The most valuable works in the art market are often not publicly for sale, not transparently priced, and not easily verified by outsiders. Yet they can move hundreds of millions of dollars, secure private-bank loans, anchor museum narratives, and define cultural status for billionaires. Larry Gagosian built his empire inside that contradiction. He is best understood not as a colourful biographical figure, or even simply as the most famous dealer of his generation, but as one of the clearest operating models for the contemporary high-end art market: a system in which trust, access, scarcity, scholarship, private liquidity, and social power are converted into price.

That framing matters because the art market is often misdescribed in both directions. One simplification treats art as a noble cultural sphere contaminated by money. Another reduces it to a speculative asset with decorative utility. Neither is adequate. At the top end, art is a hybrid market in which culture, status, scarcity, finance, and private relationships are inseparable. The language of genius, connoisseurship, museums, scholarship, and patronage sits directly on top of a hard private-market logic of sourcing, distribution, signalling, financing, and liquidity management.

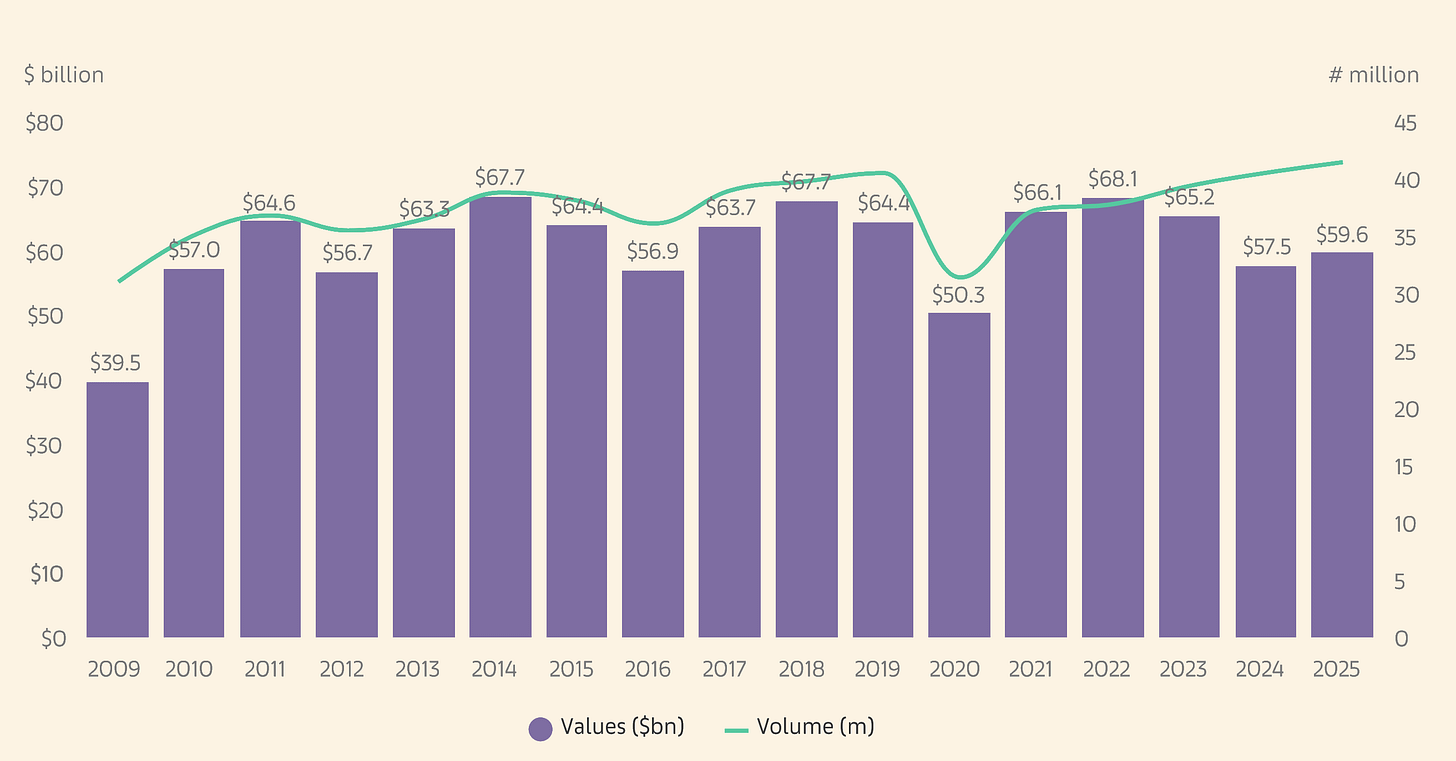

Sales in the Global Art Market 2009–2025

The 2026 edition of the Art Basel and UBS Global Art Market Report estimated global art sales at $59.6 billion in 2025, up 4% after a difficult 2024. Dealer sales rose 2% to $34.8 billion, public auction sales rose 9% to $20.7 billion, and reported private auction-house sales fell 5% to just under $4.2 billion. Growth was concentrated at the top end, with auction sales above $10 million rising 30% in 2025 after a sharp contraction in 2024. The recovery was real, but uneven, and still below the 2022 peak.

Gagosian’s own platform sits exactly where those forces meet. According to the gallery’s official materials, Gagosian now operates eighteen exhibition spaces across the US, Europe, and Asia, employs more than three hundred people, and has published more than six hundred titles. In 2023, Patrick Radden Keefe reported in The New Yorker that the business generated more than $1 billion in annual revenue, controlled more than 200,000 square feet of prime real estate, and had more exhibition space than most museums. Even if the revenue figure is treated as reported rather than audited, the scale is enough to make the point: Gagosian built a gallery network that functions as a distribution platform, a scarcity machine, a client-acquisition engine, a branding system, and, at moments, a private liquidity venue.

This is also why the debate over whether art is an “asset class” is usually framed too crudely. Art is not a single asset class in the way that sovereign bonds, listed equities, or office real estate are. It is closer to a federation of overlapping submarkets with radically different liquidity, fee structures, buyer bases, information quality, condition risk, tax treatment, and legal complexity. The investable zone is narrow and highly conditional. A museum-quality work by a canonical artist with deep institutional support, clean title, excellent condition, and strong comparables behaves very differently from a fashionable mid-career painting sold at a fair, an emerging-artist primary work, a print, or a digital collectible. The top of the market can function as collateral and, at times, as a store of value. That does not make the whole ecosystem a reliable investment universe.

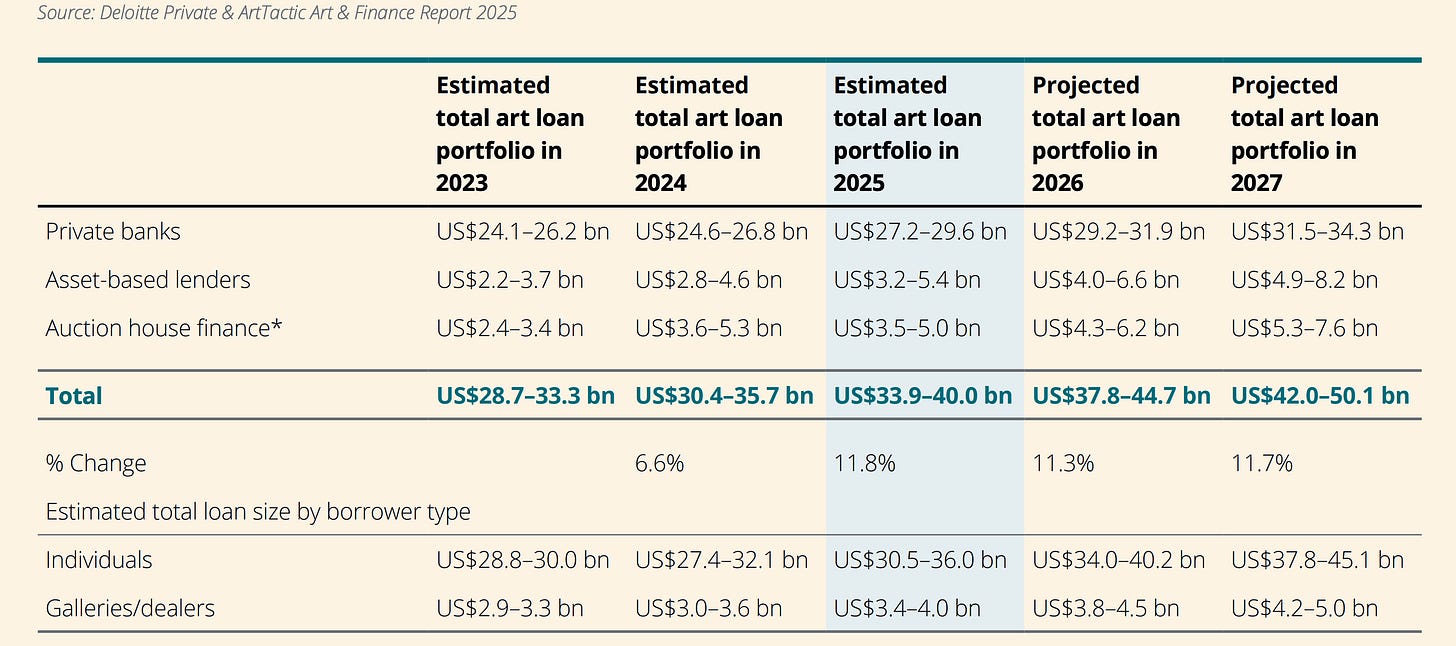

The financial side of the market is now too large to ignore. The latest Deloitte and ArtTactic Art & Finance research describes a market in which art-related wealth management has become mainstream inside private-client businesses, with 51% of wealth managers offering art-related services, up sharply since 2011. The same report, as summarised by the Financial Times, put the art-backed loan market at $33.9 billion to $40.0 billion in 2025 and projected $42.0 billion to $50.1 billion by 2027. At the same time, 50% of non-bank lenders reported defaults in 2024, while private banks in the survey reported none. That divergence reveals a central truth: the safest art loan is often not underwritten against the object alone, but against the borrower’s broader balance sheet and private-banking relationship.

The next question is whether onchain infrastructure changes anything meaningful. The answer is yes, but not in the way the most promotional narratives imagined in 2021. The most plausible impact is not that blue-chip galleries are replaced by retail tokenisation platforms, or that elite collectors suddenly prefer transparent blockchain registries to private discretion. The stronger thesis is that selected layers of the market, especially provenance support, digital certificates, title-adjacent records, rights administration, settlement, and parts of lending and collateral management, become more standardised, more interoperable, and in some cases selectively onchain. The art market will not be rebuilt on public ledgers overnight. But parts of its hidden operating system may become more machine-readable.

Joseph Duveen, Leo Castelli, and the prehistory of Gagosian

The modern template for selling expensive art to new wealth begins with Duveen. His famous observation, repeated for more than a century because it remains structurally true, was that Europe had a great deal of art and America had a great deal of money. But the enduring lesson is not the geographic arbitrage alone. Duveen sold reassurance. He sold social translation. He sold the feeling that industrial or financial wealth could be upgraded into civilisation, lineage, and legitimacy by owning the right objects, authenticated by the right experts, displayed in the right rooms, and later ratified by museums. His genius lay in understanding that many buyers were not paying merely for paintings. They were paying to reduce insecurity.

Joseph Duveen

Duveen’s system had several components that still matter. He treated price as part of the theatre of value, not merely as the result of value. The Lévy Gorvy essay, reflecting on the classic Duveen corpus, describes his “economy of scarcity” and his willingness to use premium pricing itself as evidence of importance. He also institutionalised the use of scholarly authority as commercial infrastructure, most famously in his long and lucrative relationship with Bernard Berenson. As Adam Gopnik writes in his essay on Duveen and Berenson, what Berenson supplied was not just connoisseurship but order, glamour, and a taxonomy through which uncertain objects could become marketable masterpieces. The combination of expert authority and elite client management remains one of the permanent operating logics of the top market.

If Duveen’s market was driven by old masters, old money, and old authority, Castelli transformed the dealer model for living artists. He did not merely redistribute canonical works from one wealthy owner to another. He assembled rosters, built careers, protected prices, placed work with museums and influential collectors, and normalised the idea that a gallery was not just a shop but a long-horizon career manager and network node. Artsy’s overview of Castelli is useful here: it describes him as the first to assemble a stable of boundary-pushing artists and market them as brands, effectively defining the modern concept of gallery representation. He also pioneered cross-city and cross-Atlantic dealer partnerships, greatly widening distribution for postwar American art.

Leo Castelli, Ivan Karp, Andy Warhol

The so-called “Leo Castelli model” rested on mutual trust and long duration. Castelli supported artists with stipends, studio support, and active market management, often continuing to subsidise them even when inventory was slow or debt mounted. That model only works when the dealer believes that long-term institutional and collector demand can be cultivated more effectively than short-term opportunism can be monetised. It is an artist-centred system, even when it remains commercial. It also depends on the dealer’s ability to choreograph museums, critics, collectors, and peer galleries into a reinforcing loop of legitimacy.

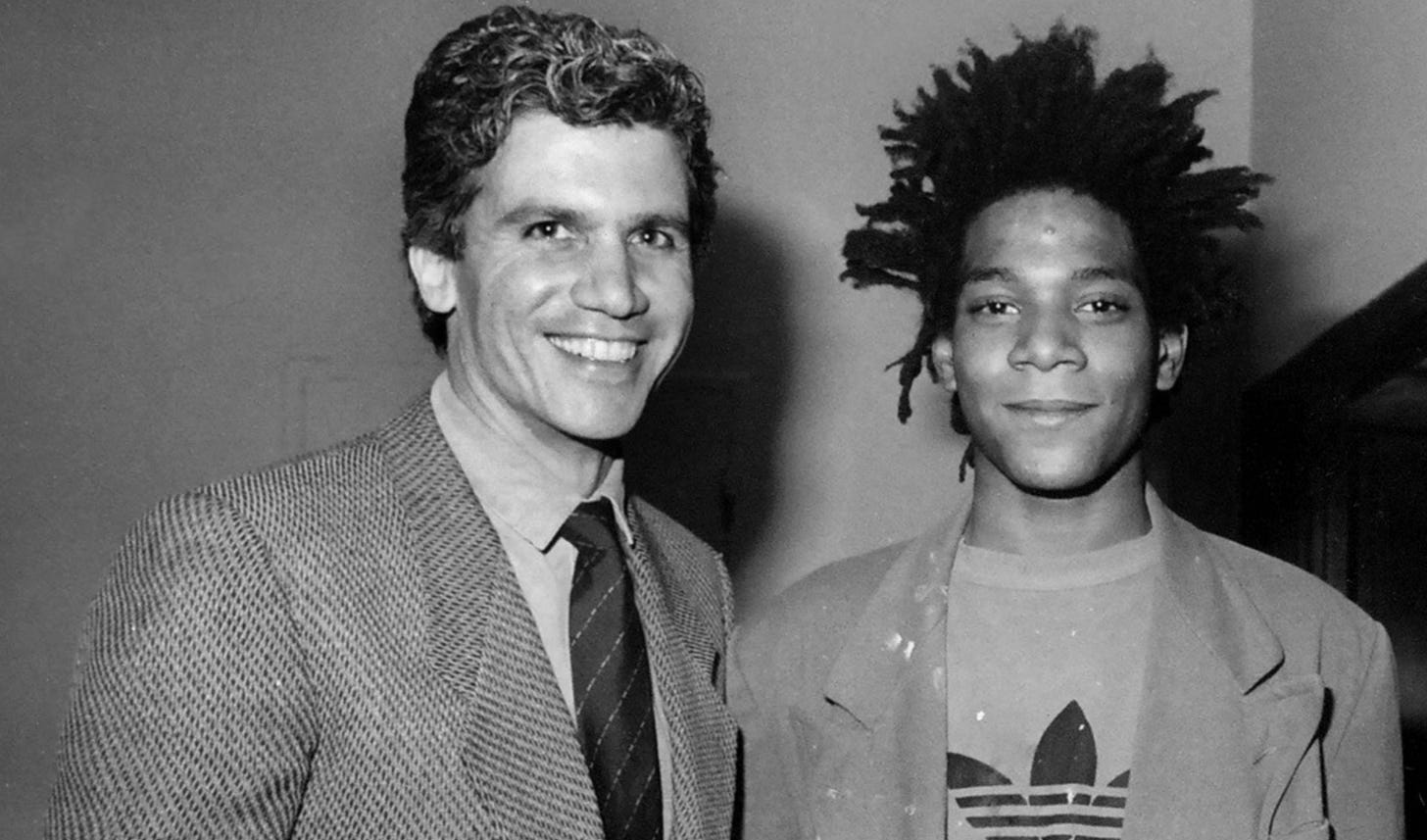

Gagosian inherited pieces of both systems and fused them into something more aggressive and more scalable. From Duveen he took the ultra-wealthy client logic, the social drama of acquisition, the premium attached to access, and the insight that many buyers are paying against status anxiety as much as against aesthetic conviction. Keefe’s profile explicitly places Gagosian in Duveen’s tradition and notes that Gagosian himself read Duveen biographies closely. From Castelli he absorbed the importance of artists, institutions, collectors, and the choreography of legitimisation, as well as the value of a trusted client list. Castelli introduced him to the photographer Ralph Gibson, later took a liking to him, and crucially connected him to collector circles that included Si Newhouse. Their collaboration even extended to the joint gallery at 65 Thompson Street in SoHo.

But Gagosian did not remain within either historical template. Castelli prioritised the primary market and the shaping of living artists’ careers. Duveen sold dead masters into the collections of industrial titans. Gagosian fused the billionaire-client psychology of Duveen with the artist-and-institution logic of Castelli, then added something distinctly late twentieth century: secondary-market intelligence at scale. That meant knowing where works were, who owned them, which marriage might break down, which estate might sell, which collection needed rebalancing, which billionaire felt under-collected relative to a rival, and which museum-quality work could be coaxed out through a mix of premium pricing, social pressure, and discretion.

This synthesis changed the market’s centre of gravity. With Duveen, the masterpiece’s value lay partly in its oldness and courtly pedigree. With Castelli, value crystallised around the dealer’s role in discovering, supporting, and placing the new. With Gagosian, the highest-value zone became a hybrid field in which primary and secondary, contemporary and historical, commerce and scholarship, exhibition and inventory, collector service and market-making all blur. That hybridisation is one of the core reasons he matters. He did not merely succeed within the high-end art market. He helped reorganise how it works.

What Gagosian actually built

The foundation of the Gagosian model was not connoisseurial pedigree or inherited capital. It was markup discipline. Keefe’s account of the Westwood years is instructive because it is so unromantic. Gagosian observed a street vendor selling cheap posters, copied the business, and then discovered that presentation itself could create margin. A two-dollar poster became a fifteen-dollar item once framed. He then charged small craft sellers rent and commissions. The lesson was basic but durable: aesthetics, display, and framing are not cosmetic to commercial value. They are commercial value. Many years later, Mark Kostabi’s line that “he’s the frame” captured the same logic at a higher level. By then, the Gagosian imprimatur itself justified the premium.

Larry Gagosian & Jean-Michel Basquiat

The second layer was self-education plus audacity. Gagosian had no formal art-historical training, but Keefe’s profile describes stacks of art books by his bed and a rapid learning curve. The cold call to Ralph Gibson captures the method. He saw work he liked in a magazine, called the artist, guaranteed some purchases, flew to New York with a cheque, and turned that move into an introduction to Castelli. This is a repeated pattern in the Gagosian story: he entered networks by behaving as though he already belonged inside them. He did not wait to be credentialled. He acted, and the action itself became credentialling.

The third layer was a pivot away from the part of the market most dealers then considered nobler. Castelli specialised in primary representation. Gagosian lacked artist relationships at the start, but he had access to Los Angeles, to new West Coast money, and to the secondary market. Keefe reports that he often made more than one hundred cold calls a day, hunting for works, locating buyers, and haggling owners into releasing objects that were not formally on the market. This is perhaps the purest description of what he built: an off-market search engine powered by social intelligence, persistence, and the confidence to treat private walls as potential inventory.

That search-engine logic matters because the top of the art market is supply constrained in a very particular way. The most desirable works are usually not listed. They surface through death, divorce, debt, estate planning, collection rotation, or relationship pressure. Keefe quotes Marc Jacobs saying that Gagosian sells things that are not for sale. That is not mere theatre. It describes the economic moat. Anyone can bid on an object once it reaches public auction. The elite dealer’s advantage is to intermediate before public competition begins, or to prevent public competition from beginning at all.

The relationship with Newhouse made this secondary-market detective function strategic. Keefe describes Castelli introducing Gagosian to Newhouse and Gagosian quickly realising the importance of the connection. Newhouse was not just wealthy. He had aesthetic seriousness, collecting ambition, and the ability to buy at the highest level. Keefe’s profile makes clear that Gagosian’s core service to him was not basic advising on new talent. It was sourcing masterpieces on the secondary market, in a world with no central ownership registry and little price transparency. That is where information asymmetry becomes a business model. If you know where exceptional works are, and you know who might sell, and you know which client feels the need to own them, you can earn not just commissions but control over price formation itself.

The fourth layer was the conversion of selling into staging. Gagosian’s official gallery history emphasises museum-quality exhibitions, scholarly publications, and architecture. Keefe sharpens the point. He notes that even critics of Gagosian credit him with popularising museum-quality historical exhibitions in a commercial setting. The gallery did this partly because, as Gagosian put it, “We had no artists!”, but the move evolved into a masterstroke. Historical shows attached the gallery’s name to canonical figures such as Peter Paul Rubens and Pablo Picasso, brought scholars such as John Richardson into its orbit, and created public legitimacy that spilled over into private sales. Keefe reports that some of those exhibitions were effectively advertisements, and that aggressive negotiation often continued in the back room while visitors admired the brushwork out front.

This is the point at which the Gagosian model stops looking like a gallery and starts looking like infrastructure. The exhibition is not only a show. It is also a trust-generating environment. The catalogue is not only scholarship. It is also asset support. The architecture is not only branding. It is also an assurance mechanism for collectors who want to believe they are buying into art history, not merely into inventory. The dinner at the house, the opening dinner, the vernissage, the placement of a work next to museum loans, the fact that the same platform can sell a living painter, stage a historic Picasso exhibition, and advise on a secondary-market acquisition, all of this collapses the distance between commerce and legitimacy.

The fifth layer was geographic scale as signalling. Officially, Gagosian now spans eighteen exhibition spaces. Keefe described nineteen galleries in 2023 and more than 200,000 square feet, with the line that “the sun never sets on my gallery.” The precise count is less important than what the real estate communicates. Expansion in this context is not merely distribution. It is proof of permanence, proof of access to artists and collectors across time zones, and proof that the gallery can compete with museums as a site of cultural serious-mindedness. A collector does not just buy a painting from a room. He or she buys from a regime of visibility and institutional adjacency.

The sixth layer was brand premium. Keefe reports that Gagosian can charge meaningful commissions on secondary sales and that his endorsement alone may enhance a work’s value. Other dealers told Keefe that collectors often knowingly pay more through Gagosian and accept less transparency because the purchase carries a trust premium. That premium is not irrational. In a market where authenticity, condition, quality within an artist’s oeuvre, and future resale prospects matter immensely, buying through the market’s most powerful dealer can function as a form of risk compression. It is expensive. But it can be rationally expensive.

The seventh layer was social inversion. Keefe’s most penetrating observation is that Gagosian became so successful selling to the ultra-rich that he became an aspirational figure to them. That is more than gossip. It explains why status anxiety among wealthy buyers can be monetised so effectively in art. The billionaire who can buy a jet or a penthouse on pure financial power still cannot, by money alone, buy cultural ease, insider access, or the appearance of cultivated certainty. Gagosian’s dinners, houses, parties, contacts, and studio access became part of the offer. The object on the wall came bundled with a social script.

There are, however, fragilities in this architecture. It is heavily founder-led, highly relationship-dependent, and unusually reliant on tacit knowledge rather than transparent systems. Keefe reported that the business was owned by Gagosian without a partner or shareholder. He also described a management culture in which directors were largely told to sell, with little mentoring and limited formal process. One can infer from that structure that succession is not a trivial governance issue but a central strategic risk. The moat is real, yet much of it lives in one man’s memory, instincts, contacts, and authority. That is very powerful. It is also difficult to institutionalise.

What Gagosian built, then, was not a gallery in the ordinary sense. He built a market-making platform that integrates sourcing, scholarship, architecture, private sales, status theatre, institutional signalling, and cross-border client capture. It works because all of those elements reinforce each other. It is fragile because a surprisingly large share of the reinforcement still depends on human trust concentrated around a founder rather than around standardised market infrastructure. That tension, between bespoke power and scalable systems, is the hinge on which the next fifteen years may turn.

How the high-end art market works

The first analytical mistake in discussing the art market is to talk about it as if it were singular. It is better seen as a stack of partially connected submarkets. The primary market concerns first sales from artists or their representing galleries. The secondary market concerns resale of already-owned works through galleries, private dealers, advisors, auction houses, estates, and occasionally directly between collectors. In practice, the top of the market blurs these boundaries: mega-galleries operate in both primary and secondary; auction houses do significant private dealing; advisors source in both directions; estates can shape both supply and scarcity; museums and curators alter market outcomes without directly pricing works.

The scale and mix of those channels continue to shift. In 2025, the Art Basel and UBS report estimated dealer sales at $34.8 billion, public auction sales at $20.7 billion, and reported private auction-house sales at just under $4.2 billion. In 2024, during the downturn, public auction sales plunged 25% while private auction-house sales rose 14% to $4.4 billion, which is an important reminder that visible public prices and the broader liquidity of the market can move in opposite directions. When confidence is fragile, participants often prefer the discretion of private transactions.

At the house level, that private layer is already large. Christie’s projected $6.2 billion in global sales for 2025, including $1.5 billion of private sales, roughly a quarter of the total. A Christie’s profile of its private-sales division says the team executed the equivalent of four transactions a day in 2025 through an international network of five hundred specialists. Sotheby’s projected $7.0 billion in 2025 sales, including $1.2 billion in private sales. In other words, even the most public brands in the art trade now do a great deal of business in the dark.

Price formation in this environment is therefore only partially transparent. Auction prices are observable, but they are not neutral. They are shaped by guarantees, reserve prices, irrevocable bids, lot selection, catalogue language, timing, currency conditions, and the willingness of consignors to risk failure. Private prices are often undisclosed, or disclosed only selectively and strategically. The result is that “the market price” of a work is often an estimate constructed from partial comparables, private whispers, specialist judgement, and the object’s particular characteristics. Those characteristics include provenance, condition, scale, date, subject matter, exhibition history, literature, catalogue raisonné inclusion, institutional ownership history, and the quality of the specific work within the artist’s overall production.

Courts have repeatedly recognised that this is not a market with easy objective value. The Perelman litigation against Gagosian was revealing not because it proved dealer malfeasance, but because the courts were unsympathetic to the idea that a sophisticated art buyer in negotiated arm’s-length transactions could easily rely on a precise notion of “fair market value.” Commentary on the case notes that New York courts stressed the absence of a fiduciary relationship and the lack of a singular objective market value for non-fungible works in an inefficient market. That is not a side issue. It is one of the system’s defining features.

Fees magnify the frictions. Christie’s current buyer’s premium, effective September 2025, is 27% up to $1.5 million, 22% from $1.5 million to $8 million, and 15% above $8 million in New York, with similar structures across major sale sites. Sotheby’s, updated in February 2026, charges 28% up to $2 million, 22% between $2 million and $8 million, and 15% above $8 million in New York, with equivalent thresholds in London, Paris, Hong Kong, and elsewhere. On top of that come seller’s commissions, negotiated or waived house-by-house; shipping; insurance; storage; conservation; taxes; possibly artist resale royalties; legal due diligence; and advisory fees. These costs are why gross auction headlines should almost never be confused with investor returns.

The top end also behaves differently from the mid-market because wealth concentration matters more than broad participation. The 2024 downturn was driven largely by cooling above $10 million, where the number of fine-art works sold at auction fell sharply. By contrast, lower-priced segments remained resilient, with growth in volumes and in some sub-$50,000 slices. In 2025, that relationship partially reversed at the top. Public auction sales above $10 million rose 30%, and sales above $1 million rose 21%, while lower-priced segments were weaker. This is the core reason broad statements such as “the art market is up” or “the art market is down” are often analytically useless. The trophy market and the middle market can move in different directions at the same time.

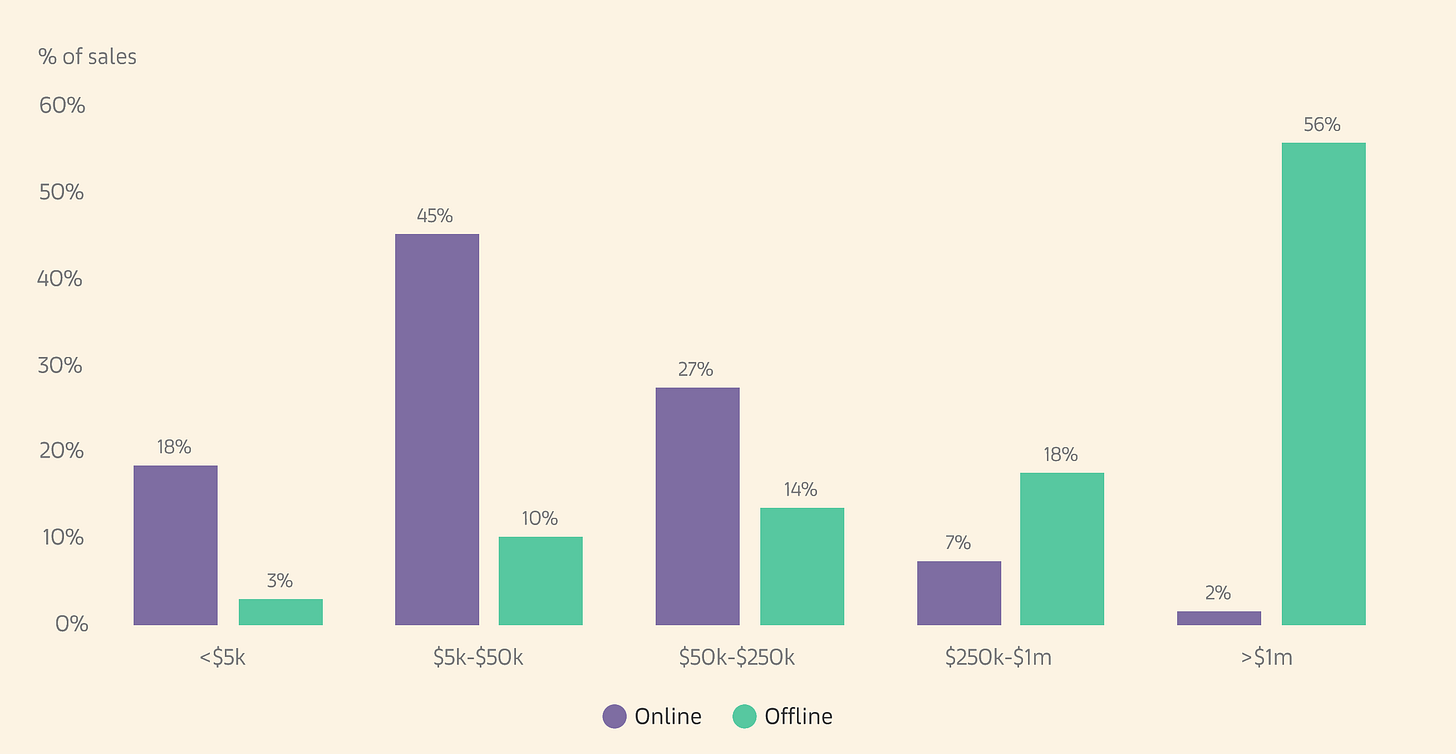

Dealers and fairs sit inside this segmentation in an equally uneven way. In 2024, dealers with turnover under $250,000 posted a 17% sales increase, while those over $10 million saw a 9% decline. In 2025, sales below $500,000 remained strong, and top-end dealers returned to modest growth. Art fairs also remain central to discovery and client acquisition: Art Basel and UBS found that, in 2025, 58% of HNW collectors made purchases linked to fairs, up from 39% in 2023, while dealers said nearly half their buyers were new to their business. This suggests a market in which in-person aggregation still matters intensely, even as online and social channels broaden discovery.

Share of the Value of Online Versus Offline Sales in Fine Art Auctions by Price Segment 2025

The upshot is that the high-end art market is best understood as a relationship-driven private market with selective public price revelation. Galleries allocate access, auction houses create pricing events, advisors broker interpretation and discretion, museums confer legitimacy, estates manage scarcity, and collectors use art both as cultural speech and as balance-sheet substance. In such a market, opacity is not merely a defect to be solved. For many participants, especially at the top, it is a feature that preserves flexibility, prestige, and advantage.

Is art an asset class

The intellectually serious answer is that art is investable in a narrow, access-dependent, segment-specific sense, but it is not a clean asset class in the way allocators normally use that term. What most people call “art” bundles together objects with wildly different liquidity, durability, market depth, fee drag, and data quality. A seventeenth-century painting with contested attribution, a museum-exhibited Richter, a primary-market painting by an emerging twenty-eight-year-old, an editioned print, and a generative artwork on-chain do not belong in one asset bucket simply because they are all sold through the culture industry.

The older academic literature was often read too optimistically. Jianping Mei and Michael Moses, using repeat-sales data from 1875 to 2000, found that art outperformed fixed income but underperformed US equities, with lower correlation to other assets and thus some diversification value. Luc Renneboog and Christophe Spaenjers, using a much larger hedonic data set of paintings and works on paper, estimated real annual appreciation of 3.97% in US dollar terms between 1957 and 2007, similar to corporate bonds but with substantially higher risk. Those findings are serious and useful, but they do not justify the slogan that art is a straightforward portfolio substitute for listed assets.

More recent work became more sceptical for good reason. Arthur Korteweg, Roman Kräussl, and Patrick Verwijmeren showed that repeat-sales data are selection biased because assets trade endogenously. Once they corrected for that bias, annual returns in their sample fell from 8.7% to 6.3% and the Sharpe ratio collapsed from 0.27 to 0.11. That is one of the most important findings in art-finance research because it aligns with lived market reality: the works most likely to reappear publicly are not a random sample of everything owned. Better works can be tightly held; weaker works may be sold; and unsold objects often disappear from reported datasets entirely.

The 2026 short-term evidence is a useful reality check. Barron’s reported that Mei and Moses’s first-quarter 2026 repeat-sales work showed a mean compound annual return of 1.7% for works sold at the major houses, an improvement from the dismal 2024 environment. Yet 47% of the observed repeat-sales still produced negative returns, and about 25% of works with repeat-sale histories did not sell. That is exactly how a lumpy, fee-heavy, highly selective market behaves. Some owners do very well. Many do not. The average glosses over a painful distribution.

This is why the segments matter so much. Trophy works by canonical artists can behave like portable wealth, especially when they are of exceptional quality and kept for long periods. Blue-chip works with deep institutional support and broad collector demand are the most plausibly investable part of the market. Estates with disciplined supply and strong museum validation can also sustain value. But the “blue-chip” label itself is often abused. Emerging artists can experience violent boom-bust cycles. Mid-market works may suffer from weak liquidity and high transaction costs. Editions can offer accessibility but often carry thinner upside once costs are included. Digital works can have strong cultural importance while still being financially unstable.

Access and quality discrimination explain much of the apparent outperformance when it occurs. The wealthy buyer with first look at the right primary allocation, experienced advisors, tax planning, long holding periods, and the ability never to be a forced seller operates in a different universe from the investor buying whatever headlines suggest is “hot.” The asset does not determine the result on its own. The network around the asset does. This is one reason the line “buy what you love” persists. It is not rigorous investment advice, but it is a shorthand warning against entering an opaque, expert-intensive market under the illusion that passion and price are easily separable.

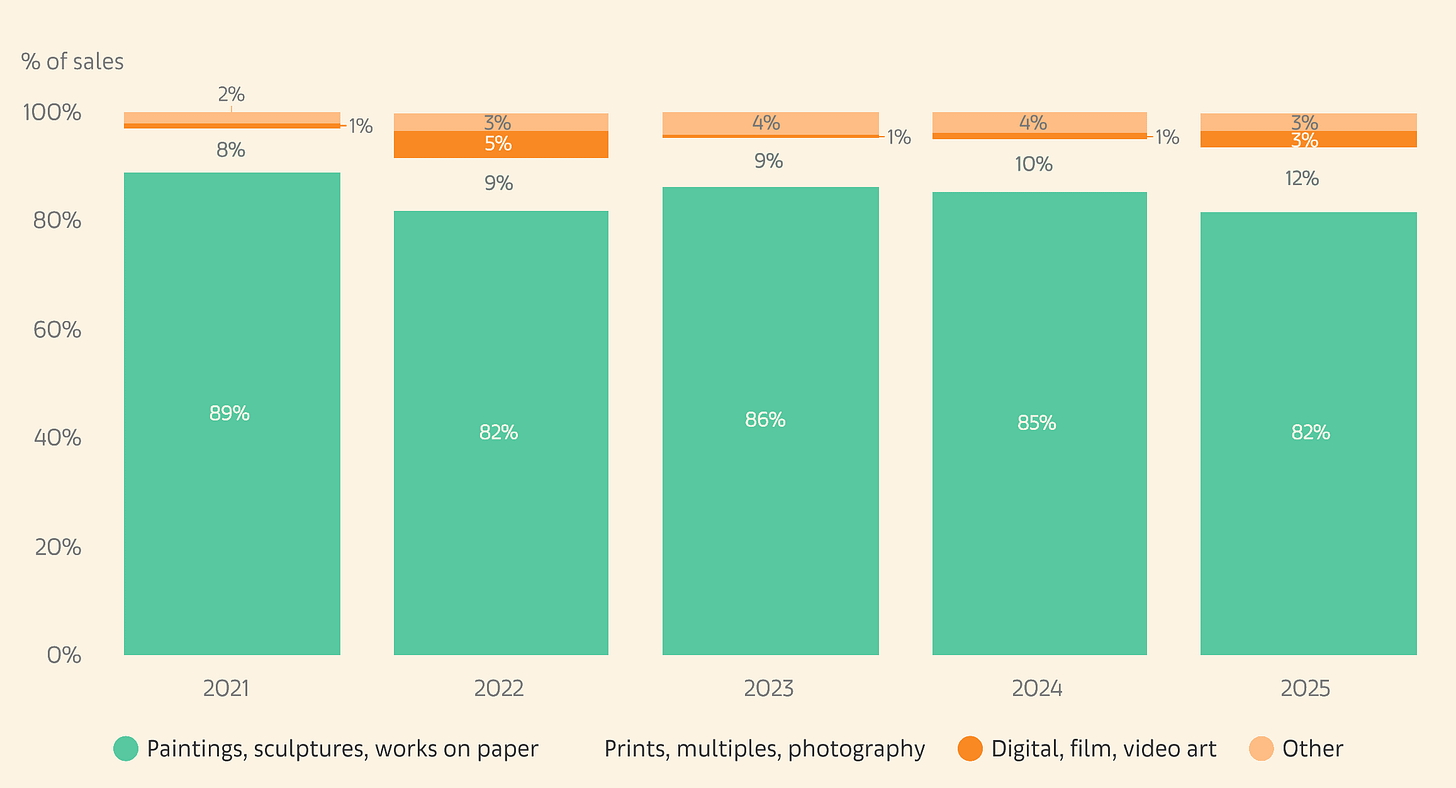

Dealer Sales by Medium 2021–2025 (Digital art in 2025: 0.4%)

A further complication is that many wealthy collectors do not treat art allocation the way institutional allocators treat capital allocation. The 2025 Art Basel and UBS collector survey found that HNW respondents said they allocated an average of 20% of wealth to art, rising to 28% among those above $50 million and 26% for Gen Z collectors. Those numbers are striking and should be read as behavioural evidence rather than portfolio-optimisation proof. They show that art matters deeply in wealthy balance sheets and identity formation. They do not show that the category is efficiently priced or institutionally replicable.

The correct conclusion, then, is sceptical but not dismissive. Art is not mostly a financial asset pretending to be culture. Nor is it mostly culture pretending not to be financial. In a narrow blue-chip segment, under conditions of access, patience, quality control, and low leverage, it can function as a store of value and a source of occasional outsized gains. In the broader market, however, fees, illiquidity, tax friction, selection bias, information asymmetry, and adverse selection mean that many buyers are participating primarily in a consumption-and-status market with uncertain financial upside.

Luxury Collectibles Are Stabilising, But Selectively

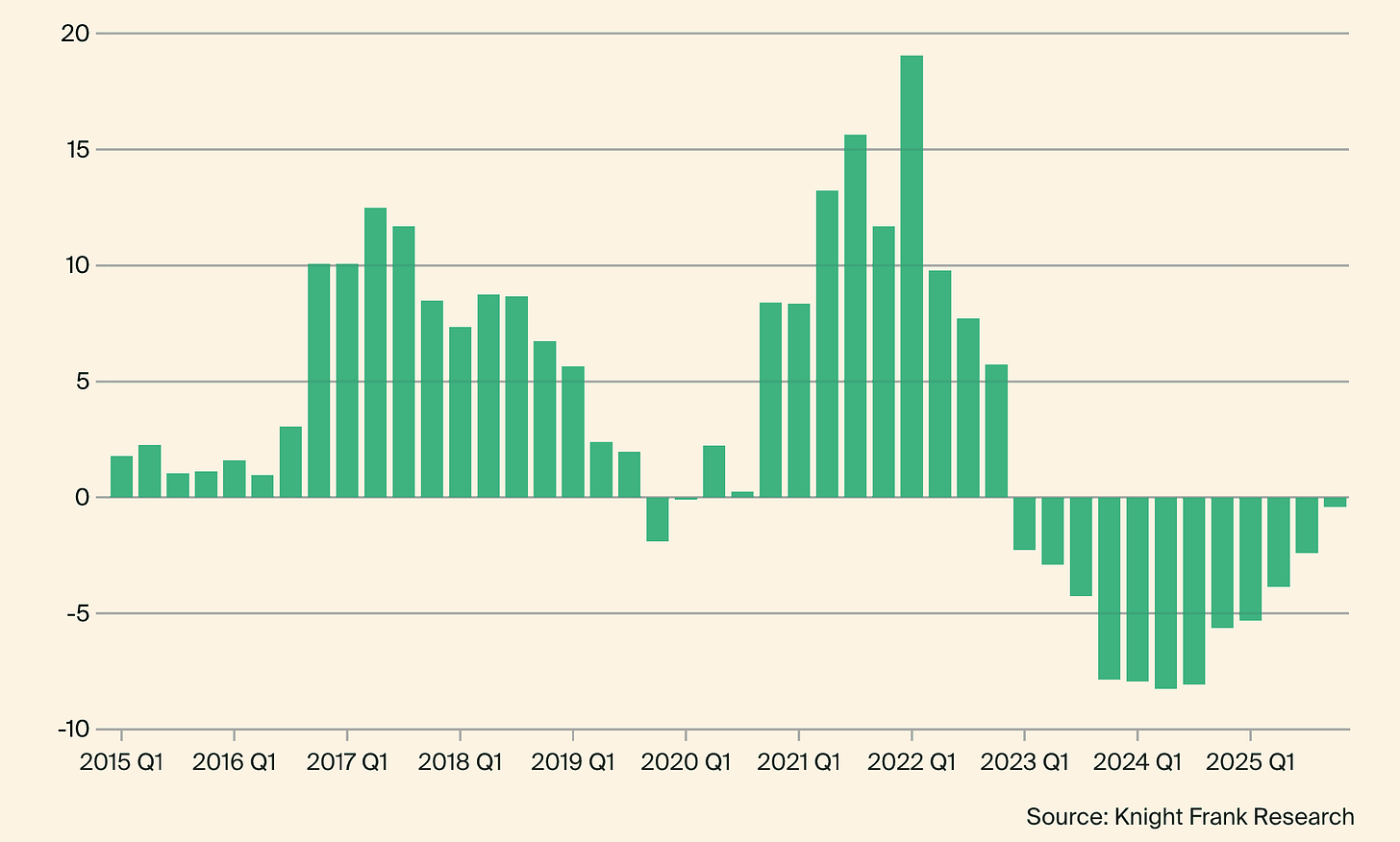

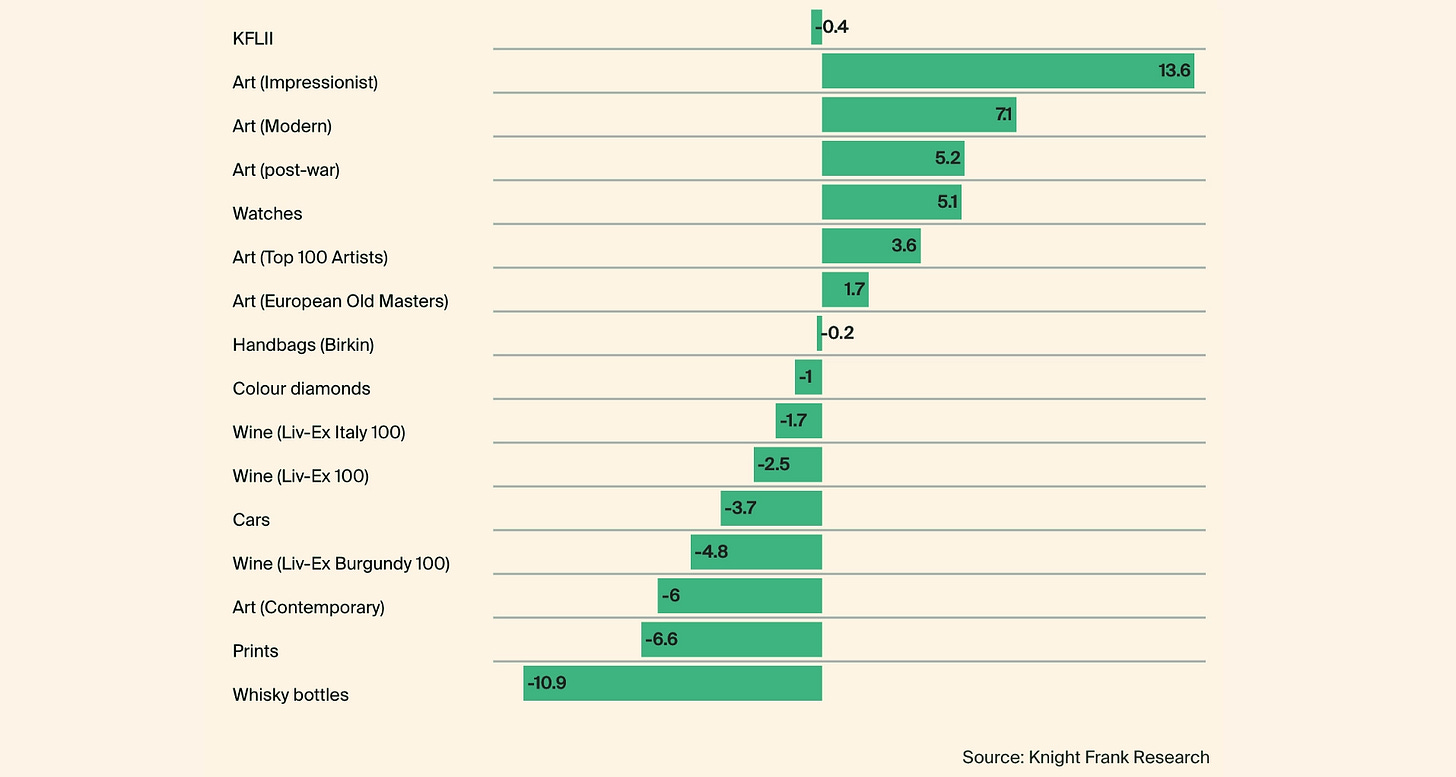

Knight Frank’s 2026 Luxury Investment Index is useful because it places art inside the broader world of passion assets rather than treating it in isolation. The index closed 2025 down only 0.4%, after two difficult years, while remaining up 38.6% over the past decade, which suggests stabilisation rather than a full recovery. The important point is that performance has become highly selective. Impressionist art rose 13.6% over twelve months, modern art gained 7.1%, post-war art rose 5.2%, and the Top 100 artists index was up 3.6%, while contemporary art fell 6.0% and prints declined 6.6%.

A volatile decade in luxury investment (KFLII annual % change)

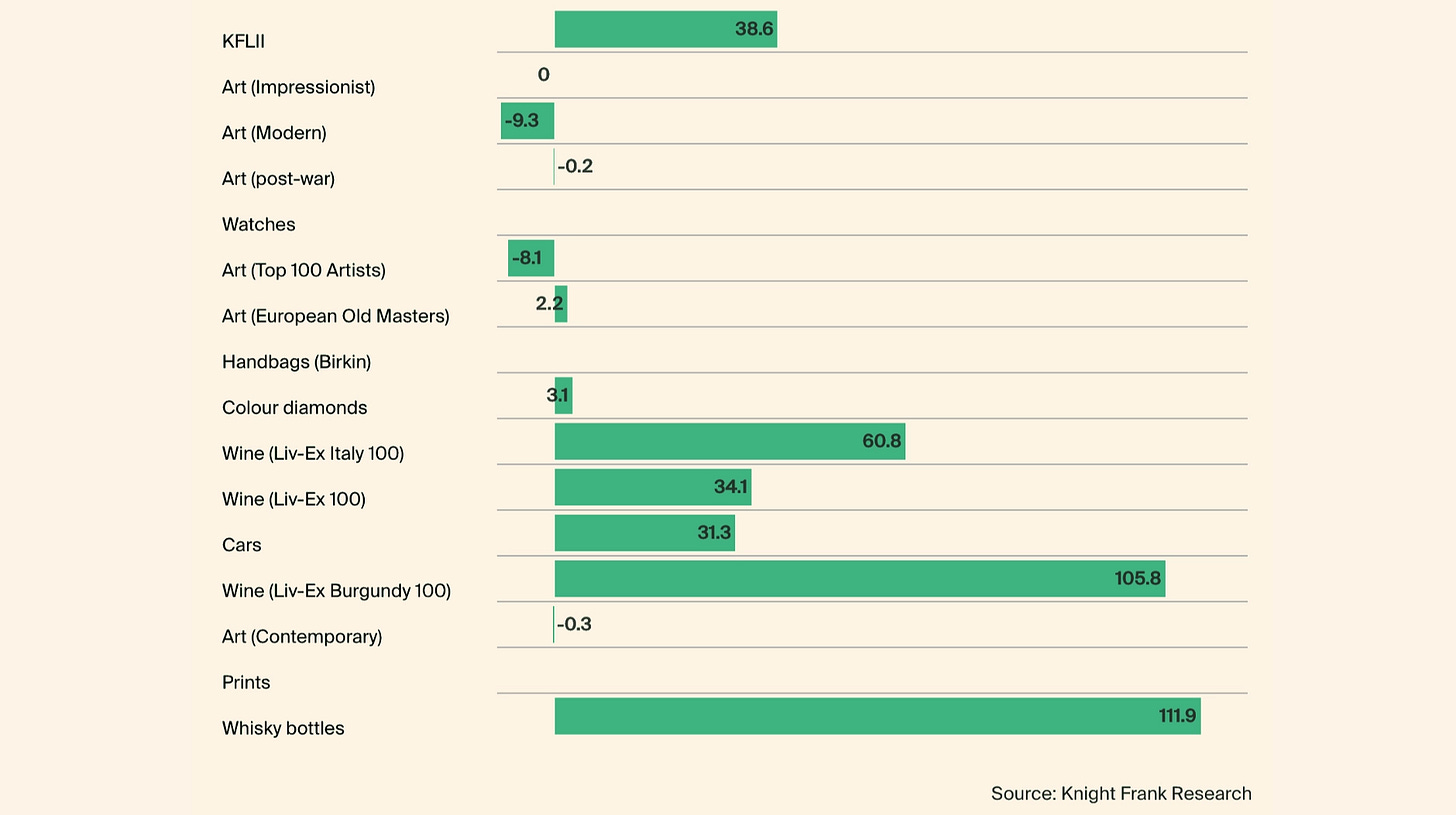

This reinforces a broader pattern visible across the art market: buyers are still active, but they are more disciplined and are favouring rarity, quality, provenance, and recognisable names over broad exposure. It also shows why “art” cannot be analysed as one uniform market, because different periods, artists, and formats are moving in different directions at the same time. Compared with other luxury assets, art’s short-term recovery looks real but uneven: watches rose 5.1%, while classic cars, wine, whisky bottles, and colour diamonds all declined over twelve months. The ten-year picture is also revealing, with whisky bottles and Burgundy wine still showing far stronger long-term gains than most art categories, despite recent weakness. For investors, the 2026 signal is not that passion assets are broadly back, but that the market is becoming more selective, more quality-driven, and less forgiving of weak liquidity or weak cultural relevance.

The Knight Frank Luxury Investment Index (KFLII) - 12-month % change

The Knight Frank Luxury Investment Index (KFLII) - 12-month % change

Art finance and collateralization

Art becomes collateral when someone with a sufficiently valuable, sufficiently legible object prefers liquidity to sale. That preference is understandable. Selling triggers taxes, forfeits upside, and may signal weakness or shift bargaining power. Borrowing instead lets the owner retain possession or at least beneficial ownership while unlocking capital for business, portfolio management, lifestyle spending, or further collecting. On the lender side, the appeal is clear too: high-net-worth borrowers, trophy collateral, and an asset class that is portable, scarce, and in some cases globally recognisable.

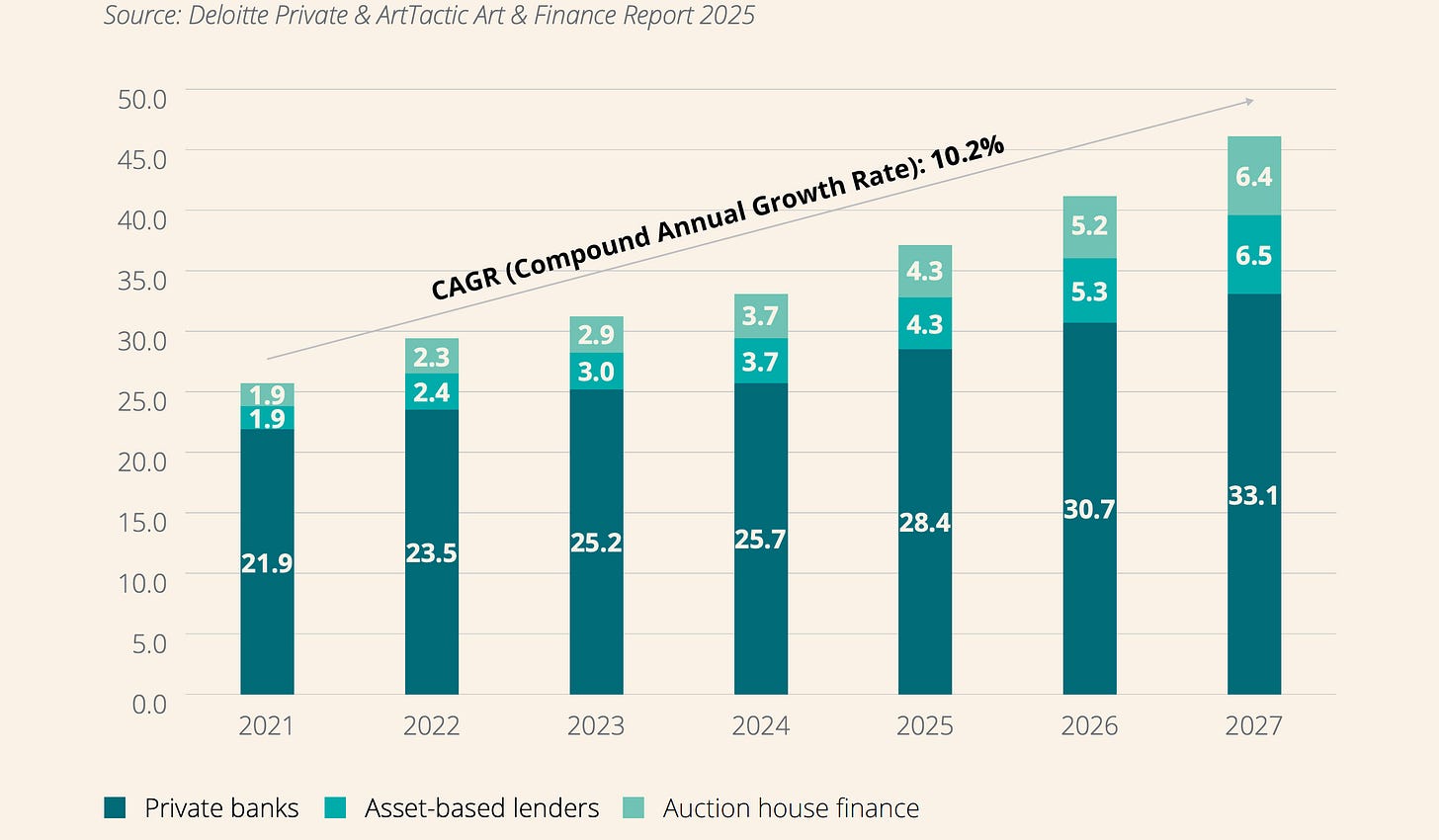

Outlook: Art-secured lending market 2025–2027

The lender ecosystem now spans private banks, auction houses, and specialist firms. J.P. Morgan and Citi Private Bank both market fine-art financing directly to clients. Christie’s offers loans above $1 million against fine-art collections, with other collateral considered case by case. Sotheby’s describes its financial-services arm as asset-based lending against fine art and other passion assets, with underwriting centred on collection expertise and market data rather than conventional retail loan processes. Specialist firms such as The Fine Art Group advertise loans from $1 million to $200 million at up to 50% loan-to-value.

Scale has grown. The Deloitte and ArtTactic estimates, as reported by the Financial Times, place the art-backed loan market at $33.9 billion to $40.0 billion in 2025, with a projected rise to $42.0 billion to $50.1 billion by 2027. Sotheby’s projected in December 2025 that its financial-services portfolio balance had reached a record high above $1.8 billion. In February 2026, Reuters reported that Bank of America had launched an art-consulting service for wealthy clients amid rising use of art as loan collateral, and that wealth managers were seeing growth in such services. The trend is unmistakeable: art finance is no longer a niche curiosity. It is a routine tool in private wealth.

Average loan portfolio outstanding against art (US$ bn)

But art finance is not one thing. Lending against art in a private bank is often relationship lending disguised as object lending. The bank knows the client’s broader assets, can cross-collateralise, and may be willing to restructure before enforcing against the art. The Financial Times reported that none of the private banks surveyed in the latest Deloitte and ArtTactic work suffered defaults in 2024, while half of non-bank lenders did. That difference is central. It suggests that the “object-only” loan is riskier and more cyclically dangerous than the broader relationship-based loan, even when both are described as art-backed.

The mechanics explain why. Art collateral requires appraisal, initial and periodic revaluation, authenticity comfort, provenance review, condition assessment, custody planning, insurance, and a credible enforcement route. Day Pitney’s 2026 overview notes that lenders commonly require appraisals establishing fair market value for collateral purposes and may reserve rights to annual or more frequent reappraisals. If the work is stored in a warehouse, the warehouse agreement needs to subordinate release rights to the lender. If the work remains in the borrower’s home, lenders want inspection and retrieval rights. Insurance obligations also cannot be assumed away; Thompson Hine notes they must be addressed explicitly in art agreements.

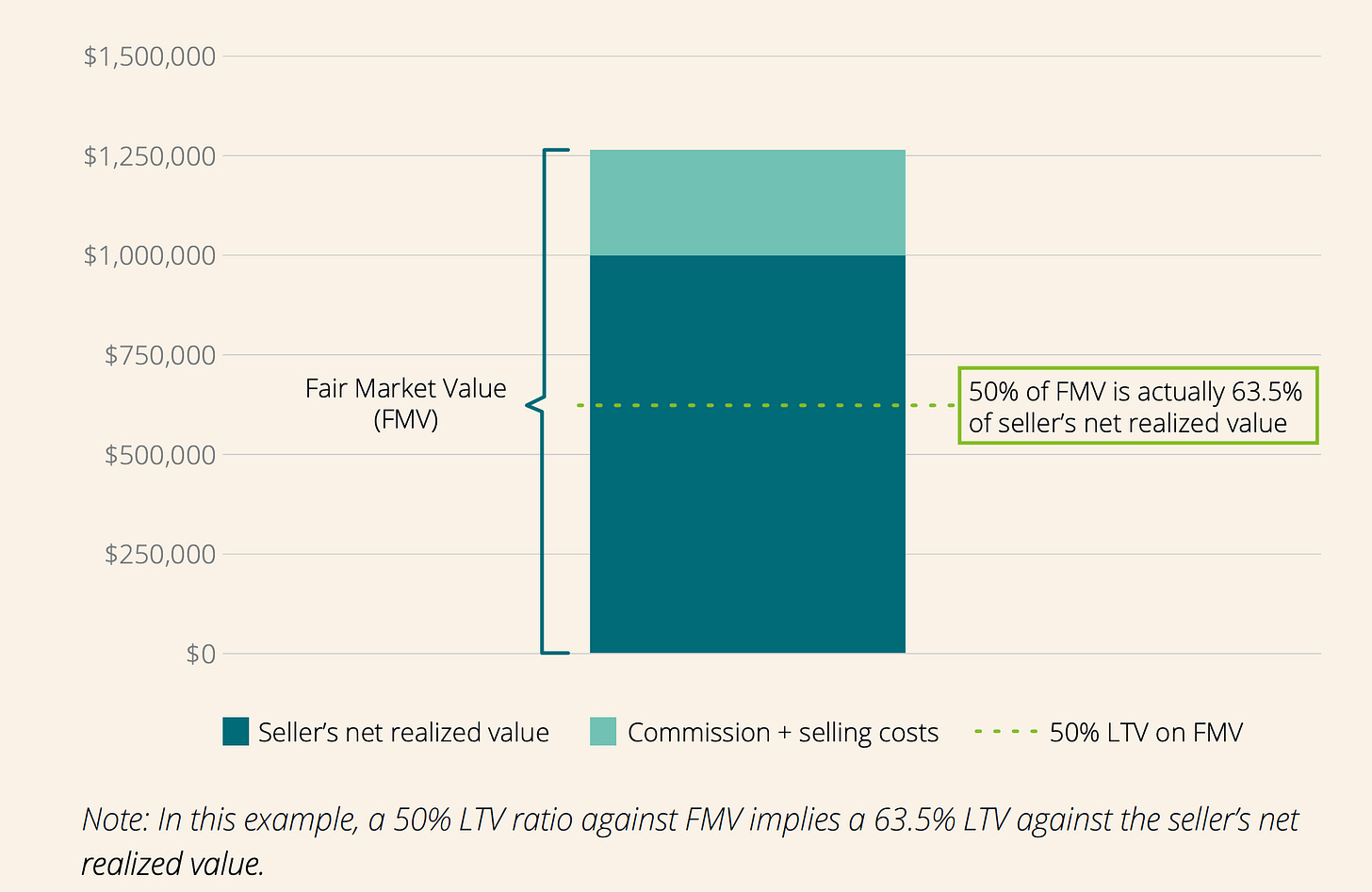

FMV in art-secured lending has inherent flaws (Source: SFS)

Loan-to-value discipline is therefore low by mainstream secured-credit standards. The Fine Art Group advertises up to 50% LTV, which is a useful market signal. The reason is obvious: valuation is uncertain, forced-sale discounts can be severe, and enforcement can be slow, reputationally sensitive, and geographically complex. The object may be unique, but uniqueness is not the same as liquidity. A lender foreclosing on a masterpiece does not have the foreclosure certainty of a lender repossessing listed securities. It has an art-market event to manage.

The fragility becomes clearer in down markets. In early 2026, the Financial Times reported that non-bank defaults had soared and that art lenders were issuing margin calls as collateral values fell. Non-bank lenders can face the uncomfortable situation of lending against mark-to-model valuations in a market where the cleanest comparables have disappeared and the borrower cannot or will not top up collateral. Some lenders, according to the same reporting, re-emerged in “loan-to-own” form, meaning that the real economic objective may be to acquire the underlying art cheaply through default rather than to run a stable performing loan book. That turns what looks like liquidity support into a transfer mechanism for cultural assets.

Art finance also reveals the market’s institutional maturation. Sotheby’s first securitised a pool of art-backed loans in 2024 with a $700 million asset-backed notes offering, then announced a second, larger $900 million securitisation in January 2026. The market is no longer just lending against individual pictures; it is beginning to tranche and distribute the credit risk associated with those pictures. That is a classic sign of financialisation.

Onchain infrastructure and the next art-market paradigm

The key mistake in blockchain discussions about art has been to confuse front-end democratisation with back-end infrastructure. The stronger institutional case for onchain systems does not begin with fantasy claims that blue-chip paintings will soon trade like liquid stocks on public blockchains. It begins with much duller, much more powerful questions: how records are created, which documents can be standardised, how rights are represented, how settlement conditions are enforced, how collateral data travel across institutions, and when a token is legally more than a token. Serious institutional research now points in exactly that direction. The World Economic Forum’s 2025 report argues that tokenisation’s defensible advantages are shared systems of record, programmability, flexible custody, composability, and selected forms of fractional ownership. It also stresses that adoption is slowed by legacy infrastructure, regulation, interoperability limits, and liquidity gaps.

That caution matters because commercial-scale adoption remains limited even in far more standardised financial assets than art. IOSCO’s 2025 final report found that 91% of responding jurisdictions saw nil or very limited commercialised use cases for tokenisation of capital-market products. It also noted that more market participants were experimenting than deploying, and that surveyed asset managers cited deployment costs, lack of feature benefits, and skills deficits as reasons not to use DLT. If tokenisation remains early in bonds, funds, repos, and settlement infrastructure, one should be very careful about assuming it will rapidly transform a legally messier, culturally sensitive, physically grounded market such as fine art.

Where, then, could onchain systems matter first in art? Provenance support is the strongest candidate, but only if one is precise about the problem being solved. Blockchain does not magically determine authenticity, perfect title, or restitution status. Those are legal and factual questions requiring human evidence and institutional authority. What it can do is create tamper-evident, time-stamped records around events in an artwork’s life, such as issuance of a certificate, transfer of a certificate, conservation documentation, exhibition history, lending, or approved condition reports. The value here is cumulative and documentary, not metaphysical.

MoMA adds nfts to its permanent collection

That is why the legal structure matters more than the technology slogan. Xavier Lavayssière’s 2024 paper on legal structures of tokenised assets is especially useful. He distinguishes between “complete tokenisation,” where tokens embody legally enforceable rights, and “incomplete tokenisation,” where tokens function as “digital twins” with limited or no legal value. His core conclusion is that the effectiveness of tokenisation depends on the robustness of the legal bond between token and underlying asset. For physical art, that is decisive. A token is not title simply because it is scarce and transferable on a ledger. It becomes title-adjacent only if the contractual, custodial, and legal architecture makes it so. Otherwise, one owns a record about a painting, or a claim on an SPV, not the painting itself.

Still, early art-market implementations show where the infrastructure thesis has substance. In 2018, Christie’s became the first major auction house to record an auction’s artwork information on blockchain through its partnership with Artory for the $323 million Barney A. Ebsworth Collection. Christie’s later extended the Artory relationship to provenance-focused initiatives such as the Steinitz sale. Those projects did not “tokenise the art market” in any sweeping sense. They did something more modest and more plausible: they attached vetted sale and provenance information to an immutable registry layer.

The same pattern is visible in younger infrastructure firms. Arcual markets a blockchain platform for galleries, fairs, artists, and institutions focused on sales documentation, inventory management, provenance tracking, digital certificates of authenticity, and digital portfolios containing exhibition history, insurance documents, and other records. Verisart offers permanent blockchain-backed certificates designed to be publicly verifiable while preserving privacy about ownership and transaction details. Whatever one thinks of their commercial prospects, these products are aimed at the correct layer of the stack: records and workflows, not the elimination of dealers.

Certificates are especially important because the current paper-based system is fragmented, vulnerable to administrative loss, and poorly interoperable across galleries, artists, estates, shippers, insurers, auction houses, and lenders. A credible digital-certificate regime, ideally controlled or co-signed by artists, foundations, or estates, could reduce friction meaningfully. But the most credible implementations are likely to be permissioned and institutionally controlled, not maximally open and anonymous. This is where the art world’s social logic collides productively with onchain technology’s design space. The market wants better records, but it does not necessarily want universal transparency. It wants selective legibility.

Settlement is another realistic use case, but again mainly in hybrid form. IOSCO’s analysis of DLT-based settlement is clear that atomic settlement and conditional transfer can reduce failed trades, lower certain counterparty risks, and improve collateral efficiency, while also warning that many of these gains remain theoretical because commercial adoption is still nascent and because pre-funding and interoperability create new frictions. In art, a hybrid settlement architecture could prove valuable for high-value cross-border transactions in which title-support records, AML checks, escrow conditions, stable-value payment rails, and transfer conditions all need to sync. Yet the chain will still sit on top of shipping, customs, sanctions screening, local property law, and physical delivery. Atomic settlement does not move the painting off the wall.

The stronger medium-term opportunity may therefore be in finance rather than in retail trading. The World Economic Forum and IOSCO both treat collateral management and repo-style markets as serious tokenisation use cases, and IOSCO notes that tokenised collateral can improve portability, information flow, and capital efficiency. In mainstream finance, permissioned infrastructures such as J.P. Morgan’s Kinexys Digital Assets and its Tokenized Collateral Network show what institutional adoption actually looks like: private or semi-private rails, known counterparties, synchronised settlement logic, legal wrappers, and compliance built in. If art ever becomes a programmable collateral class at scale, it is more likely to arrive through a Kinexys-like architecture adapted for unique physical assets than through consumer-facing fractional NFT marketplaces.

This is where art lending becomes one of the more credible onchain use cases. A lender does not need the painting to trade like a liquid token; it needs reliable data on title, provenance, custody, insurance, valuation, lien status, and transfer restrictions. In that sense, the opportunity is not to make art instantly liquid, but to make art-backed credit less manual, less fragmented, and easier to monitor across lenders, custodians, insurers, and advisors. A programmable collateral layer could allow loan terms, margin triggers, custody confirmations, and repayment conditions to sit closer to the asset record itself, while still leaving authentication, enforcement, and legal ownership in the off-chain institutional world. That is a more realistic future than public fractionalisation: not art as DeFi collateral overnight, but art finance with better rails.

The market evidence is also sobering. ArtTactic’s 2025 Fractional Ownership Monitor showed that platforms were increasingly moving down-market, toward the more liquid middle market, and that activity remained modest in absolute terms. Splint had listed 219 artwork assets worth €23.9 million between September 2023 and July 2025, and Artex had listed only one art asset, the Francis Bacon work, despite its regulated exchange-traded approach. That does not mean the model has no future. It means the scale remains tiny relative to the blue-chip physical market, and it remains unclear whether fractionalisation is solving the deepest problem. The deepest problem is not access alone. It is quality selection, legal clarity, and genuine exit liquidity.

Digital-native art is a different story because the legal and technical bond between token and asset can be much stronger from inception. Here, the blockchain is not trying to simulate ownership of an off-chain object after the fact. It is often part of the object’s native architecture. Sotheby’s continues to run a dedicated digital-art department and positions itself as an active venue for curated NFT and onchain-native works. Art Basel and UBS found that 51% of surveyed HNW collectors bought digital art in 2025, making it the third-largest fine-art spending category in the survey, while younger collectors led participation in digital, film, and video art. That does not mean the NFT bubble has come back. It means digital-native collecting has survived the bubble and is likely to persist as a distinct cultural and commercial lane.

NODE Foundation

Micky Malka’s NODE Foundation offers a useful counterpoint to the tokenisation narrative. Instead of trying to fractionalise physical masterpieces or turn galleries into exchanges, NODE treats onchain-native works as cultural objects that need preservation, exhibition, education, and institutional context. Its Palo Alto space, opened with 10,000, an exhibition devoted to CryptoPunks, suggests a different path for digital art: not replacing the gallery with the marketplace, but building new physical institutions around works whose provenance, ownership, and circulation are already native to the network.

Could onchain infrastructure reduce information asymmetry? At the margin, yes. Better certificates, standardised records, and synchronised collateral data could reduce some fraud and friction. But the elite market is unlikely to surrender opacity wholesale, because opacity itself is part of how power and premiums are maintained. The highest-value collectors often prize discretion, and mega-galleries benefit from controlling allocation and information flow. So the more realistic question is not whether blockchains make the art world democratic. It is whether they make selective parts of the market more efficient for the actors who already dominate it. The answer, over a five-to-fifteen-year horizon, is probably yes. But that is a very different claim from the old promise of cultural disintermediation.

AI, analog prestige, and conclusion

The next tense of the art market is likely to be technologically richer and socially older at the same time. AI will multiply images, compress certain forms of design labour, widen discovery, and intensify questions of authorship, originality, and authentication. That abundance does not automatically reduce the value of physical art. It may do the opposite. The scarcer and more replicable digital imagery becomes, the more valuable embodied, socially validated objects and gatherings may appear. That is partly an inference, but it is supported by current buyer behaviour: Art Basel and UBS found strong continuing use of galleries and fairs, rising studio-visit attendance, and near-universal plans among surveyed HNW collectors to attend art events in 2026.

This is where Gagosian’s importance returns at the end. His dinners, openings, architecture, social worlds, and large-format gallery exhibitions are not peripheral to the business. They are part of the trust architecture. In a world awash with digital images, synthetic media, and algorithmic recommendation, people with money and cultural ambition may value human curation, physical rooms, real objects, and live social rituals even more. If that happens, the vernissage becomes more rather than less important, even as back-office documentation becomes more structured and machine-compatible.

The broad conclusion follows directly. Larry Gagosian did not merely build a gallery empire. He built one of the most effective playbooks of the modern art market: a system for converting scarcity, information, trust, status anxiety, institutional adjacency, and private liquidity into price realisation. The model reveals that the top end of the market is not governed chiefly by transparent price discovery. It is governed by access to exceptional supply, control over who sees what and when, the ability to wrap objects in legitimacy, and the ability to speak fluently to both artists and billionaires.

Art, on this view, is investable only in a narrow and highly uneven sense. A small slice of the market can function as a store of value, a collateral asset, and occasionally a strong investment. But that slice is access-heavy, expertise-heavy, and expensive to own. Reported historical returns are often flattered by survivorship and repeat-sales bias; real-world costs are high; and the broader market remains segmented, illiquid, and opaque. Serious allocators should therefore resist both romance and hype. Art can matter financially without being reducible to finance.

Art finance pushes the point further. Once artworks back loans, support securitisations, and sit inside private-bank liquidity planning, culture is not outside capital markets. It is one of their fringe collateral pools. Sotheby’s art-loan securitisations, growing private-bank art-lending businesses, and the expansion of advisory-plus-finance offerings at large banks all show that the market is becoming more institutional in its plumbing. Yet defaults among non-bank lenders also show that art credit can turn fragile quickly when valuations soften and liquidity narrows. Financialisation increases utility, but it can also increase reflexivity and fragility.

Onchain infrastructure is likely to matter most where the art world is weakest operationally: records, certificates, rights metadata, settlement conditions, and selected collateral workflows. It is likely to matter least where the art world’s value system is most social: primary allocation of blue-chip physical works, museum-grade trust networks, collector discretion, and the cultural pricing of access itself. The better question, then, is not whether blockchains replace galleries or auction houses. They will not. The better question is whether they become part of the hidden operating system beneath them. On present evidence, that is the more plausible path.

Two limitations should keep any forecast humble. First, private sales remain opaque, so some of the highest-value transactions are never fully observable. Second, art-return datasets exclude enormous amounts of untranslated reality: unsold works, private transactions, quality differences within an artist’s output, and the fact that exceptional objects are not random. Those caveats do not weaken the central thesis. They reinforce it. The future art market is unlikely to become fully transparent or fully democratic. It is more likely to become more infrastructural, more data-rich at the margins, more financially integrated, and still very much ruled, at the top, by human trust, social power, and the embodied authority of physical culture.

Sources

- Art Basel and UBS. The Art Basel and UBS Global Art Market Report 2026

- Sotheby’s Financial Services. “Sotheby’s Financial Services Announces $900 Million Securitization.”

- Lévy Gorvy. “How Duveen Made European Art Part of American Culture.”

- **Artsy. “**Why Leo Castelli Paid his Artists Even When They Weren’t Making Work”

- Knight Frank. The Wealth Report: Our Luxury Investment Index Results 2026

- J.P. Morgan Private Bank. “Fine Art Financing.”

- Deloitte. “Art & Finance Report 2025 - 9th edition.”

- NODE Foundation. “A HOME FOR ARTISTS DEFINING DIGITAL CULTURE TODAY”

- **IOSCO. “**Tokenization of Financial Assets”

- Christie’s. “Our Best Kept Secret in 2025: How Some 500 Specialists Across 40 Departments Drove $1.5 Billion Worth of Private Sales.”

Partner Highlight

At insights4vc, we pay attention to teams that are not just shipping products, but shaping categories.

Moto is one of them. The company is building a premium card experience positioned as an alternative to traditional incumbents such as Amex, combining a high-end user interface with more modern financial infrastructure.

Moto is currently expanding access to a limited testing group. If you would like to test the product and typically spend more than $5,000 per month, please contact us at: [email protected]

Cover Artwork

The Five Senses: Hearing

Jan Brueghel the Younger, c. 1625

Risk Disclaimer:

insights4.vc and its newsletter provide research and information for educational purposes only and should not be taken as any form of professional advice. We do not advocate for any investment actions, including buying, selling, or holding digital assets.

The content reflects only the writer’s views and not financial advice. Please conduct your own due diligence before engaging with digital assets or related technologies, as they carry high risks and values can fluctuate significantly.