Kraken’s roadmap now points to an IPO in 2026. This issue delivers a full teardown of the exchange’s financial trajectory and growth levers, plus a side-by-side comparison with Coinbase and Binance to sharpen your edge.

Key findings include:

- Robust Growth and Scale: Kraken rebounded strongly from the 2022–23 crypto bear market. FY2024 revenue reached $1.5 billion (up 128% YoY) with $424 million in adjusted EBITDA. Trading volume hit $665 billion in 2024, and Q2 2025 volume was $186.8 billion. As of mid-2025, Kraken serves ~15 million clients globally and holds $43 billion in customer assets, reflecting growing user engagement.

- Business Diversification: Kraken generates the bulk of revenue from spot trading fees, but has expanded into derivatives, staking, tokenized equities (“xStocks”), and payments. It acquired regulated futures broker NinjaTrader for $1.5 billion in 2025 to accelerate U.S. crypto derivatives offerings. After a regulatory setback in 2023, Kraken’s on-chain staking service has resumed under clearer guidelines. New initiatives like commission-free stock trading for U.S. clients and a global money transfer app (“Krak”) broaden Kraken’s platform beyond cryptocurrencies.

- Competitive Position: Kraken is the #2 U.S. exchange by volume after Coinbase but ranks lower globally (~8th by spot volume) with about 2% market share versus Binance’s ~39%. Kraken’s strength lies in fiat-to-crypto liquidity – it commands over 40% of global stablecoin-to-fiat trading volumes – and a reputation for security and compliance (no major hacks to date). However, it lags Coinbase and Binance in retail mindshare and scale. Kraken’s fee structure (~0.2–0.4% per trade for most users) is competitive but not the lowest (Binance offers ~0.1% or less). Its product breadth (spot, margin, futures, staking, equities) now rivals Coinbase’s, while its regulatory focus and transparency stand out against Binance’s more opaque posture.

- Regulatory Landscape: Kraken has proactively built a broad compliance footprint. It is registered with U.S. FinCEN and obtained a Wyoming bank charter (SPDI) in 2020. It holds licenses or authorizations in Canada (Restricted Dealer in 2023) and was the first exchange licensed under Europe’s MiCA framework (Ireland, 2025). Past regulatory run-ins – including a $30 million SEC settlement in 2023 over its staking program and a $1.25 million CFTC fine in 2021 – have now largely been resolved. In a pivotal development, the SEC dismissed its staking lawsuit with prejudice in 2025, imposing no penalties. This regulatory clearance, alongside new crypto-friendly U.S. legislation, positions Kraken to expand services legally.

- Financial Outlook and IPO Valuation: Kraken’s last private funding round is reportedly targeting $500 million at a $15 billion valuation ahead of the IPO. That equates to ~10× 2024 revenue or ~35× EBITDA – a premium to Coinbase’s multiples. At $15 billion, Kraken would be valued around $1,000 per user, roughly double Coinbase’s ~$500/user. Scenario analysis values Kraken at 7–10× forward sales and 20–30× EBITDA, yielding a valuation range of $10–18 billion depending on crypto market conditions. Coinbase earned $6.3 billion revenue in 2024 and trades around a $50–60 billion market cap, while Binance reportedly had $16.8 billion revenue in 2023 and could be worth $60–100 billion+ by extrapolation. Kraken’s IPO pitch hinges on its resumed growth (18% YoY revenue rise in Q2 2025), diversified product suite, and a “compliance premium” in a regulated market.

- Key Risks and Catalysts: Kraken’s fortunes are tied to crypto market volatility – a sustained downturn could compress trading volumes and revenue. Other risks include regulatory reversals, security incidents, reliance on stablecoins for liquidity, and competition driving fee compression. Catalysts include potential Bitcoin spot ETF approval, further U.S. regulatory clarity, growth in the crypto derivatives market, and broader crypto cycle tailwinds. Kraken’s strong balance sheet post-fundraise and M&A appetite position it well.

Management and Governance

Kraken was founded in 2011 by Jesse Powell, an alumnus of California State University, Sacramento, together with Thanh Luu and Michael Gronager. Powell had earlier consulted for Mt. Gox to resolve a security breach and started Kraken as a likely successor because he expected Mt. Gox to fail. Mt. Gox did collapse in 2014 after failing security audits.

Leadership Team

Kraken is led by CEO David “Dave” Ripley, who took the helm in late 2022. Ripley was Kraken’s COO for six years prior, overseeing the company’s growth from 50 to more than 3,000 employees. He joined Kraken via the 2016 acquisition of Glidera, a wallet start-up he co-founded. With a background as a software engineer and a stint at Boston Consulting Group, Ripley is known for operational execution. Kraken credits him with leading 16 acquisitions and securing many of its regulatory licenses. As CEO, Ripley has focused on scaling Kraken’s product offerings while instilling “crypto-first” values and efficiency; he navigated the firm through 2022 cost-cutting and has emphasized strengthening operating leverage for sustainability.

Working alongside Ripley is Arjun Sethi, appointed co-CEO in October 2024. Sethi is a co-founder of Tribe Capital and an early Kraken investor; Tribe became Kraken’s second-largest institutional shareholder in 2021. He joined Kraken’s board in 2022 and was instrumental in pushing Kraken to disclose financials and prepare for public markets. As co-CEO, Sethi drives strategy, partnerships and growth initiatives, leveraging his venture-capital experience. He has framed Kraken’s vision as the “tech-forward Nasdaq of crypto,” contrasting it with Coinbase’s more conservative “NYSE” approach. Under Sethi’s influence, Kraken has accelerated innovations such as tokenized stocks and the Krak payment app.

Kraken’s broader executive bench includes **CJ Rinaldi (Chief Compliance Officer)**, hired from Deutsche Bank in 2022 to bolster compliance; **Carrie Dolan (CFO)**, who joined in early 2023 to lead IPO readiness after serving as CFO at Lending Club and Metromile.

The board is chaired by founder Jesse Powell, who remains a significant shareholder and influential figure. Besides Powell and co-CEO Sethi, directors include investor representatives such as Nicolas Cary (Blockchain Capital).

Ownership and Cap Table

Kraken is a private, venture-backed company that has largely avoided heavy dilution. Founder Jesse Powell is believed to retain a substantial stake, since Kraken raised only about 27 million USD of primary capital before 2021. Major outside holders include Hummingbird Ventures, Blockchain Capital, Tribe Capital, SkyBridge Capital, SBI Holdings and Digital Currency Group. More than 2,000 smaller investors came in through a 2019 crowdfunding round. A February 2022 equity raise tied to an acquisition valued Kraken at roughly 10.8 billion USD post-money. By mid-2025, an additional capital raise implied a valuation near 15 billion USD, with no single investor holding a majority position.

Employee Base and Culture

Kraken is remote-first and nominally registered in Cheyenne, Wyoming. Headcount peaked above 3,000 in 2022; after layoffs, estimates place staff near 1,700 in mid-2025, though some public materials still show “2,300+” employees. Employees span more than 60 countries, with engineering hubs in Europe and Asia-Pacific. Kraken’s culture is crypto-purist and libertarian-leaning, emphasizing transparency and security (95 percent of assets in cold storage and regular Proof-of-Reserves audits). A 2022 “Jedi” culture memo caused internal debate, but Kraken retained key talent and reaffirmed its mission. The firm is known for 24 / 7 customer support and strong compliance; it has pulled out of jurisdictions like New York where regulations conflict with its principles.

Governance-wise, Kraken is preparing for an eventual IPO. It already works with EY on audits and runs SOX-readiness programs. Independent-director recruitment is under way to satisfy public-listing rules, and typical committees such as Audit and Compensation will be formalized.

Business Segments and Revenue Streams

Kraken operates five main segments: Spot Trading, Derivatives Trading, Staking and Yield, Tokenized Stocks & Equities, and Payments & Banking Services.

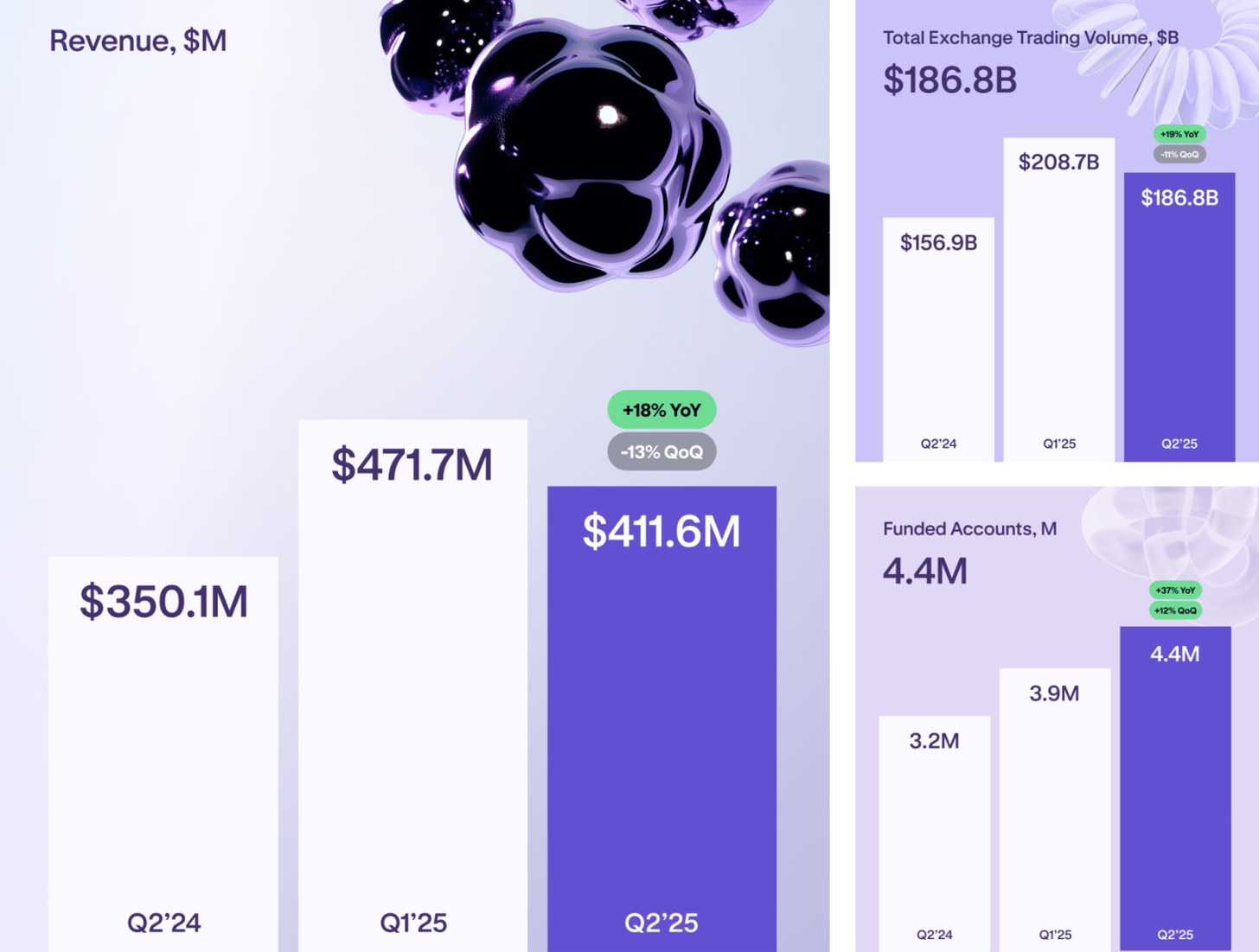

- Spot Cryptocurrency Trading – Kraken lists more than 220 crypto assets and seven fiat currencies (USD, EUR, GBP, JPY, CAD, CHF, AUD). For advanced users, Kraken Pro charges maker-taker fees that range from 0.16–0.26 percent for low-volume traders down to 0–0.10 percent at high volumes; instant-buy retail fees are about 1.5 percent. In Q2 2025, spot volume reached 186.8 billion USD, generating 411.6 million USD in revenue (about 0.22 percent effective fee). Spot still represents roughly 70-80 percent of revenue, with direct contribution margins above 50 percent thanks to scalable infrastructure and deep fiat-to-crypto liquidity.

- Margin and Derivatives Trading – Kraken offers up to 5× spot margin and, via Kraken Futures, perpetual and fixed-maturity futures with up to 50× leverage for non-U.S. users. A 2021 CFTC settlement limited U.S. margin activity, but the 2025 NinjaTrader acquisition lets Kraken route U.S. clients to regulated CME crypto futures through the Kraken Pro interface. Internationally, Kraken now lists its own perpetual futures under a UK MTF license and even 24 / 7 forex-perpetual pairs such as EUR / USD. Derivatives revenue (fees of roughly 0.02–0.05 percent notional) was below 10 percent of total in 2024 but is expected to grow.

- Staking and Earn – Kraken supports staking for assets such as ETH, DOT and SOL, keeping an estimated 10–15 percent of staking rewards as commission. After pausing U.S. staking under SEC pressure in 2023, Kraken resumed on-chain staking for U.S. customers in 2025 following a favorable outcome. With the 2021 acquisition of Staked, Kraken can offer non-custodial staking for security-conscious clients. Staking accounts for a minority of revenue but carries high margins.

- xStocks and Equities Hub – In Q2 2025 Kraken launched commission-free U.S. stock and ETF trading for American users and introduced “xStocks,” 24 / 7 tokenized equities for non-U.S. users. Stock trades monetize via payment for order flow or cash-interest spreads, while xStocks bring standard trading fees and custody charges. Volumes remain small but position Kraken as a one-stop investing platform.

- Payments and Banking Services – June 2025 saw the debut of “Krak,” a global money app that lets users send crypto or fiat across 160 plus countries with automatic currency conversion. Kraken integrates local rails (Bit Trade in Australia, Pix in Brazil) and is developing products such as debit cards and yield-bearing USDⱽ (USDG) accounts under its Wyoming SPDI charter. Fees come from FX spreads, interchange and B2B treasury services.

Revenue Mix and Profitability

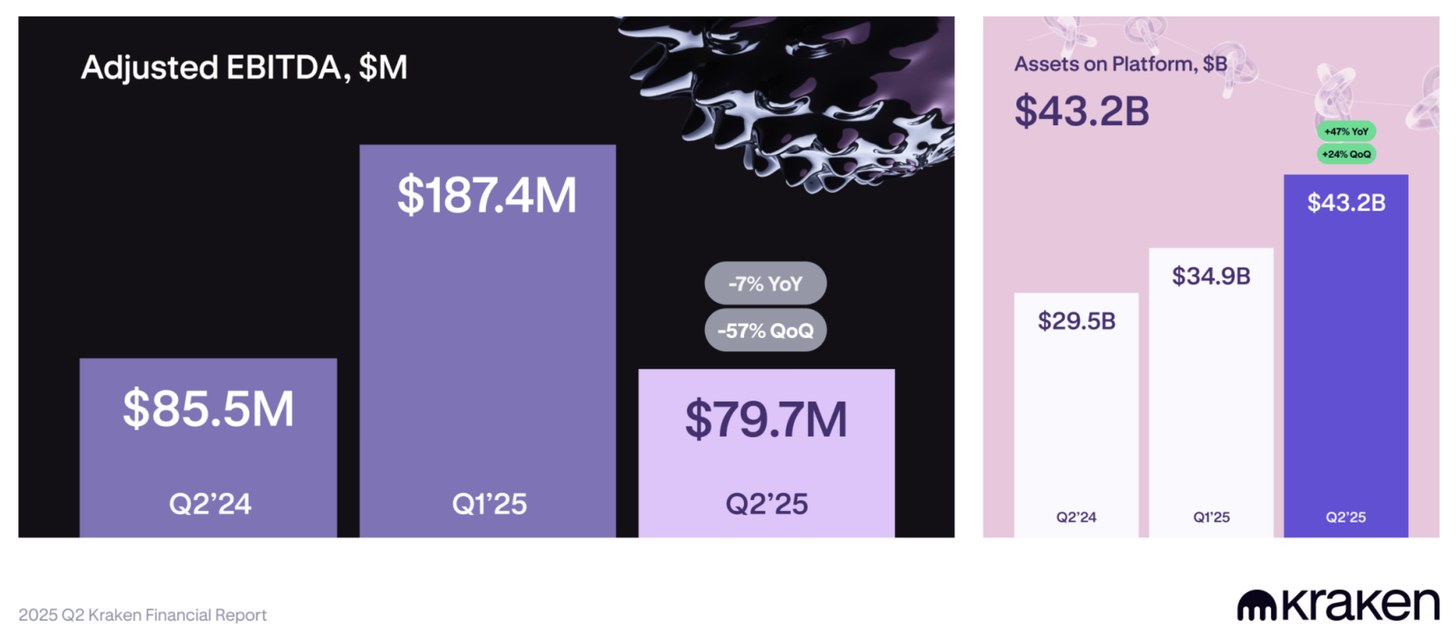

Estimated 2024 mix: spot 70-80 percent, derivatives 5-10 percent, staking about 10 percent, and other services the remainder. Kraken’s adjusted EBITDA margin was roughly 28 percent in 2024 but slipped to about 19 percent in Q2 2025 due to investment in new products and geographic expansion. Management expects mature spot and derivatives businesses to subsidize emerging segments until they scale.

Key Operating Metrics (2019 – Q2 2025)

To assess Kraken’s trajectory, we compile its key operating and financial metrics from the pre-pandemic era through the latest quarter. This includes trading volumes, revenue, profitability, user counts, and other indicators, with growth rates to contextualize performance through crypto market cycles.

Revenue and EBITDA:

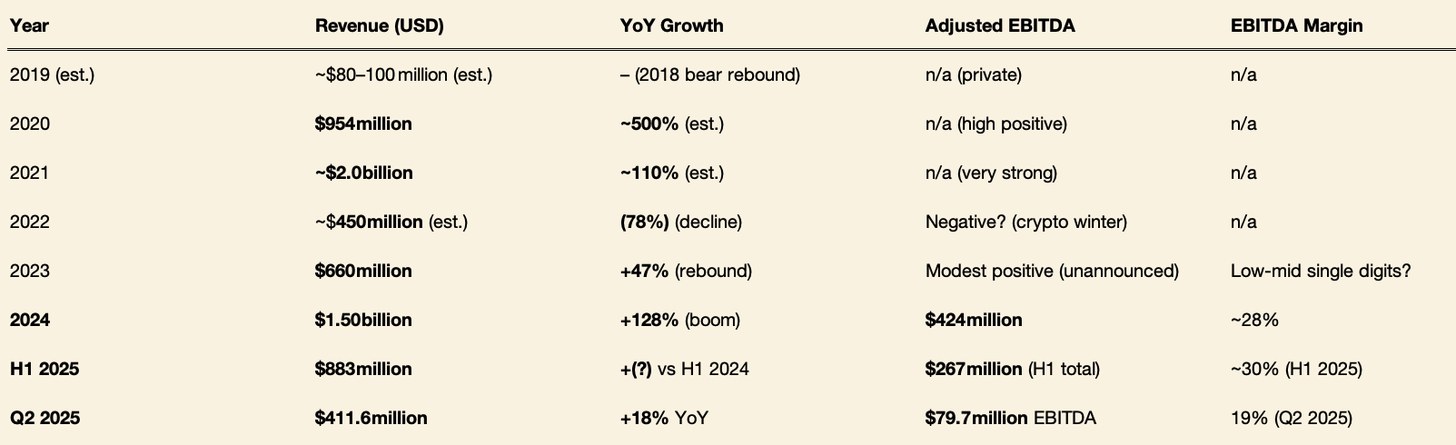

Kraken’s revenue swung from ~$2B in 2021 to ~$450–660M in 2022–23 amid the crypto downturn, then recovered strongly in 2024 to $1.5B. Adjusted EBITDA followed a similar pattern: likely near break-even or a small loss in 2022, then improving to $424M in 2024. Q2 2025’s 13% sequential revenue drop (from a record $472M in Q1 to $412M in Q2) reflects seasonality and macro "market turbulence," yet revenue was still up 18% YoY. Kraken’s EBITDA margin was pressured in Q2 (19%) due to higher expenses; notably, EBITDA was down 7% YoY despite higher revenue, as Kraken invested in growth. Overall, Kraken demonstrates high operating leverage in bull runs (EBITDA margin exceeded 50% at points in 2021, by our estimates) and discipline in cutting costs during bears (rapid layoffs in late 2022 to protect margins).

Trading Volume and Market Share: Volume is a key driver of revenue. Kraken’s annual spot trading volumes were: ~$85 billion in 2019 (est.), $320 billion in 2020 (boosted by DeFi summer and Bitcoin’s run), $625 billion in 2021, then perhaps ~$300 billion in 2022 (bear market contraction). In 2024, volume rebounded to $665 billion, up 148% YoY (implying ~$268B in 2023). Through H1 2025, Kraken processed $884 billion (annualized ~$1.77T) – a sign of increasing activity if crypto markets remain strong.

In terms of market share, Kraken has consistently been among the top exchanges by volume, but its global share is in the low-single digits. As of April 2025, Kraken was not in the top 5 globally (Binance ~38%, several Asian exchanges ~5–9% each, Coinbase ~6.9%). Kraken’s share is roughly ~2% of worldwide spot volume. However, in its niche of fiat-centric trading, Kraken is a leader (often #1 in BTC/EUR volume). In the U.S. market, Kraken’s share has grown – it’s firmly the #2 regulated platform after Coinbase. Domestically, Coinbase reportedly has ~40% share of U.S. fiat-to-crypto volume vs Kraken’s ~25% and others making up the rest (Coinbase’s USD volumes are higher, but Kraken leads in EUR/GBP volumes including U.S. customers trading those). Kraken’s volume market share expanded in 2024 as some competitors (FTX, Binance’s U.S. arm) fell away.

User Base and Activity: Kraken’s total registered user count grew from single-digit millions to over 15 million by 2025. In 2018, Kraken had ~1 million users; by mid-2020 ~4M; by early 2022 about 8.5M users; and significant growth through 2023–25 to reach ~15M. Funded accounts (users with an active balance) were 2.5 million at end-2024 and 4.4 million by Q2 2025 – a 37% YoY increase. The surge from 2.5M to 4.4M in six months suggests strong new user acquisition amid the 2024–25 market rally.

Average Revenue per User (ARPU): With $1.5B revenue over ~2.5M funded accounts in 2024, simple ARPU per funded account was ~$600. Kraken indicated ARPU per active customer was over $700 in 2024. External analysts estimate ARPU around $2,023 per transacting user (likely annualized, focusing on active traders). Kraken’s high ARPU underscores its success with heavy traders. By comparison, Coinbase’s ARPU (blended across 8–9M monthly active users) was ~$825 for 2024, and Robinhood’s was ~$164 (including non-crypto services).

Assets Under Custody: At year-end 2024, assets under custody were $42.8 billion, including crypto and fiat. Assets nearly doubled YoY (+47% YoY by Q2 2025 to $43.2B), reflecting rising crypto prices and net new inflows. Kraken’s AUC indicates it holds about 6–7% of the total crypto market cap of major coins.

Geographical Spread: Kraken serves clients in 190+ countries, but its revenue is weighted towards North America and Europe. Europe (especially Eurozone and UK) has historically been largest, with North America likely rivaling or exceeding Europe after U.S. growth in 2024. Kraken is expanding in Asia-Pacific (Japan, Australia) and Middle East (UAE), but these newer markets contribute modestly for now.

Headcount: Kraken’s headcount fluctuated from ~1,200 in 2019 to ~3,200 in mid-2022, then down to ~2,200 post-layoffs, and stabilized at 1,700–1,800 by mid-2025. Rationalization improved Kraken’s revenue per employee significantly ($0.75M per employee in 2024 vs Coinbase’s ~$0.5M).

Key Operating Metrics Summary (2019–2025):

- Trading Volume: ~$85B (2019) → $625B (2021) → $665B (2024), Q2 2025 vol $186.8B (+19% YoY).

- Revenue: <$0.1B (2019) → $1.5B (2024), H1 2025 $883M.

- Adj. EBITDA: Robust $424M (2024), Q2 2025 $79.7M (down YoY).

- Registered Users: ~1M (2017) → ~4M (2020) → 8.5M (2022) → ~15M (2025).

- Funded Accounts: 2.5M (2024) → 4.4M (Q2 2025), active customer base expanding ~37% YoY.

- Assets on Platform: $42.8B (2024) → $43.2B (Q2 2025), YoY +47%.

- ARPU: ~$600 per funded acct in 2024; ~$2,000 per active trader.

- Market Share: ~2% global spot; #2 in U.S. behind Coinbase; leading ~40–60% share in fiat/crypto niches.

- Employees: ~1,700 (2025) vs ~2,300 (2022), improved operating efficiency post-layoffs.

These metrics paint Kraken as a company that weathered the crypto cycle, now hitting new highs in users and volumes, demonstrating solid momentum heading into its IPO.

Competitive Landscape

Kraken operates in a highly competitive crypto exchange industry, facing both large global players and smaller niche rivals. We compare Kraken’s position versus key competitors on market share, fees, product breadth, regulatory posture, and brand trust. The main comparables are Coinbase (U.S. market leader), Binance (global leader), and other notable exchanges like Bitstamp, Gemini, and Bybit.

Market Share and Size:

In terms of overall size, Binance is the dominant exchange globally, with approximately 39% of spot trading market share in 2025 and an even higher share in derivatives. Binance processed $7.4 trillion in spot volume in 2024—more than 11× Kraken’s $665 billion. Binance’s revenue ($16.8 billion in 2024) was roughly 11× Kraken’s. Coinbase, while smaller than Binance, is the largest U.S.-regulated exchange, with $6.3 billion revenue in 2024 on approximately $1.3 trillion trading volume (spot). Coinbase’s global spot market share is around 6–7%, with strong traction in U.S. retail markets. Kraken, by comparison, held about 2% of global volume, typically ranking between #8 and #15 worldwide. Other competitors like Gate.io, OKX, MEXC, Bitget, and Upbit command 5–9% global share as of Q2 2025, mainly focusing on Asian markets. Bybit, a major derivatives-focused exchange, holds around 6–7% spot share.

In the U.S. market, Coinbase is #1, and Kraken firmly holds the #2 spot. Binance.US has significantly shrunk due to regulatory issues. Gemini and Bitstamp compete in the U.S./EU at smaller scales, with Gemini’s volumes significantly lower (around $117 million daily vs Kraken’s ~$1 billion). Bitstamp maintains under 5% market share in the EU. Bybit and KuCoin primarily serve international users outside the U.S.

Fees and Pricing:

Kraken’s fee schedule (up to 0.26% taker fee, down to 0.10% for high-volume traders) is comparable to Coinbase Advanced Trade (0.6% taker for <$10k volume, down to 0.15% at >$100k monthly, with zero maker fees for smaller volumes). Binance historically undercuts competitors with a flat 0.1% spot fee, occasionally offering zero-fee Bitcoin trading and lower fees through VIP programs. Bybit, OKX, and KuCoin offer similar competitive pricing (~0.1% or lower), while Gemini (up to 0.35%) and Bitstamp (~0.3%) charge higher fees. Kraken’s fees position it between these groups, attracting loyal users who prioritize fiat support and security despite slightly higher costs. Kraken+ (Plus), introduced in 2025, offers zero-fee trading up to specific limits and quickly gained over 100k subscribers, demonstrating demand for alternative pricing structures.

Product Breadth:

Kraken and Coinbase offer diverse products, including spot trading, staking, custody services, OTC desks, some derivatives, and equities and banking features in Kraken’s case. Binance leads globally with a broader product suite, including NFTs, crypto loans, yield farming, launchpads, and blockchain ecosystems (BNB Chain). Kraken has not significantly expanded into NFTs or launchpads despite testing an NFT marketplace. Its new traditional asset (stocks) and payments offerings differentiate it from Binance and Coinbase, as Coinbase doesn’t offer stock trading, and Binance shut down tokenized stocks due to regulatory issues.

Kraken serves U.S. clients with more comprehensive products, including equities and soon crypto futures via NinjaTrader, surpassing current Coinbase and Binance.US offerings. Its institutional Kraken Prime brokerage competes directly with Coinbase Prime, Gemini Custody, and BitGo.

Regulatory Posture:

Kraken positions itself as one of the most regulated exchanges, holding multiple licenses, auditing reserves, and maintaining legal compliance. Coinbase, similarly regulated, is currently in litigation with the SEC but maintains strong compliance records. Gemini emphasizes a conservative, compliant approach.

Binance, in contrast, faces global regulatory crackdowns from the U.S. SEC and CFTC and lacks a fixed headquarters. It has historically operated in regulatory gray areas, resulting in restricted access or outright bans in several jurisdictions. Kraken’s proactive compliance stance is evident through its early adoption of MiCA in Europe, licensing in Canada, and willingness to adjust to stringent regulatory standards.

Brand Trust and Reputation:

Kraken enjoys a positive reputation, particularly regarding security and reliability, having never been hacked. Coinbase, a public company, holds strong mainstream trust, especially among beginners. Gemini’s reputation was impacted by the Gemini Earn collapse. Bitstamp remains respected for its secure European exchange model, despite limited recent innovation. Bybit and KuCoin, offshore entities with less stringent KYC requirements, hold lower trust levels. Kraken notably benefited from its clear stance post-FTX collapse, advocating transparency and aiding regulatory investigations.

In summary, Kraken positions itself as a trusted, comprehensive crypto platform emphasizing quality, security, and regulatory compliance. It remains competitively placed against Coinbase and captures market share from Binance’s regulatory uncertainties. Kraken might consider strategic acquisitions of smaller compliant exchanges like Bitstamp or Gemini to consolidate market presence. Emerging competitors include OKX, Crypto.com, and traditional stock trading apps offering crypto like Robinhood, prompting Kraken to strategically integrate stock trading and advanced crypto features.

Regulation and Legal Environment

Kraken’s operations are deeply influenced by regulatory frameworks across jurisdictions. Overall, Kraken has taken a pro-compliance stance, seeking licenses and engaging with regulators, which sets it apart from some industry peers. Here we detail Kraken’s regulatory status, past legal challenges, and readiness for upcoming regimes like MiCA, as well as any outstanding risks.

Licenses and Registrations: Kraken is legally known as Payward, Inc. in the U.S., and it operates through various subsidiaries globally. Key regulatory licenses/registrations include:

- United States: Kraken is registered as a Money Services Business (MSB) with FinCEN since 2014, which covers federal AML/CTF obligations in the U.S. It has state-level money-transmitter licenses in the majority of U.S. states (except where not required or where it doesn’t operate – e.g., it historically did not operate in New York due to the BitLicense rule, calling the BitLicense “onerous”). Notably, Kraken obtained a Special Purpose Depository Institution (SPDI) charter in Wyoming in September 2020, establishing “Kraken Bank.” This made Kraken the first crypto exchange to become (in principle) a bank in the U.S. The SPDI charter allows Kraken to offer certain banking services (custody, deposit-taking) under Wyoming law, with 100 % reserve requirements. As of 2025, Kraken Bank has not yet launched to the public – it’s awaiting a Federal Reserve master-account approval. There’s a pending court case where Wyoming SPDI applicants (including Kraken) sued the Fed for delays; however, indications in 2023-2024 were that Kraken Bank would begin limited operations once approved. When operational, Kraken Bank will be regulated by Wyoming’s Division of Banking and have access to the U.S. payment system (potentially a big advantage). Aside from the bank charter, Kraken must comply with CFTC and SEC rules to the extent applicable: Kraken does not currently list securities (to avoid SEC issues) and limited margin trading for U.S. users after the CFTC action in 2021. It also holds a U.S. Futures Commission Merchant (FCM) license indirectly via the NinjaTrader acquisition (NinjaTrader is registered with the NFA/CFTC as an Introducing Broker and has relationships with FCMs). This gives Kraken a regulated pathway to offer futures in the U.S., as discussed.

- Canada: Kraken has a strong presence in Canada (it acquired Canadian exchange Cavirtex in 2016). It is registered with FINTRAC as an MSB. More importantly, in March 2023, Canada introduced a new pre-registration undertaking (PRU) requirement for crypto exchanges. Kraken was among the first to file a PRU and was granted a restricted-dealer license in Ontario in 2023, allowing it to continue operating across Canadian provinces. This is notable as competitors like Binance chose to exit Canada due to these rules. Kraken’s Canadian license means it adheres to investor protections there (like suitability assessments, limits on certain crypto buys, etc.).

- European Union (MiCA): Kraken achieved a milestone by becoming the first exchange to receive authorization from the Central Bank of Ireland under MiCA (Markets in Crypto-Assets Regulation) in mid-2025. This registration in Ireland will passport Kraken’s services across all 27 EU member states once MiCA takes full effect by end-2024/2025. It likely registered as a Crypto Asset Service Provider (CASP) for services like trading, custody, and possibly its new tokenized-stocks offering under e-money or other classifications. Kraken also has a long-standing UK entity: it’s registered with the UK Financial Conduct Authority (FCA) as a crypto-asset business under the interim regime (since Brexit, the UK requires exchanges to register for AML purposes). Kraken’s UK arm (Payward Ltd.) gained this FCA registration in 2021. Additionally, Kraken’s futures business (Crypto Facilities) is authorized by the UK FCA as a Multilateral Trading Facility (MTF) and as an EU MTF via passport – enabling Kraken to legally offer crypto derivatives to European clients. After Brexit, Crypto Facilities retained an FCA license and possibly operates under the UK’s Temporary Permissions Regime in the EU. With MiCA, it might need additional approval, but Kraken’s new Irish authorization could cover spot and derivatives in the EU going forward.

- Asia-Pacific: Kraken has had mixed history here. It withdrew from Japan in 2018 citing costs, but relaunched in 2020 after obtaining a license under Japan’s Payment Services Act. However, in April 2022 Kraken decided to exit Japan again (post-FTX slump and global downsizing, it shut its Japan unit in early 2023 to focus elsewhere). In Australia, Kraken is registered with AUSTRAC and, after acquiring Bit Trade, it can service Aussie clients with AUD pairs (no specific license needed beyond AML registration, as Australia had no exchange-licensing regime until very recently when they proposed one). Middle East: Kraken got a license in Abu Dhabi (ADGM) in 2022 to operate a regulated exchange in the UAE, including dirham pairs – but reportedly Kraken later paused that plan and closed its Abu Dhabi office in early 2023 amid cost cuts. It’s unclear if it fully activated that license. In any case, Kraken does serve some Middle-East customers remotely. Other jurisdictions: Kraken is selective; for instance, it does not serve China (banned), and likely restricts countries under sanctions (Kraken paid a ~$362 k fine to the U.S. Treasury’s OFAC in 2022 for inadvertently serving Iranian users). It now has beefed-up sanctions compliance, as noted by that settlement, which also required Kraken to invest $100 k in compliance programs.

SEC Staking Case Outcome: A major legal development was the February 2025 dismissal of SEC vs Kraken (staking). The SEC under Gensler had filed a civil complaint in late 2022 accusing Kraken of offering unregistered securities via its staking program. Kraken fought back, filing a motion to dismiss in late 2024, arguing the case was politically motivated and lacked evidence of fraud. With the change in U.S. administration in January 2025 (and a crypto-friendlier SEC stance), the SEC staff agreed to drop the case with prejudice – meaning it’s permanently closed. No penalties, no admission of wrongdoing, and no changes to Kraken’s business were required. This is an important victory: it sets a precedent that staking services can be offered compliantly (though note: Kraken likely had to implement improved disclosures to satisfy new SEC leadership informally). Right after, Kraken re-enabled staking for U.S. customers (e.g., Ethereum staking, which Coinbase also offers, but Kraken’s case clarity gives it an edge). The blog post “A win for fairness” from Kraken celebrated this outcome and framed it as the end of “regulation by enforcement” in the U.S. Indeed, in July 2025 Congress was advancing crypto-market-structure bills and a stablecoin bill (the Genius Act mentioned was signed in July 2025, providing stablecoin regulatory clarity). Kraken is well-positioned under these emerging laws, given its proactive approach.

Ongoing Investigations or Liabilities: As of mid-2025, Kraken does not appear to have major active lawsuits from regulators. The CFTC matter was settled in 2021 with a $1.25 M fine, and Kraken ceased offering the problematic product (on-platform margin with 28-day terms) in the U.S. (the CFTC’s commentary acknowledged Kraken cooperated fully). The OFAC sanctions issue was settled in 2022 with a $362 k fine. Kraken likely also adjusted its geofencing and KYC to prevent such lapses going forward. EU and UK regulators: Kraken’s operations in Europe so far haven’t been subject to the kind of enforcement we saw for, say, BitMEX or Binance. Having an FCA-regulated subsidiary and now an Irish license means Kraken’s EU/UK business is regularly audited and monitored. We haven’t heard of any specific EU probes into Kraken; by contrast, Binance and other exchanges have been under investigation in countries like France and Germany for AML issues – Kraken seems to have avoided those by adhering to AML directives.

One potential legal red flag: In late 2018, the New York Attorney General’s office included Kraken in a report (“Virtual Markets Integrity Initiative”) noting Kraken refused to respond to the NYAG’s questionnaire and might be operating in NY illegally. Kraken’s Powell famously dismissed that, since Kraken wasn’t servicing NY residents. NYAG did not take further action specifically against Kraken, as Kraken was indeed geoblocking NY. That matter is closed, but it signaled Kraken’s willingness then to push back. Nowadays, Kraken would rather avoid a market (like NY) than compromise on something – which, while limiting market size, also limits legal risk.

Lawsuits and Consumer Issues: Kraken has faced far fewer private lawsuits than some peers. There have been occasional user lawsuits over system outages or lockouts, but none high-profile. In 2021, one incident involved a sudden flash crash of Ethereum price on Kraken (ETH dropped to ~$700 from $1 600 briefly on Kraken during a volatile day). Some leveraged traders were liquidated unfairly. Kraken cited a technical issue with an order flow. There was talk of a class action, but Kraken offered compensation credits to affected users, and it mostly blew over. Such incidents underline the importance of robust systems. Kraken’s matching engine is generally robust now (it underwent major upgrades in Dec 2020 and later).

Another area of regulation is custody and security standards. Kraken uses its Proof-of-Reserves audits to show it holds client assets 1:1, which is a proactive measure not legally required (Coinbase and others haven’t done it regularly). If these audits continue, it will help regulators and users trust Kraken. Kraken also holds a crypto-escrow-agent license in some states (like a Louisiana license in 2020) – essentially regulatory oddities that allow certain operations.

MiCA Readiness: Kraken getting that Irish registration implies full readiness for MiCA. MiCA will impose requirements like whitepapers for token listings, stablecoin-reserve rules, and capital requirements for CASPs. Kraken likely already complies with many (it has a compliance department of significant size and is adequately capitalized – though as a private company we don’t see its balance sheet, it has presumably enough equity to meet capital thresholds). Kraken will have to ensure all the coins it lists meet MiCA’s standards by 2025 (MiCA has a grandfathering period). This could mean providing disclosures or delisting privacy coins if required by certain interpretations (some countries like the UK have hinted at banning privacy coins; Kraken might adapt accordingly).

Future Regulatory Changes: In the U.S., if the market-structure bill passes, Kraken might need to register as an Alternative Trading System (ATS) or a Broker-Dealer if certain tokens are deemed securities. Kraken’s incoming CEO said in 2022 they had no plans to register with the SEC as a broker – that was under Gensler’s regime. If new legislation clarifies token categories, Kraken could adjust. It already segregates its futures business under an entity that can deal with the CFTC.

Legal Risks: At this point, Kraken’s legal risks are relatively lower than many competitors, but not zero. Potential risk factors include:

- Regulatory flip-flop: If a less-friendly U.S. administration returns by 2029 or if there’s backlash, Kraken could again face enforcement on something (e.g., if staking or certain tokens get re-characterized).

- New tax-reporting rules: The U.S. will implement stricter tax reporting for crypto brokers in 2025 (IRS rules under the Infrastructure Act). Kraken will comply (it likely already issues 1099s to U.S. users trading above thresholds). Non-compliance fines could be heavy but Kraken has no incentive to shirk here.

- Global coordination: As G20 and FATF push for Travel Rule compliance (sharing customer info on transfers between exchanges), Kraken has to implement that – which it has been working on (likely compliant by now).

- Lawsuit by users due to hacks or loss: If a major incident occurs (though none yet), legal liabilities could emerge.

Given Kraken’s careful approach, it has mostly resolved past legal issues: paid roughly $30 M in various fines (SEC, CFTC, OFAC), and now operates with those lessons learned. The Wikipedia entry notes Kraken “[has] been the subject of several regulatory investigations since 2018, with cumulative fines of over $30 million” – which matches our recount of SEC, CFTC, and OFAC penalties. Importantly, none of those materially hurt Kraken’s business or required customer restitution (they were compliance-related, not fraud cases).

Regulatory Standing vs Competitors: We should note Kraken’s relative standing:

- Kraken vs Coinbase: Both are top-compliance exchanges. Coinbase is larger and has taken a more active role in pushing for new laws (it’s currently in litigation with the SEC about what constitutes a security token). Kraken benefited from the SEC’s change of heart without going to court (since its case was dropped). Coinbase, being public, faces the SEC’s scrutiny more. Kraken’s advantage is being nimble (private) and less in the political spotlight – it quietly got its relief.

- Kraken vs Binance: Binance is under active U.S. lawsuits; its CEO CZ could face deposition; some countries banned it from derivatives, etc. Kraken looks saintly in comparison – it’s likely considered a model exchange by regulators who want a compliant industry. For example, when Canada forced Binance out, Kraken was the kind of actor they aimed to keep.

- Kraken vs Gemini: Gemini is similarly compliant, but Gemini’s Earn fiasco has drawn action from the SEC (the SEC sued Gemini and Genesis for the unregistered Earn product in Jan 2023; case ongoing). Kraken avoided offering yield products that could be securities (aside from staking, which it resolved). So Kraken now has fewer entanglements.

- Kraken vs new EU competitors: Firms like Bitpanda (in Austria) or Bitstamp are also MiCA-ready, but Kraken’s first-mover license under MiCA is a bragging right.

IPO Thesis and Valuation Analysis

Kraken’s anticipated IPO (targeted for early 2026) will invite investors to value the company’s future cash flows amid a maturing crypto-exchange industry. Here we outline the investment thesis for Kraken’s IPO, the expected timeline and use of proceeds, and conduct a valuation analysis using multiple approaches.

IPO Timing and Market Context: Kraken is reportedly aiming to go public by Q1 2026 (as early as January–March 2026). Management likely chose this timing to allow time to ride the current crypto up-cycle (Bitcoin’s next halving is in 2024, historically leading to a late-2025 bull-market peak) and to differentiate from Coinbase’s direct listing, which came mid-cycle in April 2021. By 2026, Kraken will have a solid year of post-bull financials to show, hopefully smoothing out volatility. The IPO is expected to be a traditional listing (probably on NASDAQ), potentially preceded by a private fundraising (the ongoing $500 million round at $15 billion) to shore up the balance sheet. The broader stock-market environment by 2026 (and appetite for crypto equities) will influence Kraken’s valuation; current indications (2025) show renewed institutional interest in crypto (Bitcoin ETFs, etc.), which bodes well.

Use of Proceeds: While Kraken has not publicly detailed IPO proceeds usage, we can infer priorities:

- Growth Capital: Kraken might raise, say, $1–2 billion gross in the IPO (depending on market cap and float), which could fund further acquisitions (Kraken has been acquisitive – future targets might include smaller exchanges in emerging markets, tech solutions, or infrastructure companies to enhance Prime services).

- Technology and Product Expansion: Proceeds could bolster Kraken Bank’s launch, including regulatory-capital requirements for the bank, and scaling the payments business. Also continued product R&D (perhaps moving into areas like DeFi integration, self-custody tech, or more mobile features).

- Geographic Expansion: With more regulatory clarity, Kraken may re-enter markets it left (Japan, perhaps India if laws change) or strengthen presence where it sees opportunity (MENA region, Latin America).

- Balance Sheet and Reserves: As a public company, Kraken might want a strong balance sheet as a competitive advantage – for example, maintain a large war-chest to assure clients (like a bank-capital buffer) and to underwrite any contingent liabilities.

- Secondary Liquidity: Some portion of the IPO likely allows early investors and employees to cash out. Kraken’s early VCs (Hummingbird, Blockchain Capital, etc.) have been invested for nearly a decade; they will want liquidity. Jesse Powell, as founder, might also diversify some holdings but likely will remain a significant holder post-IPO (similar to how Coinbase’s CEO kept a large stake but also sold some). Given Kraken’s relatively small total primary fundraising ($27 million historically plus whatever came in 2022–25), most shareholders’ ROI comes at IPO.

Latest Private Valuation ($15 billion): The current indicative valuation is $15 billion post-money, per July 2025 reports. This is up ~36 % from the $11 billion last known valuation in 2022, reflecting Kraken’s 2024 financial upswing. At $15 billion, Kraken’s price-to-sales ratio (P/S) on 2024 revenue is 10.0 × – substantially higher than Coinbase’s ~8 × for 2024 – implying investors foresee higher growth or are assigning a premium for Kraken’s private status. However, private valuations often factor forward growth; Kraken’s implied 2025 forward P/S might be closer to ~7 × if revenue reaches ~$2.1 billion (an illustrative ~40 % YoY-growth scenario).

In terms of Enterprise Value/EBITDA, using 2024 EBITDA of $424 million, $15 billion equates to ~35 × EV/EBITDA. That is rich compared with traditional exchanges (for instance, CME Group trades around 25 ×), and richer than Coinbase’s ~16 × 2024 EBITDA. This suggests either optimism about Kraken’s margin expansion or a willingness to pay a premium for the sector’s potential. If Kraken’s EBITDA margin improves into 2025–26 (say it can hit $600 million by 2025 through operating leverage), then a $15 billion valuation would drop to ~25 × forward EBITDA.

Let’s benchmark Kraken against Coinbase and Binance more directly:

- Coinbase (COIN): For FY 2024, Coinbase posted $6.29 billion revenue (up 115 % YoY) and $3.3 billion adjusted EBITDA. Coinbase’s market cap in mid-2025 has fluctuated (it fell to ~$10 billion in 2022, but by 2025 with crypto’s revival, it increased dramatically – some reports put it at $54 billion in January 2025 and others have cited $97 billion for peak or fully-diluted figures). Using the $54 billion figure, Coinbase’s P/S is 8.6 × and EV/EBITDA ~16.4 ×. Public-market pricing of Coinbase is thus lower than Kraken’s implied private multiple, possibly due to SEC litigation or simply public-market discounting; Kraken must justify a double-digit sales multiple by arguing its growth and profit trajectory.

- Binance: Binance is not public, but disclosures and outside analyses give estimates. Binance self-reported $16.8 billion revenue for 2024, +40 % YoY, whereas Bloomberg estimated only $9.8 billion trailing-twelve-month revenue, applying a discount for potential overstatement. Applying Kraken’s 10 × P/S to Binance’s self-reported number yields ~$168 billion, while even a more conservative haircut suggests >$100 billion. Bloomberg’s method yielded ~$58 billion. The wide range highlights uncertainty and legal-risk discounts. If Kraken lists publicly, investors may pay a premium for Kraken as a safer, more transparent proxy for the sector.

User-Based Valuation: At $15 billion and roughly 15 million customers, Kraken is valued at ~$1,000 per customer (or ~$3,400 per funded account). Coinbase’s 110 million verified users at ~$20 billion market cap equate to ~$182 per user, but its ~8 million monthly transacting users imply ~$2,500 per active user. Binance’s ~275 million registered users at an imputed $100 billion value equate to ~$364 per user. Kraken’s high revenue per user (its clientele skews toward heavy traders) implies each user is “worth” more. If Kraken doubles its user base while maintaining ARPU, that metric would normalize toward peers.

Scenario Analysis:

- Bull Case: Crypto markets thrive through 2025. Kraken’s FY 2025 revenue reaches ~$2.2 billion (+45 %), FY 2026 revenue ~$3.0 billion (+36 %). EBITDA margins ~30 % yield 2025 EBITDA ~$660 million and 2026 ~$900 million. Valued at 10 × sales or 20 × forward EBITDA, Kraken could reach $18–25 billion at IPO.

- Base Case: Moderate growth. FY 2025 revenue ~$1.8 billion (+20 %), FY 2026 ~$2.0 billion (+11 %). EBITDA margins 25–30 % give 2025 EBITDA ~$450 million and 2026 ~$500–600 million. Valued around 8 × sales or 25 × EBITDA, Kraken centers near $14–16 billion – matching its current private mark.

- Bear Case: Crypto downturn in 2025. FY 2025 revenue falls to ~$1.0 billion, EBITDA margin slips to

15 % ($150 million). At a 5 × sales multiple, Kraken would be worth ~$5 billion; in this scenario Kraken would likely postpone the IPO.

Comparable Multiples: Traditional exchanges such as CME trade near 12 × EV/EBITDA and 12 × revenue; ICE trades ~16 × EV/EBITDA and 6 × revenue. Crypto exchanges carry higher multiples owing to growth and risk. If listed, Kraken may market itself as a high-growth fintech stock benefiting from digital-asset adoption, with scarcity value (few large crypto exchanges will be public).

Valuation via User/Volume Metrics: Coinbase’s $6.3 billion revenue on $1.3 trillion volume implies a 0.48 % average fee. Kraken’s $1.5 billion on $665 billion volume implies ~0.23 %. Kraken’s enterprise value of $15 billion is roughly 2 % of annual volume; Coinbase’s is ~1.5 % and a hypothetical $60 billion Binance would be ~0.8 %. Kraken’s higher EV/volume is acceptable if it can push ARPU higher by increasing retail share.

Latest Raise Signaling: A $500 million raise at $15 billion would set a valuation floor headed into IPO and bolster Kraken’s balance sheet. Incoming investors expect a markup; the cash adds resilience, letting Kraken avoid a secondary offering anytime soon.

Potential IPO Risks (Valuation-wise):

- Dependence on crypto-asset prices.

- Regulatory uncertainty (though clarity is improving).

- Competition from DeFi and zero-fee platforms.

- Public-market discount once private-market froth disappears.

Valuation Summary:

- 2024 actuals: 10 × sales or 35 × EBITDA → $15 billion.

- 2025 forward (growth): 7–8 × sales or 20–25 × EBITDA still centers near $15 billion.

- Coinbase at $20 billion trades ~3 × 2024 sales; if Coinbase rebounds to 5–6 ×, Kraken at 7–8 × is plausible given faster growth.

Enterprise Value per Active User: $3,000–4,000 for Kraken (4.4 million funded accounts) versus $2,500 for Coinbase (8 million MTUs). Using total users, Kraken’s ~$1 k per user exceeds Binance’s ~$300 but reflects higher monetization; on a per high-value user basis, Kraken may be cheaper.

Related insights4vc research: read our Revolut digital-assets strategy, crypto venture capital in early 2026, and Crypto Venture Capital 2026.

Sources

- https://www.cftc.gov/PressRoom/PressReleases/8433-21#:~:text=Washington%2C D,S

- https://blog.kraken.com/news/kraken-q2-2025-financials

- https://fxnewsgroup.com/forex-news/retail-forex/kraken-expanding-beyond-crypto-trading-with-1-5b-ninjatrader-buy-wsj/

Risk Disclaimer:

insights4vc and its newsletter provide research and information for educational purposes only and should not be taken as any form of professional advice. We do not advocate for any investment actions, including buying, selling, or holding digital assets.

The content reflects only the writer’s views and not financial advice. Please conduct your own due diligence before engaging with digital assets or related technologies, as they carry high risks and values can fluctuate significantly.

Note: This research paper is not sponsored by any of the mentioned companies.