Stablecoins are no longer best understood as collateral for crypto trading. By April 2026, the market had reached roughly $317 billion, according to the Federal Reserve, up more than 50% since early 2025. At the same time, the policy conversation has shifted. The core institutions now studying stablecoins are not only crypto market participants, but the International Monetary Fund, the Bank for International Settlements, the European Central Bank, and national central banks. That is an important signal. Stablecoins are increasingly being analysed as payment instruments, reserve-holding entities, Treasury market participants, cross-border settlement tools, and building blocks for tokenised capital markets.

The central tradeoff is not regulation versus innovation. It is a set of linked financial tradeoffs. Safer reserve rules reduce run risk, but compress issuer economics. Banning direct issuer-paid yield may reduce the risk of deposit flight from banks, but it also pushes demand towards wrappers, wallets, exchanges, tokenised funds, and higher-risk yield structures. Dollar stablecoins strengthen demand for U.S. safe assets and extend the reach of the dollar, but they also intensify concerns about monetary sovereignty outside the United States. Faster settlement and always-on liquidity improve certain payment and treasury workflows, but once stablecoins are used at scale they become tightly connected to T-bills, bank deposits, FX conversion, custodians, market makers, payment processors, and tokenised securities markets.

Clear categorisation matters. Payment stablecoins are digital bearer instruments designed to hold par and function as money-like settlement assets, typically backed by cash, bills, repo, deposits, or in some frameworks central bank balances. Yield-bearing stablecoins add an investment return to the instrument, either directly or through wrappers. Tokenised money market funds are fund shares, not payment money, even if they circulate on-chain and maintain a stable NAV profile. Tokenised deposits are digital commercial bank liabilities that preserve the two-tier monetary system and settle through regulated intermediaries. CBDCs are liabilities of the central bank. These are not semantic differences. They determine who bears risk, who earns yield, how convertibility works, and how monetary policy transmits.

The practical implication for institutional readers is straightforward. The safer stablecoins become, the more they look like regulated financial infrastructure. The more attractive they become to users through yield, rewards, programmability, and liquidity, the more they start to compete with bank deposits, money market funds, and sovereign monetary systems. That is why the winning business models are moving beyond simple issuance. They are converging on distribution, orchestration, compliance, settlement, treasury integration, and risk management. Stablecoin issuance is becoming only one layer of a broader stack.

The market has moved past the crypto-native phase

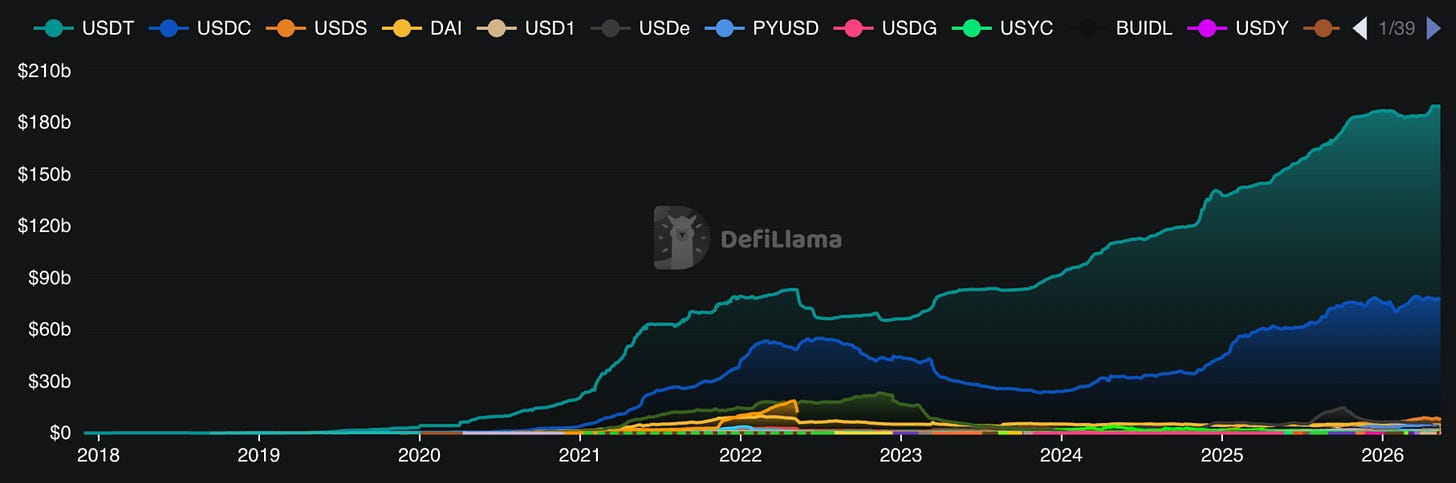

The stablecoin market is now large enough to matter to traditional finance. The Federal Reserve estimated aggregate stablecoin market capitalisation at approximately $317 billion as of 6 April 2026. On 8 May 2026, ECB President Christine Lagarde said that stablecoins had moved from the periphery to the centre of policy debate, growing from less than $10 billion six years earlier to more than $300 billion, while remaining overwhelmingly dollar-denominated. Her speech also noted that almost 90% of the market is controlled by just two issuers: Tether and Circle.

Stablecoin Market Capitalisation; Source: defillama

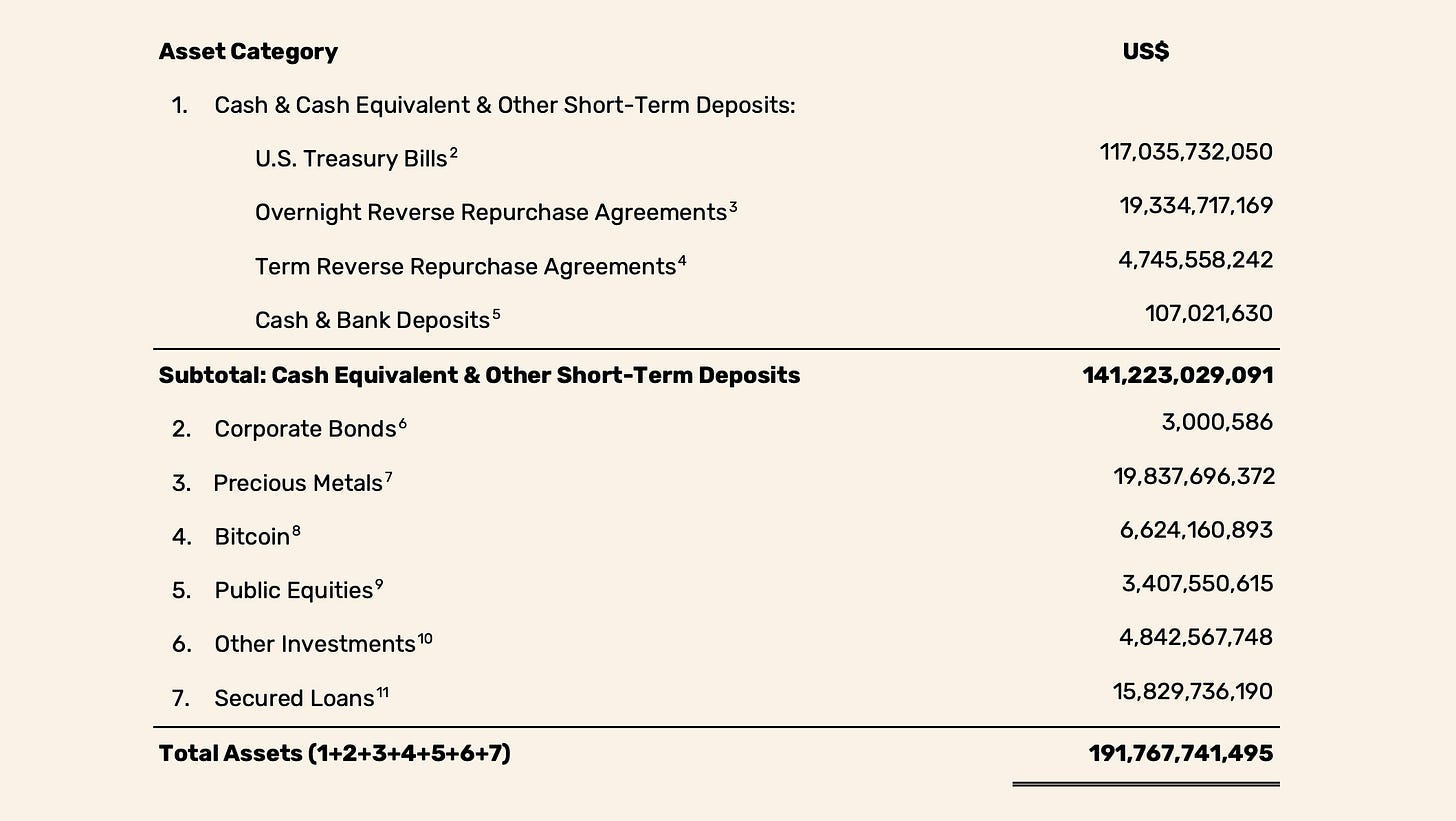

That concentration is not abstract. Tether reported approximately $183.4 billion of token liabilities as of 31 March 2026, around $141 billion of direct and indirect exposure to U.S. Treasury bills, and an $8.23 billion reserve buffer. It also described itself as the world’s 17th-largest holder of U.S. Treasuries. Circle reported $77.0 billion of USDC in circulation at the same quarter end. The largest stablecoin issuers have therefore reached a scale where reserve management, custody, counterparty structure, and regulatory treatment are no longer crypto niche issues. They are becoming questions of financial-market infrastructure.

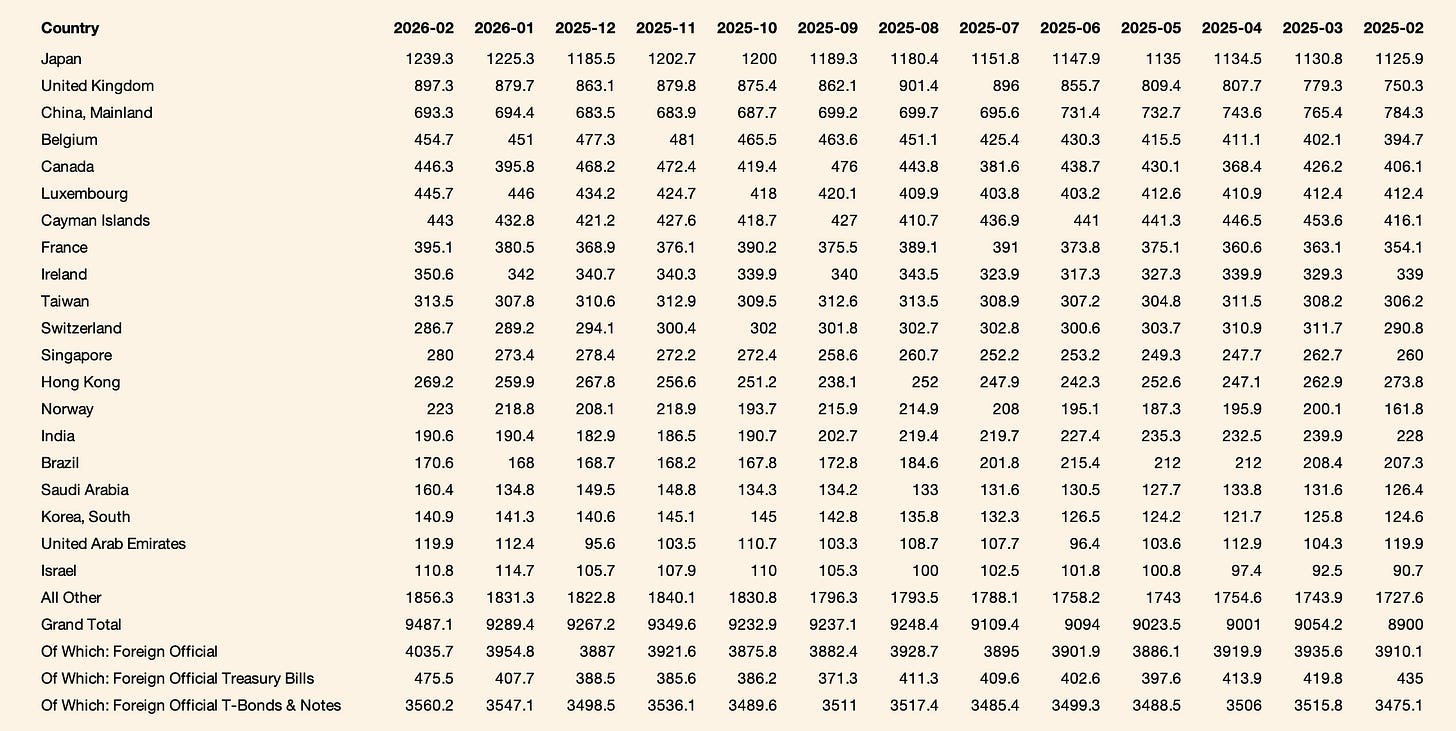

Major Foreign Holders of U.S. Treasury Securities

It is also important to distinguish headline transfer volume from actual economic payments. Much of the stablecoin debate still loses discipline at this point. A 2026 McKinsey & Company analysis, drawing on Artemis and Castle Island research, estimated bottom-up stablecoin payment volume in 2025 at about $390 billion. This included roughly $220 billion of B2B payments, $100 billion of P2P transfers, and around $30 billion of card-linked flows. These figures are meaningful, but they remain far below raw on-chain transfer volume. Banca d’Italia made a similar distinction, noting that annual stablecoin transaction volumes are often cited at around $26 trillion to $35 trillion, while real-economy usage is more plausibly estimated at about $400 billion to $1.3 trillion. It also estimated card-linked stablecoin initiatives at roughly $4.5 billion in 2025.

This is why 2025 to 2026 should be viewed as a transition period, not an end state. In the United States, the GENIUS Act created a federal payment-stablecoin framework. In Europe, MiCA became fully applicable from December 2024. Circle became a public reporting company. Visa expanded stablecoin settlement across nine blockchains. Mastercard agreed to acquire BVNK. Stripe completed its acquisition of Bridge. PayPal expanded PYUSD across its app footprint. At the same time, Europe continued to experiment with euro stablecoins and tokenised-deposit infrastructure, while remaining more sceptical than the United States about stablecoins as a monetary instrument.

The market has therefore moved beyond its first phase, when stablecoins were used mainly for exchange settlement, offshore dollar access, and crypto leverage. It is entering a second phase in which regulators, asset managers, payment networks, banks, and enterprise software companies are all trying to define what the “safe” version of a stablecoin economy should look like. That is the context in which the next decade of issuer margins, payment adoption, and regulatory structure will be decided.

Why traditional finance is adopting stablecoins

Traditional finance is interested in stablecoins for practical reasons, not ideological ones. The strongest near-term use case remains cross-border payments and treasury operations. The Federal Reserve’s March 2026 note explains why. Cross-border payments still depend on long chains of correspondents, high fixed compliance costs, FX inventory management, and the declining reach of correspondent banking. Stablecoins can reduce some of that friction by letting individuals, businesses, and smaller banks transfer a payment token directly, while larger banks remain important liquidity and compliance counterparties.

But stablecoins do not abolish payment frictions. The Fed explicitly warns that on-chain transfer costs may be low while on-ramp and off-ramp costs can remain significant. FX still has to clear somewhere. Local fiat liquidity still matters. Inventory holders still matter because recipients often do not want foreign-currency exposure. And central banks may still face balance-sheet effects depending on whether stablecoins are backed by deposits, T-bills, or reserves. Fabio Panetta added a useful empirical caution in May 2026: stablecoin-based remittance solutions show no systematic cost advantage across corridors, and in some corridors on-ramp and off-ramp costs can reach 9%.

Where stablecoins look strongest today is not broad consumer retail, but a narrower set of high-friction or always-on workflows. The 2025 payment data suggest B2B is the largest real-economy category so far. Card-linked programmes are growing, but still small in absolute terms. Visa’s own settlement pilot reached a $7 billion annualised run rate by April 2026, supported 130-plus stablecoin-linked card programmes in more than 50 countries, and now spans nine blockchains. These numbers are still modest relative to global card volumes, but they are large enough to confirm live institutional usage rather than mere experimentation.

The appeal to enterprises is easy to understand. Stablecoins offer 24/7 liquidity, programmable settlement, finality that is visible on-chain, and easier integration into multi-party workflows that do not fit banking hours. Circle highlighted enterprise treasury integrations, including Kyriba embedding USDC capabilities for corporate treasury teams. The World Economic Forum’s 2025 tokenisation report framed the same underlying mechanism more generally: shared records, programmability, flexible custody, and composability are the differentiators that can make tokenised finance operationally more efficient than the traditional fragmentation of records and messaging.

There is also a forward-looking use case that should be taken seriously, even if it remains early: machine-native and AI-agent payments. Circle’s Agent Stack and Gateway-based nanopayments are explicitly designed for gas-free, high-frequency transfers, including sub-cent transfers that would be uneconomic on conventional rails. That does not mean large AI payment volumes exist today. It does mean issuers increasingly view machine commerce and developer infrastructure as future revenue lines, especially if reserve income compresses. The important point is not the hype cycle around AI. It is the business model logic: if stablecoin margins migrate away from reserve spread, issuers need transaction, orchestration, and software revenue instead.

So the right institutional view is balanced. Stablecoins are live today in cross-border treasury flows, distributor settlement, crypto-adjacent commerce, corporate liquidity management, and card-linked experiments. They are plausible over the next three to five years in broader B2B, supplier payments, tokenised-fund settlement, and agentic payment rails. They are not yet proven as a universal retail-money layer, and the data still do not support that claim.

Reserve safety and issuer economics

The IMF’s April 2026 paper provides the best single analytical anchor for this report. Its core finding is stark: payment stablecoins can improve payment efficiency, support innovation, and expand financial inclusion, but they are vulnerable to runs. Requiring issuers to hold safe assets reduces run risk, yet doing so lowers profitability and can weaken incentives to issue stablecoins in the first place. In the IMF model, unregulated issuers choose too much risk because risky assets increase profits; a safer reserve mix is socially preferable, but it narrows the economic rationale for issuance unless other revenue streams exist.

That theoretical result is increasingly visible in market data. The Federal Reserve notes that, during 2025, stablecoins with safer and more liquid reserves saw relatively stronger adoption. It also highlights meaningful differences in reserve quality across issuers. According to the Fed’s summary of attested disclosures, USDT had roughly 1.04x reserves per coin in circulation, but only about 0.74x in what the note classifies as higher-quality reserves, namely Treasuries, Treasury-backed repo, and bank deposits. By contrast, USDC maintained full backing with higher-quality reserves. Safety, in other words, has become a competitive variable.

But safety is not free. Once reserves are confined to cash, bills, repo, deposits, money market claims, or central-bank balances, the issuer begins to resemble a regulated narrow-bank or money-market utility. At that point, the core margin is essentially a spread business with compliance attached. Circle’s results show how quickly that becomes interest-rate sensitive. The company reported $653 million of reserve income in Q1 2026, supported by higher average USDC in circulation, but also disclosed a 66 basis-point decline in the reserve return rate. Distribution, transaction, and other costs reached $407 million, with management explicitly citing higher distribution payments. That is not the economics of a pure software business. It is balance-sheet income offset by distribution and operating infrastructure costs.

Circle as the public-market case study

Circle’s Q1 2026 numbers make the structural point unusually clear. At quarter end, USDC in circulation stood at $77.0 billion. USDC on-chain transaction volume reached $21.5 trillion during the quarter. Circle generated $694 million of total revenue and reserve income, $55 million of net income from continuing operations, and $151 million of adjusted EBITDA. Other revenue, including subscription, services, and transaction revenue, reached $42 million.

Circle also disclosed $8.3 billion of annualised transaction volume for Circle Payments Network, based on trailing 30-day activity as of 31 March 2026. In April, it launched Managed Payments, allowing financial institutions to use stablecoin payments without directly managing digital assets.

These figures support two conclusions.

First, reserve income still dominates the business model. Second, Circle is already trying to reduce its dependence on reserve spread by building more of the surrounding infrastructure stack: developer tools, enterprise payments, payment-network routing, and AI-agent infrastructure.

That is also the right way to read the Arc announcement. Circle disclosed a $222 million ARC token presale at a $3 billion fully diluted network valuation, but this was not a conventional equity fundraise. The Arc whitepaper states that any ARC token would be a network coordination asset, not equity, not profit participation, not a dividend claim, and not yet a launched token. Circle is effectively trying to move beyond issuance into settlement-layer and coordination-layer infrastructure.

Tether provides the contrast. It is not a public-market issuer with the same disclosure stack, but its Q1 2026 attestation shows how profitable scale can be when reserve spread, distribution power, and more flexible market positioning combine. Tether reported approximately $1.04 billion of quarterly net profit, an $8.23 billion reserve buffer, and $141 billion of Treasury exposure. That gives Tether substantial earnings power and makes it a major conduit of offshore dollar demand into U.S. public debt.

Tether - Assets at 31 March 2026

The tradeoff is that Tether’s reserve model, disclosure style, and regulatory perimeter remain different from the post-GENIUS archetype that U.S. policymakers increasingly have in mind.

The broader conclusion is that safe-reserve stablecoins are moving away from crypto-style issuer economics and toward infrastructure economics. If reserve income compresses, winning issuers will need additional revenue lines: merchant fees, enterprise services, transaction routing, software, network fees, or data-adjacent revenue.

The IMF’s discussion of Chinese e-money payment service providers points to the same pattern. Once these entities became closer to narrow banks, merchant fees and data-related cross-subsidies became important revenue lines. Stablecoin issuers are moving in a similar direction.

Yield, adoption, and the fight for distribution

The policy logic behind stablecoin yield restrictions is straightforward. Regulators do not want payment stablecoins to become unregulated bank deposits. The BIS FSI brief notes that payment-stablecoin issuers are uniformly prohibited from remunerating balances across the main regulatory frameworks it reviews. The Federal Reserve’s March 2026 note makes the U.S. position explicit: payment stablecoins can be backed by safe assets, but issuers are prohibited from directly paying interest, even though indirect rewards are not ruled out.

That framing leaves open a large strategic question: if users cannot receive direct issuer-paid interest, where does demand migrate?

The BIS brief is useful because it separates the possible yield channels. Stablecoin-related yield can come from direct issuer remuneration, third-party rewards and loyalty schemes, exchange or CASP relending activity, margin or derivatives collateral, DeFi lending protocols, tokenised fund structures, or explicitly yield-bearing stablecoins. These channels are economically different, but from a user’s perspective they can all look like “earning on dollars.”

That means regulation may change where the yield is hosted, without eliminating the search for yield.

This is why the competition set for a non-yielding payment stablecoin is broader than bank deposits alone. It includes money-market funds, tokenised Treasury products, brokerage cash products, fintech cash balances, exchange incentive programmes, and wrappers such as sUSDS.

The ECB has made the same point indirectly. Christine Lagarde noted that tokenised money-market funds roughly doubled in market capitalisation during 2025 to around €7 billion. Franklin Templeton is a useful example. Its Franklin OnChain U.S. Government Money Fund invests at least 99.5% in U.S. government securities, cash, and Treasury-backed repo, had $824.6 million of net assets at 30 April 2026, and pays daily distributions, while explicitly warning that it is not a bank account and is not government-insured. That is not money, but it is clearly the yield leg that stablecoin users can move into.

The market is already routing around the direct-interest restriction through distribution. PayPal announced in March 2026 that PYUSD would be available in 70 markets through PayPal accounts, and it also markets PYUSD inside the app with a rewards rate for holders. Paxos, the issuer, separately emphasises that reserves are held in dollar deposits, Treasuries, and cash equivalents.

The structure matters. Reserve backing remains one layer. User-facing incentives can sit somewhere else in the stack. That is precisely the loophole-like behaviour policymakers are trying to define, and it is why the boundary between a payment instrument and an investment product will remain contested.

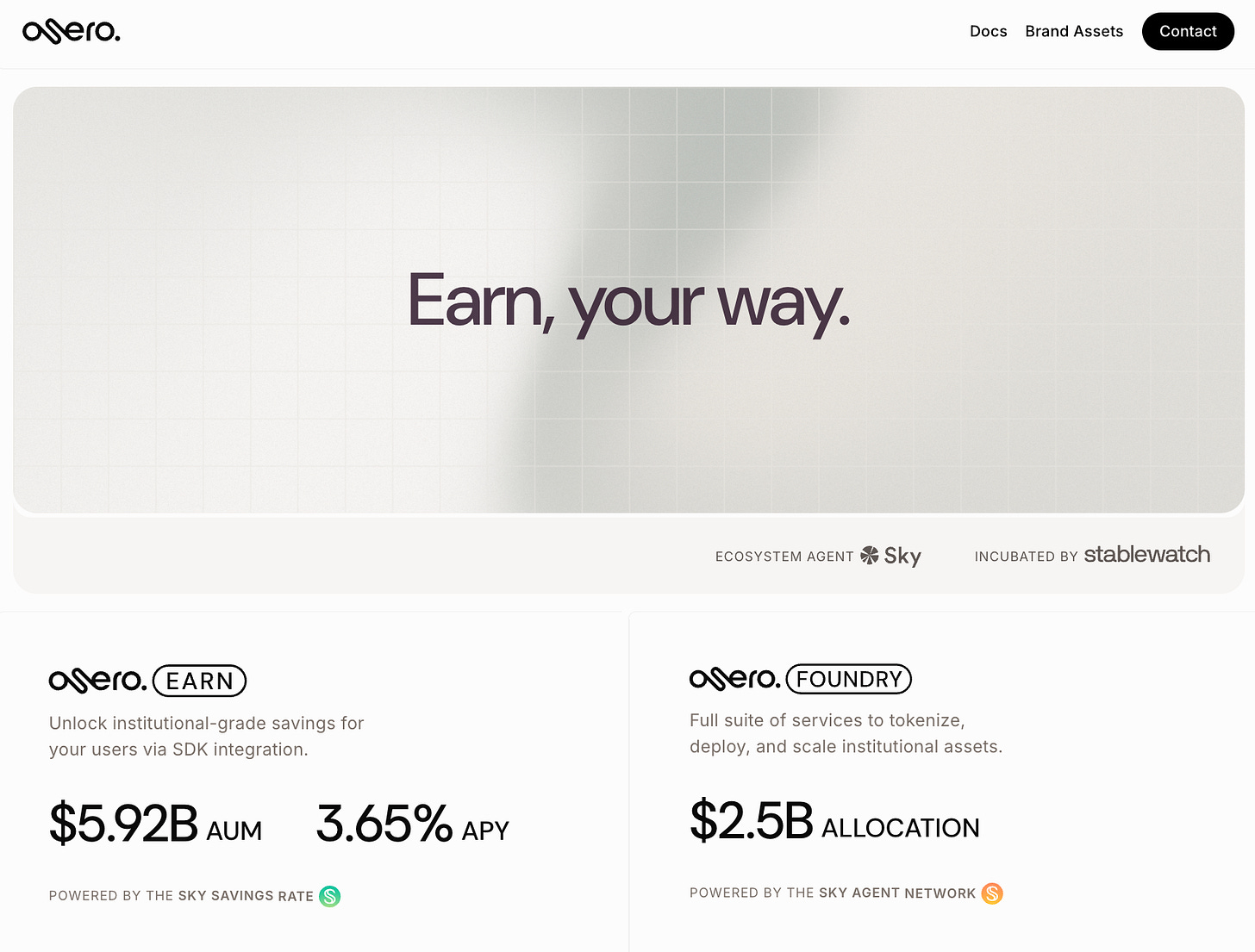

Osero and the Rise of Stablecoin Yield Infrastructure

The most interesting May 2026 case study is not only a stablecoin issuer, but a yield-distribution layer. According to Stablewatch’s incubation note, Osero raised $13.5 million in a round led by the Sky Ecosystem and co-led by Plasma.

Its product architecture is especially revealing. Osero Earn is designed for wallets, neobanks, custodians, exchanges, and similar platforms that want to embed the Sky Savings Rate without managing the asset-management layer themselves. Osero App offers a direct interface for retail and institutional users, while Osero Foundry acts as an origination layer for asset managers and structured-product issuers.

Public information on operating traction remains limited, but the product thesis is clear: if regulated payment stablecoins cannot pay yield directly, then distribution, wrapping, and embedded-yield infrastructure may become one of the most valuable control points in the market.

The underlying yield engine also matters. Sky Ecosystem’s Q1 2026 report stated that sUSDS ended the quarter at $6.49 billion, making it the largest yield-generating stablecoin by supply, while USDS supply reached $11.70 billion. Sky’s public materials position sUSDS as a variable-rate savings token rather than a payment coin. That distinction is critical. The market is already separating transactional dollars from yield-bearing dollars.

In practice, this means that rules restricting interest payments on payment stablecoins may not eliminate deposit competition. They may simply shift that competition away from issuers and toward wrappers, ecosystems, embedded-yield products, and treasury infrastructure.

For institutions trying to navigate this increasingly fragmented market, Stablewatch is useful as a market-intelligence and risk-analytics platform, not as an allocation recommendation. Its materials focus on real-time analytics across stablecoins and yield-bearing stablecoins, including APY, TVL, RWAs, vaults, and token-level risk vectors.

The emergence of specialist tooling is itself a signal. The stablecoin economy is becoming complex enough that tracking yield source, collateral quality, liquidity, legal structure, and platform risk now requires dedicated intelligence infrastructure.

Dollarisation, Spillovers, and the New Public-Debt Channel

The ECB’s working paper on private money and public debt is one of the most important recent contributions to the stablecoin debate because it reframes stablecoins as a macro-financial mechanism, not merely a payments product.

Its core claim is that dollar-backed payment stablecoins create a “global safe asset channel,” linking private money creation and global payment demand directly to U.S. public debt. When foreign users demand more dollar stablecoins, issuers buy more U.S. Treasury bills. When demand contracts, issuers sell. This can expand the global footprint of the dollar and compress U.S. risk-free yields, but it also increases cross-border spillovers and may make a more dollar-centric digital monetary system less stable at scale.

The BIS working paper on stablecoins and safe-asset prices provides market evidence for this mechanism. Using daily data from 2021 to 2025, it finds that a two-standard-deviation inflow into dollar-backed stablecoins lowers three-month Treasury bill yields by roughly 2.5 to 3.5 basis points. During periods of bill scarcity, the effect rises to around 5 to 8 basis points.

The implication is not that stablecoins dominate the Treasury bill market today. Rather, if adoption continues, stablecoin flows could become a non-trivial component of short-end public-debt demand. They may also create an additional channel through which crypto-linked and payment-linked demand affects safe-asset prices.

This helps explain why stablecoins are strategically attractive for the United States and strategically uncomfortable for others. The BIS paper on the international monetary system notes that around 98% of stablecoin value is dollar-denominated and argues that widespread use is likely to reinforce existing currency hierarchies. It also warns that digital dollarisation can create acute risks to monetary sovereignty, especially in emerging markets and developing economies facing macroeconomic instability.

Stablecoins, therefore, are not only a payments technology. They are also a private distribution channel for offshore dollars.

Europe’s response is not simply scepticism. It is an alternative architecture. Lagarde’s May 2026 speech argues that Europe should not assume a foreign private substitute will become the default settlement asset for tokenised finance. Instead, she points to tokenised deposits, interoperable euro instruments, and central-bank money as the appropriate settlement anchor.

The European Commission has taken a similar position. Its April 2026 note states that stablecoins may improve certain cross-border payments, but that tokenised deposits preserve the existing two-tier monetary system and may be better suited for treasury, liquidity management, and tokenised-securities settlement in Europe. MiCA also imposes prudential, governance, and reserve requirements on stablecoin issuers, including significant holdings with credit institutions for qualifying issuers.

The UK sits closer to the European side of this debate. The Bank of England’s proposed regime for systemic sterling stablecoins focuses on stable value, operational resilience, local backing, and UK supervision once a coin becomes systemic. Its consultation acknowledges the potential payment benefits of stablecoins, but also stresses that stablecoins and CBDCs are distinct instruments, and that systemic stablecoins require much closer prudential treatment than open crypto-market norms would imply.

The international divergence is therefore real. The United States appears more willing to use stablecoins as a way to extend dollar infrastructure globally. Europe and the UK remain more focused on monetary control, prudential supervision, and the architecture of settlement itself.

Banks, tokenised markets, and strategic implications

The major risk in the next phase is not simply “a run on a coin.” It is the combination of runs with deeper financial interdependence. The Federal Reserve’s 2026 stability note identifies three emerging vulnerabilities: complex intermediation chains, vertical integration, and deeper links with traditional finance. Its examples include wallet providers relying on third-party stablecoin infrastructure, payment processors launching issuance platforms, exchanges operating their own chains, and stablecoin issuers building proprietary infrastructure.

In plain terms, the stablecoin stack is becoming layered enough that operational shocks, liquidity shocks, and confidence shocks can move in several directions at once.

Banks matter in this transition for two reasons.

First, they can lose deposits. The ECB’s March 2026 working paper on monetary transmission describes a deposit-substitution mechanism in which stablecoin adoption shifts funds away from retail bank deposits and into digital assets. This can increase banks’ reliance on wholesale funding and, in some cases, reduce lending to the real economy.

Second, banks can respond by issuing their own tokenised forms of money. J.P. Morgan presents JPM Coin as a 1:1 bank-backed deposit token for institutional settlement around the clock, while Reuters reported in March 2026 that BMO plans a tokenised cash platform for exchange margining and treasury use.

The strategic split is becoming clearer: banks tend to prefer tokenised deposits or tokenised cash, while fintechs and crypto-native firms tend to prefer open stablecoins.

That distinction also shapes tokenised capital markets. The most plausible steady state is not winner-take-all. It is layered.

Stablecoins become the open and portable cash leg of many tokenised markets. Tokenised money market funds become the yield leg. Tokenised deposits become the bank-native leg inside regulated balance-sheet and treasury workflows. CBDCs, especially wholesale CBDCs or DLT bridges to central-bank money, become the public settlement anchor.

The WEF, IMF, ECB, European Commission, and Banca d’Italia all point toward the same architectural conclusion: tokenisation only scales safely when settlement assets, legal claims, governance, and interoperability are designed together.

The competitive map is therefore broader than “which stablecoin wins.”

On issuance, the leading players remain Circle and Tether, with PayPal and Paxos as mainstream distribution entrants, and Société Générale-FORGE and Qivalis as European bank-led responses.

On payment orchestration, Visa, Mastercard, Stripe, Bridge, and BVNK are building the fiat-connective tissue.

On the yield and RWA layer, Sky, tokenised funds, wrappers, and vault providers are competing for the “digital dollar with return” category.

On analytics and risk, tools such as Stablewatch are becoming increasingly important because collateral quality, liquidity, and yield risk can no longer be inferred from a ticker alone.

For investors and operators, the most attractive categories may sit adjacent to issuance rather than in issuance itself. These include stablecoin orchestration, compliance and wallet infrastructure, enterprise treasury tooling, on-ramp and off-ramp liquidity, accounting and reconciliation, risk intelligence, yield routing, tokenised-fund settlement, and agentic payment rails.

The hardest open questions are also becoming clearer.

Will regulation commoditise issuers? Can issuer economics survive in a lower-rate environment? Will users accept non-yielding payment coins, or will wrappers become the real adoption layer? Can stablecoins scale without amplifying Treasury-market spillovers? Will banks partner, compete, or retreat into deposit-token models? And how much of today’s volume is durable payment activity rather than exchange settlement, treasury churn, and crypto-native liquidity management?

Public data on real-economy stablecoin usage remains imperfect, especially outside card-linked flows and enterprise-reported channels.

The conclusion follows directly from the evidence. Stablecoins are entering traditional finance, but not because they are surviving as lightly regulated crypto products. They are entering because they are being transformed into regulated payment, reserve, settlement, and yield infrastructure.

The safer the reserve model becomes, the more a stablecoin issuer starts to resemble a narrow bank, a money-market utility, or a payments-network node. The more attractive the product becomes through yield, rewards, and portability, the more directly it competes with deposits, funds, and sovereign monetary systems.

The real question for the next phase is therefore not whether stablecoins survive regulation. It is what kind of financial institution a successful stablecoin issuer becomes once safety, yield, distribution, and monetary policy are all priced in.

Sources

- International Monetary Fund, Making Stablecoins Stable, April 2026.

- Federal Reserve, Stablecoins in 2025: Developments and Financial Stability Implications, April 2026.

- Federal Reserve, Payment Stablecoins and Cross-Border Payments: Benefits and Implications for Monetary Policy Implementation, March 2026.

- European Central Bank, Christine Lagarde, Stablecoins and the Future of Money: Separating Functions from Instruments, speech, 8 May 2026.

- Bank for International Settlements, Stablecoins and Safe Asset Prices, Working Paper No. 1270, revised February 2026.

- Bank for International Settlements, Stablecoin-Related Yields: Some Regulatory Approaches, FSI Brief No. 27, October 2025.

- Bank for International Settlements, The Impact of Stablecoins on the International Monetary and Financial System, BIS Papers No. 170, May 2026.

- World Economic Forum, Asset Tokenization in Financial Markets: The Next Generation of Value Exchange, May 2025.

- Circle, Circle Reports First Quarter 2026 Results, including related Arc and Agent Stack materials, May 2026.

- Tether, Tether Posts $1.04B Q1 2026 Profit, 1 May 2026.

- Stablewatch, platform materials, including Stablewatch Incubates Osero with a $13.5M Raise, May 2026.

- McKinsey & Company, Stablecoins: From Crypto Byproduct to Payments Challenger, April 2026, drawing on Artemis and Castle Island data.

- Banca d’Italia, speeches on digital money, DLT adoption, and cross-border payments, April to May 2026.

Partner Highlight

At insights4vc, we pay attention to teams that are not just shipping products, but shaping categories.

Moto is one of them. The company is building a premium card experience positioned as an alternative to traditional incumbents such as Amex, combining a high-end user interface with more modern financial infrastructure.

Moto is currently expanding access to a limited testing group. If you would like to test the product and typically spend more than $5,000 per month, please contact us at: [email protected]

Cover Artwork

The Art Gallery of Jan Gildemeester Jansz

Adriaan de Lelie c. 1794–95

Risk Disclaimer:

insights4.vc and its newsletter provide research and information for educational purposes only and should not be taken as any form of professional advice. We do not advocate for any investment actions, including buying, selling, or holding digital assets.

The content reflects only the writer’s views and not financial advice. Please conduct your own due diligence before engaging with digital assets or related technologies, as they carry high risks and values can fluctuate significantly.