How Global Digital Asset Markets Are Being Rebuilt

For more than a decade, much of the legal debate focused on whether a token should be classified as an investment contract, utility instrument, commodity, or another type of asset. By mid-2026, regulatory attention had increasingly shifted toward market structure and the conditions under which digital assets may be issued, distributed, held, traded, and settled. The relevant question is therefore not limited to whether an asset is legally recognized. It also concerns which entities are authorized to perform specific activities within each jurisdiction.

This development is taking place across several areas: the integration of stablecoin issuance into the U.S. banking and payments framework, the end of transitional arrangements under the European Union’s Markets in Crypto-Assets Regulation, and the introduction of licensing requirements across other financial jurisdictions.

United States: Federal Stablecoin and Market Structure Framework

The GENIUS Act and the Treatment of Reserve Deposits

The Guiding and Establishing National Innovation for U.S. Stablecoins Act, known as the GENIUS Act, was signed into law on July 18, 2025. It establishes the federal framework for the issuance of payment stablecoins. The statute limits issuance to Permitted Payment Stablecoin Issuers, or PPSIs, and defines payment stablecoins as privately issued digital instruments that are redeemable at par value and recorded on distributed ledger systems.

The framework provides three principal routes to PPSI status: authorization for a subsidiary of an insured depository institution, a Federal Qualified Payment Stablecoin Issuer charter issued by the Office of the Comptroller of the Currency, or qualification under an approved state supervisory regime subject to federal standards.

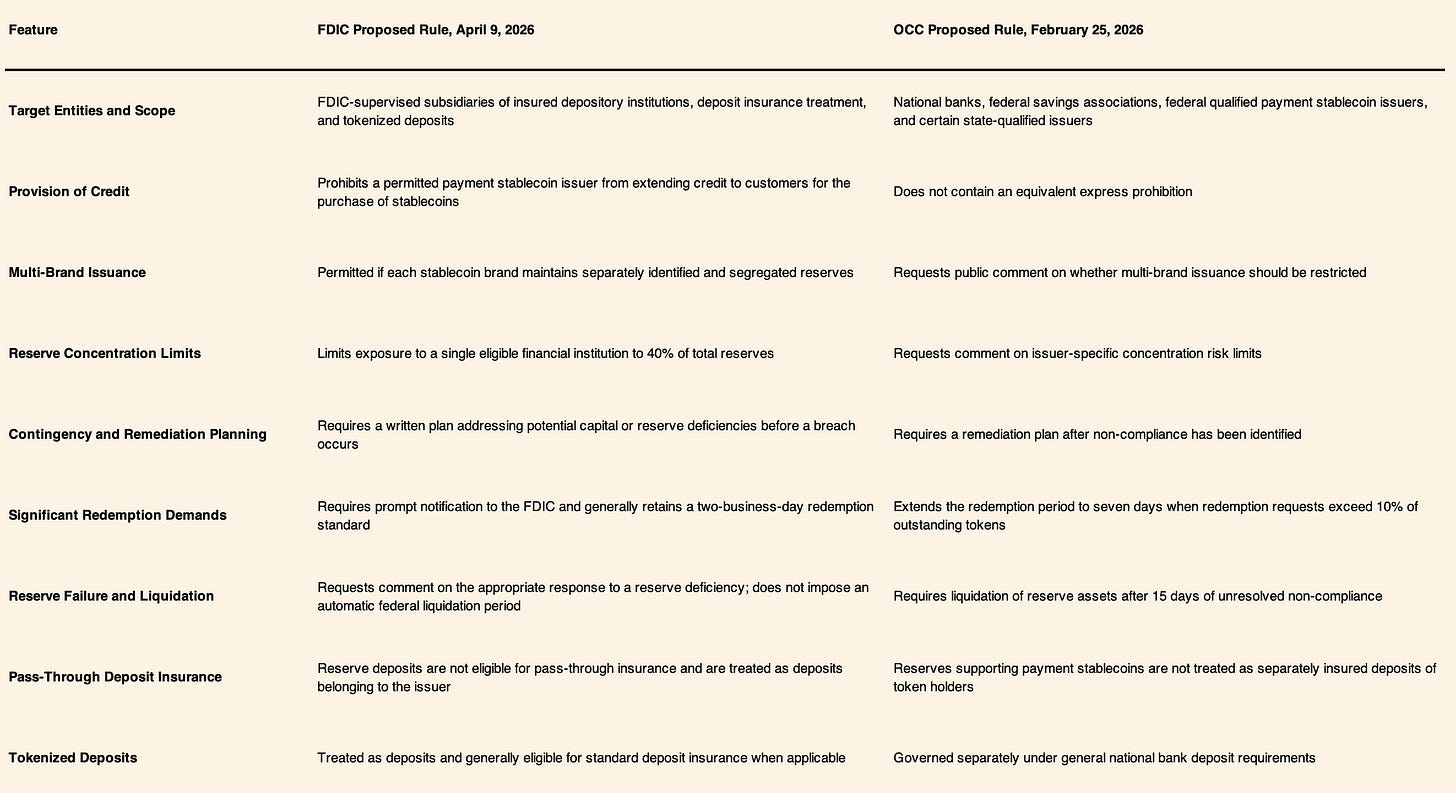

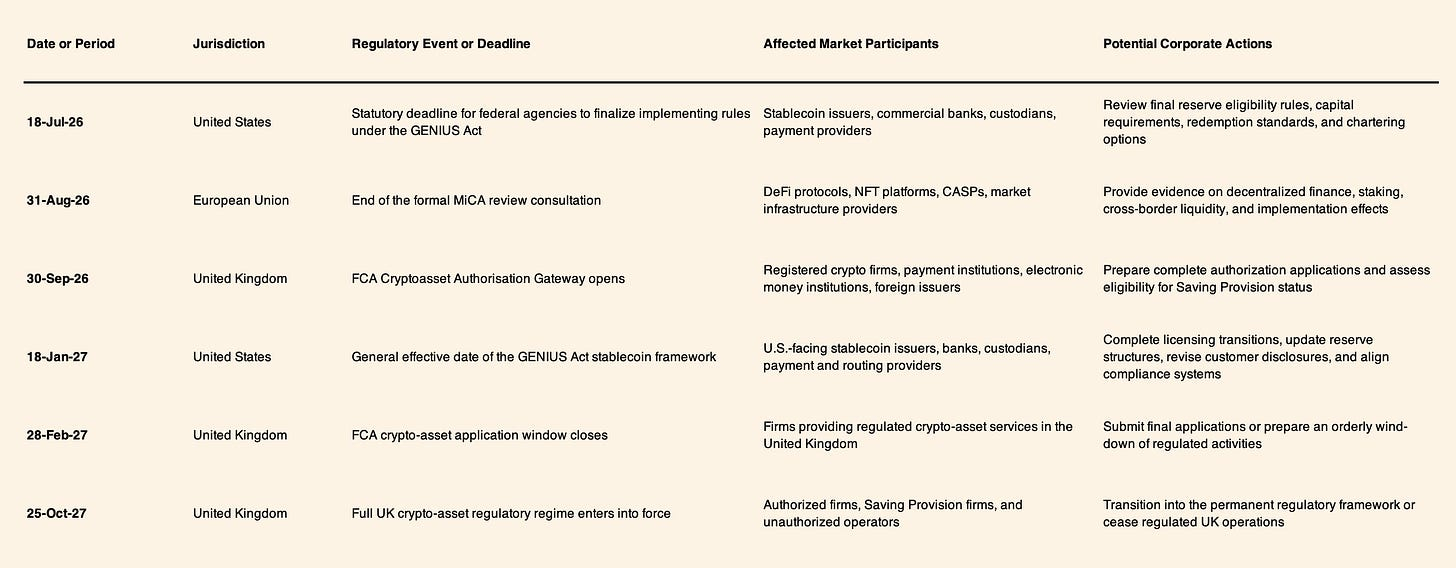

The implementing rules, due to be finalized by July 18, 2026, are intended to define reserve, liquidity, capital, redemption, and supervisory requirements. The GENIUS Act prohibits issuers from paying interest or programmatic yield directly to stablecoin holders. The OCC’s proposed rules also include a three-tier liquidity framework and a minimum capital requirement of USD 5 million. These requirements may affect the ability of smaller or less-capitalized companies to obtain federal authorization independently.

The treatment of stablecoin reserve deposits remains an important implementation issue. Although the GENIUS Act specifies that stablecoin tokens are not covered by federal deposit insurance, the Federal Deposit Insurance Corporation has proposed that the underlying cash reserves should also be ineligible for pass-through insurance. Under this interpretation, reserve deposits would be treated as deposits belonging to the PPSI rather than deposits held separately on behalf of individual token holders.

Insurance coverage would therefore be limited to USD 250,000 for the reserve account as a whole, rather than USD 250,000 for each token holder. This approach may increase the relevance of the issuer’s banking relationships, reserve composition, custody arrangements, and counterparty exposure. It may also affect how institutional users evaluate stablecoins issued by banks, non-bank entities, and state-chartered trust companies.

State regulatory frameworks are also being adjusted in response to the federal legislation. On June 9, 2026, the New York State Department of Financial Services released a proposed Part 202 of Title 23 of the New York Codes, Rules and Regulations. The proposal is intended to align New York’s limited-purpose trust company framework with the GENIUS Act. It would replace the superintendent’s 2022 Industry Letter with a consolidated regime for authorized payment stablecoin issuers and provide a framework for state-qualified firms operating under federal standards.

The CLARITY Act and Digital Asset Classification

The Digital Asset Market Clarity Act continues to move through the U.S. legislative process. After passing the House of Representatives in July 2025, a reconciled substitute version was approved by the Senate Banking Committee on May 14, 2026, by a vote of 15 to 9. The bill was subsequently placed on the Senate Legislative Calendar.

Its final passage remains uncertain because of the legislative timetable and unresolved policy issues. Prediction markets have estimated the probability of enactment during 2026 at approximately 48% to 60%. Regardless of the final outcome, the bill provides an indication of how Congress may allocate regulatory responsibility between the Securities and Exchange Commission and the Commodity Futures Trading Commission.

The Senate substitute introduces several digital asset categories. It defines network tokens as digital commodities associated with decentralized distributed ledger systems and places them under CFTC jurisdiction. Ancillary assets are defined as network tokens whose value initially depends on the entrepreneurial or managerial efforts of an originator.

The bill also proposes a Regulation Crypto disclosure process. Under this framework, an issuer could submit a written certification to the SEC, supported by evidence, stating that the relevant network has reached a level of decentralization that supports treatment of the token as a non-security commodity. The certification would create a rebuttable presumption rather than a final or irreversible classification.

The Senate substitute also addresses stablecoin reward programs. Digital asset service providers would be prohibited from paying interest or yield to U.S. customers solely for holding stablecoins. However, the bill would permit incentives connected to payments, transactions, or other forms of active use. This distinction separates passive holding rewards from transaction-based promotional programs.

The substitute bill also includes provisions related to illicit finance. Digital commodity intermediaries would become subject to Bank Secrecy Act obligations. Digital asset kiosks would be subject to a separate compliance framework covering registration, designated compliance officers, transaction confirmations, customer notices, and holding limits.

Administrative Changes Affecting Digital Asset Custody

In parallel with the legislative process, federal agencies have revised several administrative positions affecting digital assets. In March 2026, the SEC and CFTC issued a joint interpretive statement addressing the regulatory treatment of Bitcoin, Ether, and certain blockchain activities. The statement recognized Bitcoin and Ether as commodities and stated that activities such as network staking, validation, mining, token wrapping, and free airdrops do not automatically constitute securities offerings.

The SEC also rescinded Staff Accounting Bulletin 121. The bulletin had required certain entities safeguarding digital assets to recognize corresponding liabilities on their balance sheets. Its removal changes the accounting treatment applied to digital asset custody and may reduce some of the capital and balance-sheet costs previously associated with the activity.

The SEC and FINRA also withdrew their 2019 joint statement concerning broker-dealer custody of digital asset securities. This changed the conditions under which registered broker-dealers may safeguard digital asset securities under Rule 15c3-3.

In September 2025, the SEC’s Division of Investment Management issued a no-action letter allowing registered investment advisers to treat state-chartered trust companies as qualified custodians under specified conditions. These conditions include the segregation of customer assets and restrictions on lending, pledging, or rehypothecating client assets without prior written consent.

Taken together, these measures have modified the conditions under which banks, broker-dealers, investment advisers, and trust companies may provide digital asset services. The remaining policy questions concern the prudential, custody, disclosure, and supervisory standards that will apply to each category of institution.

European Union: MiCA Following the Transitional Period

Requirements Following July 1, 2026

The transitional grandfathering period under the European Union’s Markets in Crypto-Assets Regulation expired on July 1, 2026. Before that date, some crypto-asset service providers registered under national anti-money laundering frameworks were able to continue operating during temporary national transition periods. After the expiry of those arrangements, firms providing regulated crypto-asset services to EU clients are generally required to hold authorization under MiCA.

Guidance issued by the European Securities and Markets Authority sets out expectations for national competent authorities in relation to firms that have not obtained authorization. Such firms may be required to implement funded wind-down plans and provide for the transfer of customer assets to authorized crypto-asset service providers or self-hosted wallets.

National authorities may impose administrative and civil measures under Article 111 of MiCA. These may include cease-and-desist orders, public statements, and financial penalties of up to EUR 5 million or 5% of annual turnover, depending on the circumstances and the applicable national implementation.

ESMA has also addressed the use of reverse solicitation and the activities of non-EU firms. A non-EU company that actively markets or provides services to EU clients may be required to establish an authorized and substantively managed EU entity. The application of these rules depends on the nature of the service, the manner in which the client relationship was initiated, and the level of activity conducted within the Union.

The compliance framework also includes the Transfer of Funds Regulation. Under the regulation, crypto-asset service providers must collect and transmit specified information for crypto-asset transfers without a minimum transaction threshold. Transfers involving unhosted wallets may require additional verification and risk assessment.

Regulatory technical standards issued by the European Anti-Money Laundering Authority on July 10, 2026, introduce further requirements relating to transaction monitoring and the assessment of financial crime risk. These measures expand compliance obligations beyond initial customer onboarding and toward ongoing monitoring of transactions and counterparties.

Stablecoin Authorization and Market Access Under MiCA

MiCA Titles III and IV govern asset-referenced tokens and e-money tokens. An e-money token referencing a fiat currency must be issued by an authorized credit institution or electronic money institution. Issuers are required to maintain reserves corresponding to the value of outstanding tokens and are prohibited from paying interest or yield to holders.

MiCA also includes restrictions on the use of foreign currency-denominated stablecoins as a means of exchange within the European Union. The framework refers to a threshold of 200,000 transactions per day for certain uses of such tokens. These provisions are intended to address the potential monetary and financial stability implications of widespread use of privately issued tokens denominated in non-EU currencies.

The application of MiCA has resulted in different market access outcomes for Tether and Circle. Tether has not obtained an electronic money institution authorization under MiCA. As a result, some regulated exchanges and licensed crypto-asset service providers have delisted or restricted USDT for customers in the European Economic Area.

USDT remains available through self-custodial wallets and decentralized protocols. However, its availability through regulated fiat on-ramps, institutional custody platforms, and authorized trading venues may be more limited within the European Union.

Circle obtained authorization as an electronic money institution and is therefore able to issue USDC and EURC within the relevant MiCA framework. This allows regulated institutions to use these tokens in payment, settlement, custody, and treasury arrangements, subject to applicable operational and compliance requirements.

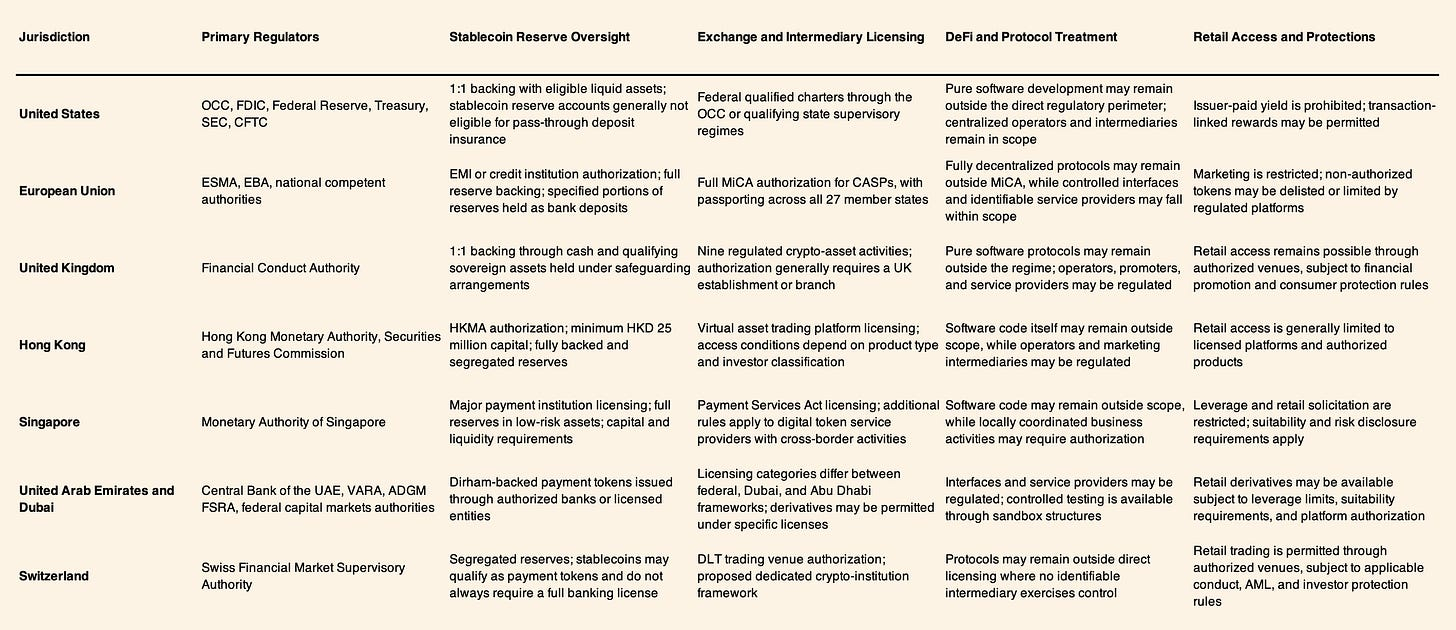

Selected International Regulatory Frameworks

United Kingdom: FSMA Integration and the Authorisation Gateway

The United Kingdom has introduced a crypto-asset regime under the Financial Services and Markets Act 2000. The Financial Services and Markets Act 2000 (Cryptoassets) Regulations 2026 establish nine regulated activities relating to crypto-assets. These activities include stablecoin issuance, custody, exchange operation, principal dealing, and token staking.

HM Treasury has excluded advising on and discretionary management of qualifying crypto-assets from the proposed regime. This means that these activities will not initially be treated in the same manner as regulated investment advice or portfolio management involving conventional financial instruments.

The United Kingdom is using a transitional authorization process. The Financial Conduct Authority is scheduled to operate a Cryptoasset Authorisation Gateway from September 30, 2026, until February 28, 2027. Firms that submit complete applications during this period may qualify for Saving Provision status, allowing them to continue certain activities beyond the formal commencement date of October 25, 2027, while their applications are reviewed.

Firms that do not apply within the gateway period may be required to stop marketing to and onboarding new UK customers. A narrower Transitional Provision is intended to allow existing activities to be wound down in an orderly manner.

The FCA is also consulting on CP26/4, which concerns the application of the wider FCA Handbook, and GC26/2, which addresses the Consumer Duty. These consultations consider how existing governance, disclosure, conduct, and consumer protection requirements should apply to authorized crypto-asset firms.

Hong Kong: Stablecoin Licensing and Tokenization Pilots

Hong Kong introduced the Stablecoins Ordinance, Cap. 656, in August 2025. The ordinance creates a licensing regime for stablecoin issuers under the supervision of the Hong Kong Monetary Authority.

Licensed issuers are required to maintain minimum paid-up capital of HKD 25 million, hold reserves corresponding to outstanding stablecoin liabilities, segregate reserve assets from operating capital, and comply with anti-money laundering, counter-terrorist financing, and transaction monitoring requirements.

In April 2026, the HKMA granted stablecoin issuer licenses to Anchorpoint Financial and HSBC. HSBC has announced plans to issue a Hong Kong dollar-denominated stablecoin during the second half of 2026 and to make it available through selected consumer and corporate payment channels.

The HKMA is also conducting tokenization pilots through EnsembleTX. These pilots involve transactions using tokenized money market funds, commercial bank deposits, and regulated settlement assets. The initiative is intended to test how different forms of tokenized money and assets may interact within a supervised environment.

Singapore: Restrictions on Offshore Digital Token Services

Under Part 9 of the Financial Services and Markets Act 2022, which became effective on June 30, 2025, digital token service providers incorporated in Singapore or operating from a place of business in Singapore may be subject to licensing requirements even when their services are offered only to customers outside the jurisdiction.

The Monetary Authority of Singapore has stated that licenses for these cross-border digital token service providers will be granted only in limited circumstances. Its stated concerns include the difficulty of supervising offshore activity and managing money laundering, terrorism financing, and reputational risks.

The framework limits the ability of firms to use Singapore solely as a place of incorporation while conducting their commercial activities elsewhere. Companies may need to establish substantive operations under the Payment Services Act or relocate their corporate and management functions outside Singapore.

United Arab Emirates and Switzerland: National Licensing Developments

The United Arab Emirates has continued to develop its federal and regional regulatory frameworks for digital assets. Federal Decree-Law No. 6 of 2025 and subsequent capital markets rules introduced during 2026 establish licensing categories that operate alongside the frameworks of Dubai’s Virtual Assets Regulatory Authority and Abu Dhabi’s Financial Services Regulatory Authority.

The UAE Central Bank’s Payment Token Services Regulation restricts algorithmic and privacy-focused payment tokens and provides a framework for fiat-backed payment tokens. AEDZ, a dirham-backed stablecoin issued by Zand Trust, has been approved under this framework.

Zand Bank has also entered into a partnership with Ripple concerning potential links between AEDZ and RLUSD, Ripple’s U.S. dollar-denominated stablecoin. The arrangement is intended to explore settlement and liquidity connections between dirham and dollar-denominated digital assets.

Switzerland is pursuing amendments to its existing financial legislation rather than adopting the European Union’s MiCA framework. Following a consultation that concluded in February 2026, the Swiss Federal Council advanced proposed amendments to the Financial Institutions Act.

The proposed reforms would remove the CHF 100 million deposit ceiling applicable to fintech licenses, establish a crypto-institution license with conduct and conflict-of-interest requirements, and define the conditions under which licensed non-bank entities may issue stablecoins.

These issuers would remain subject to reserve, segregation, governance, and anti-money laundering requirements. Switzerland’s proposed framework differs from the approaches adopted in the European Union and the United States by providing a specific category for specialized non-bank crypto institutions.

Onchain Capital Markets: Comparative Regulatory Matrix

The following matrices compare stablecoin requirements, intermediary licensing frameworks, protocol treatment, retail access rules, and selected regulatory milestones across major financial jurisdictions. The analysis focuses on differences in institutional design, market access, reserve requirements, and implementation timelines.

Comparison of Stablecoin and Intermediary Licensing Frameworks

Comparison of FDIC and OCC Proposals Under the GENIUS Act

Selected Legislative and Regulatory Milestones

Market Structure Implications for Private Markets

Capital Requirements and Market Concentration

One likely consequence of the emerging regulatory structure is a gradual concentration of regulated digital asset activity among banks, established payment companies, licensed custodians, and well-capitalized non-bank financial institutions. Capital thresholds such as Hong Kong’s HKD 25 million minimum and the OCC’s proposed USD 5 million capital floor raise the cost of entering the stablecoin issuance market.

These thresholds do not necessarily prevent smaller companies from participating, but they may change the most viable route to market. Early-stage firms may increasingly rely on partnerships with banks, regulated infrastructure providers, trust companies, or licensed electronic money institutions rather than seeking independent authorization.

Large financial institutions may have an advantage because they can use existing compliance systems, deposit relationships, risk management functions, and regulatory infrastructure. Smaller crypto-native companies may face proportionally higher costs related to licensing, reserve management, audits, governance, cybersecurity, and transaction monitoring. This could increase the frequency of joint ventures, acquisitions, white-label issuance models, and regulated infrastructure partnerships.

The longer-term effect will depend on how regulators calibrate proportionality. If authorization requirements are applied uniformly regardless of issuer scale or risk, market concentration may increase. If regulators introduce tiered regimes and proportionate requirements, smaller firms may retain a viable role in product development, distribution, and specialized infrastructure.

Segmentation of Global Digital Asset Liquidity

Global digital asset liquidity is increasingly divided between regulated onshore infrastructure and offshore or permissionless markets. The distinction is not absolute, as the same token may circulate across centralized exchanges, decentralized protocols, self-hosted wallets, and institutional custody platforms. However, access to banking services and regulated distribution is becoming more dependent on the authorization status of issuers and intermediaries.

The Regulated Onchain Segment

The regulated segment includes licensed stablecoins such as USDC and EURC, alongside emerging bank-issued or locally authorized instruments such as HSBC’s proposed Hong Kong dollar token and Zand’s AEDZ.

These assets may operate on public blockchains while remaining connected to regulated reserve accounts, institutional custodians, commercial bank settlement systems, and authorized exchanges. Their use may be subject to Travel Rule compliance, sanctions screening, transaction monitoring, wallet controls, redemption requirements, and jurisdiction-specific limits.

The principal advantage of this segment is access to regulated financial infrastructure. The trade-off is a higher level of operational control, identity verification, and regulatory reporting.

The Offshore and Permissionless Segment

The offshore and permissionless segment includes stablecoins issued outside major onshore licensing regimes, as well as decentralized stablecoins and other blockchain-native settlement assets.

These instruments may continue to support substantial activity across decentralized exchanges, lending protocols, derivatives platforms, self-hosted wallets, and over-the-counter markets. However, their integration with regulated banks, licensed exchanges, and institutional custody systems may become more limited in jurisdictions that require local authorization.

The economic effect of this segmentation may appear through differences in liquidity, redemption access, market depth, counterparty eligibility, and transaction costs. Spreads between authorized and non-authorized stablecoins may widen during periods of regulatory change, market stress, or exchange delistings. At the same time, offshore and permissionless markets may retain higher volumes in regions where access to dollar liquidity is limited or where local banking infrastructure is less developed.

DeFi Governance and the Use of Formal Legal Structures

The expansion of the regulatory perimeter is also changing how decentralized protocols organize governance, development, and interface operations. Current legislative proposals generally distinguish between publishing open-source software and operating a commercial financial service. Raw protocol code may remain outside direct regulation, while entities that control user interfaces, collect fees, administer assets, or actively market services may fall within licensing or intermediary rules.

This distinction encourages protocol teams to separate core software development from front-end operations, governance administration, treasury management, and commercial service provision. It may also increase the use of formal legal entities that provide liability protection and define the responsibilities of developers, delegates, service providers, and token holders.

One structure receiving increased attention is the Decentralized Unincorporated Nonprofit Association, or DUNA. Certain U.S. state laws allow decentralized organizations to use this structure to obtain legal personality, contractual capacity, and limited liability protection without adopting a conventional corporate model. The suitability of a DUNA depends on the protocol’s governance design, revenue model, tax position, and degree of decentralization.

DeFi interfaces are also adopting jurisdictional restrictions, including IP blocking, wallet screening, and limitations on access from the United States or European Union. These controls may reduce the compliance exposure of identifiable interface operators, but they do not necessarily remove regulatory risk where the underlying team retains substantial control over the protocol or its economic activity.

The likely outcome is not the disappearance of decentralized finance, but a clearer separation between protocol infrastructure, regulated access layers, and permissionless user interaction. Protocols with decentralized governance and limited centralized control may remain broadly accessible at the smart-contract level, while commercial interfaces and institutional access providers operate within licensing frameworks.

Conclusion

By mid-2026, digital asset regulation had moved from broad classification disputes toward more detailed rules governing issuance, custody, reserves, intermediary conduct, market access, and transaction monitoring. The implementation of the GENIUS Act in the United States, the end of MiCA transition periods in the European Union, and the development of bank-linked stablecoin frameworks in Hong Kong and the United Arab Emirates indicate a broader integration of digital assets into existing financial regulatory systems.

This integration is not uniform. The United States is placing payment stablecoins within a combined federal and state banking framework. The European Union is relying on electronic money institutions, credit institutions, and authorized crypto-asset service providers. The United Kingdom is creating a crypto-specific authorization regime under FSMA. Hong Kong and the UAE are emphasizing bank-linked issuance and institutional settlement. Singapore is restricting offshore-only structures, while Switzerland is considering a specialized licensing category for crypto-native financial institutions.

The composition of regulatory risk is changing. Asset classification risk remains relevant, particularly for tokens whose legal status depends on decentralization, issuer involvement, or investor expectations. However, operational risks are becoming more important. These include licensing execution, reserve eligibility, custody arrangements, governance standards, transaction monitoring, regulatory capital, and access to banking infrastructure.

The firms most likely to operate across multiple regulated markets are those able to maintain sufficient capital, local regulatory permissions, transparent reserve structures, qualified custody relationships, and jurisdiction-specific compliance systems. Smaller firms may remain competitive by focusing on software, distribution, specialized infrastructure, or partnerships with licensed entities rather than attempting to reproduce the full regulatory stack independently.

Market participants should therefore assess corporate structures, token issuance models, reserve arrangements, custody providers, front-end operations, and geographic exposure against the requirements of each target jurisdiction. The relevant question is no longer only whether a digital asset is permitted. It is also whether each entity involved in issuing, distributing, safeguarding, promoting, or settling that asset has the required authorization and operational capacity.

Sources

- https://www.sullcrom.com/insights/memo/2026/March/OCC-Proposes-Regulations-Implement-GENIUS-Act

- https://www.occ.gov/news-issuances/bulletins/2026/bulletin-2026-3.html

- https://www.galaxy.com/insights/research/clarity-act-passage-odds-60-percent-senate-calendar-june-2026

- https://www.banking.senate.gov/newsroom/majority/the-facts-the-clarity-act

- https://www.pwchk.com/en/research-and-insights/digital-assets/stablecoins-in-hk-mar2026.html

- https://www.globallegalinsights.com/practice-areas/blockchain-cryptocurrency-laws-and-regulations/united-kingdom/

- https://practiceguides.chambers.com/practice-guides/fintech-2026/united-arab-emirates/trends-and-developments

Partner Highlight

At insights4vc, we pay attention to teams that are not just shipping products, but shaping categories.

Moto is one of them. The company is building a premium card experience positioned as an alternative to traditional incumbents such as Amex, combining a high-end user interface with more modern financial infrastructure.

Moto is currently expanding access to a limited testing group. If you would like to test the product please contact us at: [email protected]

Cover Artwork

The Dam and Damrak, Amsterdam

Jan van der Heyden c. 1663

Risk Disclaimer:

insights4.vc and its newsletter provide research and information for educational purposes only and should not be taken as any form of professional advice. We do not advocate for any investment actions, including buying, selling, or holding digital assets.

The content reflects only the writer’s views and not financial advice. Please conduct your own due diligence before engaging with digital assets or related technologies, as they carry high risks and values can fluctuate significantly.