeds from token sales, sign employment and vendor contracts, run grant programs, pay taxes, defend trademarks and speak to banks. Swiss foundations were well suited to this because they offered a recognisable non-profit form with institutional credibility and a degree of governance neutrality relative to a conventional operating company.

Ethereum is the clearest example. The Ethereum blog described 14 July 2014 as “the birth of the Swiss Ethereum Foundation”, and the Ethereum Foundation’s current legal disclosures identify Stiftung Ethereum as a Swiss Stiftung in Zug.

The Swiss foundation did not encompass the whole Ethereum project, which was always broader than any one entity, but it did provide a legally recognised hub for early development funding and ecosystem support.

The significance of that model extended beyond Ethereum. By 2017 Swiss reporting was already describing the proliferation of token-related foundations in Zug, including projects such as Tezos, and raising questions about how large on-chain treasuries should be governed. That debate itself is evidence of a broader point: Switzerland became a place where the governance problem of crypto could be formalised. The country did not solve every governance problem. But it gave protocol teams a jurisdiction where governance could at least be expressed through known legal forms rather than improvised entirely in cyberspace.

Institutionally, this was crucial. The distinction between protocol and legal entity allowed Switzerland to host part of the governance layer without implying that any Swiss entity “owned” the network in the corporate sense. That separation appealed to projects that wanted legal credibility without abandoning the rhetoric and structure of open-source decentralisation. It is one reason Switzerland attracted protocol foundations in the first place. The country did not offer a blank cheque. It offered a compromise between decentralised aspiration and institutional necessity.

Regulation as product-market fit

Switzerland’s real advantage was regulatory clarity. FINMA’s 2018 ICO guidelines did something more important than simply bless fundraising: they turned token ambiguity into categories. Payment tokens, utility tokens and asset tokens were separated by economic function and transferability, with hybrid forms explicitly acknowledged. Payment tokens triggered AML obligations, utility tokens escaped securities treatment only if they were immediately consumptive, and asset tokens were treated as securities. That taxonomy gave projects and their advisors a usable map.

The Swiss approach was not laissez-faire. FINMA stressed from the start that blockchain projects could not “circumvent the tried and tested regulatory framework”. In 2019, in its well-known Libra assessment, it signalled that a large Swiss stablecoin-style arrangement would likely require a payment-system licence under FMIA, and that “same risks, same rules” would apply, including additional requirements for bank-like risks. That is a strong clue to how Switzerland thought about digital assets: not as a parallel legal universe, but as new technology entering existing categories with adapted rules where necessary.

AML policy shows even more clearly why Switzerland should not be described as merely light-touch. In August 2019 FINMA said its supervised institutions were only permitted to send tokens to, and receive them from, external wallets belonging to their own verified customers where sender and recipient information could not otherwise be transmitted reliably. FINMA explicitly noted that this Swiss practice went beyond the FATF standard and was among the most stringent in the world. That is not permissiveness. It is early adaptation combined with supervisory conservatism.

The same pattern appears in stablecoins. FINMA’s 2019 supplement already noted that stablecoins could trigger banking, fund-management, securities or infrastructure rules depending on reserve assets and claim structures. Its 2024 guidance then addressed default guarantees, stablecoin-related banking-law workarounds and heightened money-laundering risks. Switzerland’s edge, therefore, was not the absence of boundaries. It was the fact that boundaries were drawn comparatively early, with enough precision that legitimate firms could build against them. That is why “regulation as product-market fit” is a more accurate description than “friendliness”.

The DLT Act and tokenised asset law

The DLT Act was the legal hinge between Switzerland’s first crypto chapter and its current infrastructure chapter. In December 2020 the Federal Council brought into force, from 1 February 2021, the parts of the legislative package enabling ledger-based securities. The remaining package, including the provisions for DLT trading facilities and insolvency clarifications, entered fully into force on 1 August 2021. Official Swiss government materials describe the package as creating legal certainty for tokenised assets and trading venues.

Two elements mattered most. First, the law gave a secure legal basis for rights to be registered and transferred through electronic registers, creating the concept of ledger-based securities. Second, it clarified the segregation of crypto-based assets in bankruptcy, which is critical for custody and investor protection. Those changes pushed tokenisation out of the realm of clever contractual workarounds and into the domain of recognised property and market-infrastructure law.

The DLT Act also created a new authorisation category for DLT trading facilities. This was not cosmetic. It acknowledged that tokenised markets can combine elements that the traditional market structure often separates: multilateral trading, settlement and aspects of custody or downstream post-trade processing. FINMA’s 2025 licensing of BX Digital shows that the category was not merely theoretical. It became the basis for a new regulated venue under Swiss law.

The Swiss version of legal adaptation was unusually targeted. Rather than writing a single omnibus crypto rulebook covering every token business model, Switzerland modified the relevant civil, insolvency and market-infrastructure statutes so tokenised assets could fit cleanly into existing parts of private and public law. That makes the DLT Act central to the institutional story. It is the bridge from token issuance as an exceptional activity to tokenised securities as a legally grounded capital-markets activity.

The rise of regulated crypto banks

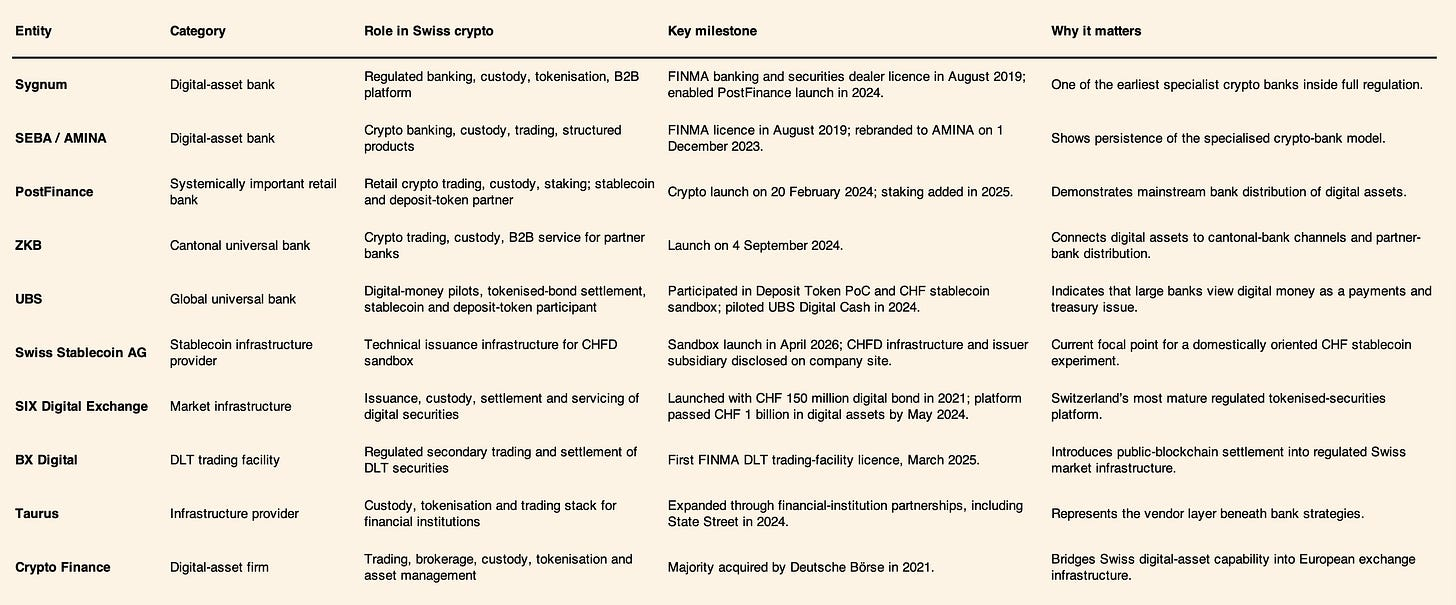

Switzerland was among the first jurisdictions where crypto-native institutions could obtain genuine banking status rather than operate permanently in the shadow of banks. In August 2019 FINMA said it had issued banking and securities dealer licences to two pure-play blockchain service providers, SEBA Crypto in Zug and Sygnum in Zurich, for services to institutional and professional clients. That decision was a major signal to the market: digital-asset banking could be a supervised category rather than a tolerated edge case.

Since then, that first generation has matured into a broader institutional layer. Sygnum describes itself as a regulated digital-asset banking group with services spanning banking, asset management, tokenisation and B2B banking. AMINA, formerly SEBA, rebranded in December 2023 but remains one of the core Swiss crypto-bank franchises. Crypto Finance, founded in 2017 and later majority-acquired by Deutsche Börse, operates under consolidated FINMA supervision and offers trading, storage, tokenisation and asset-management services to professional and institutional clients. Taurus has taken a different route, providing custody, tokenisation and trading infrastructure to financial institutions rather than building itself as a bank.

This layer matters because it created specialised competence inside the regulated perimeter. Instead of forcing every Swiss bank to build crypto expertise from scratch, Switzerland produced a set of institutional intermediaries that could supply custody, trading, tokenisation and compliance capabilities to the broader market. Sygnum’s B2B platform is the clearest example, acting as the infrastructure behind other banks’ launches. Crypto Finance plays a similar intermediation role via execution and market connectivity. Taurus represents the infrastructure-vendor model. Together, these firms helped bridge native crypto markets and traditional institutions without pretending the two were already the same thing.

The deeper point is that Swiss crypto banking was not only about letting specialised banks exist. It was about creating institutional middleware. That is why the sector’s importance cannot be judged solely by retail volumes or token listings. Its real contribution has been to make digital assets operable for private banks, cantonal banks, brokers, asset managers and tokenised-securities issuers. This is where Switzerland’s early legal precision became economically productive.

Traditional Swiss banks enter crypto

Mainstream bank adoption is where Switzerland’s digital-asset story begins to matter for scale. When PostFinance launched its crypto offering in February 2024, it did more than add a new product category. According to Sygnum, the service made PostFinance the first systemically important Swiss bank to launch regulated trading and custody for cryptocurrencies, initially offering access to 11 tokens and integrating the service through Sygnum’s B2B banking platform. That move brought digital assets into the interface of a mass-market institution with 2.5 million customers.

PostFinance then widened the proposition. By early 2025 it had added Ethereum staking, and by mid-2025 its range included sixteen cryptocurrencies. The bank has also indicated ambitions to extend relevant services to corporate customers. This is significant not because staking itself is the decisive institutional product, but because it shows the shift from one-off experimentation to iterative product integration inside a major Swiss bank.

ZKB’s September 2024 launch was important for a different reason. The bank enabled integrated trading and custody for Bitcoin and Ether through its existing digital channels, while also making the service available to partner banks on a B2B basis. ZKB handles custody itself, while order execution is routed via Crypto Finance. That model illustrates how specialist digital-asset firms and universal banks can combine: the bank keeps the client relationship and custody control, while external specialists supply execution or infrastructure where appropriate.

UBS is relevant less as a retail crypto gateway and more as an infrastructure actor. It participated in Project Helvetia transactions, in the Deposit Token proof of concept, in the April 2026 CHF stablecoin sandbox, and in late 2024 it piloted UBS Digital Cash, a private blockchain-based payment system for domestic Swiss-franc and cross-border transactions. Together these steps suggest that the most strategically important bank-led digital-money initiatives may emerge first in payments, settlement and treasury rather than in consumer-facing crypto brokerage.

Tokenised securities and market infrastructure

Tokenised securities in Switzerland are no longer a thought experiment. SIX launched SDX in November 2021 with a CHF 150 million senior unsecured digital bond, structured with both a digital and a traditional tranche to connect the two worlds. By May 2024, SIX said SDX had passed CHF 1 billion in digital assets on the platform. The design choice has been consistent throughout: digital securities should remain usable by the existing investor base, not be isolated in a parallel market.

That integration logic matters. SDX has been built as regulated market infrastructure rather than as an exchange-style crypto experiment. SIX notes that digital bonds issued on SDX have ISINs, can sit in traditional central securities depositories, can be traded on established exchanges and, where eligible, can enter the Swiss Bond Index and the SNB’s general collateral basket. This explains why tokenised securities in Switzerland should be read as a capital-markets story as much as a crypto story. The ambition is not to replace the regulated securities market with tokens; it is to tokenise parts of the securities market without breaking the institutions around it.

Project Helvetia deepens that logic by connecting tokenised securities with central-bank settlement. Since the end of 2023 the SNB has provided wholesale CBDC on SDX for real-value settlement of tokenised transactions, and in 2024 it issued digital SNB Bills on SDX settled in wholesale CBDC. The pilot was extended at least to June 2026 and later to mid-2027. The message is that tokenised securities become far more institutionally credible when the cash leg is solved inside a trusted settlement framework.

BX Digital represents a second infrastructure path. FINMA licensed it in March 2025 as the first DLT trading facility in Switzerland. Unlike SDX, BX Digital uses a public blockchain, Ethereum, for the asset leg, while ensuring delivery-versus-payment via a connection to SIC and smart-contract logic. That creates a different model of regulated tokenised market infrastructure: closer to public-chain settlement, but still anchored to existing Swiss payment systems and supervised participants. The coexistence of SDX and BX Digital is important. Switzerland is testing more than one architecture for the same future market question.

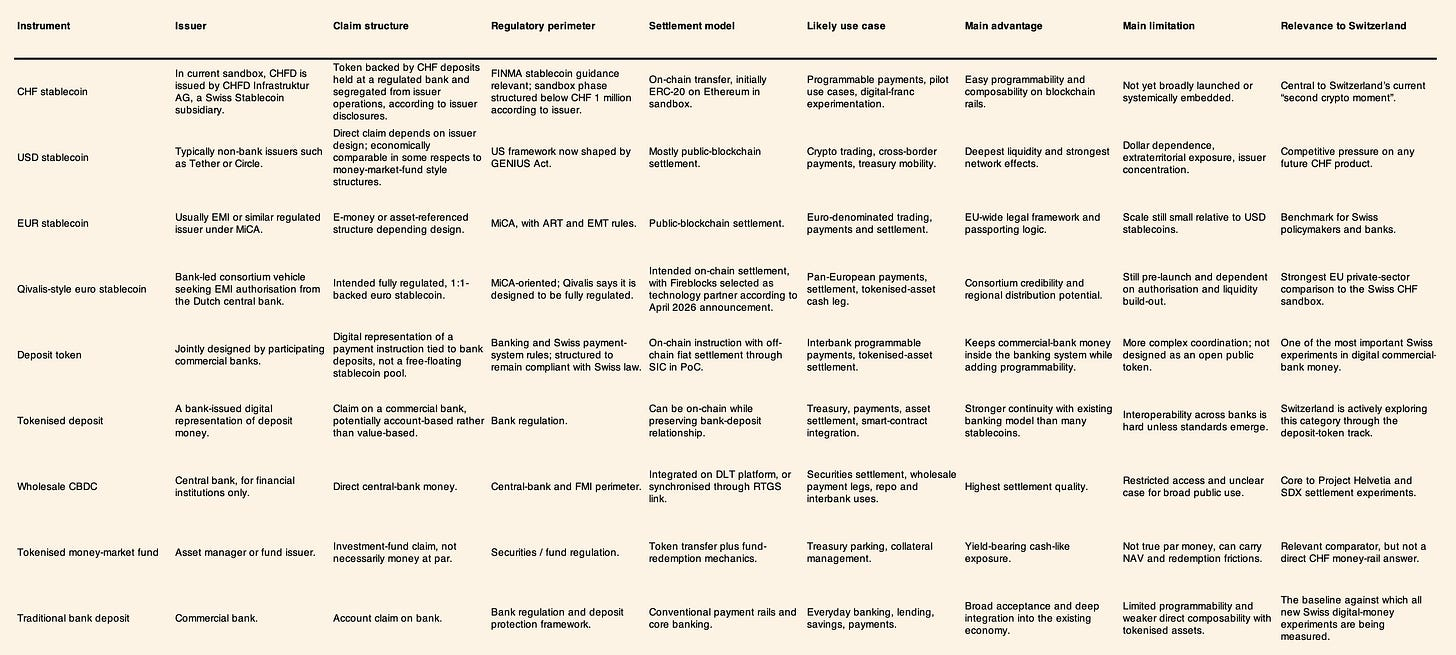

The digital money stack

Switzerland’s newest institutional question is not whether digital money will exist, but which forms of digital money belong where. Stablecoins, deposit tokens, tokenised deposits and wholesale CBDC are often discussed interchangeably, but they embed different claims, issuers, legal structures and settlement models. Switzerland’s importance in 2026 is precisely that it is testing several of these in parallel instead of betting on a single winner.

Start with the April 2026 CHF stablecoin sandbox. Official announcements from UBS, PostFinance and others say the sandbox involves UBS, PostFinance, Sygnum, Raiffeisen, ZKB, BCV and Swiss Stablecoin AG. The partners are testing potential use cases for a Swiss-franc stablecoin in a controlled live environment during 2026, with Swiss Stablecoin AG supplying the technical issuance infrastructure. The banks’ own statement is careful: Switzerland currently has no regulated Swiss-franc stablecoin with broad domestic application. In other words, the initiative is exploratory, not yet a launched national money layer.

The Swiss Stablecoin side adds an important nuance. According to Swiss Stablecoin AG, the sandbox token is CHFD, issued and redeemed by its wholly owned subsidiary CHFD Infrastruktur AG, which is affiliated with a FINMA-recognised self-regulatory organisation. The company says the architecture is blockchain-agnostic, but the sandbox initially runs on Ethereum as an ERC‑20 token. It also says circulation will be kept below CHF 1 million during the sandbox phase so the project can rely on Swiss fintech-sandbox exemptions without a bank guarantee. The stablecoins are described as fully backed by Swiss-franc deposits held at a regulated Swiss bank and segregated from the issuer’s operating funds. The careful wording matters: this is not yet “bank-issued money” in the narrow sense of a token minted directly as a bank liability by the participating banks. It is better understood, at this stage, as an institutionally backed test of a CHF stablecoin infrastructure.

The Deposit Token proof of concept is different. In September 2025 the Swiss Bankers Association said PostFinance, Sygnum and UBS had completed a feasibility study that, for the first time, executed a legally binding payment across institutions using bank deposits and a public blockchain. The results report explains that the PoC used an account-based model in which on-chain tokens represented payment instructions that triggered off-chain movements of fiat through SIC. Legally, the design was framed as a digital representation of a payment instruction rather than as a new bearer-like claim instrument. In plain English, the Deposit Token was not trying to create a transferable stablecoin-like pool of CHF claims for the public. It was testing how interbank-compliant, programmable commercial-bank money could function on blockchain rails while the actual deposit settlement remained anchored in banking infrastructure.

Wholesale CBDC is different again. Project Helvetia’s first approach places tokenised central-bank money on the same DLT infrastructure as tokenised assets, allowing integrated delivery-versus-payment on SDX. The second approach uses traditional central-bank money via an RTGS link to SIC, synchronising asset and cash settlement across systems. The SNB’s 2025 annual report also describes a third approach it analysed conceptually: private token money that is bankruptcy-protected and backed by central-bank money. Switzerland is therefore sketching a layered digital-money stack. Retail or quasi-retail use cases may suit regulated stablecoins; interbank and programmable payment use cases may favour deposit-token or tokenised-deposit structures; and securities-settlement use cases may rely on either integrated wholesale CBDC or synchronised central-bank money. The lesson is not convergence on one instrument. It is coexistence by function.

Lugano as a secondary cluster

Lugano should not be confused with Zug’s role, but it deserves a separate place in the Swiss story. If Zug was the foundation-and-protocol cluster and Zurich became the banking-and-infrastructure centre, Lugano has positioned itself as the city-level adoption experiment. Through Plan ₿, a joint initiative with Tether, Lugano has promoted payments in Bitcoin, USDT and LVGA, along with education, events and relocation incentives. City materials say the second phase of the initiative was formalised on 3 March 2026 and runs through 2030.

The numbers are non-trivial but should be handled carefully. Lugano says Plan ₿ has enabled more than 400 merchants to accept LVGA, BTC and USDT, while the city’s MyLugano platform describes LVGA as a local blockchain-based payment token used for cashback and local spending incentives.

The March 2026 city release also credited the initiative with helping attract more than 100 fintech and blockchain companies and noted the introduction of digital bonds and some municipal-payment options in digital currencies. These are meaningful signals of municipal experimentation, though not evidence that Lugano has become the centre of Swiss institutional digital finance.

What Lugano adds is a different institutional layer: political branding, merchant acceptance and local digital-economy experimentation. It shows that the Swiss model is not only about prudential regulation and wholesale settlement. But it also shows the limits of city-led narratives. Merchant adoption and Bitcoin-friendly branding are part of the ecosystem; they are not the core reason Switzerland matters to global institutional capital. In that sense, Lugano is best understood as a complementary case study, not the main thesis.

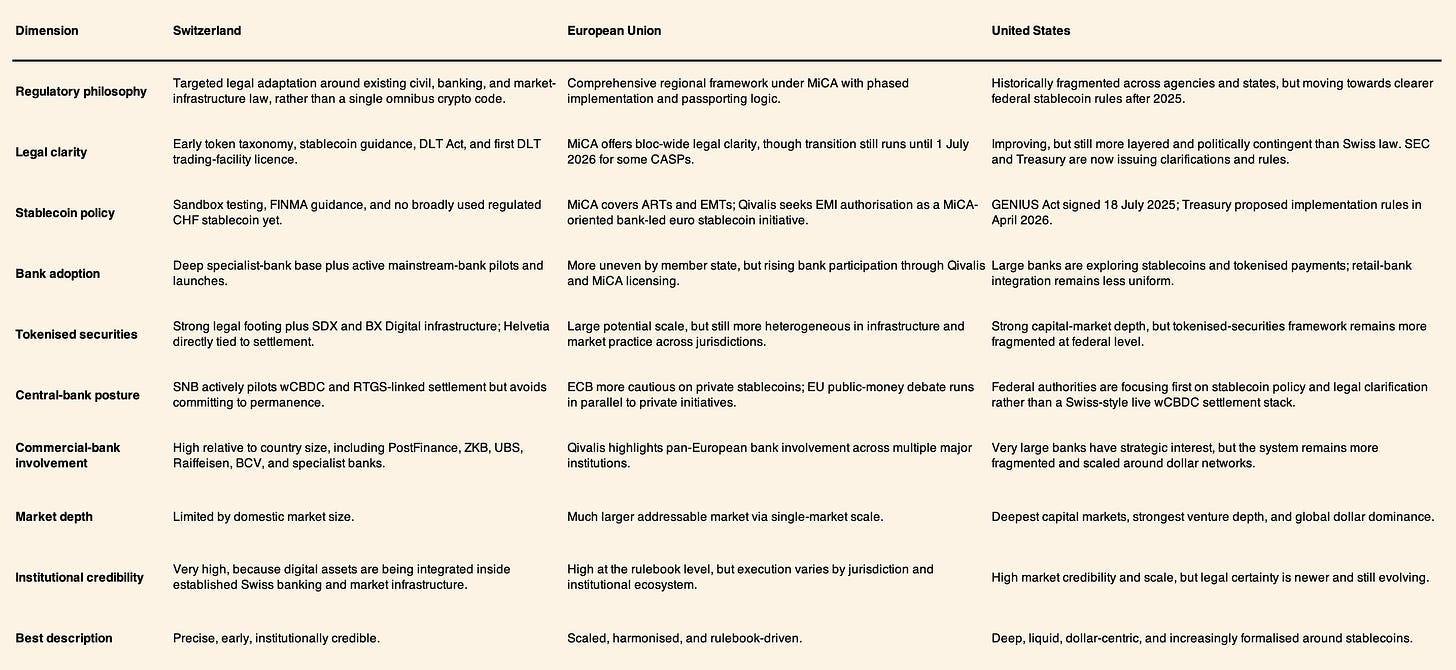

Switzerland, the EU and the US

The best comparison is not “who is ahead”, but how institutional adaptation is being sequenced. In the European Union, MiCA has given the bloc a comprehensive regional rulebook. Stablecoin-related provisions applied from 30 June 2024, and MiCA applied fully from 30 December 2024. ESMA said in April 2026 that the remaining transitional period for legacy CASPs would expire on 1 July 2026. The EU therefore has scale and harmonisation that Switzerland cannot match, even if it lacks Switzerland’s density and historical first-mover advantage.

Qivalis is the clearest private-sector euro comparison point. Its own website describes a fully regulated, 1:1-backed euro stablecoin project backed by leading European banks. Reuters reported in December 2025 that the Amsterdam-based venture, formed by major banks including ING, UniCredit, BNP Paribas and others, was seeking authorisation as an electronic money institution from the Dutch central bank and targeting a 2026 launch.

ING and CaixaBank have also referenced Qivalis as a bank-led euro stablecoin initiative, and Fireblocks said in April 2026 that it had been selected as infrastructure partner for the planned MiCA-compliant launch in the second half of 2026. Compared with the Swiss CHF sandbox, Qivalis is more explicitly pan-European, more directly shaped by MiCA, and larger in potential distribution reach. Switzerland’s sandbox, by contrast, is smaller, more experimental and more tightly embedded in one financial centre.

The European Central Bank context is more cautious. Reuters reported in late 2025 that the ECB had warned stablecoins could siphon deposits from euro-area banks and create financial-stability concerns. That caution sits alongside Europe’s desire to develop euro-denominated digital-money capacity. The implication is that Europe’s strategy is likely to remain a mixture of public caution and private experimentation under MiCA.

The United States presents a different contrast. For much of the previous cycle, US crypto regulation was more fragmented and more enforcement-led than Switzerland’s tailored adaptation. But the US is not standing still. On 18 July 2025, the President signed the GENIUS Act into law, creating a federal framework for payment stablecoins. In April 2026, the Treasury proposed rules implementing the Act’s AML and sanctions programme requirements for permitted payment stablecoin issuers. The SEC’s Crypto Task Force, led by Commissioner Hester Peirce, states that its objective is to provide clarity on the application of federal securities laws to crypto assets and to recommend practical policy measures. That is a notable shift towards formalisation.

Switzerland therefore sits between two larger systems. It does not have the EU’s regulatory scale or the US’s capital-market depth, venture ecosystem and dollar-network effects. But it adapted earlier in a targeted way, and that early adaptation helped it build living institutional infrastructure before the EU and US had finished deciding what category many of these activities belonged to. That is the Swiss comparative edge, precision before scale.

Conclusion

The main lesson is that the next stage of digital assets looks less like a consumer token boom and more like a contest over regulated rails. There are at least five rails to watch in Switzerland: bank-integrated custody and trading; tokenised-securities issuance and distribution; DLT trading venues; tokenised commercial-bank money; and settlement in or against central-bank money. The Swiss ecosystem already has live pieces in each category.

For institutional allocators, the commercial signal is not only asset prices or venture rounds. It is whether regulated institutions continue to add services and real client activity. PostFinance and ZKB should be watched for product expansion, corporate-client adoption and any movement beyond the current asset menus. Sygnum, AMINA, Taurus and Crypto Finance should be tracked as picks-and-shovels providers into the broader financial sector. SDX and BX Digital should be monitored for issuer quality, trading volumes, secondary-market participation and settlement reliability.

For venture investors and fintech operators, the more interesting opportunity may sit in interoperability, workflow software, treasury tooling and compliance infrastructure rather than in speculative-token consumer applications. Deposit tokens, stablecoins and wCBDC do not eliminate each other. They create a need for orchestration: wallet controls, allow-listing, audit trails, identity, treasury management, tokenisation middleware and legal-operational translation between traditional ledgers and DLT environments. Switzerland is attractive here because the relevant institutional users, bank partners and regulators are unusually concentrated.

The watchlist for the next 12 to 24 months is clear. First, whether the CHF stablecoin sandbox produces credible use cases and graduates beyond a controlled environment. Second, whether the Deposit Token concept moves from proof of concept to broader bank participation. Third, whether Project Helvetia continues to expand and whether BX Digital’s SIC-linked model gains meaningful adoption. Fourth, whether SDX activity deepens through higher-value issuers and more secondary trading. Fifth, how MiCA implementation, Qivalis and US GENIUS-rule implementation reshape competitive pressure on Swiss initiatives. Those indicators will tell investors whether Switzerland remains a niche pioneer or becomes a durable template for regulated digital finance.

Sources

- (2025 Report): [www.cvvc.com](https://www.cvvc.com/insights)

- cryptovalley.swiss

- sygnum.com

- swissstablecoin.ch

- qivalis.eu

- stadtzug.ch

Partner Highlight

At insights4vc, we pay attention to teams that are not just shipping products, but shaping categories.

Moto is one of them. The company is building a premium card experience positioned as an alternative to traditional incumbents such as Amex, combining a high-end user interface with more modern financial infrastructure.

Moto is currently expanding access to a limited testing group. If you would like to test the product and typically spend more than $5,000 per month, please contact us at: [email protected]

Cover Artwork

Les Heures Saintes

Ferdinand Hodler

Risk Disclaimer:

insights4.vc and its newsletter provide research and information for educational purposes only and should not be taken as any form of professional advice. We do not advocate for any investment actions, including buying, selling, or holding digital assets.

The content reflects only the writer’s views and not financial advice. Please conduct your own due diligence before engaging with digital assets or related technologies, as they carry high risks and values can fluctuate significantly.