The genesis of artificial intelligence investment is best understood as a transition from military necessity to commercial possibility. In the mid-20th century, the costs and uncertainty associated with advanced computation were so extreme that the state functioned as the only feasible investor. Commercial pathways were unclear, markets were unproven, and private capital had little incentive to participate.

This initial phase, spanning from the end of World War II to the mid-1950s, quietly established the physical infrastructure and theoretical foundations upon which modern venture capital would later build.

Context

Last month marked the publication of Artificial Intelligence: Law and Regulation (Second Edition, Edward Elgar Publishing, 2026). At insights4vc, we contributed Chapter 18, “Investing in AI,” which traces the evolution of AI venture capital across cycles of innovation, regulation, and market maturity. We are grateful to Charles Kerrigan, Partner at CMS UK, for his editorial leadership, as well as to the broader group of contributors whose rigor defines the book.

Table of contents

The book brings together lawyers, technologists, regulators, and academics to map the legal, ethical, and commercial frameworks shaping AI globally, covering areas such as the EU AI Act, intellectual property, data protection, competition law, governance, and sector-specific AI deployment across finance, healthcare, and infrastructure.

For enquiries regarding the book, please contact: [email protected]

On the occasion of its release, we decided to revisit and expand this analysis by tracing the Investing in AI landscape from its earliest origins to the present day. Many market participants remain unaware that the foundations of AI investment were laid not in the last decade, but in state-funded research programs of the 1950s. This paper builds on that historical arc, connecting those early roots to today’s highly concentrated, capital-intensive AI venture ecosystem.

Military Origins of Large-Scale Computation

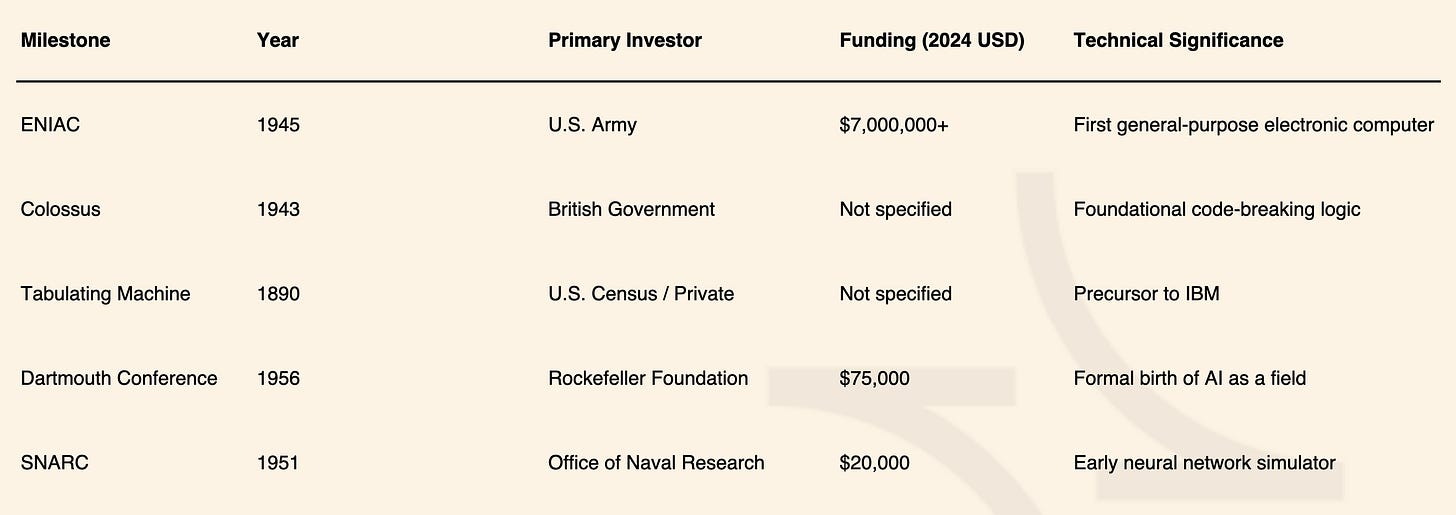

A defining milestone of this era was the Electronic Numerical Integrator and Computer (ENIAC), completed in 1945 with funding from the U.S. Army Ballistic Research Laboratory. With an original cost of approximately $500,000, equivalent to over $7 million in 2025-adjusted terms, ENIAC was a logistical and technical behemoth. It weighed roughly 30 tons, used 18,000 vacuum tubes, and consumed massive amounts of power.

Its purpose was narrowly defined but strategically critical: the rapid calculation of artillery firing tables. In this role, ENIAC performed calculations roughly 1,000 times faster than contemporary electro-mechanical machines, demonstrating for the first time the operational superiority of fully electronic computation.

Parallel efforts in the United Kingdom, most notably the Colossus machines at Bletchley Park, reinforced the strategic value of computation in wartime contexts. These systems were designed for cryptographic analysis and code-breaking rather than general-purpose calculation, but they similarly underscored the military utility of computational power.

Absence of Private Capital and Commercial Incentives

Despite their technological significance, these early systems existed in a near-total vacuum of commercial scalability. Government sponsors prioritized immediate operational effectiveness, not profitability, productization, or mass adoption. As a result, private investment was almost entirely absent during this period.

This hesitation had historical precedent. In the 19th century, Charles Babbage’s Analytical Engine had already illustrated the risks of premature private backing. Babbage’s failure was not a function of insufficient technical vision, but of external constraints: precision manufacturing was not yet viable at scale, and industrial demand for advanced computation had not materialized. Capital markets had learned, implicitly, that being too early could be fatal.

Key Early Computational Milestones

First Bridge to Commercialization

The initial shift from purely state-driven tools to commercial enterprise emerged through Herman Hollerith’s tabulating machine, developed for the 1890 U.S. Census. By dramatically reducing census processing time, the machine demonstrated a clear productivity benefit with immediate economic value. Hollerith’s venture evolved into the Tabulating Machine Company, which later became IBM, providing one of the earliest templates for translating government-funded innovation into private-sector scale.

Theoretical Foundations as Investable Capital

By the late 1930s and 1940s, theoretical advances began to complement physical infrastructure. Claude Shannon’s application of Boolean algebra to digital circuits and John von Neumann’s stored-program architecture for the EDVAC reframed computation as a scalable, general-purpose technology rather than a bespoke military instrument.

These intellectual breakthroughs did not immediately unlock venture capital, but they laid the groundwork for future investment by clarifying how abstract research could translate into repeatable, economically viable systems. In retrospect, this period marks the quiet accumulation of intellectual capital that would later make private investment in computation, and eventually artificial intelligence, not only possible but inevitable.

Institutional Foundations and the First Wave of Optimism (1956–1973)

The formalization of artificial intelligence as an academic and investment discipline began with the 1956 Dartmouth Conference, funded by a $7,500 Rockefeller Foundation grant (approximately $75,000 today). The conference brought together early pioneers such as John McCarthy and Marvin Minsky, setting a research agenda that would define the field for decades and laying the groundwork for early institutional capital involvement.

By the early 1960s, government funding became the dominant force behind AI development. Agencies such as ARPA (now DARPA) emerged as primary sponsors, most notably through the $2.2 million grant (roughly $20 million today) allocated to MIT’s Project MAC. This initiative played a foundational role in the development of time-sharing systems and advanced John McCarthy’s LISP programming language, which remains a landmark in AI history.

Corporate interest began to surface during this period, albeit cautiously. IBM’s early support for neural network research signaled initial private-sector recognition of AI’s long-term potential. Despite this, commercialization remained elusive. Development cycles were long, hardware costs were high, and technological constraints were severe. For example, the UNIVAC I offered just 1 kB of memory, dramatically limiting algorithmic complexity.

As a result, investors were highly conservative. AI applications were confined largely to scientific and academic contexts, public awareness was minimal, and credible exit pathways were scarce.

By the late 1960s, a recurring pattern in AI history began to emerge. Expectations scaled faster than hardware capabilities. While projects such as DENDRAL and MYCIN demonstrated the promise of expert systems, their extended timelines and mounting costs strained both government sponsors and early private backers.

Cycles of Disillusionment: The AI Winters

The investment history of AI is defined by repeated periods of contraction known as AI Winters, during which funding and interest declined sharply following unmet expectations. These cycles are critical for understanding today’s venture capital approach, which places greater emphasis on incremental progress and near-term validation.

The First AI Winter (1974–1980)

The first downturn was triggered by a series of influential critiques that questioned the viability of AI research.

1966: ALPAC Report

Concluded that machine translation had failed to justify Cold War-era investment, leading to sharp funding cuts in natural language processing.

1969: Perceptrons by Minsky and Papert

Demonstrated the mathematical limitations of simple neural networks, halting progress in that area for nearly a decade.

1973: Lighthill Report (UK)

Criticized the lack of practical outcomes in AI research, prompting a major reduction in public funding.

In response, U.S. defense agencies, including DARPA, reallocated resources toward immediate military applications. Academic AI research entered a prolonged period of stagnation through the remainder of the 1970s.

The Second AI Winter (1987–1993)

A renewed wave of optimism in the early 1980s drove AI investment to nearly $1 billion by 1985, largely focused on expert systems designed for narrow decision-making tasks.

Some commercial successes emerged. Digital Equipment Corporation’s XCON system delivered meaningful operational savings. However, the broader ecosystem proved fragile.

The downturn began in 1987, driven by several structural failures:

- The collapse of the LISP machine market as general-purpose workstations became cheaper and more capable

- High maintenance costs and poor scalability of expert systems

- The end of major public initiatives, including the U.S. Strategic Computing Initiative

- Japan’s Fifth Generation Computer Project failing to meet its objectives

By the late 1980s, private capital retreated sharply, triggering consolidation, shutdowns, and widespread bankruptcies among early AI firms.

Summary of AI Winter Phases

The Renaissance: Embedded Systems and the First Sustained VC Surge (1994–2020)

Following the second AI winter, the industry adopted a more restrained strategy. AI was no longer positioned as a standalone “thinking machine,” but embedded quietly into existing software and hardware systems.

This period saw:

- The revival of neural networks and fuzzy logic

- Falling hardware costs

- The rise of “soft computing” techniques

- Gradual reintegration of AI into commercial products

In the early 2000s, robotics regained visibility through commercially viable products such as the iRobot Roomba. At the research level, advances in deep learning accelerated, including the development of Long Short-Term Memory (LSTM) networks by Hochreiter and Schmidhuber.

By the 2010s, AI had become a central pillar of global innovation. Several milestones marked this transition:

- IBM Watson winning Jeopardy!

- Google’s early self-driving car initiatives

- The success of AlexNet (2012), which demonstrated the scalability of deep learning using modern hardware

Between 2012 and 2020, venture capital investment in AI grew at a 45% CAGR, expanding from under $3 billion to nearly $75 billion.

Investment activity concentrated heavily in two regions. By 2020, the United States and China accounted for over 80% of global AI funding. U.S. firms led with 57% of total investment, while China surged rapidly after 2015, peaking in 2018 before stabilizing at $17 billion, representing 24% of global funding.

Sector-wise, capital flowed most heavily into:

- Mobility and autonomous vehicles, which attracted approximately $95 billion between 2012 and 2020

- Healthcare, where AI investment doubled in 2020 alone, reaching $12 billion, driven by pandemic-related demand

The Generative Epoch: Resilience and Hyper-Growth (2021–2024)

The launch of large-scale generative models marked a new phase of investment concentration in venture capital. Despite a broader market slowdown in 2024, AI deal activity proved notably resilient.

In Q3 2024, global AI deal activity increased 24% quarter over quarter, reaching 1,245 deals. This period also saw the emergence of the “AI Unicorn” phenomenon. Thirteen new AI unicorns were created in Q3 2024 alone, accounting for more than half of all newly minted venture unicorns globally.

Several companies secured outsized financings during this phase. xAI, Anthropic, and CoreWeave each raised multi-billion-dollar rounds, even as total venture funding declined slightly due to a reduction in mega-rounds above $1 billion.

Diverging Investment Paths

By late 2024, capital allocation strategies began to split into two distinct tracks:

Infrastructure-layer leaders

Companies such as NVIDIA dominated capital inflows. However, the capital-intensive nature of hardware and compute infrastructure significantly constrained new venture entry.

Application-layer startups

Growth-stage capital increasingly flowed to application-layer companies, particularly those operating under a “Service-as-a-Software” model, where revenue is outcome-driven rather than subscription-based.

The 2025 Intelligence Supercycle: A Record-Breaking Year

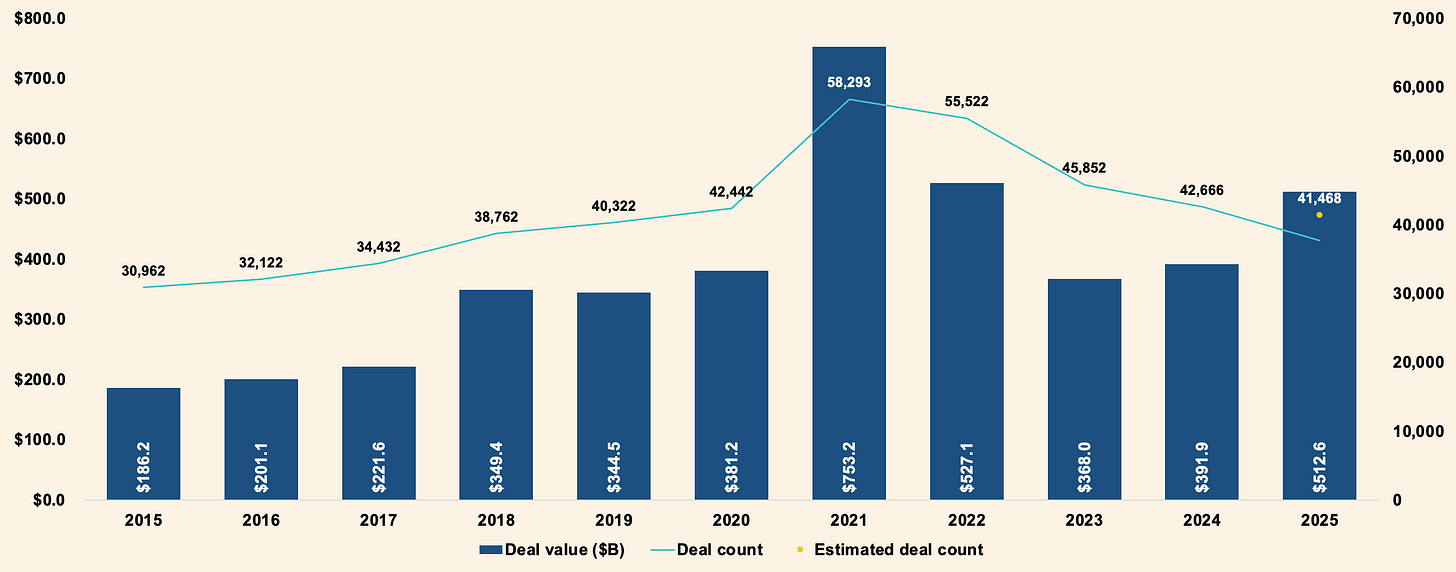

By 2025, AI and machine learning have moved from a high-growth subsector to the central axis of global venture capital, accounting for over 52% of total VC deal value and more than 31% of deal count. This shift reflects not only sustained capital inflows, but a structural repricing of AI as the core driver of future economic productivity rather than a speculative technology theme. While overall global VC deal counts have compressed since the 2021 peak, AI deal activity has remained resilient, with rising average check sizes signaling growing conviction rather than breadth-driven exuberance.

Global VC deal activity

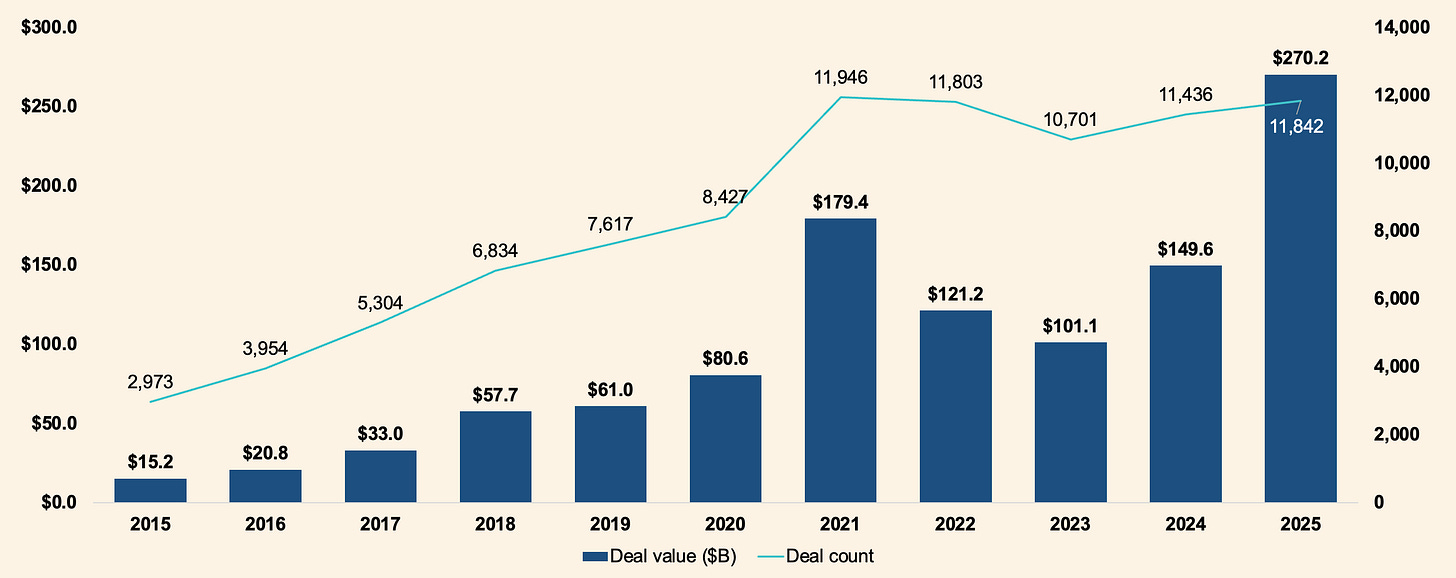

Capital intensity has increased sharply, as evidenced by AI deal value reaching $270 billion in 2025, driven by late-stage infrastructure and platform leaders. Regionally, North America and Europe continue to deepen AI penetration within their venture ecosystems, while Asia’s relative share has stagnated, highlighting divergence in capital formation rather than innovation capacity. Emerging markets, particularly Latin America and the rest of the world, are seeing rapid percentage gains, albeit from a smaller base, suggesting AI diffusion is accelerating globally.

Global AI & ML VC deal activity and share of all VC deal activity

Extreme Capital Concentration at the Top

Investment in 2025 was characterized by unprecedented capital concentration among a small number of private market leaders.

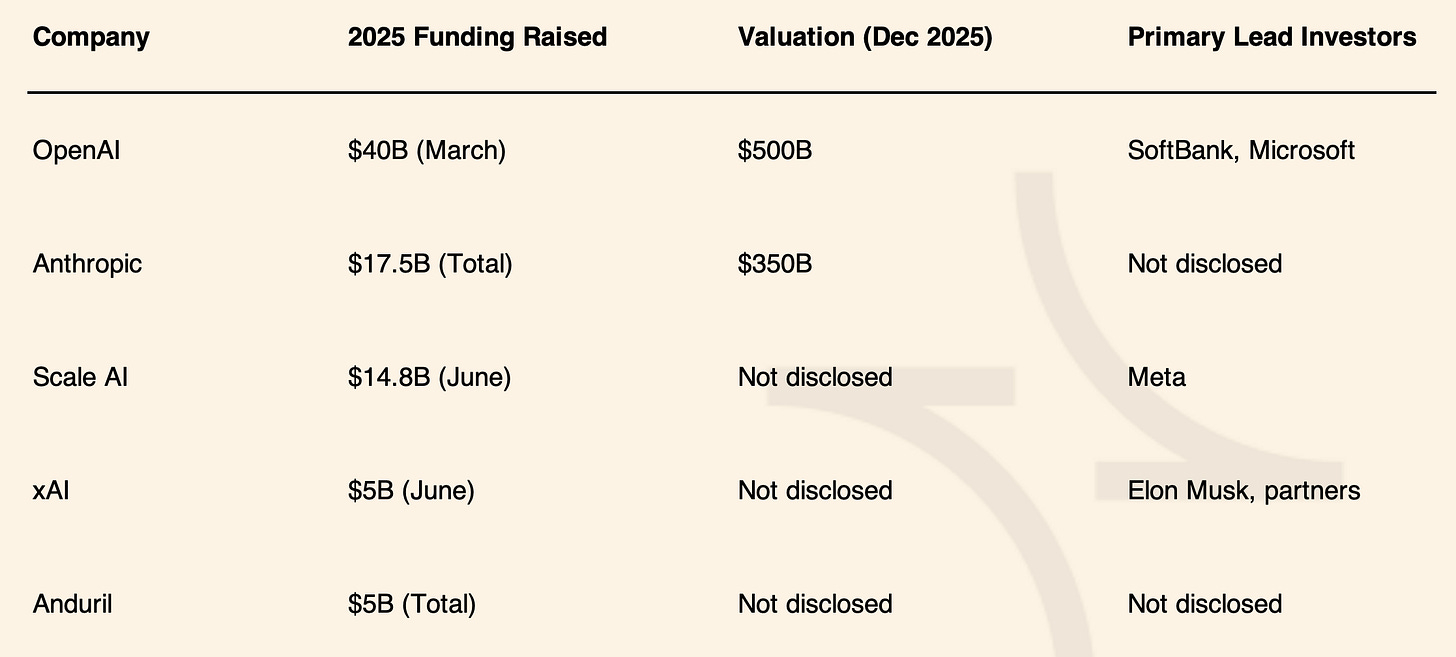

Five firms OpenAI, Scale AI, Anthropic, Project Prometheus, and xAI collectively raised $84 billion, representing 20% of total global venture funding for the year.

OpenAI set a historic benchmark in March 2025 with a $40 billion round, valuing the company at $500 billion. Anthropic followed with successive raises throughout the year, totaling $17.5 billion.

This capital surge was largely driven by what became known as the “Great GPU Rush.” Major technology firms aggressively invested in AI capacity and strategic equity stakes.

- Amazon, Meta, Nvidia, Google, and Microsoft invested over $90 billion in AI startups during the first half of 2025.

- Nvidia emerged as a strategic capital allocator, deploying $27.7 billion across the year.

- Meta returned to active investing after a four-year pause, committing $14 billion to Scale AI.

Market Dynamics

After a two-year freeze, public markets reopened in late 2025.

- 62 IPOs generated $119.4 billion in exit value.

- Health Tech 2.0 stocks rose 18% during the year, broadly tracking gains in the NASDAQ and S&P 500.

- The reopening provided long-awaited liquidity for late-stage investors and reaffirmed public market appetite for scaled AI-adjacent businesses.

Conclusion

The reopening of public markets in late 2025 provided long-awaited liquidity and validated the investment thesis behind scaled, compute-intensive AI platforms. Yet beneath this renewed exit activity, the structure of AI venture capital has shifted decisively. The widening gap between AI’s share of deal value and deal count underscores extreme concentration at the top of the market. In effect, AI venture capital has entered a consolidation phase, where scale, compute access, and capital durability matter more than experimentation. For investors, AI is no longer a cyclical bet, but the primary lens through which venture portfolios are constructed.

Sources:

Cover Artwork

A Ship on the High Seas Caught by a Squall, Known as ‘The Gust’

Willem van de Velde (II), c. 1680

A study in capital under pressure: sudden volatility, structural fragility, and the difference between vessels built to endure and those swept aside by regime change.

Risk Disclaimer:

insights4.vc and its newsletter provide research and information for educational purposes only and should not be taken as any form of professional advice. We do not advocate for any investment actions, including buying, selling, or holding digital assets.

The content reflects only the writer’s views and not financial advice. Please conduct your own due diligence before engaging with cryptocurrencies, DeFi, NFTs, Web 3 or related technologies, as they carry high risks and values can fluctuate significantly.

Note: This research paper is not sponsored by any of the mentioned companies.