Before premium finance became a metal rectangle in a wallet, elite access was organised through doors, lists, vouchers and introductions. Price alone was rarely enough. The deeper question was who could be admitted, who would vouch for them, and whether their presence would improve or dilute the room. Almack’s, London’s private clubs and later private-banking circles all operated on the same principle: admission was a form of underwriting.

That logic matters because the premium card was never only a payment instrument. The Black Card archetype made status portable. It compressed recognition, service, travel utility, merchant trust and problem-solving capacity into an object that could move with the customer. The card was visible, but the real product was the membership architecture behind it.

Today, that architecture is becoming more important than the object itself. Premium finance is no longer defined only by rewards, metal cards or annual fees. Beneath the surface sit service layers, travel access, partner networks, credit structures, reputation signals and increasingly invisible financial infrastructure. Visa Infinite, World Elite Mastercard and American Express’s own “Membership Model” all point in the same direction: the premium product is not just the card, but the network around it.

This paper examines that shift through the lens of admission as underwriting: the idea that premium networks preserve value by controlling who enters, how they enter and what their participation adds to the system. It moves from Almack’s and private members’ clubs to watchmaker collector families, luxury’s shift from product to utility, premium-card economics and the failure of token-gated access.

Moto appears as the modern case study of this broader transition. Not as another card product, and not as a crypto-card narrative, but as an early example of a private financial layer built around access, secured credit, referrals, travel utility, partner benefits, 0 FX and invisible stablecoin-aware infrastructure. The central question is not whether the next premium card can look more exclusive. It is whether it can rebuild the trusted network behind the card.

Partner Highlight

The Black Card Was Never Just a Card

American Express’s own 2025 annual report effectively describes a membership machine disguised as a payments company. In 2025 it generated $9.993 billion of net card fee revenue, up from $8.449 billion in 2024, and it reported 30 consecutive quarters of double-digit net card fee revenue growth. Amex added 12.5 million new proprietary cards in 2025, with more than 70 percent of new accounts acquired on fee-paying products. Millennial and Gen Z customers represented about 65 percent of new consumer account acquisitions globally, about 75 percent of new U.S. Consumer Gold and Platinum acquisitions, and the average age of new U.S. Consumer Platinum and Gold customers in 2025 was 33 and 29 respectively. Amex explicitly says that annual fees help support the value offered on those products and that spend, lending and fee revenue allow it to invest in its “Membership Model.”

This is not semantics. It is business model design. Annual fees are subscription-like revenue. They allow a premium issuer to spend ahead of usage, to refresh benefits, to buy perception and to keep the member relationship economically meaningful even when interchange is commoditised. Amex’s annual report also makes clear that partnerships are not decorative extras. It highlighted “over 20 leading brands” with whom it co-created benefits for the September 2025 Platinum refresh. That refresh, reported by Reuters and detailed by Amex, raised the Platinum annual fee to $895 and promoted more than $3,500 in annual value through credits and benefits. The important point is not the absolute number. It is the engineering principle: recurring fee revenue funds the club, partner benefits widen perceived surplus, and member usage deepens attachment.

The same logic now reaches beyond Amex. JPMorgan raised the Chase Sapphire Reserve annual fee to $795 while adding a larger credit stack tied to travel, hotels, dining, entertainment and subscriptions; Chase’s own materials frame the product around more than $1,500 in annual travel value, more than $1,500 in annual lifestyle value, no foreign transaction fees, premium lounges and a travel designer service. Visa Infinite packages trip-delay cover, emergency medical and dental reimbursement, emergency evacuation and hotel theft protection. Mastercard World Elite packages forty-five-plus destination experiences, 24/7 concierge, zero-liability protection and global emergency services. Atlas, an invite-only charge card, openly markets the same private-club operating system in another language: exclusive dining reservations, curated luxury hotels, concierge text fulfilment, event tickets, private air links, wellness access and no pre-set spending limits. Premium cards are no longer simple payment credentials with rewards attached. They are portable private clubs with a settlement rail underneath.

This is the immediate relevance of emerging products such as Moto. The question is not whether a new card looks premium, weighs more, or offers a richer rewards grid. The question is whether it can rebuild the membership layer around trust, access, credit structure, service quality and infrastructure.

Admission as Underwriting

If the premium card is a modern form of portable recognition, then older elite institutions help explain what the card is actually recognising. The Black Card did not invent financial status. It translated an older access system into a payment object. Long before issuers spoke about premium portfolios, closed-loop data or fee-paying cardmembers, elite societies had already developed a more primitive but powerful technology: admission. The point was not only to identify who could pay. It was to decide who should be allowed inside, who could be trusted once inside, and what their presence would do to the quality of the room.

Almack’s Assembly Rooms - Photograph by Look and Learn, Peter Jackson Collection/Bridgeman Images

Almack’s remains the cleanest historical analogy because it reveals admission stripped down to its social core. A surviving Almack’s voucher from 1816 to 1817 sits in the Huntington Library’s collections, a small document whose material form is almost comically modest relative to the social power it represented. The voucher was not a mass-market ticket. It was a credential of acceptance into one of Regency London’s most selective social environments. Historical accounts of Almack’s make clear that entry depended on vouchers associated with the authority of the patronesses, which meant that the true product was not the ballroom, the supper or the dance. It was being admitted by the people who controlled the social list.

That is why the Almack’s voucher should be read less as a ticket and more as a social credit instrument. It certified that someone with standing had already made a judgement. In modern language, it bundled identity verification, reputational screening and social suitability into one object. It did not ask only whether the applicant had money. It asked whether the applicant fit the room. That distinction is the foundation of this paper’s central concept: admission as underwriting.

Admission is often misread as mere exclusivity. In stronger systems, it is more practical than that. It is a way of reducing uncertainty where price alone is a weak filter. A ballroom, a private club, a family-office network or a premium financial product can all be damaged by the wrong participant, even when that participant is wealthy. The institution therefore needs a proxy for future behavior. In the old language, those proxies were patronage, nomination, reputation, manners, address and existing relationships. In modern finance, the proxies become liquidity, spend behavior, compliance posture, referral source, partner relevance, travel frequency, service expectations and observed conduct over time.

London clubland turned that logic from a social ritual into a durable institutional form. Debrett’s history of private members’ clubs shows that different clubs did not simply sell hospitality to people who could afford it. They sorted by identity, worldview and affiliation. White’s was associated with Tories, Brooks’s with Whigs, Boodle’s with the country set, the Carlton Club with Conservatives, the Reform Club with Liberals, the Travellers Club with globe-trotting gentlemen, and the Athenaeum with men of science, literature and art. The room was valuable because it was filtered. Membership did not merely grant access to a building. It placed the member into a legible network.

That structure still exists in modern club form. Soho House’s own rules state that its Membership Committee meets quarterly and makes the final decision on who becomes a member. That is a revealing detail because it shows that even in a globalised, app-enabled membership business, the committee has not disappeared. The interface has changed, but the logic remains recognisable. A committee preserves the meaning of the door by deciding who can enter and, by implication, who should wait.

The committee is therefore not bureaucracy. It is the institution’s underwriting desk for social fit. It protects the room from becoming a marketplace where price alone determines entry. This is the hidden economic function of many premium membership systems. A club may sell dining, events, workspace, travel reciprocity or status, but the deeper asset is the quality of the people inside. If the committee admits too loosely, the room loses signal. If it admits too narrowly, the network lacks density. The art is not exclusion for its own sake. The art is selective expansion without dilution.

Private banking is the financial version of the same principle. At the upper end, wealth management is not only portfolio construction, lending or tax-aware structuring. It is access, discretion, human coverage and trusted adjacency. J.P. Morgan Private Bank’s public materials use the phrase “unlock exceptional access” and describe exclusive experiences attended by distinguished peers who share clients’ interests and goals. That language matters. It shows that the bank is not only selling a balance-sheet service. It is selling entry into a curated environment where capital, reputation and introductions can interact.

Family offices sit even deeper inside this logic. UBS’s Global Family Office Report describes the 2025 survey as covering more than 300 single family offices across seven regions and over 30 markets, representing families with an average net worth of USD 2.7 billion and USD 651 billion of wealth. That scale makes family offices economically significant, but their role is not only capital allocation. They are private governance systems for wealth, succession, access, risk, reputation and intergenerational continuity. At that level, who is introduced to whom, which managers are shown a deal, which co-investors are trusted and which advisers are allowed near the family become part of the wealth architecture itself.

The family-office world is especially relevant because it demonstrates that ultra-high-net-worth finance is rarely purely transactional. A family office can evaluate managers, funds, founders, co-investors and advisers with a lens that goes beyond nominal return. Trust, discretion, time horizon, values, governance fit and reputational safety all matter. The system is financial, but the filter is partly social. This is the same pattern repeated across clubs, elite schools and private banks: the more valuable the network, the more carefully it must underwrite admission.

The distinction can be stated simply. Traditional underwriting asks whether someone can repay. Membership underwriting asks whether someone improves the room. Traditional underwriting is designed to minimise credit loss. Membership underwriting is designed to preserve trust density. The best premium systems often need both. A private bank wants assets, but it also wants the right client. A university wants excellence, but it also wants the right cohort. A club wants dues, but it also wants a room that still feels worth joining. A premium financial product wants spend and deposits, but it also wants members whose behavior increases the value of the network.

This framework also clarifies why referrals matter. In mass-market fintech, referrals are usually discussed as customer-acquisition mechanics. They lower CAC, increase virality and push users through the funnel. In premium networks, referrals can perform a different function. They externalise part of the admission process to people already inside the system. A referral says that an existing participant is willing to attach some reputation to the next entrant. It does not replace formal underwriting, but it adds a social signal that pure application data cannot easily capture.

A well-designed referral system is therefore closer to a nomination committee with a user interface than to a discount code. The inviting member is not just generating a lead. They are helping define the room. This is why referrals become strategically powerful in premium finance only when they remain scarce enough to mean something. If every invite is unlimited, the referral loses signal. If every member can bring anyone, the room becomes self-diluting. But if referral rights are constrained, observed and tied to member quality, they can become a form of distributed underwriting.

Why the Private Club Returns

The return of the private room is not simply a story about elitism. It is a response to the degradation of signal in the public square. Edelman’s 2026 Trust Barometer found that seven in ten people globally exhibit an “insular” trust mindset, meaning they are unwilling or hesitant to trust people who differ from them in values, facts, problem-solving approaches or cultural background. McKinsey’s 2025 consumer research adds a behavioral layer: consumers have gained free time since 2019, but allocate almost 90 per cent of that additional time to solo activities. Eventbrite’s 2025 “Fourth Spaces” research then captures the counter-movement: 84 per cent of interest-based event attendees say they have formed close friendships through these gatherings, 45 per cent cite belonging and identity as key reasons for joining communities, and 73 per cent of 18 to 35 year-olds plan to attend live events in the next six months. The public internet has grown noisier; people are paying up, or queueing up, for smaller rooms with better filters.

Accenture’s official Life Trends work offers a complementary concept: “social rewilding”. In its 2025 materials, the firm argues that people are looking to restore meaningful real-world interactions and healthier relationships with technology. That framing matters because it explains private-club demand as a reaction to saturation, not just as a performance of status. The private room is valuable because it feels more human, more legible and more governable. In a world of algorithmic feeds, AI-generated sameness and collapsing trust, curation itself becomes a premium good.

The data from clubs supports the point. GGA Partners’ 2024 Club Leaders’ Perspectives report found that membership demand remained strong across the industry even as post-pandemic surges moderated. Forty per cent of respondents still reported an increase in member numbers, 34 per cent said they had a waiting list that increased during the year, 49 per cent said their club was at capacity, average initiation fees reached roughly $58,000, and average annual dues were around $10,700. In the same report, initiation fees were expected to rise another 8.7 per cent and operating dues another 6.2 per cent. Scarcity, when paired with functioning demand, remains a pricing power engine.

The modern club market is not one category. Soho House and NeueHouse represent creative and work-social clubs; Casa Cipriani and Maison Estelle are hospitality-led clubs; Zero Bond and Annabel’s operate closer to nightlife and status; The Arts Club and Core sit near wealth, culture and power; Aman Club points toward ultra-luxury travel membership. Each model has different aesthetics, but the same underlying function: creating a filtered room whose value depends on who enters.

This is where premium finance begins to mirror club strategy. A financial membership product does not only need more users; it needs the right users, behaving in ways that increase the value of the network for other members and for partners. If growth degrades the signal, the premium collapses. This is why referral-led access in a product such as Moto should not be dismissed as a growth hack. Properly designed, it is a mechanism for selective expansion, the financial equivalent of letting the room grow without making the room ordinary.

The Door Must Still Mean Something

The return of private clubs creates a paradox. The stronger the demand for admission, the greater the temptation to expand. But the more a club expands, the more carefully it has to protect the meaning of the door. A private club rarely fails because nobody wants in. More often, it runs into trouble when too many people want in, too quickly, and the admission signal begins to weaken.

Soho House is the clearest modern case because it proves both sides of the equation. On the one hand, demand has been real. The company reported $418.0 million of membership revenue in 2024, up 17.2 percent year over year, and said it operated 45 Houses by the end of the year. In Q3 2024, it reported 267,494 total members, 208,078 Soho House members and a membership waitlist of approximately 111,000, which it described as remaining at record levels. That is the economics of successful membership: recurring revenue, high demand, waitlists and global reciprocity.

On the other hand, Soho House also shows how quickly growth can become congestion. In December 2023, the company stopped accepting new members in London, New York and Los Angeles after complaints about overcrowding and declining service quality. Founder Nick Jones told members that the company was focused on improving service and making sure Houses did not feel too busy, adding that it would only accept members in locations where there was capacity. That is the key operational lesson: when a membership product becomes too available, the room may still be full, but the membership can become less valuable.

This is not simply an issue of atmosphere. It is an issue of network economics. A club’s value depends on density, but density has a limit. Up to a point, more members can make the network more useful: more events, more connections, more revenue, more locations, more partner opportunities. Beyond that point, the same growth can damage the product: harder reservations, weaker service, crowded spaces, less recognition, lower signal quality and a feeling that admission no longer means much. The network grows, but the premium can shrink.

That is the exclusivity paradox. Scarcity cannot be only theatrical. It has to be operational. A waiting list is valuable only if it protects the experience inside. A committee is valuable only if it improves the member base. A referral is valuable only if it preserves trust. A high price is valuable only if it corresponds to better access, better service or better density. Otherwise, the language of exclusivity becomes a costume for ordinary capacity management.

For premium finance, this lesson matters directly. A card product can scale faster than a physical club because the interface is digital and the payment network is global. But the membership layer cannot scale infinitely without consequence. If a premium financial product promises access, concierge, partner benefits, travel utility and recognition, the constraint is not only technology. It is service quality, partner capacity, underwriting discipline and the quality of the members themselves. Too much openness can dilute the very signal the product is trying to monetise.

This is why admission architecture matters. The best premium networks do not simply maximise sign-ups. They manage capacity, sequence, member quality and service intensity. They know that growth has to be paced against the ability of the network to deliver. In a club, that means the room must not feel overcrowded. In high horology, it means allocation must not become arbitrary. In private banking, it means the relationship cannot feel automated. In premium finance, it means the card cannot promise private access while behaving like a mass-market funnel.

The Soho House lesson is therefore not that scale is bad. Scale can create better economics, better programming, more locations and more partner leverage. The lesson is that scale must not destroy the filter. Once the door stops meaning something, the product loses the very asset that made people wait outside it. That principle becomes the bridge into luxury allocation: the most durable premium brands do not only create demand. They decide how much demand they are willing to satisfy, through whom, and on what terms.

From Allocation to Utility Luxury

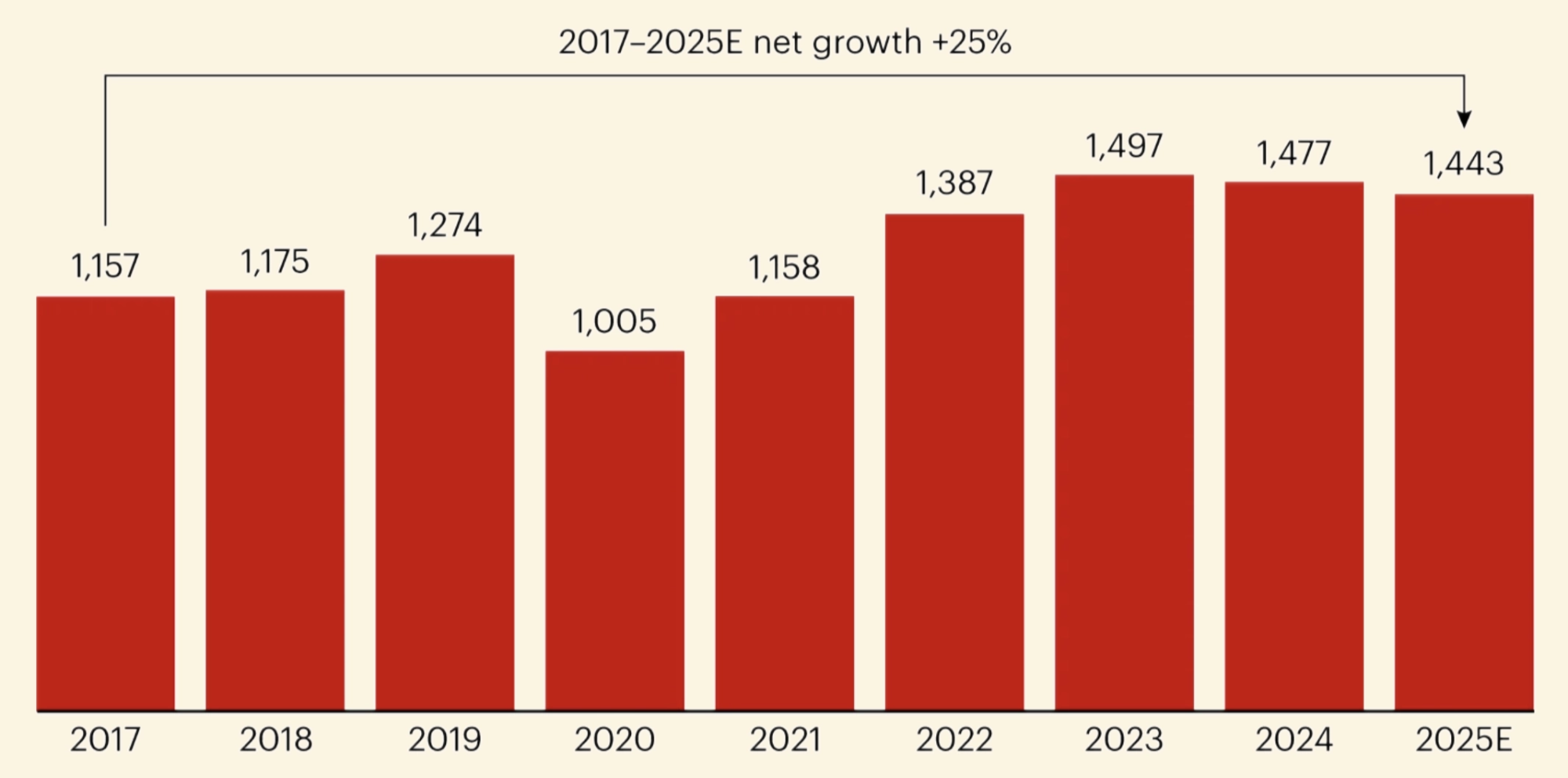

Luxury’s centre of gravity has shifted. The old growth model depended on a broadening funnel: more aspirational consumers, more entry-level products, more global boutiques, more price elevation, more brand heat. That model is now under pressure. Bain and Altagamma estimate that overall luxury spending reached roughly €1.44 trillion in 2025, broadly stabilising after the post-Covid boom, but the structure underneath changed materially.

Worldwide luxury spending (EUR Billions)

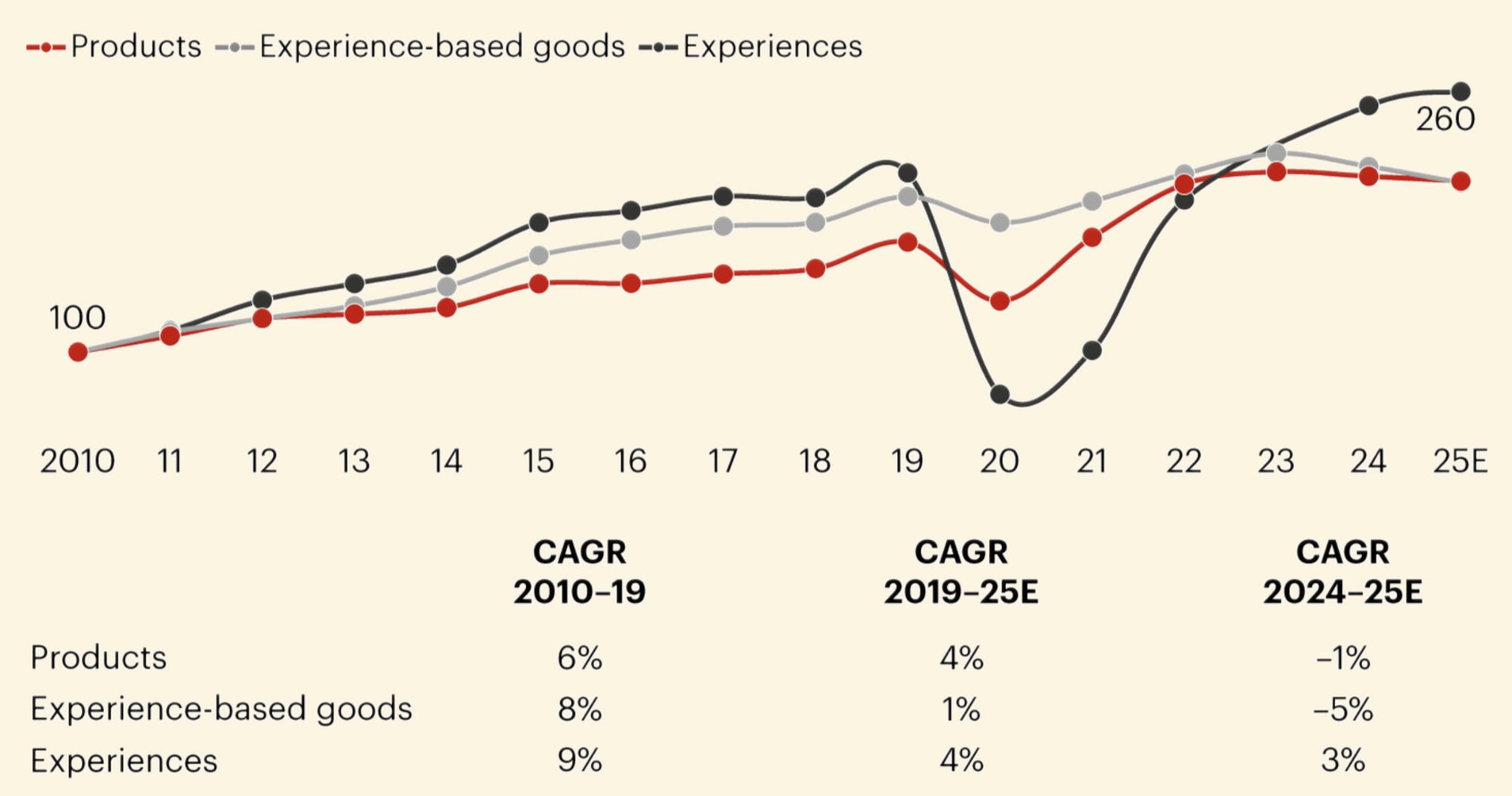

Luxury experiences continued to outpace the broader market, driven by wellness, social connection and self-reward, while personal luxury goods were expected to total about €358 billion, a mild erosion from 2024. Bain also notes that the luxury consumer base kept contracting, with the sector losing about 20 million consumers in 2025 alone.

Growth of global luxury spending by segment

Reuters’ coverage of the same Bain-Altagamma work sharpened the implication: the global luxury client base fell from around 400 million in 2022 to about 340 million in 2025, while top buyers now account for roughly 46 to 47 per cent of the €358 billion personal luxury goods market. That is a very different luxury market from the one that emerged after the pandemic. The issue is no longer only demand. It is trust, value perception and client concentration. Bain warned that years of aggressive price increases have alienated aspirational buyers and even left some ultra-wealthy clients feeling “betrayed” when price elevation was not matched by creativity, craft or service.

The strategic implication is clear. The next luxury cycle is not about signing up ever more marginal buyers. It is about extracting deeper value from fewer, better, more durable relationships. BCG makes the same point from the client side: brands most exposed to aspirational consumers have been hit hardest, while those that stayed close to top-tier clients have been more resilient. BCG estimates that top-tier luxury clients spend around €360,000 annually on luxury, rising to roughly €500,000 when cars and wellness or longevity are included, and that the broader HNWI base behind these clients held about €68 trillion in financial wealth in 2024. These clients do not want more generic outreach. BCG’s research says 65 per cent feel overwhelmed by brand over-communication and lack of personalisation. What they value is connection, intimacy, excellence and recognition.

That is the context in which allocation becomes more important than ordinary sale. In mass luxury, the question is whether the buyer can pay. In true high luxury, the more revealing question is whether the maison wants to allocate the product to that buyer. Once scarcity becomes strong enough, access itself becomes the prestige layer. The object matters, but the right to receive the object matters too. Allocation is status.

The watch world supplies the clearest version of that logic because high horology has long understood that scarcity is not simply an inventory condition. It is a relationship system. The finest watchmakers do not merely sell timepieces. They manage mythology, production discipline, retail control, collector behavior, secondary-market perception and long-term client quality. The buyer is not only purchasing a product. They are entering a stewardship relationship with the brand’s scarcity.

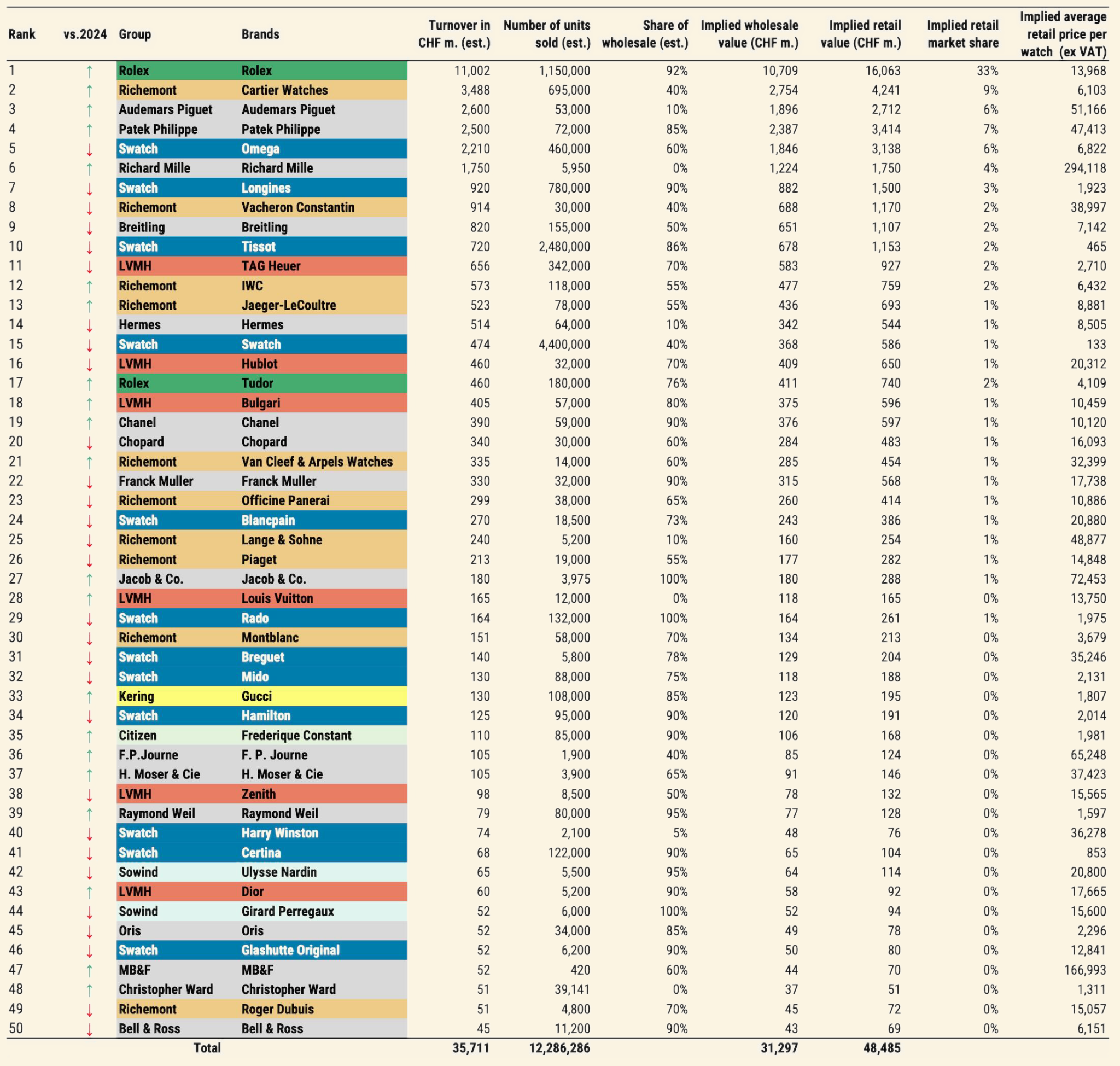

Patek Philippe is the institutional example. In May 2026, the Financial Times reported that president Thierry Stern continues to hold production around 75,000 watches annually and has reduced the brand’s retail footprint from 500 outlets in 2009 to 259, while maintaining only four exclusive salons. Morgan Stanley estimated Patek Philippe’s revenue rose 25 per cent over two years to CHF 2.5 billion in 2025. Stern’s approach is not aggressive expansion. It is selective control: limited production, disciplined distribution and a retail footprint designed to protect quality over volume.

This is not conservatism for its own sake. It is network control. By limiting output and tightening distribution, Patek protects the social meaning of ownership. The maison reduces the risk that the product becomes merely available to whoever can pay the highest immediate price. The retail network itself becomes an allocation mechanism, and the allocation mechanism preserves myth. In that sense, scarcity is not only produced inside the manufacture. It is produced through the relationship between production, retail, authorised dealers, client history and the long memory of the collector market.

Audemars Piguet demonstrates the spatial evolution of the same logic. AP House is not a standard boutique. Audemars Piguet describes AP House as a timeless space created with some of the manufacture’s most loyal clients, imagining how Jules Louis Audemars and Edward Auguste Piguet would deal with clients if they were alive in the 21st century. The result, in the brand’s own language, is a space where the comfort of home and the warmth of friendship take priority. That phrasing matters. It reframes luxury retail away from throughput and toward private hospitality.

The Financial Times has described the broader industry shift in similar terms: watchmakers are moving away from street-level stores toward more exclusive, off-street spaces where privacy, hospitality and deeper client knowledge become part of the sales model. The article cites AP House as the starting point for a wider movement that now includes brands such as Vacheron Constantin, A. Lange & Söhne and Richard Mille-style hospitality environments. The commercial insight is straightforward: relationship architecture can be more valuable than square-foot retail.

Greubel Forsey shows the collector-family end state. Its official “Family” programme is explicitly not public, promoted or advertised. The language is precise: collectors are described as more than clients, and the programme is positioned as a private, invitation-based circle with direct communication, exclusive content, private previews and private encounters. Greubel Forsey’s broader brand language is equally revealing: each timepiece is “entrusted” to a collector who understands what it carries. This is not loyalty marketing in the ordinary sense. It is a controlled expansion of the room around the collector.

This is why anti-flipping culture sits so close to allocation culture. At the top end, maisons do not simply want transactions. They want holders who protect the house story, reappear over time, attend private events, absorb allocation norms and reinforce the long-term desirability of the brand. A flipper treats allocation as arbitrage. A collector treats allocation as relationship. The brand’s task is to distinguish one from the other before the product leaves the house.

The broader Swiss watch market reinforces the same polarisation. Coverage of the 2026 Morgan Stanley and LuxeConsult Swiss watch report noted that the largest privately owned brands, including Rolex, Patek Philippe, Audemars Piguet and Richard Mille, continue to dominate the profit pool and are pulling away from weaker players. One summary of the report estimates that the top four privately owned brands capture about 76 per cent of the profit pool, with an aggregate operating margin around 33 per cent. The exact percentages matter less than the direction: the strongest houses can use profitability to buy more control, more selective distribution, more direct clienteling and more patience.

That is the deeper luxury lesson. Control compounds. Brands that control production, retail, client relationships, service quality and allocation can preserve pricing power even when the wider market slows. Brands that rely too much on volume, price increases and aspirational churn become vulnerable when consumers begin questioning value. The market therefore moves in two directions at once: the broad luxury base becomes more fragile, while the best-controlled houses become more powerful because their scarcity feels earned rather than manufactured.

Bain’s data points in that direction. Experiences are gaining ground over product ownership, driven by wellness, social connection and rewarding oneself. But the word “experience” is too soft if treated only as mood. The stronger concept is operational utility. A luxury hotel is not only a beautiful room. It is recognition at check-in, a problem solved before it becomes visible, a reservation secured, a transfer arranged, a late checkout granted, a concierge who knows which request matters and which can be ignored. The value sits not only in beauty, but in the conversion of money into time, certainty and access.

Premium Finance Beyond the Card

The shift from product luxury to utility luxury has a clear financial equivalent. Premium finance is also moving away from the visible object and toward the operating system around it. The card still matters, but increasingly as an interface. The deeper product is the recurring access bundle: service, travel, protection, partner benefits, concierge, identity, global acceptance, 0 FX utility, credit structure and the confidence that someone will solve the problem when ordinary financial infrastructure fails.

American Express is the clearest incumbent example. It no longer behaves like a simple card issuer. It behaves like a membership platform. In its 2025 annual report, American Express said net card fee revenues reached a record $10 billion and grew double digits for the 30th consecutive quarter. That number matters because it shows how central annual-fee economics have become to premium finance. The annual fee is not just a charge. It is recurring membership revenue that funds benefits, service layers, partner credits, retention and the perception that the product deserves renewal each year.

The Platinum refresh made that model visible. American Express raised the U.S. Platinum annual fee from $695 to $895 and promoted more than $3,500 in annual value through travel, dining, hotel, retail and lifestyle credits. Chase moved in the same direction with Sapphire Reserve, lifting the annual fee to $795 while expanding the product around travel credits, hotel access, lounge benefits, dining, entertainment and no foreign transaction fees. The point is not whether every customer captures the full stated value. The point is that premium cards are being priced and packaged like access memberships, not ordinary payment tools.

That model works because premium-card value is not only about points. Annual fees stabilise revenue. Partner credits increase perceived value. Lounge access turns airport friction into habit. Hotel benefits create recognition away from home. Dining access embeds the product into urban life. Concierge and emergency assistance become trust products when travel, reservations, payments or cards fail. 0 FX matters disproportionately to globally mobile users. The more a card becomes embedded in travel, hospitality and service recovery, the less it behaves like a commodity payment instrument.

This is why premium finance increasingly resembles private banking. At the top end, financial products have never been only about yield, lending or portfolio construction. They are also about access, discretion, introductions, human coverage and the ability to solve problems adjacent to the balance sheet. J.P. Morgan Private Bank’s language around “exceptional access” captures this clearly. In high-end finance, access is not decoration. It is part of the relationship.

Newer premium-card products point in the same direction. Atlas, for example, presents itself as an invite-only charge card built around dining, travel, concierge and premium experiences. Whether every benefit proves durable is a separate question. The signal is category-level: new entrants are not trying to win only through rewards. They are presenting the card as an access interface for a high-spend lifestyle.

Premium finance is therefore becoming a travel, service and access operating system with credit attached. For affluent users, travel is not only leisure. It is a behavioral map of wealth, mobility and network density. It reveals where the user spends, how often they cross borders, what hotels and restaurants matter, how often service recovery is needed, how much FX friction exists and whether partner access has real utility. A premium product that understands the travel graph can become more valuable than one that simply pays back points after a transaction.

This also explains why many NFT-gated membership experiments failed to create durable trust. The issue was not that access is a bad idea. The issue was that many projects built around tradable access, scarcity theatre and speculative upside before they had earned cultural, operational or service legitimacy. In some cases, the product looked less like a membership institution and more like a fundraising wrapper with a private-club narrative attached.

The problem was sequence. NFT-gated clubs financialized the access layer before proving the operating layer, cultural layer and trust layer. Membership became liquid before it became meaningful. A traditional private club uses admission to filter people before privileges accrue. A speculative token-gated club risks doing the opposite: it lets the market allocate access before the institution has shown that the room is worth entering.

The distinction is fundamental. Tradable access is not trusted access. A transferable token can prove ownership. It cannot prove that someone improves the room. It cannot establish discretion, behavior, partner relevance, service expectations, long-term fit or network quality. When the credential becomes speculative, it may attract precisely the behavior that premium systems are supposed to filter out: floor-price obsession, resale incentives and status arbitrage.

Stablecoins are different because they matter most when they disappear into the product. Visa’s disclosures show the direction. In its 2025 annual report, Visa said stablecoin settlement volume had surpassed a $2.5 billion annualised run rate by September 2025. By April 2026, Visa said its stablecoin settlement pilot had reached a $7 billion annualised run rate after expanding across nine blockchains. Circle’s Q1 2026 results showed USDC circulation at $77.0 billion and USDC onchain transaction volume at $21.5 trillion for the quarter.

The user-facing lesson is simple: stablecoins are not the brand. They are a possible infrastructure layer. The customer does not want a “stablecoin card” as an identity category. They want faster settlement, lower FX friction, more flexible collateral, stronger cross-border funding and a smoother premium-credit experience. This is not a stablecoin adoption story. It is a premium-finance infrastructure story.

That distinction separates durable innovation from crypto-native novelty. A product can use stablecoin infrastructure without asking the customer to buy a crypto narrative. It can be self-custody-aware without making wallets the marketing headline. It can improve collateral mobility without becoming a DeFi dashboard. In premium finance, the strongest infrastructure is often the infrastructure the member never has to see.

A Case Study of Moto: The Private Financial Layer

Shimon Newman’s vision as CEO of Moto is best understood not as another card launch but as an attempt to build a private financial membership layer for globally mobile, digital-asset-aware wealth. The important point is not that it uses newer financial infrastructure. The important point is that it is trying to combine several elements that used to live separately: premium access, credit, self-custody-aware infrastructure, travel utility, partner benefits and membership discipline.

That makes Moto more interesting as a case study in the broader shift described in this paper than as a standalone product announcement. The old premium-card model made the card the visible sign of a deeper institutional relationship. Moto is attempting something similar, but for a different kind of member: one whose capital, spending, mobility and identity are increasingly distributed across traditional finance, digital assets, private networks and global travel.

The starting point is to say what Moto is not. It is not best understood as a mass-market fintech card. It should not be framed primarily as a crypto card, DeFi card, stablecoin card or rewards gimmick. Those descriptions overemphasise the rail and underexplain the room. They place Moto inside categories associated with commodity card issuance, short-cycle crypto novelty or points arbitrage. The more useful comparison set is closer to premium Amex logic, Atlas-style membership architecture and aspects of private-bank curation. In that frame, the card is not the product. The product is the access layer, the trust layer, the travel layer, the member network and the financial infrastructure working underneath.

Moto’s own positioning points in that direction. The company describes itself less as a mass-market fintech product and more as a private access product built around trust, spending behavior and reputation. That matters because in premium markets, scarcity alone is no longer enough. The deeper premium is admission: who gets access, who introduces them, what network forms around the product and whether the room becomes more valuable as the right members enter. That is why Moto belongs in the same cultural conversation as private clubs, watchmaker collector circles and invitation-led luxury ecosystems, even though the product itself is financial.

The product logic begins with secured credit. Moto should not be treated as a debit product, because the user experience is designed around spending first and being debited at the end of the month. That distinction matters. A debit product is immediate and transactional. A secured credit experience creates a different relationship between assets, spending and trust. It lets Moto sit closer to the premium-credit category while building on a more modern infrastructure base. The customer-facing story is therefore not “spend crypto.” It is premium financial membership: access, credit, travel, partner benefits and global spend, with infrastructure doing its work in the background.

That is why Moto’s application and access flow are not minor product details. In mass-market fintech, the ideal funnel removes as much friction as possible. In premium finance, some friction can be beneficial because it helps protect the quality of the member base. Moto’s invite-led approach, member screening and emphasis on spending behavior suggest a product that is not trying to open access broadly all at once. The next phase of referrals fits the same logic. It is not merely a growth feature. It is part of the product's cultural architecture.

In ordinary consumer fintech, referrals lower acquisition cost. In premium finance, referrals protect network quality. The right member introduces the right member. A referral becomes a form of delegated judgment, closer to a club nomination than a discount code. This is why Moto’s upcoming referral rollout should be interpreted through the same historical lens as Almack’s vouchers, club committees, private-bank introductions and watchmaker allocation lists. Access enters through trust. The member who introduces another member is not only expanding the network. They are lending reputation to the network.

This is also where Moto’s strategy differs from the failed token-gated access models of the previous crypto cycle. The lesson from NFT membership experiments was not that access is a bad idea. It was that tradable access is not trusted access. Many projects tried to financialise belonging before building trust, service, utility or member density. Moto’s more defensible route is the opposite: preserve the filter, then attach better infrastructure and better utility to the people who pass through it. In that model, admission is not theatre. It is part of the product’s economic design.

Travel is the next crucial layer because it reveals more than leisure preference. For a premium financial product, travel is behavioral information. It shows cross-border spend, need for 0 FX, reliance on hotels and restaurants, preference for service recovery, exposure to events and the density of a member’s real-world network. A globally mobile member does not want a card that only pays rewards. They want a product that moves with them across cities, currencies, hotels, conferences, restaurants, airports and private events.

This is why Moto’s 0 FX fees are more than a simple card benefit. For a high-spend user who travels frequently, spends internationally and expects financial products to work across borders, FX friction is not a small inconvenience. It is a recurring tax on mobility. Removing that friction makes the product more useful in the exact environments where premium members already spend time: travel, hospitality, business events, private meetings and cross-border commerce. In this sense, 0 FX is not a marketing line. It is part of the core utility layer. The newly introduced Moto Travel Portal should be read in the same way. Members receive access to luxury hotels at attractive rates, with 5 percent cashback on bookings. That is not merely another perk in a rewards catalogue. It reinforces the idea that the card is an access layer.

Visa Infinite-level benefits add another layer to this positioning. Lounge access, concierge, exclusive event access, hotel and dining benefits and travel protection are familiar pieces of the premium-card category, but they matter because they signal the kind of use case Moto is trying to serve. These benefits are most valuable for members whose lives are already mobile, event-driven, internationally exposed and service-sensitive. In that context, benefits are not decoration. They become operating tools for a high-friction lifestyle.

The partner network may become the strongest expression of Moto’s membership layer over time. The goal is not simply to attach discounts to a card. The stronger version is a curated set of access points across the places members already move: hotels, restaurants, retail, events, travel and hospitality. This distinction matters. A public marketplace optimises for breadth. A premium membership layer should optimise for relevance. The best partner network is not necessarily the largest. It is the one that gives members better access, better rates, better service and better outcomes in environments where they already want to be recognized.

That is the difference between rewards and membership. Rewards are usually transactional. Membership is relational. Rewards give something back after spending. Membership changes the conditions under which the member moves through the world. A high-quality travel portal, preferred hotel rates, elevated hospitality, selected experiences, concierge and access to private events can all become part of the same layer if they are curated tightly enough. The strategic question is whether Moto can make that layer feel materially different from a standard benefits bundle.

The App Store rollout also matters because it marks a shift from private beta toward a more complete product experience. In premium markets, the app is not merely a distribution channel. It becomes the interface through which the member experiences admission, travel, partner access, spending and service. The risk for many fintech products is that the app becomes a commodity dashboard. For Moto, the opportunity is to make the app feel like the control surface for a private financial layer: card, credit, travel, benefits, partner network and support in one place.

The infrastructure should remain largely invisible. That is one of the most important narrative points. Moto’s relevance does not come from asking members to care about financial rails for their own sake. It comes from using newer infrastructure to make premium finance more flexible, more global and more aligned with how digital-asset-native wealth already behaves. Stablecoin-aware and self-custody-aware infrastructure may improve settlement, collateral flexibility, funding efficiency and cross-border movement, but the member should not need to think in protocol terms every time they book a hotel, enter a restaurant or pay abroad. The front end should feel premium. The back end can be modern.

This separation of layers is essential. The first generation of crypto cards often made the rail the story. That created novelty, but it also trapped the product in a narrow category. Moto’s better narrative is that the rail should disappear into the experience. The member sees credit, access, 0 FX, travel utility, concierge, partner benefits and private membership. The company can use better infrastructure to improve the economics underneath. Stablecoins are not the brand. They are part of the reason the brand may be able to build a different financial stack.

Moto’s opportunity is therefore not to out-Amex Amex on a benefit spreadsheet. Legacy issuers can add credits, lounges, hotel perks and merchant partnerships quickly. The harder task is to redefine the premium unit itself. Moto’s unit is not the card alone. It is the combination of admission, secured credit, spending behavior, travel utility, 0 FX, partner access, referrals, reputation and invisible infrastructure. That is the private financial layer.

This is why Moto matters intellectually even beyond its current stage. It sits at the intersection of several trends that were developing separately and are now beginning to reinforce one another: the return of curated rooms after digital saturation, the luxury shift from product to utility, the importance of allocation over open sale, premium-card subscription economics, the travel-service stack beneath affluent spending and the quiet normalisation of stablecoin-aware infrastructure in the back office of payments.

Moto is not interesting because it is another card. It is interesting because it tests whether old premium social logic can be rebuilt with new financial rails. If the old Black Card made institutional recognition portable, the next generation of premium finance may make admission, travel, credit and infrastructure programmable around a trusted member base. The card remains the interface. The network becomes the product.

The Network Is the New Status Symbol

The premium-finance market is approaching a point where the traditional levers are no longer enough. Rewards are copyable. Metal cards are copyable. Lounge access is increasingly copyable. Dining credits, hotel credits and entertainment bundles can all be imitated with sufficient subsidy. What remains harder to copy is the underlying network: the right members, the right partner graph, the right travel utility, the right service layer, the right credit structure and the right invisible infrastructure that makes the whole system feel easier than the alternatives.

That is why the central thesis holds. The AMEX Black Card was never only a card. It was a portable signal that somebody had already been recognized, prioritised and admitted into a high-value service environment. American Express’s own economics, from $10 billion of net card fees to a Membership Model built around services and experiences, show that the market still rewards products that monetise admission and usage together. The next wave of premium-finance products will compete not just on visible perks, but on how credibly they can rebuild the trust and access layer behind the card.

The history of clubs and collector maisons suggests what the durable version looks like. Doors matter when they improve the room. Allocation matters when it protects the culture. Referrals matter when they act as quality control. Luxury works best when experience is not merely theatrical, but operationally useful. Stablecoins matter when they do not dominate the user narrative, but quietly improve settlement, collateral mobility and cross-border efficiency in the background. Each of these lessons points toward the same conclusion: the future premium product is a membership system with financial primitives attached, not a payment primitive with decorative membership attached.

Moto is relevant because it appears to be building at the level where premium finance becomes membership architecture. Its application flow, invite-code logic, selective language, credit framing, end-of-cycle settlement, collateral controls, concierge layer and premium-travel posture all suggest a product trying to build a private financial room rather than a generic card programme. It is still early, and some structural questions remain open on public evidence alone, but the direction is the important thing. The product is interesting because of the architecture it implies.

The future of premium finance may not look like another bank product. It may look like a private club with a balance sheet, a travel desk, a concierge, a referral graph and invisible financial infrastructure underneath. The card is only the interface. The network is the product.

Partner Highlight

At insights4vc, we pay attention to teams that are not just shipping products, but shaping categories.

Moto is one of them. The company is building a premium card experience positioned as an alternative to traditional incumbents such as Amex, combining a high-end user interface with more modern financial infrastructure.

Moto is currently expanding access to a limited testing group. If you would like to test the product and typically spend more than $5,000 per month, please contact us at: [email protected]

Sources

- Moto, Moto Card, company website.

- Debrett’s, A History of Private Members’ Clubs, Debrett’s.

- American Express Company, 2025 Annual Report, American Express Investor Relations, 2026.

- Chase, The Most Rewarding Cards Are Here: The New Chase Sapphire Reserve and Introducing Chase Sapphire Reserve for Business, JPMorgan Chase, 2025.

- Edelman, 2026 Edelman Trust Barometer, Edelman, 2026.

- Sophie Witts, Soho House to Stop Accepting New London Members to Prevent Overcrowding, The Caterer, 11 December 2023.

- Financial Times, Thierry Stern: “You Don’t Come to Patek Philippe Because It’s More Expensive”, Financial Times, 14 May 2026.

- Greubel Forsey, Family, Greubel Forsey.

- Circle, Circle Reports First Quarter 2026 Results, Circle, 2026.

- Atlas, Atlas Card, company website.

Risk Disclaimer

insights4.vc and its newsletter provide research and information for educational purposes only and should not be taken as any form of professional advice. We do not advocate for any investment actions, including buying, selling, or holding digital assets.

The content reflects only the writer’s views and not financial advice. Please conduct your own due diligence before engaging with digital assets or related technologies, as they carry high risks and values can fluctuate significantly.