Stablecoins should not be analysed as a niche crypto payment method. In corporate finance, their most important role is increasingly as a programmable settlement layer that can sit underneath existing payment, treasury, and payout workflows. That distinction matters. The real enterprise question is not whether a company wants to “use crypto”; it is whether a company can improve liquidity efficiency, settlement predictability, reconciliation quality, and payout coverage by using a new form of always-on, API-native value transfer in selected corridors and workflows.

Why this matters now is straightforward. Cross-border payments remain structurally uneven. The BIS and FSB continue to document slow progress, persistent frictions, and a likely miss against the G20’s end-2027 targets for materially better end-user outcomes. Even in segments where fee economics have improved, the biggest cost is often not the explicit transfer fee but FX, liquidity fragmentation, compliance delays, and operational exception handling. In the FSB’s monitored B2B segment, the average fee was 0.2% and the average FX cost was 1.4% in 2025, meaning FX represented about 87% of total average cost. In wholesale payments, 93.2% were credited within one business day in 2025, but only 54.6% within one hour, which is good enough for many treasury flows but not for all use cases, especially those affected by time zones, weekends, and cut-off windows.

Stablecoins are already useful where cross-border frictions are highest: emerging-market payout corridors; weekend and holiday funding gaps; fragmented banking markets; contractor and creator payouts; marketplaces with many small cross-border beneficiaries; treasury rebalancing across entities; and payment businesses that carry significant pre-funding and off-cycle liquidity buffers. Thunes’ case study with Circle is one of the clearest enterprise examples: funding windows moved from T+2 to T+0, settlement times fell from days to minutes or seconds, and the firm states that continuous liquidity reduced the need to hold excess weekend and holiday float. Worldpay’s payout partnership with BVNK and Circle’s managed-payments model both point in the same direction: the enterprise often does not need to hold or touch stablecoins directly to capture the benefit.

Stablecoins are not obviously superior in every corridor. In G10-to-G10 or mature G10-to-major-market flows, the delta versus modern non-crypto providers can be small or negative once on-ramp, off-ramp, and compliance costs are included. Wise reported a 0.53% cross-border take rate in FY25 and 65% instant transfers, while Airwallex markets interbank FX and proprietary local payment connectivity to 200+ countries. For many corporate flows, the bottleneck is therefore not raw payment transmission speed, but last-mile banking access, compliance orchestration, and whether the recipient insists on local-bank fiat receipt. That is why Jack Zhang’s earlier scepticism, that off-ramping into fiat can be more expensive than interbank FX, was a serious institutional critique rather than a rhetorical anti-crypto stance.

The most important conclusion is therefore selective, not universal. Stablecoins are strongest as infrastructure for:

- liquidity bridging between fiat systems,

- high-friction B2B and B2P payout corridors,

- treasury movement outside banking hours,

- embedded payout stacks where counterparties are numerous, small, and globally dispersed,

- platform businesses needing programmable, traceable settlement.

They are weaker where:

- existing local rails already deliver same-day or instant settlement cheaply,

- card-style protections and chargebacks matter,

- off-ramp spreads or wallet-risk controls erode the economics,

- recipient preference is overwhelmingly fiat-bank-only,

- accounting, audit, custody, or compliance maturity is weak.

The biggest risks are not technological novelty alone. They are regulatory fragmentation, issuer concentration, reserve and redemption risk, wallet and custody controls, chain selection, sanctions and AML exposure, Travel Rule implementation, accounting classification, tax treatment, and dependence on specialist providers for liquidity and off-ramp access. The BIS remains sceptical that stablecoins meet the monetary tests of singleness and elasticity, and the IMF notes that most stablecoin turnover still relates to crypto trading rather than ordinary payments. Both caveats matter. Stablecoins are not yet a general-purpose replacement for bank money.

Executive Thesis

Cross-border payments are usually discussed as a payments problem. For CFOs and treasurers, that framing is too narrow. Cross-border payments are also a working-capital problem, a liquidity-allocation problem, a reconciliation problem, a counterparty-experience problem, and a business-model problem. When a company must pre-fund multiple currency accounts, wait through cut-off windows, absorb mid-process compliance pauses, chase payment investigations, and reconcile fragmented statements across banks and PSPs, the real cost sits far beyond the visible fee line.

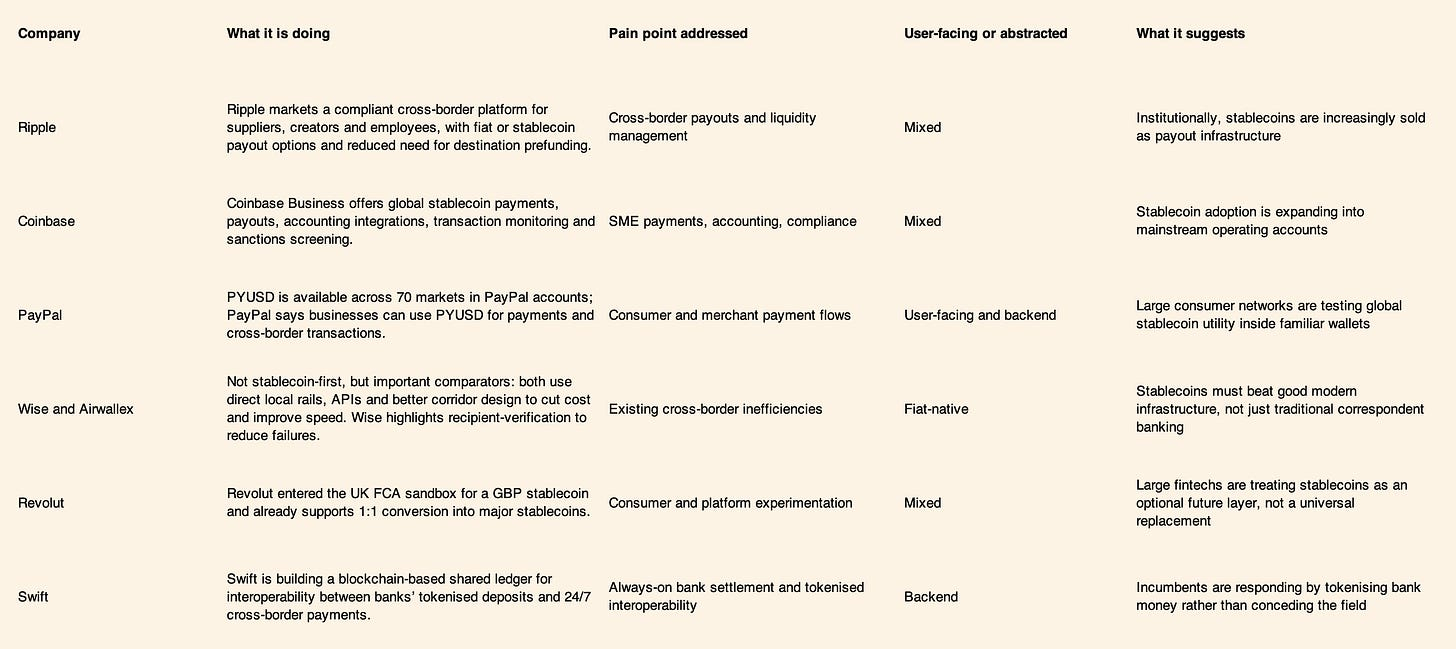

This is why stablecoins matter even if an enterprise has no interest in crypto as an asset class. The relevant innovation is not token speculation. It is the possibility of faster, more programmable, more transparent, more liquidity-efficient settlement infrastructure that can be embedded into regulated enterprise workflows. Stripe, Visa, Mastercard, Circle, Worldpay, Ripple, Coinbase, PayPal, Fireblocks and Swift are all now building products or market positions around this convergence of digital assets and mainstream payments infrastructure. That breadth of activity is the clearest sign that the market is moving from crypto-native experimentation to institutional settlement design.

The thesis of this paper is therefore precise:

Stablecoins are not simply a new payment method. In high-friction cross-border contexts, they can become a programmable settlement layer that changes how companies manage global liquidity, pay counterparties, reconcile transactions, and design international operations.

That thesis is strongest when three conditions hold. First, the pain is real: bank-hour delays, pre-funding, poor corridor coverage, payout failures, or reconciliation drag are economically meaningful. Second, the operating model is enterprise-grade: regulated providers, compliance controls, wallet governance, accounting treatment, and last-mile payout coverage are in place. Third, stablecoins are used selectively and pragmatically, often behind the scenes, rather than forced into customer-facing roles where existing rails already work well.

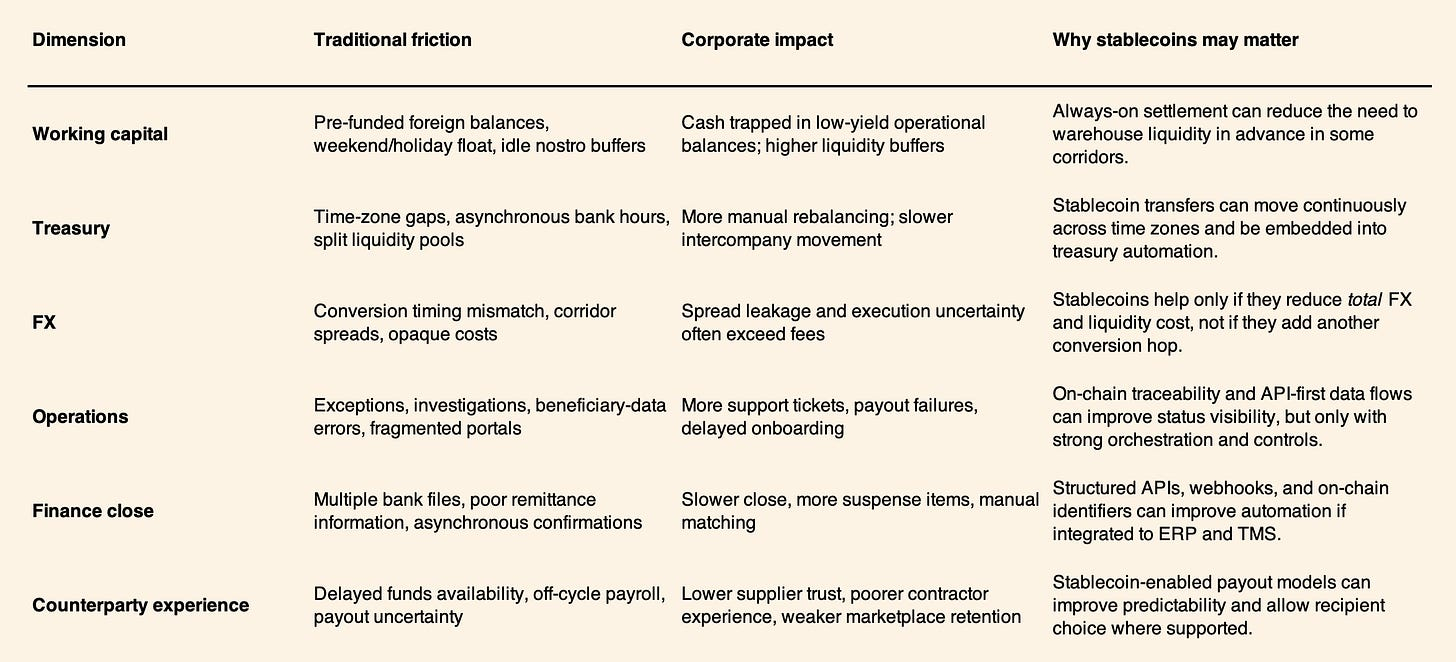

What the friction looks like in finance terms

The Hidden Cost of Cross-Border Payments

The current cross-border system still relies heavily on correspondent banking, sequential message flows, duplicated compliance controls, and fragmented local payment infrastructures. BIS data show that while the value of cross-border payments rose over 2011–22, the number of active correspondents and the number of corridors declined, particularly in emerging regions. The same BIS work notes that cross-border failures are “frequent and expensive”, because each institution in the chain performs its own information checks and, when a problem appears, earlier processing steps must often be unwound.

That matters because the corporate payment journey is rarely linear. A supplier payment may begin in an ERP, move into a treasury management system, be released via a bank API or PSP, route through correspondent banks, pause for sanctions or AML review, convert through one or more FX legs, and then land in a local bank that may or may not be able to apply the credit immediately. A contractor payout on a Friday evening can be “initiated” instantly but still miss local banking windows and settle after the weekend. A marketplace seller payout can be delayed not by core settlement itself, but by funding windows, beneficiary validation, or last-mile banking constraints.

The hidden costs break into three buckets.

Economic friction

The first bucket is explicit and implicit cost. The FSB’s 2025 monitoring of cross-border payment targets shows that in the B2B segment it tracks, average fees were low relative to FX costs: 0.2% in fees versus 1.4% in FX cost, with FX representing 87.1% of total average cost. That is a critical institutional point. It means messaging efficiency alone is not enough; the larger prize is often better liquidity and FX execution design.

The second economic friction is pre-funding and trapped liquidity. Businesses, PSPs, and treasury teams often keep local currency operating balances or rely on pre-positioned liquidity to maintain payout reliability across time zones and holidays. Thunes states that before its USDC integration, pre-funding over traditional rails could take three to five business days and required significant capital in nostro accounts to cover weekends and holidays. That is not just a payments cost. It is an opportunity-cost and cash-efficiency cost.

Operational friction

Operational friction is often under-appreciated because it does not show up as a clean line item. Cross-border flows remain vulnerable to bank cut-off times, local holidays, beneficiary-data mismatches, inconsistent message formats, and payment investigations. Stripe’s guidance on immediate cross-border payments notes that different countries still have different infrastructures, rules, message formats, and clearing windows, while Wise says the “single biggest cause” of payment failures is incorrect recipient details and has launched recipient verification specifically to reduce these failures. In practice, this produces exception queues, support tickets, suspense accounts, and delayed closes.

Reconciliation is a major part of the hidden cost. Many corporates still reconcile across PSP dashboards, multiple bank statements, FX confirmations, and ERP records that were never designed for a single real-time global status layer. BIS and Stripe both point to ISO 20022 and better technical interoperability as important because they reduce manual processes, improve data quality, and enable better automation. Stablecoins are not the only way to improve this, but they do push the operating model toward API-native, event-driven workflows.

Regulatory friction

Regulatory friction is not an external nuisance; it is part of the operating economics. Cross-border payments trigger KYC, KYB, AML, sanctions, fraud, and sometimes local reporting checks across multiple jurisdictions. The BIS notes that these controls are sequenced across the payment chain, creating duplication and delay, and FATF’s 2025 update emphasises that jurisdictions should urgently implement and operationalise the Travel Rule and should pay specific attention to stablecoin risks. In other words, speed is possible only if compliance becomes more automated and more tightly integrated into the flow.

The frictions are not uniform across use cases. Large-value wholesale treasury payments on mature bank rails are already quite efficient: SWIFT/FSB data show 54.6% of wholesale payments credited within one hour and 93.2% within one business day in 2025. By contrast, fragmented payout businesses such as global contractor payroll, creator-economy disbursements, seller settlement, and SME supplier payouts can still suffer from poorer corridor coverage, higher exception rates, and stronger working-capital drag.

Why Stablecoins Matter

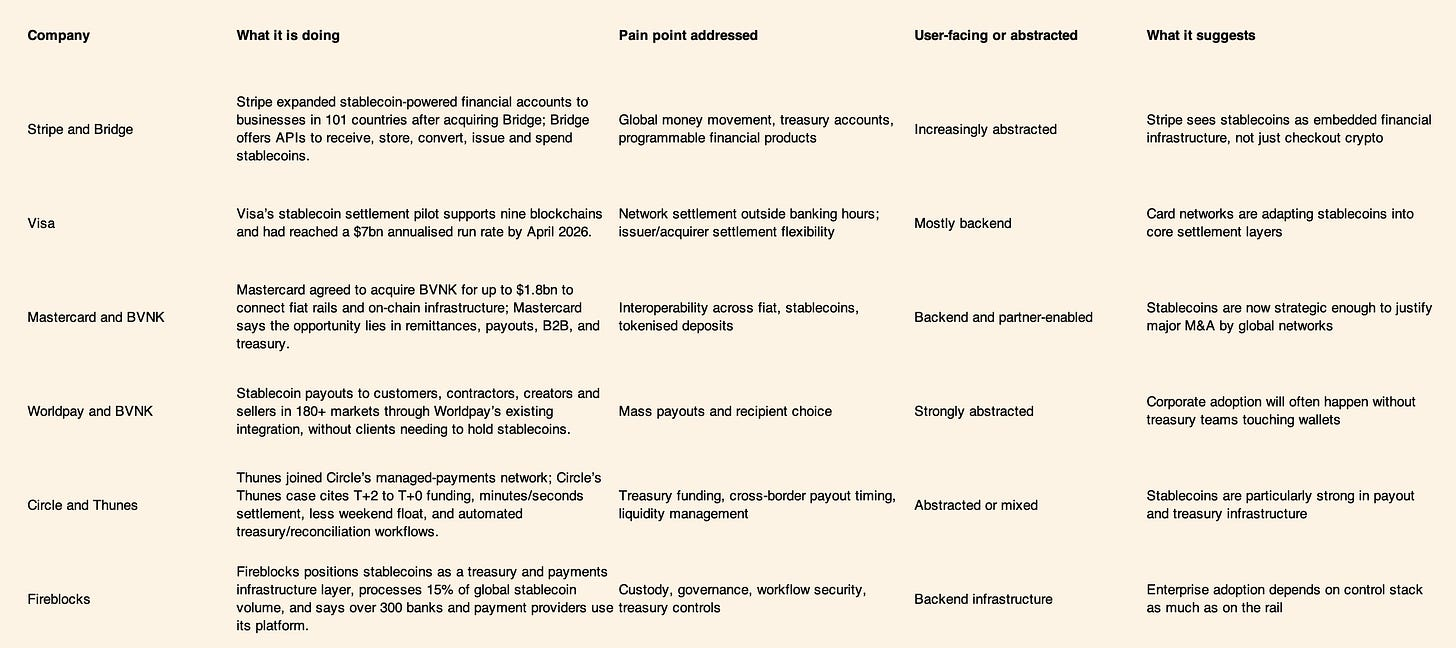

Stablecoins matter in institutional finance because they change the shape of settlement. They are not merely a digital bearer of fiat value. In an enterprise setting, they can provide always-on movement of value, programmable transfer logic, transparent transaction status, API-native connectivity, and new forms of liquidity routing between disjoint fiat systems. That is why major incumbents increasingly describe them in infrastructure terms: Bridge as “the end-to-end stablecoin platform”; Circle as “managed payments” for PSPs, banks, and enterprises that do not want to manage digital assets directly; Visa as a common multi-chain settlement layer; Mastercard as interoperability between fiat rails and stablecoins.

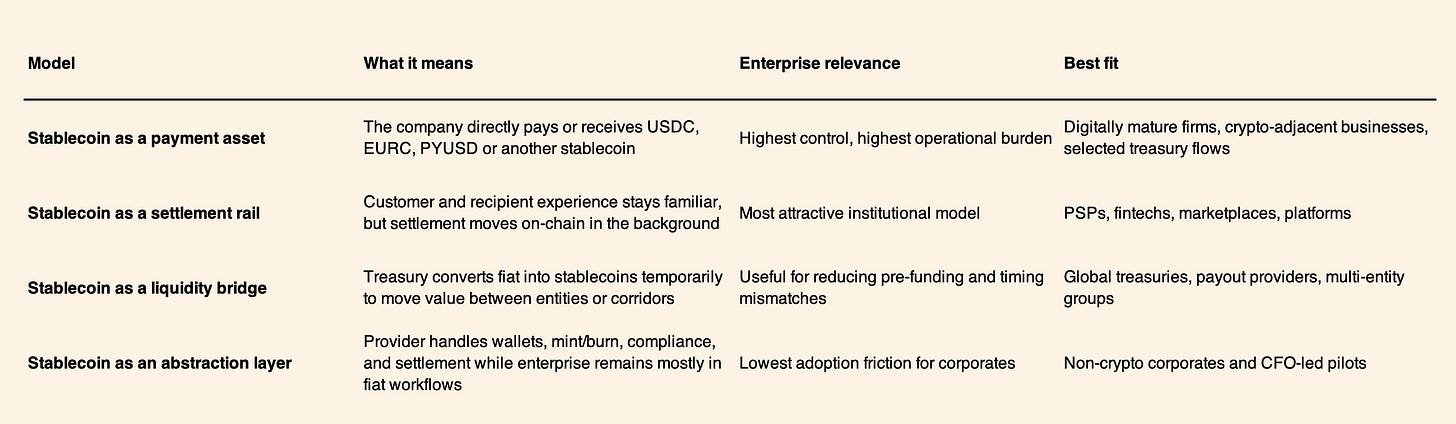

It is important, however, to separate four different concepts that are often collapsed into one.

Stablecoins as payment asset, rail, bridge, and abstraction

The last model is gaining the most institutional traction. Worldpay’s stablecoin payout service with BVNK allows clients to pay beneficiaries in 180+ markets “without having to hold or handle stablecoins themselves.” Circle’s CPN Managed Payments says the same thing in different language: PSPs, banks, fintechs, and global enterprises can access stablecoin settlement “without managing digital assets directly.” This is the state of the market in 2026. The most scalable corporate design is often not direct wallet-based adoption, but regulated abstraction.

The innovation, then, is not simply the token. It is the operating architecture around the token:

- always-on settlement,

- composable APIs and webhooks,

- visible transfer status,

- programmable routing and split settlement,

- continuous liquidity movement,

- easier embedding into software,

- and the possibility of linking value movement more tightly to treasury and ERP logic.

That said, the institutional caveat is essential. The IMF notes that most stablecoin turnover still relates to crypto trading and that around 80% of transactions are conducted by bots and automated systems for arbitrage and rebalancing. Cross-border payments use is increasing, but it is still only part of the story. Stablecoins are therefore commercially relevant, but not yet proof of universal mainstream payment adoption.

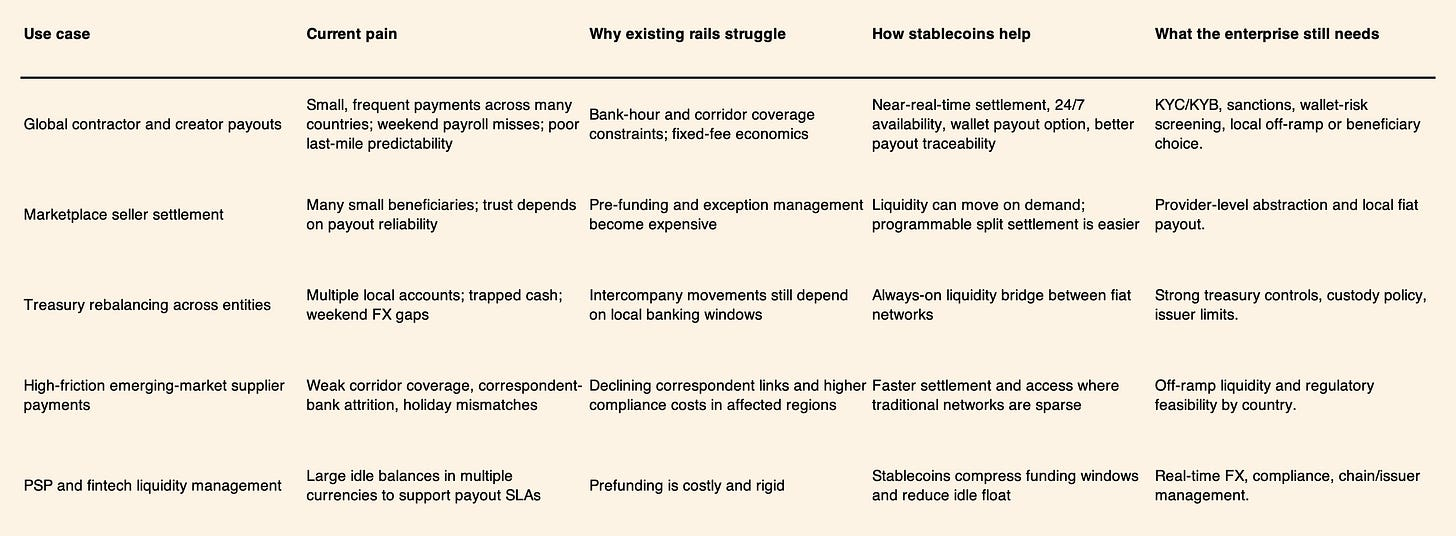

Where Stablecoins Win and Where They Do Not

Stablecoins win when they solve a specific friction that existing rails do not solve well enough. They do not win merely because on-chain transfer is fast.

Where the strongest advantages exist

The highest-conviction use cases are those where the corporate pain is concentrated in timing, liquidity, access, and exception handling rather than in front-end checkout alone.

The strongest currently documented enterprise example is Thunes. Circle’s case study states that funding windows moved from T+2 to T+0, settlement improved from multi-day pre-funding delays to minutes or seconds, and continuous 24/7 liquidity reduced the need to hold excess float over weekends and holidays. That is exactly the kind of treasury outcome CFOs should care about.

Mastercard’s May 2026 partnership with Yellow Card is another important signal. The focus markets are Ghana, Kenya, Nigeria, South Africa, and the UAE, and the partnership explicitly targets cross-border remittances, B2B settlement, and treasury management. The message is not that cards are being replaced. It is that network-scale incumbents see stablecoins as especially relevant in higher-friction regions where banking connectivity and local settlement quality are uneven.

Where stablecoins do not win yet

Stablecoins are less compelling in mature corridors that already have good economics and high reliability. The case against indiscriminate adoption has three parts.

First, modern non-stablecoin challengers have already removed much of the pain in selected corridors. Wise reported a 0.53% cross-border take rate and 65% instant transfers in FY25, and says 80% of global payments via Wise Platform are instant and 88% arrive within 24 hours for the Upwork programme it references. Airwallex promotes interbank FX, local collections, and transfers to 200+ countries through its proprietary local payments network. In these settings, stablecoins do not automatically beat the available alternative.

Second, off-ramp economics can destroy the benefit. Jack Zhang’s public criticism in June 2025 focused on a hard operational truth: if a recipient still needs local fiat in a bank account, stablecoin-to-fiat conversion may be more expensive than an interbank FX route in mainstream currencies. That critique remains valid in many G10-to-G10 flows. Airwallex’s own 2026 writing shows a more nuanced position, describing stablecoins as “the newest and most exciting innovation” and acknowledging they serve poorly covered corridors well, especially in retail and consumer contexts. The evolution of his view is instructive: scepticism about blanket superiority can coexist with strategic openness to selective infrastructure use.

Third, some use cases fundamentally favour existing rails. Mastercard notes that card payments still provide unmatched reach, acceptance and consumer protections. Wherever dispute resolution, chargebacks, or regulated consumer protection are central, stablecoins are more likely to sit behind the scenes than in front of the user. The same is true where local tax, payroll, or safeguarding regimes require deep domestic-bank integration.

Airwallex and Jack Zhang

Jack Zhang’s early 2025 scepticism was not a rejection of technology; it was a corridor-level economic argument. In his public post, he argued that off-ramping stablecoins into bank-delivered local fiat could be more expensive than using interbank FX in mainstream currency pairs. That is a serious institutional point and one this paper broadly agrees with for mature G10 corridors.

By March 2026, Zhang’s framing had evolved materially. Airwallex’s official blog described stablecoins as “the newest and most exciting innovation” and acknowledged “near-instant settlement, lower fees, and access to corridors that traditional rails serve poorly,” particularly for retail and consumer use cases. Airwallex’s own published 2026 trends piece also expects stablecoin adoption to continue growing as regulated digital dollars and tokenised deposits move from pilots into early use.

The institutional reading is this: a high-quality global payments company does not need to become crypto-native to shift from scepticism to exploration. It simply needs to observe that stablecoins can be uneconomic in mainstream corridors yet valuable in difficult ones. That is exactly the broader market pattern now emerging.

Market Map and CFO-Grade Implementation Model

Market map and case studies

The market map below highlights what the leading firms are actually doing.

Implementation model

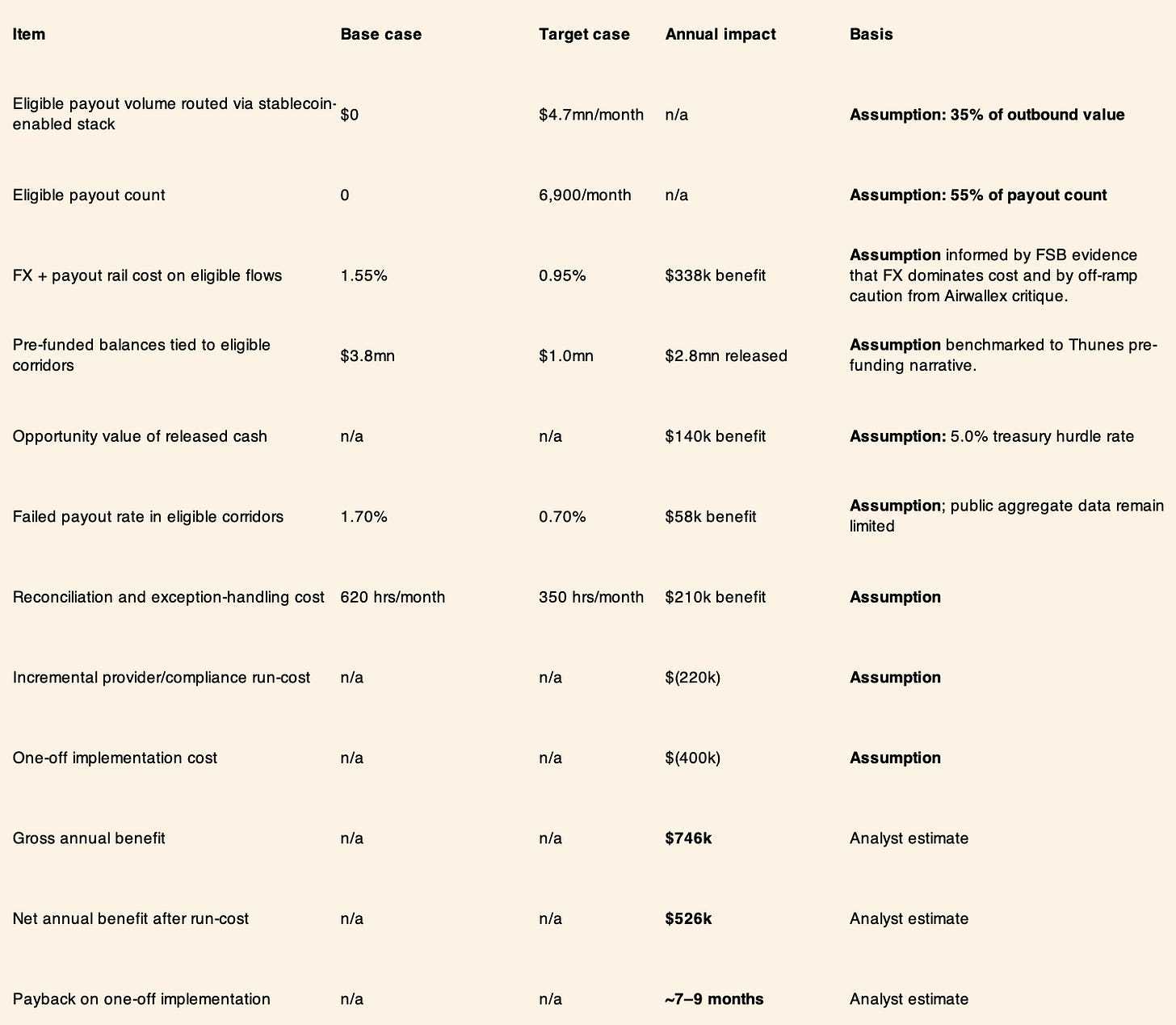

Company profile.

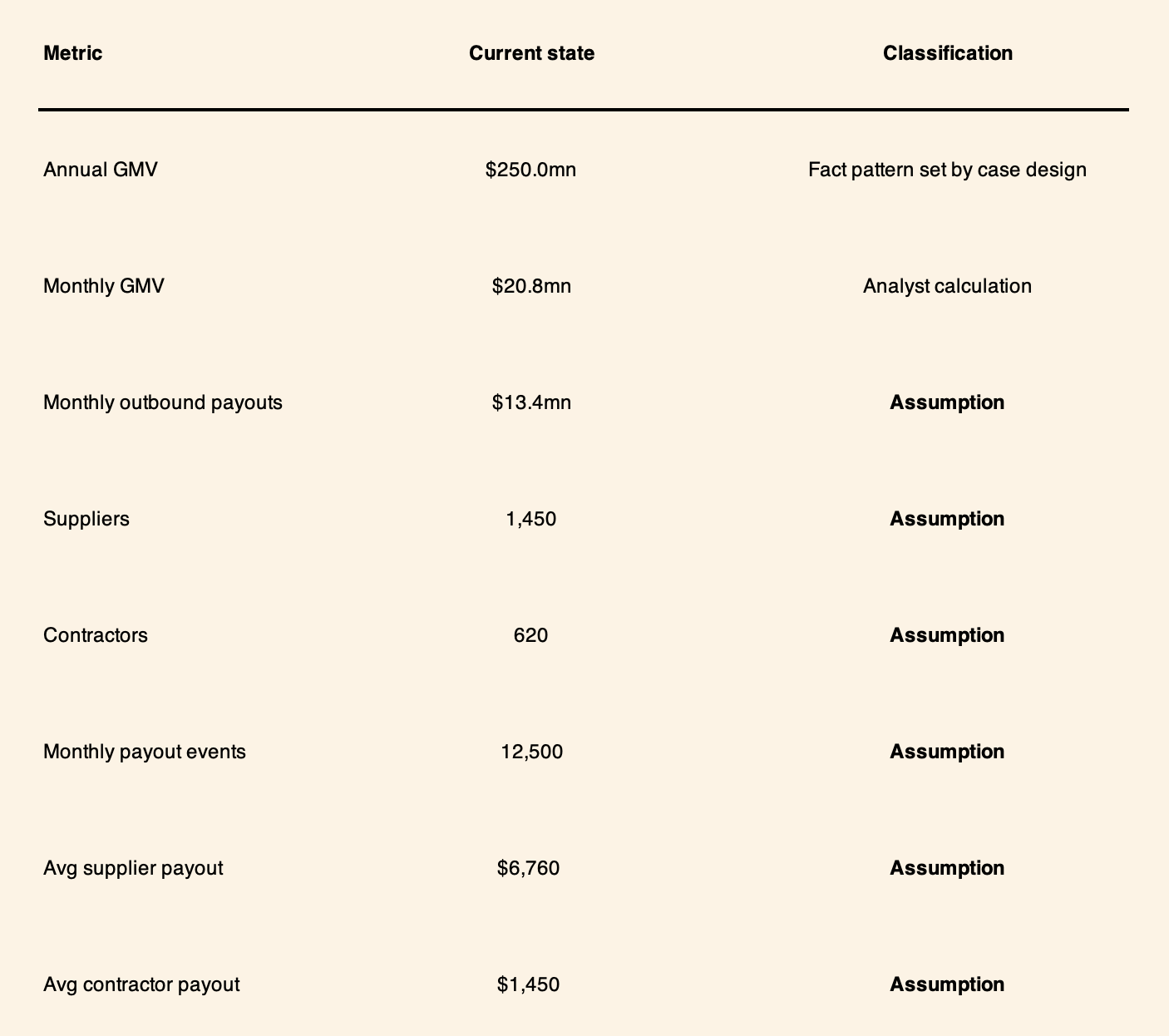

A fictional global B2B marketplace and SaaS-enabled commerce platform with $250mn annual GMV, operations in 40 countries, customers in the US and Europe, suppliers in Latin America and Southeast Asia, and a globally distributed contractor base.

Current-state operating profile.

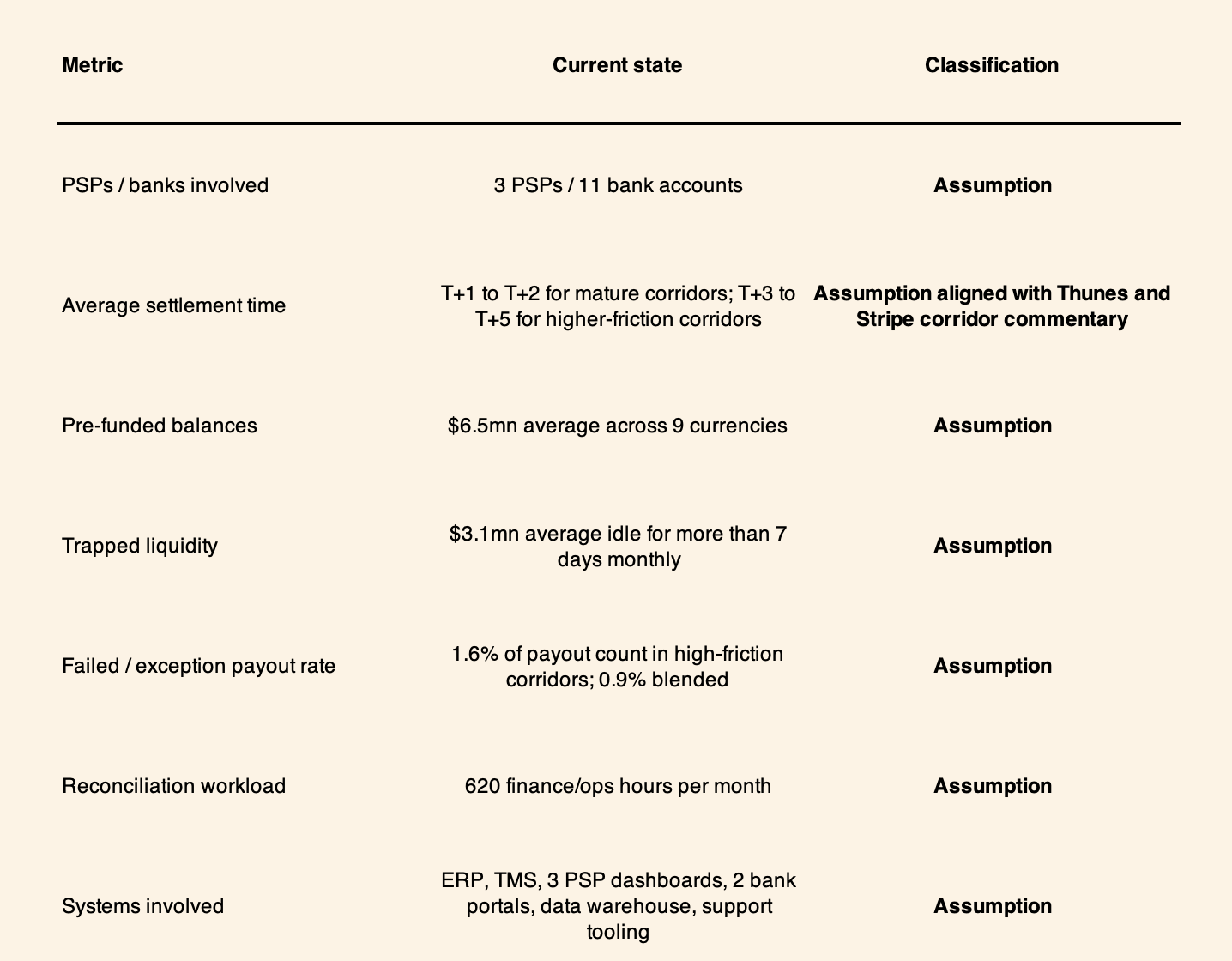

The platform collects customer funds in fiat via existing PSPs and local payment methods. Payouts are made through three PSPs, multiple local bank accounts, and a small number of FX counterparties.

This profile is typical of a mid-sized global platform that has already modernised collections but still runs payouts and treasury on fragmented rails. The constraint is not customer checkout. It is the cost of global disbursement reliability.

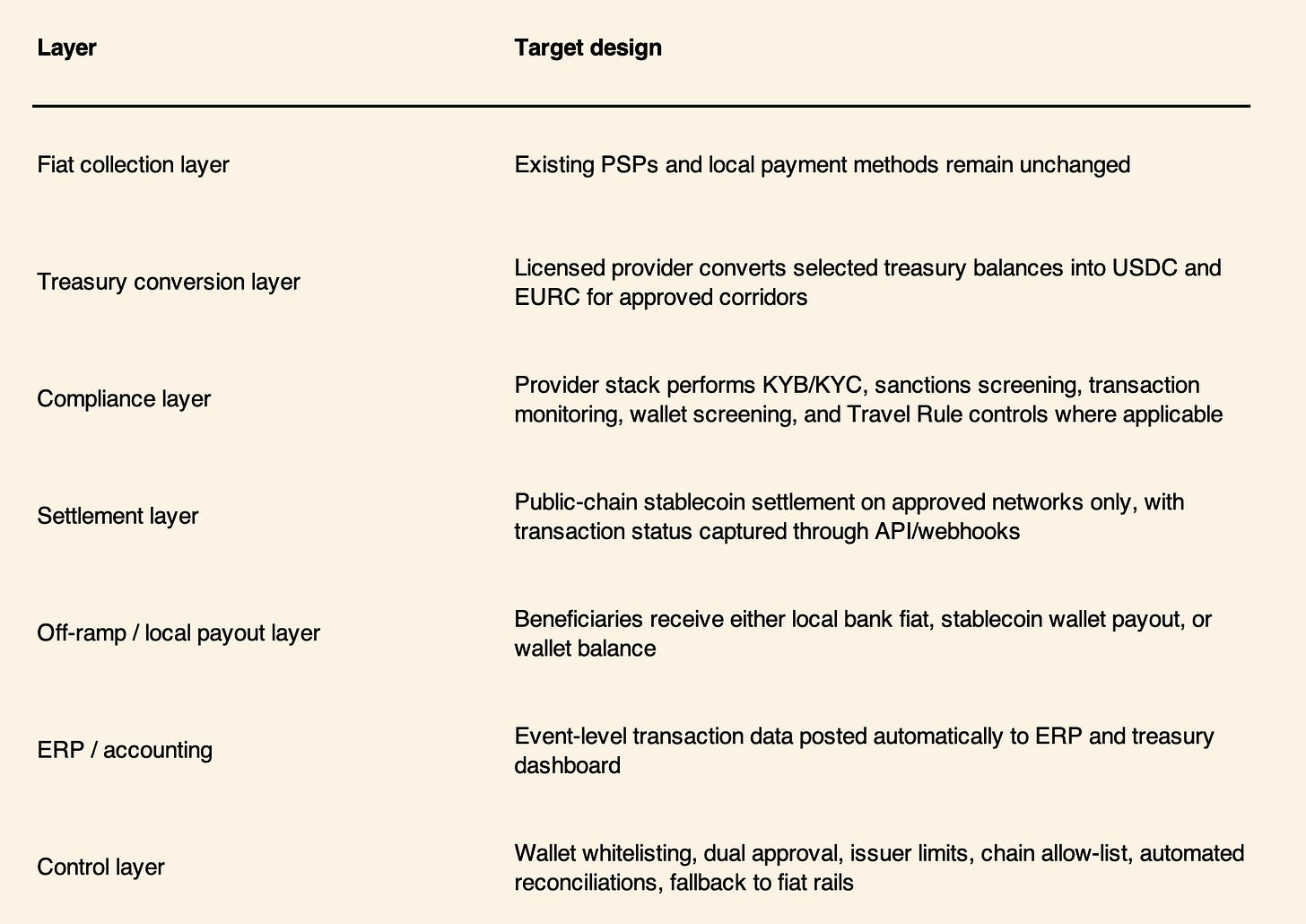

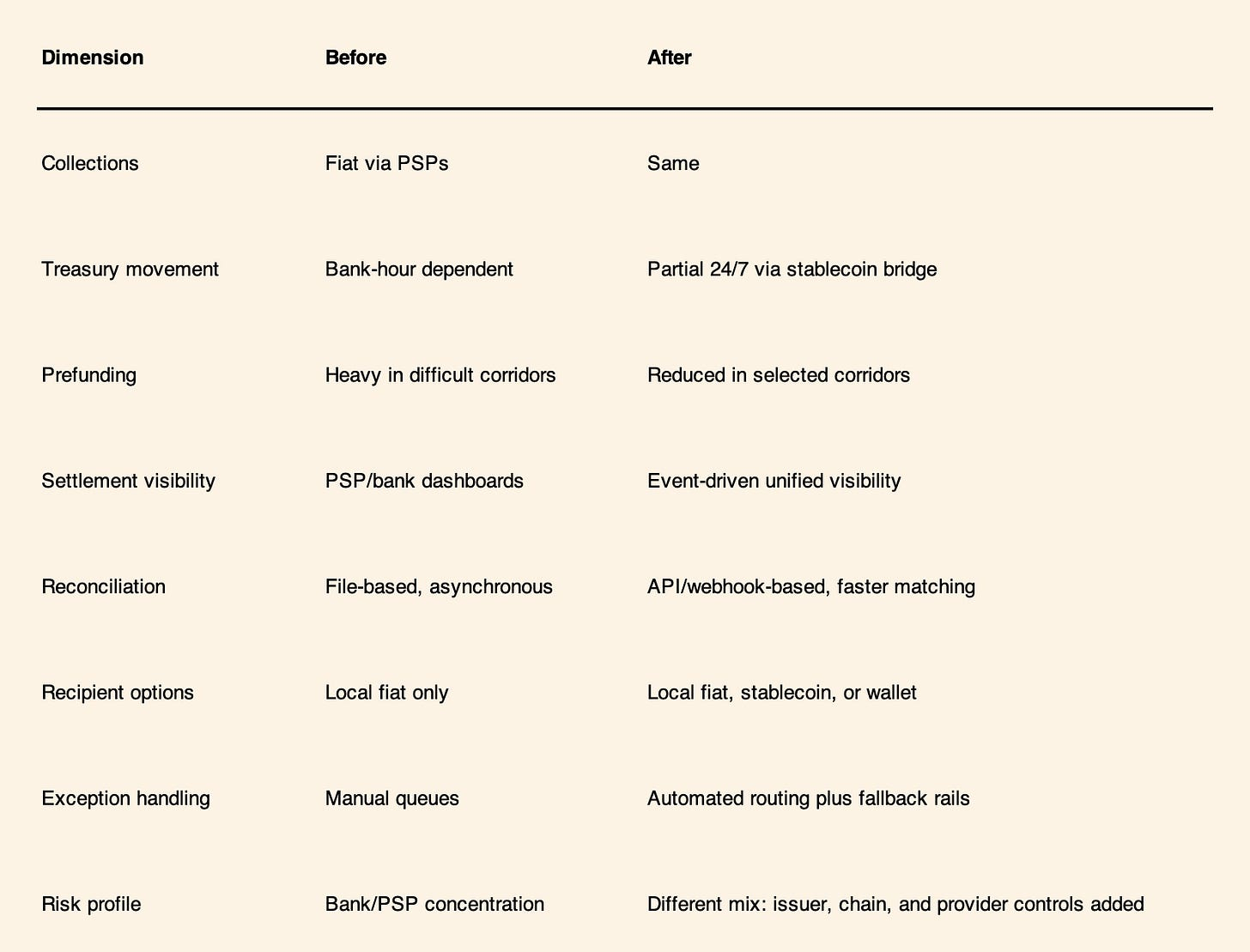

Stablecoin-enabled target architecture

The company does not change customer collection. Customers still pay via cards, ACH, SEPA, local account transfers, and existing PSPs. Treasury converts selected USD and EUR liquidity into regulated stablecoins through licensed providers only for pre-approved corridors and use cases. Recipients can receive local fiat, stablecoin, or platform wallet balance depending on corridor, regulation, and preference.

Step-by-step payment flow

- Customer collections remain fiat-native and settle to existing treasury accounts.

- TMS identifies eligible payout corridors based on rule engine: corridor, amount, urgency, SLA, provider availability, recipient preference, and compliance score.

- Treasury converts a defined tranche of USD/EUR liquidity into approved stablecoins through a regulated provider.

- Funds move on-chain to the provider or orchestrated payout partner.

- Provider conducts sanctions checks, Travel Rule logic where required, ongoing monitoring, and beneficiary routing.

- Beneficiary receives local fiat, stablecoin, or platform wallet balance.

- Webhooks feed ERP, TMS, and dashboard with timestamp, amount, network fee, FX rate, beneficiary status, and reconciliation references.

- Exceptions automatically route to operations queues; non-eligible corridors revert to fiat rails.

This model is closest to the Worldpay/BVNK and Circle-managed-payments pattern, where the enterprise benefits from stablecoin settlement without having to become a crypto-native operator.

Financial model

The main financial gain is not “blockchain is cheaper.” It is a combination of lower corridor friction, less idle liquidity, fewer exceptions, and better operating leverage. The prize is usually balance-sheet efficiency plus back-office efficiency, not just lower transaction fees.

Before-and-after architecture

Decision Framework, Risks, Roadmap, and Conclusion

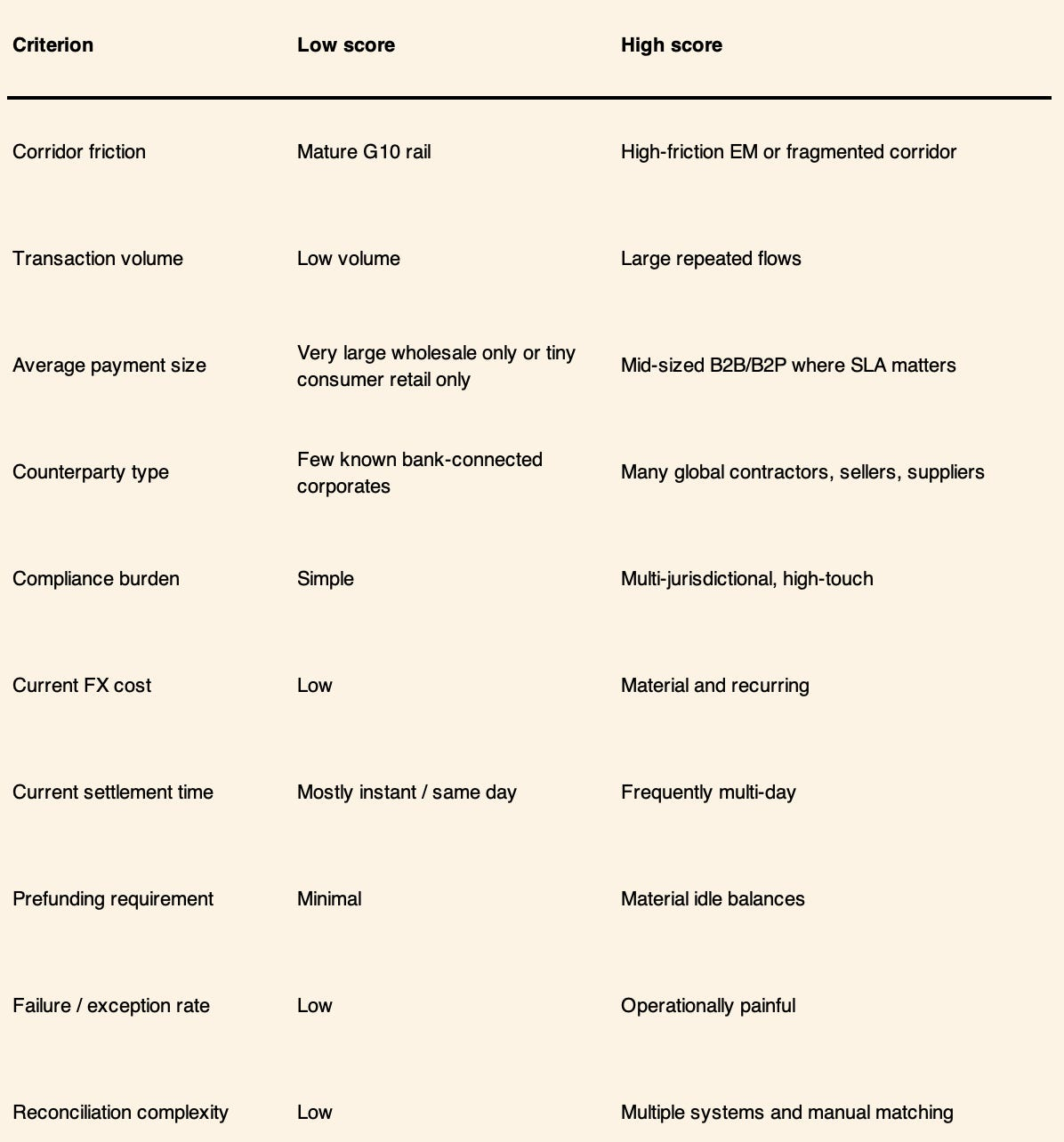

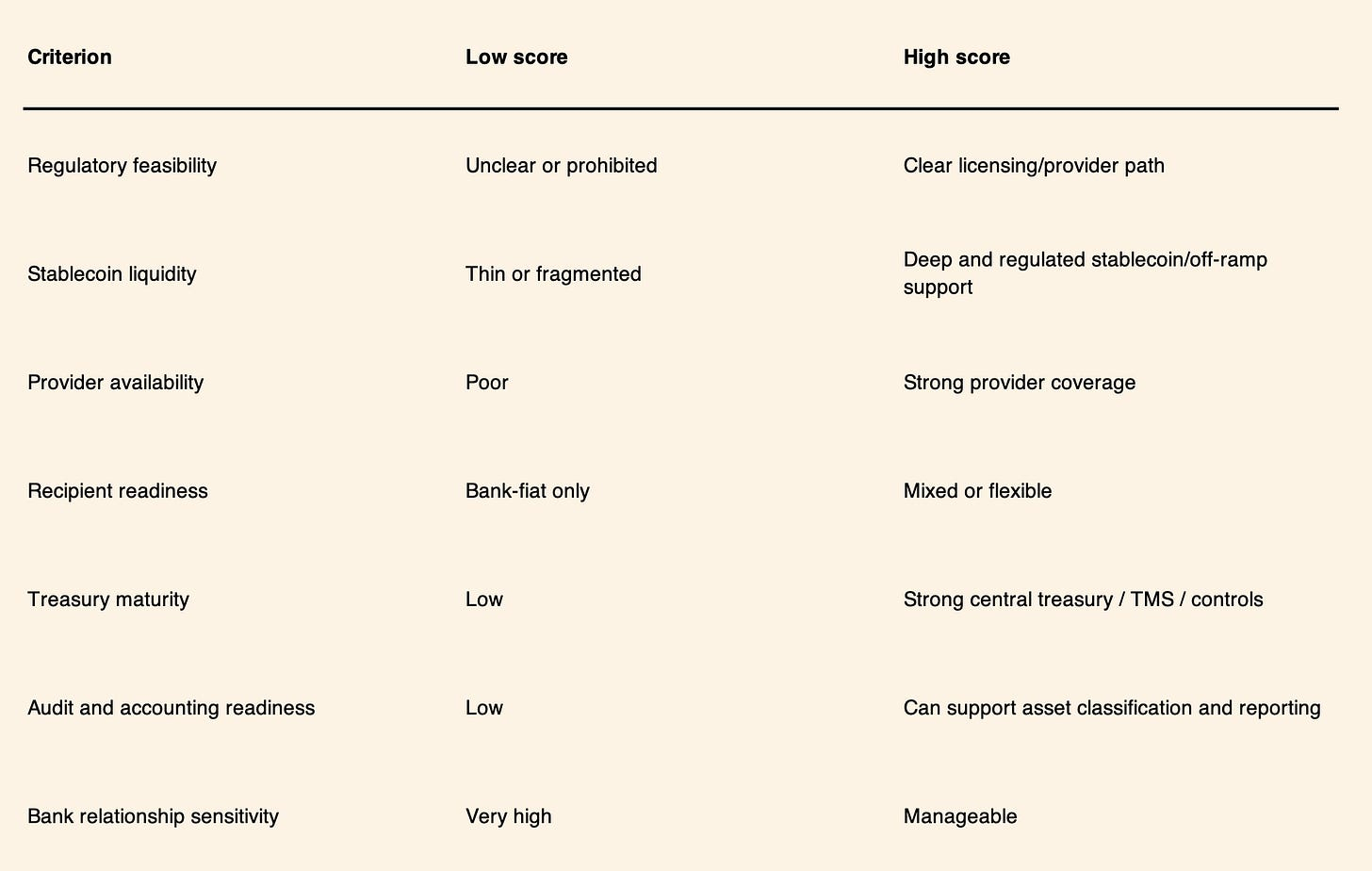

The matrix below is an analyst tool, not an industry standard. It is designed to help decide whether stablecoins are irrelevant, experimental, or strategically important.

Scoring method.

Score each criterion from 1 to 5.

Any company scoring high on corridor friction, prefunding, reconciliation complexity, and provider availability should move faster than a company scoring high only on general innovation interest. Stablecoins should be approved because they solve a measurable treasury problem, not because peers are experimenting.

Enterprise-grade stablecoin-enabled payment stack

The direct-versus-abstracted choice is central. Direct stablecoin adoption offers more control, but most corporates will initially prefer provider-abstracted stablecoin settlement. That is the model currently being reinforced by Worldpay/BVNK, Circle Managed Payments, and many Stripe/Bridge customer narratives.

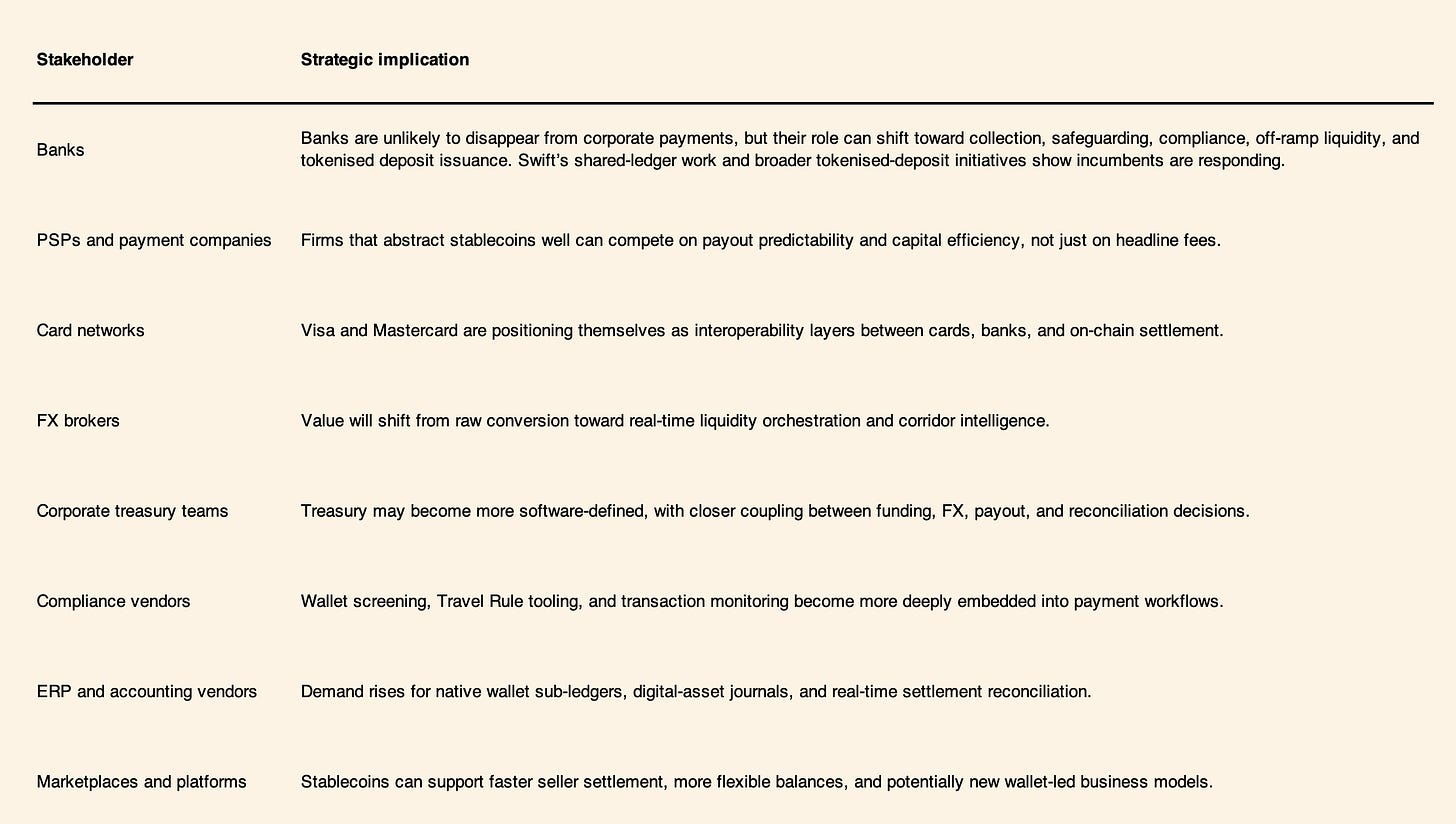

Strategic implications

Open questions and conclusion

Public evidence is still uneven in four areas. First, there is little high-quality public data on aggregate enterprise payment-failure rates and the exact amount of labour consumed by reconciliation in cross-border B2B settings. Second, many provider case studies report strong benefits but remain vendor-authored and should be treated as directional rather than independent proof. Third, accounting treatment for some stablecoins still depends heavily on legal rights, redemption terms, and jurisdiction-specific facts. Fourth, regulatory regimes are clearer in some major markets than they are on a truly global basis, so corridor-by-corridor feasibility remains essential.

Stablecoins are not a universal replacement for banks, card networks, or fiat payment rails. They are a new settlement primitive. Their value becomes clear when they are embedded into regulated, compliant, enterprise-grade payment workflows that solve real treasury and operating problems.

The opportunity is not “crypto adoption.” The opportunity is to rebuild selected parts of corporate money movement around speed, liquidity efficiency, programmability, transparency, automation, and global interoperability. In that world, stablecoins are less a product category than a settlement capability.

For CFOs, the right stance is neither evangelism nor dismissal. It is disciplined selection. Where existing rails already deliver speed, cost efficiency, and reliability, stablecoins may add little. Where pre-funding, weekend delays, corridor fragmentation, payout unreliability, and reconciliation drag are material, stablecoins can already be economically and operationally relevant. The winners will be the firms that treat them as infrastructure, not ideology.

Source list

Public-sector and standards sources

BIS Bulletin 87, Next generation correspondent banking; BIS Papers 167, Cross-border payment technologies; BIS Annual Economic Report 2025 chapter on the next-generation monetary and financial system; BIS statistics on cross-border bank claims; FSB G20 Roadmap for Enhancing Cross-border Payments: Consolidated progress report for 2025; FATF 2025 targeted update on virtual assets and VASPs; ESMA MiCA materials; EBA MiCA supervision materials; White House / Reuters coverage of the GENIUS Act; IMF Departmental Paper Understanding Stablecoins; IMF blog on stablecoins and global payments.

Infrastructure and market sources

Visa stablecoin settlement updates; Mastercard acquisition of BVNK and Yellow Card partnership; Swift digital-asset and shared-ledger announcements; Worldpay/BVNK payout release; Circle CPN Managed Payments and Thunes case study; Stripe/Bridge product and thought-leadership materials; Fireblocks stablecoin infrastructure materials; Ripple cross-border payments materials; Coinbase Business materials; PayPal PYUSD releases; Wise and Airwallex public materials.

Accounting and audit references

KPMG on ASU 2023-08; Deloitte implementation guidance on crypto assets and stablecoins; Deloitte and EY IFRS commentary.

Partner Highlight

At insights4vc, we pay attention to teams that are not just shipping products, but shaping categories.

Moto is one of them. The company is building a premium card experience positioned as an alternative to traditional incumbents such as Amex, combining a high-end user interface with more modern financial infrastructure.

Moto is currently expanding access to a limited testing group. If you would like to test the product, please contact us at: [email protected]

Cover Artwork

Too Early

James Tissot c. 1873

Risk Disclaimer:

insights4.vc and its newsletter provide research and information for educational purposes only and should not be taken as any form of professional advice. We do not advocate for any investment actions, including buying, selling, or holding digital assets.

The content reflects only the writer’s views and not financial advice. Please conduct your own due diligence before engaging with digital assets or related technologies, as they carry high risks and values can fluctuate significantly.